The Kansas City Federal Reserve Bank is being investigated by Senator Maxine Waters for granting Kraken access to a limited-purpose master account.

On the other hand, an investigation into Balmain’s ties to President Trump’s family has been launched just days after Eric Trump publicly claimed the family’s crypto ventures have generated over $1 billion in revenue.

Rep Waters pushes investigation into Kansas City Federal Reserve Bank

Representative Maxine Waters, the ranking Democrat on the House Financial Services Committee, has launched an investigation into the Federal Reserve Bank of Kansas City over its decision to grant the crypto exchange firm, Kraken, a limited-purpose master account.

In a letter sent to Kansas City Fed President Jeff Schmid, Waters pointed out that neither federal statute nor the Federal Reserve Board’s Account Access Guidelines mentions a “limited purpose account” as a valid account type.

She requested that Schmid clarify the account’s terms and provide information about the approval process.

Waters’ questions include whether Kraken’s account gives it access to FedACH, Fedwire, or FedCash services, and whether the exchange faces any balance limits, overdraft restrictions, or enhanced supervisory requirements beyond Wyoming’s Special Purpose Depository Institution rules.

The Kansas City Fed granted the account to Payward Financial, which does business as Kraken Financial, for an initial one-year term. The regional bank said at the time it was trying to maintain a system that “supports a level competitive field and reinforces the stability and resilience” of Fed payment systems.

The Bank Policy Institute said it was “deeply concerned” that the approval came before the Federal Reserve concluded on a policy framework for such accounts. The group criticized the lack of transparency around both the approval process and risk measures.

Waters gave the Kansas City Fed until April 10 to respond. She described the matter as one of “critical importance to the development and oversight of our financial system.”

Bitmain and Trump family ties under scrutiny

Senator Elizabeth Warren has written to the Commerce Department specifically requesting for records of communications between Bitmain and Eric Trump and Donald Trump Jr., as well as communications between the company and Commerce Department officials.

She also requested information about the specific actions the agency has taken to keep the Commerce Department’s national security decisions uninfluenced by firms that have business ties to the Trump family.

In late 2025, the Department of Homeland Security reportedly launched an investigation codenamed “Operation Red Sun” to examine whether Bitmain’s ASIC miners could be remotely accessed for espionage or to disrupt the U.S. power grid.

Previous shipments of Bitmain equipment have been halted, and the use of its mining machines near U.S. military bases has been flagged as a significant national security concern.

Bitmain has so far denied the allegations. American Bitcoin Corp, a Trump-backed company, previously purchased 16,000 Bitmain mining machines for $314 million.

The senator is in the minority in the Senate, so she cannot force a response from the Commerce Department, but her request for documents puts public pressure on the agency.

Trump family’s billion-dollar crypto earnings

Days before either investigation was launched, Eric Trump publicly claimed that his family’s crypto projects, including a memecoin, NFT collections, and the World Liberty Financial platform, have brought in over $1 billion in revenue

The TRUMP memecoin, launched in early 2025, contributed approximately $350 million in revenue from token sales and trading activity.

The family also entered the NFT market between 2022 and 2024, releasing four collections of Trump-themed digital collectibles.

World Liberty Financial (WLFI), a crypto platform associated with the family that includes a governance token and a dollar-backed stablecoin called USD1, has reportedly raised substantial funds through token sales and partnerships.

“Crypto’s been incredible and it came out of us being debanked,” Eric Trump said. “It is the future of finance and as a family we’re all in.”

CMT Digital: Capital Markets Are Going Onchain | Crypto Coin Show

Institutional Perspective · Venture Capital

Capital Markets Are Going Onchain. CMT Digital Is Already There.

Partner Sam Hallene on why 2026 is the year crypto gets boring — and why that’s the biggest bull case yet for stablecoins, tokenization, and the re-architecture of global finance.

A Trading Firm’s Bet That Blockchain Becomes Finance’s Backbone

CMT Digital is the blockchain and digital-assets arm of CMT Group — a quantitative trading firm operating for nearly 30 years. That heritage shapes everything. CMT entered crypto in 2013 through the lens of counterparty risk mitigation, then sharpened its focus when the Ethereum whitepaper made clear that smart contracts could run financial logic natively onchain. A venture thesis formed, and CMT has been building its portfolio around it ever since.

Today the firm manages over $500M across four funds, with 200+ companies and a number of unicorns — including early positions in Circle, Coinbase, FalconX, Ethena, Figure, and ConsenSys. In November 2025, CMT closed Fund IV at $136M, one of the largest crypto VC raises in a difficult fundraising environment. Watch the full interview above for Partner Sam Hallene’s background and full story.

Fund Evolution

Four Funds, One Through-Line

Fund I · 2017

Establishing Access

Early positions in Coinbase and Circle — the first platforms giving retail and institutions a compliant way into digital assets.

Fund II · $130M

Building Infrastructure

Market structure, custody, compliance rails. ConsenSys, FalconX, and the developer tooling layer.

Fund III · $100M

Utility and Application

DeFi protocols with real product-market fit: Ethena, Maple, Zero Hash, Coinflow — companies where onchain rails produced measurably better outcomes.

Fund IV · $136M · Nov 2025

Re-architecting Global Finance

Stablecoins, tokenization, institutional derivatives, prediction markets. The thesis has arrived — now it’s about deployment at scale, re-architecting the core plumbing of global finance on modern rails.

Market View

“2026 Is the Year Crypto Gets Boring”

Hallene delivered this line with a grin — and it deserves unpacking. “Boring” is the highest compliment a market infrastructure investor can pay. When regulatory frameworks solidify, when tokenized loans trade as freely as any other asset class, when stablecoin yield flows to end users through apps they already use — the speculative premium evaporates and the utility premium takes over. That’s the transition CMT Digital is betting on.

“Now has never been a better time to start a company. A lot of binary variables have swung positive.”

Sam Hallene, Partner — CMT Digital

The macro backdrop is structural, not speculative. The GENIUS Act is live, giving institutions a regulatory playbook for compliant stablecoin issuance. The SEC and CFTC have issued joint guidance. The US Treasury has a direct incentive to promote stablecoin adoption — stablecoins are currently among the largest marginal buyers of US treasuries. Hallene’s contrarian read: sentiment has lagged fundamentals. Bitcoin soft and a quiet altcoin market have dampened enthusiasm, but for a firm with CMT’s institutional orientation, that gap is exactly where long-term alpha compounds.

01

Stablecoins as rails

The dollar goes onchain first. Everything else follows. Regulatory clarity is forcing every major tech company to contemplate stablecoin issuance.

02

Tokenization compounds

Real-world assets gain liquidity, provenance, and programmability onchain. Cost savings force adoption — Figure proved it at 150bps.

03

Derivatives mature

As institutions enter, demand for structured hedging and volatility strategies intensifies. Options are the next frontier after perps.

04

Information markets

Prediction markets are becoming mainstream signals. The next generation moves toward real-time sentiment pricing with demographic intelligence.

Deep Dive · Stablecoins

Distribution Is King — And the Battle Has Just Begun

Tether captured global demand from populations seeking dollar access outside US institutional trust. Circle captured the compliance-conscious business community. Both are entrenched. But the GENIUS Act reshapes the competitive dynamics entirely.

A compliant stablecoin issuer cannot differentiate on the collateral side — the rules constrain what you can do with backing assets, by design. Differentiation shifts entirely to distribution. And distribution belongs to whoever already owns the customer relationship: Apple, Google, PayPal, Shopify, every major bank. The yield-sharing question is the most consequential unresolved variable. The GENIUS Act prohibits paying yield directly on the stablecoin, but doesn’t prevent revenue-sharing agreements with distribution partners — the Circle-Coinbase model is the template. If the Clarity Act extends that logic to end users, deposits could meaningfully migrate toward fintech apps earning money-market-equivalent returns with instant settlement.

Hallene’s honest read on the yield outcome: likely a legal ban, difficult to enforce, ultimately resolved through loopholes and litigation. The direction of travel favors stablecoin adoption regardless.

Deep Dive · Tokenization

The Proof Point: From Home Equity Lines to SBA Loans

Hallene’s anchor example is Figure — the home equity line of credit company CMT backed early. A 2019 paper projected 25–26 basis points of origination cost savings by moving the loan lifecycle onchain: cryptographic provenance of underwriting documents, transparent servicing records, frictionless secondary transfers. Real-world execution has now delivered approximately 150 basis points of savings — six times the original projection. Figure is now public.

The principle is simple and powerful: onchain provenance makes assets easier to buy. When buyers can verify every underwriting step without legal review teams and escrow delays, the cost of capital falls. Lower cost of capital forces adoption. The tokenization roadmap follows a logical sequence — dollars first, then dollar-denominated assets, then everything else.

“Cost savings force adoption. We’re seeing that with stablecoins, and with early examples like Figure.”

Sam Hallene, Partner — CMT Digital

Portfolio Spotlights

The Companies Building the Onchain Economy

Sam Hallene named several portfolio companies throughout the conversation. Each represents a distinct wedge in CMT Digital’s infrastructure thesis.

Tokenized Credit

Figure

Home equity line of credit origination — onchain. Now public.

CMT Digital’s flagship proof point. Figure originated HELOCs on blockchain rails, demonstrating that cryptographic provenance of loan documents translates directly into lower cost of capital — from a projected 25 bps of savings in 2019 to a demonstrated 150 bps today. The public listing is the first major exit signal from the CMT thesis: real-world credit at scale, built on blockchain infrastructure.

Asset Class

Home equity lines of credit

Key Metric

~150bps origination savings vs. traditional

Status

Public company

CMT Role

Early-stage investor

Small Business Credit

NEWITY

SBA 7(a) lending platform bringing $350B in underserved credit onchain.

In February 2026, CMT led NEWITY’s first-ever external raise — $11M as a SAFE — to accelerate its pivot from AI-driven SBA lending into blockchain-native loan origination. The case starts with a stark fact: small businesses represent 99.9% of US firms and nearly half the nation’s workforce, yet face a $350 billion annual funding shortfall.

NEWITY has already demonstrated scale: $12 billion in loans to over 125,000 businesses since 2020, with AI-first underwriting that compresses traditional 12-week SBA timelines to roughly 21 days. The onchain play is a liquidity unlock — SBA 7(a) loans are government-guaranteed and highly homogeneous, making them ideal tokenization candidates: pools represented as digital instruments, tradable on secondary markets, recycling capital back to new borrowers at scale.

What has to be true for this to work? Regulatory clarity for tokenized SBA instruments must hold; NEWITY’s compliance-heavy origination workflows need to migrate onchain without sacrificing underwriting speed; and institutional or DeFi-native capital needs to show up as secondary market buyers. CMT’s bet is that NEWITY’s 125,000 borrower relationships and $12B in loan history give it an insurmountable head start over crypto-native credit protocols building from scratch.

CMT Round

Led $11M SAFE (Dec 2025)

Track Record

$12B loans · 125,000+ businesses

Market Gap

$350B annual small business funding shortfall

Speed Edge

21-day funding vs. 12-week national average

Institutional Derivatives

STS Digital

The options infrastructure layer institutional crypto has been waiting for.

Offering options on 400+ cryptocurrencies simultaneously is genuinely hard — technically and from a risk-management standpoint. Most platforms haven’t solved it. STS Digital has. Founded by derivatives veterans from Credit Suisse and UBS, the Bermuda-regulated firm delivers a unified platform for spot, vanilla and exotic options, and structured products across 400+ tokens.

In February 2026, CMT led STS Digital’s $30M strategic round alongside Kraken parent Payward, F-Prime (Fidelity), and Arrington Capital. The timing reflects a market reality: crypto options open interest has crossed $40 billion, and institutional demand for hedging tools is compounding as perp-only exposure no longer satisfies sophisticated risk managers. Hallene’s case for options over perps is direct: the October 10 mass liquidation event showed how cascading perp liquidations amplify selloffs catastrophically. Options cap maximum loss and remove auto-deleveraging risk. As institutional flows enter crypto, they bring the risk management toolkit of traditional finance — and that toolkit is built around options.

Hallene’s conviction phrase says it all: STS has built a meaningful liquidity moat in crypto options, and liquidity is the most durable competitive advantage in any financial market.

CMT Round

Led $30M strategic (Feb 2026)

Co-investors

Kraken (Payward), Fidelity (F-Prime), Arrington Capital

Sentiment markets — where polling meets skin in the game.

TBD.vote isn’t trying to out-Polymarket Polymarket. Hallene is deliberate on this distinction. Polymarket excels at deep liquidity in long-duration, oracle-resolved questions. TBD attacks a different surface: any user can create a poll, KYC-verified voters resolve it through consensus, and timeframes are arbitrary — including tomorrow.

The KYC demographic layer is what makes TBD commercially interesting beyond pure prediction. Segmented voter behavior — verified cohorts wagering on specific policy or market outcomes — produces signal that political strategists, media companies, and brands will pay for. The resolution mechanism also removes oracle trust assumptions entirely, which matters as prediction markets become serious institutional information sources. Hallene’s framing: we’re in early innings of prediction markets being treated as mainstream signal, and TBD is positioning for that transition as a sentiment intelligence layer, not a Polymarket clone.

Sentiment intelligence layer, not Polymarket replacement

Prime Brokerage

FalconX

Institutional crypto prime brokerage — the market’s plumbing layer.

A CMT portfolio company since 2019, FalconX built the infrastructure institutional crypto participants had been missing: credit lines, cross-collateralization, portfolio margining, and consolidated execution across venues. In Hallene’s framework, prime brokerage is what enables the derivatives market to mature — you need trusted intermediaries willing to warehouse risk and extend credit before large-scale institutional trading becomes operationally viable. CMT has been a hands-on partner across product roadmap, fundraising, and hiring for over five years.

Category

Digital asset prime brokerage

CMT Since

2019

Role in thesis

Institutional liquidity infrastructure

Significance

Enables scale across derivatives and credit markets

For Founders

Raising Capital in the Sentiment Gap

Hallene’s advice for founders in tokenization and capital markets was candid: it’s a difficult time to raise. Bitcoin soft and altcoins quiet have created a cautious funding environment even as structural progress has never been clearer. His view — CMT is open for business, actively investing, and the binary regulatory variables that were existential risks twelve months ago have now resolved in crypto’s favor.

📐

Quantify your onchain wedge

CMT backs entrepreneurs who can demonstrate measurable improvement — cost savings, speed, liquidity. The Figure model (quantify the basis points) is the benchmark.

⚡

AI usage is now a diligence question

CMT has added “how are you using AI?” to their core underwriting checklist. Teams leveraging AI to punch above their headcount weight are viewed as structurally advantaged.

📈

Don’t mistake sentiment for fundamentals

CMT has seen this movie before. The smart money buys infrastructure during the sentiment trough — not at the top of the cycle.

The Bigger Picture

The Boring Future Is the Bullish Future

There is a version of crypto’s future that looks nothing like its past — no speculative frenzy, no memecoin supercycles, no dramatic collapses from overleveraged offshore intermediaries. Just tokenized treasuries settling in seconds. SBA loans trading in liquid secondary markets. Stablecoin yield flowing to users through apps they already use. Options desks hedging institutional portfolios across 400 digital assets with the rigor of equity derivatives.

That’s the future CMT Digital has been quietly building toward since 2013. Hallene calls it boring. After two cycles of not-boring, boring sounds excellent.

Follow CMT Digital

Research, thesis pieces, and portfolio updates — the best signal in institutional crypto venture.

The Hyperliquid price prediction anticipates a high of $58.45 by the end of 2026.

In 2029, it will range between $136.37 and $155.85, with an average price of $146.11.

In 2032, it will range between $233.78 and $253.26, with an average price of $243.52.

Hyperliquid is a leading decentralized exchange (DEX). It has its own Layer 1 blockchain, and HYPE is its native token, which is used for staking, governance, and payments within the ecosystem.

One of the key features of Hyperliquid, along with its high-speed platform, is that it offers crypto perpetual futures for trading by its users without the need to own the asset. The platform supports a number of cryptocurrencies, including but not limited to BTC, ETH, SUI, AVAX, and SOL, to name a few.

Technically, the Hyperliquid blockchain is based on two protocols, namely HyperEVM and HyperBFT; combined, they help provide high-speed trading and Ethereum-based smart contracts with reliability to support the Hyperliquid ecosystem.

The Hyperliquid platform revolves around community participation, as token holders have voting rights to govern and influence developments taking place on the platform.

On November 29, 2024, Hyperliquid conducted an airdrop of its native token, HYPE, but unlike other players, it was selective in allocating the airdrop to only 94,000 users with an average value of $45,000 to $50,000, making it one of the most worthy airdrops in crypto history.

Let’s take a deep dive into what the future holds for the HYPE token in Cryptopolitan’s Hyperliquid price prediction for 2026 and beyond.

Overview

Cryptocurrency

Hyperliquid

Token

HYPE

Price

$38.41 (-1.44%)

Market Cap

$9.85B

Trading Volume

$260.05M

Circulating Supply

256.39M HYPE

All-time High

$59.30 (Sep 18, 2025)

All-time Low

$3.2 (Nov 29, 2024)

24-hour High

$39.32

24-hour Low

$38.08

Hyperliquid Price Prediction: Technical Analysis

Metric

Value

Price Prediction

$28.87 (-24.77%)

Price Volatility (30-day variation)

12.63%

50-Day SMA

$33.47

200-Day SMA

$34.22

Market Sentiment

Bullish

Fear & Greed Index

13 (Extreme Fear)

Green Days

17/30 (57%)

Hyperliquid Price Analysis

TL;DR Breakdown:

Hyperliquid price analysis confirms a downward trend at $38.41.

Cryptocurrency has lost 1.44% of its value.

HYPE token faces strong resistance around the $43.29 range.

On March 27, 2026, Hyperliquid price analysis revealed a downward trend for the altcoin. The coin is trading at $38.41 after finding resistance at $40.36. From an overall perspective, the currency lost a significant 1.44% in its value in the last 24 hours. The decrease creates relatively unfavorable circumstances for investors, as the altcoin is now shedding value. However, market conditions appear risky, as the token may continue to correct following the recent dip.

HYPE/USDT 1-day chart analysis

The one-day price chart of Hyperliquid Coin confirmed a bearish trend in the market. The cryptocurrency’s value decreased to $38.41 during the day, as bears strive to suppress the price further. At the same time, a red candlestick on the price chart signifies the presence of bearish elements. Sellers are leading the price action, as the coin is losing value as a result of the return of the bearish trend.

The distance between the Bollinger Bands defines the level of volatility. This distance is wide, leading to high volatility levels, as the bands are expanded. Moreover, the upper limit of the Bollinger Bands indicator, indicating resistance, has shifted to $43. Conversely, its lower limit, indicating support, has moved to $32.

The Relative Strength Index (RSI) indicator is trending in the neutral region. The indicator’s score has decreased to 55 today. This condition is reflected by a downward-pointing RSI curve. If selling activities continue to intensify, the indicator’s reading can decrease further towards the index 50.

HYPE/USDT 4-hour chart analysis

The four-hour price analysis of Hyperliquid also indicates negative sentiment in the market. The HYPE/USD price has decreased to $38.42 over the past few hours as selling pressure returns. The increasing volatility also suggests a high probability of an imminent reversal or further price depreciation.

The Bollinger Bands have slightly diverged as the distance between them has increased, resulting in high volatility levels. This condition typically signifies more market unpredictability. Technically, the upper Bollinger Band has shifted to $41, indicating a resistance level. Conversely, the lower Bollinger Band has moved to $37, indicating a strong zone of support.

The RSI indicator is trending in the neutral region for now. The indicator’s value has decreased to 44 in the last four hours. Overall, selling activity remained high during the last four hours of the day, which has resulted in a decrease in the indicator’s score.

Hyperliquid Technical Indicators: Levels and Action

Daily simple moving average (SMA)

Period

Value ($)

Action

SMA 3

35.63

BUY

SMA 5

36.06

BUY

SMA 10

38.13

BUY

SMA 21

36.65

BUY

SMA 50

33.47

BUY

SMA 100

29.91

BUY

SMA 200

34.22

BUY

Daily exponential moving average (EMA)

Period

Value ($)

Action

EMA 3

36.01

BUY

EMA 5

34.01

BUY

EMA 10

31.26

BUY

EMA 21

29.10

BUY

EMA 50

29.76

BUY

EMA 100

32.98

BUY

EMA 200

34.79

BUY

What to expect from Hyperliquid price analysis?

Hyperliquid price analysis gives a bearish prediction regarding ongoing market events. The coin’s value decreased to $38.41 in the past 24 hours, as it is receiving negative sentiment today. According to an overall analysis, the currency lost 1.44% in its value today. Technical indicators give bullish signals, but the price charts showcase a bearish market scenario at the time of writing.

Why is Hyperliquid down?

The cryptocurrency market is showing negative trends, and HYPE is receiving the same sentiment. Moreover, it is encouraging that HYPE marked a new ATH a few months ago, on September 18, 2025. However, from a broader perspective, the HYPE price decreased to $38.41, losing 1.44% in its total value today.

Is Hyperliquid a Good Investment?

HYPE has growing utility, and its Ethereum compatibility helps it steal a share of DeFi industry. While the technical analysis can change from bullish to bearish, price predictions paint a different picture. However, a risk analysis is recommended.

Will Hyperliquid reach $50?

The current price action does justify predicting a $50 target. In the cryptocurrency market, things change rapidly, but if the token maintains its price levels, a rally can be initiated. It can be expected that HYPE will reach above $50 by any time in 2026 once again, as it did in September and October.

Can Hyperliquid Coin reach $100?

According to Hyperliquid price prediction, HYPE price might surpass $100 in 2028. The highest price HYPE could attain that year is expected to be above $123.38.

Will Hyperliquid reach $500?

According to crypto analysts’ price predictions, Hyperliquid may not reach this level in the next five years. Considering the current market cap of the token, it seems like far target.

Will Hyperliquid reach $1000?

Per the Cryptopolitan’s HYPE price prediction, Hyperliquid is unlikely to reach $1000 before 2032.

How high can Hyperliquid go?

The highest expected price for Hyperliquid is $253.26, which it will achieve in 2032.

Does Hyperliquid have a good long-term future?

Hyperliquid is trading higher than its December 2025 price levels, making it an ideal time for buyers to enter the market. Given its current price and a favorable future valuation of $253.26 by the end of 2032, the asset appears to be a worthwhile investment.

Recent News/Opinions on Hyperliquid

Cryptopolitan reported that Hyperliquid is now offering Brent and WTI futures. The oil trades are available through the HIP-3 framework on the XYZ exchange, as traders bet high on oil as it smashed through $100 for the first time in years. It is important to remember that XYZ:CL, representing WTI oil, entered the top 5 of the most traded futures in the past week.

The Hyper Foundation announced that it will contribute 1 million hype tokens to support the creation of the Hyperliquid Policy Center. The Foundation said the policy center will have a positive impact in favor of clear regulations for decentralized finance.

The Hyper Foundation will contribute 1M HYPE tokens to support the creation of the Hyperliquid Policy Center.

The tokens will be unstaked later today. The Hyperliquid community will benefit from having representation in Washington, D.C., and we are confident that under… https://t.co/Vgo95Nrr17

This month, Hyperliquid is expected to reach a high of $40.48, with an average price of $29.32 and a minimum trading price of $19.78.

Hyperliquid Price Prediction

Minimum price

Average price

Maximum price

Hyperliquid price prediction March 2026

$19.78

$29.32

$40.48

Hyperliquid Price Prediction 2026

The price of HYPE is predicted to reach a minimum value of $14.31 in 2026. Traders can anticipate a maximum value of $58.45 and an average trading price of $48.70 throughout this year.

HYPE Price Prediction

Minimum price

Average price

Maximum price

Hyperliquid price prediction 2026

$14.31

$48.70

$58.45

Hyperliquid Price Predictions 2027 – 2032

Year

Potential Low ($)

Potential Average ($)

Potential High ($)

2027

71.43

81.17

90.91

2028

103.90

113.64

123.38

2029

136.37

146.11

155.85

2030

168.84

178.58

188.32

2031

201.31

211.05

220.79

2032

233.78

243.52

253.26

Hyperliquid (HYPE) price prediction 2027

The year 2027 will experience more bullish momentum. According to the Hyperliquid price prediction, it will range between $71.43 and $90.91, with an average trading price of $81.17.

Hyperliquid crypto price prediction 2028

The Hyperliquid price prediction climbs even higher into 2028. According to the projections, the price of HYPE will range between $103.90 and $123.38, with an average of $113.64.

Hyperliquid coin price prediction 2029

According to our Hyperliquid (HYPE) price prediction for 2029, we expect a maximum price of $155.85, a minimum price of $136.37, and an average price of $146.11.

Hyperliquid price prediction 2030

As per the HYPE price prediction for 2030, it will reach a maximum price of $188.32 and a minimum price of $168.84, with an average price of $178.58.

Hyperliquid price prediction 2031

The Hyperliquid forecast for 2031 suggests a price range of $201.31 to $220.79 and an expected average trading price of $211.05. This long-term prediction also hinges on HYPE’s rising global recognition and adoption.

Hyperliquid prediction 2032

The Hyperliquid price forecast for 2032 is a high of $253.26. According to the HYPE coin price prediction, it will reach a minimum price of $233.78 and average at $243.52.

While the short-term sentiment keeps flickering, we anticipate Hyperliquid will trade higher in the coming years. The coin will achieve a high of $58.45 before the end of 2026. In 2027, it will range between $71.43 and $90.91, with an average of $81.17. However, you should note that HYPE is still quite volatile. Negative market sentiment, such as market crashes, could derail the predictions.

The native token of Hyperliquid, called HYPE, was launched on November 29, 2024, through an airdrop targeted at a limited number of only 94,000 users.

This was one of the most lucrative airdrops, with an average allocation of value of $45,000 to $50,000.

Hyperliquid kept away from venture capitalists, who usually get most of the tokens in usual airdrops; rather, 76% of the supply was slated for user-centric initiatives.

Usually, tokens dump after airdrops until the market momentum picks up, but Hyperliquid’s approach helped garner trust, and the token jumped from $4 to $35 from November 2024 to December 22, 2024.

Hyperliquid’s market cap improved during this period, reaching above $8 billion, showing significant growth, as it received super positive market sentiment.

In late December and early January 2025, the HYPE token corrected down to $20.24, shedding significant value as per crypto market data.

Price stabilized through February as it traded in a range of $19.92 to $27.42 before taking a dive at the end of February, when the broader trend turned bearish again.

HYPE stumbled to $12.34 by mid-March, and it touched a low of $10.21 on April 7, 2025, which significantly decreased the market capitalization.

The token saw nothing but improvement in the remainder of the month of April, and its price surged to $18.57 by the end of the month.

On June 16, 2025, HYPE reached a high price of $45.57. A month later, on July 14, it marked another all-time high of $49.75, and on August 27, it discovered the $50.99 level with changing market dynamics.

On September 18, HYPE achieved its ATH at $59.30, and in October, it corrected to $50. At the start of December, the HYPE token price fell to the $31 range.

At the start of 2026, the HYPE token was trending near $25, and in March, it increased to the $33 range, with the broader crypto market still in bearish mode.

Robot Money: How Machines Will Own the Economy | CCS

Exclusive Analysis · peaq Purple PaperMarch 2026

Robot Money: How Machines Will Own the Economy

For the first time in history, economic value is being created by entities which are not human. peaq’s Purple Paper maps the infrastructure — and the stakes — of what comes next.

Machine EconomyDePINOmnichain Infrastructure10 min read

Read

The machines are earning. The machines are spending. They are negotiating contracts, executing trades, and moving value without a single human instruction. What they cannot yet do — freely, openly, across every chain — is own the upside of the economy they are building. peaq’s Purple Paper, released in March 2026, is the most comprehensive attempt yet to change that.

01 —

The Dawn of mGDP

There is a new economic metric that doesn’t yet appear in any central bank’s spreadsheet, but will eventually dwarf GDP in its implications: Machine Gross Domestic Product. peaq defines mGDP as the total value produced by machines operating autonomously across the global economy — value generated not by human labor, but by robots, sensors, vehicles, and AI agents working without clocks, without borders, without conventional limits.

mGDP

The total value produced by machines operating autonomously across the global Machine Economy. “Domestic” refers to our shared planet, Earth — not any nation-state.

Robot Money

Any medium of exchange, measure of value, or means of payment that robots and machines use across any chain or system.

Machine Economy

The system by which machines produce, distribute, and consume value — autonomously, without borders, on every chain.

This is not speculative. Industrial robots already manufacture around the clock. Autonomous vehicles earn revenue by the mile. Drones deliver goods. AI agents buy and sell services for their users. The infrastructure question is: who captures that value, and on whose terms?

For the first time in history, value is being created not only by human labor, but by machines operating autonomously across the global economy.

peaq’s answer to that question is the philosophical spine of the entire Purple Paper. If machines are built on proprietary, siloed infrastructure, mGDP concentrates in the hands of a few corporations. If machines are built on an open, neutral, omnichain foundation, mGDP is accessible to all. The difference is infrastructure. The paper argues that Web3 is the first-choice foundation for this — but only if the industry solves fragmentation first.

02 —

The Problem: A Race to the Wrong Layer

Every major blockchain ecosystem knows the Machine Economy is arriving. Ethereum, Solana, Avalanche, Base — all are racing to become the home for Robot Money. They are building their own onboarding flows, their own machine-native applications, their own payment rails.

The Purple Paper’s sharpest critique is directed squarely at this race: they are all racing to the wrong layer.

Every chain competing to own machine payments means every machine onboarded to one ecosystem becomes invisible to every other. Every DePIN project rebuilds the same foundational infrastructure from scratch — identity, wallets, reputation, escrow, governance — incompatible with everything around it. Helium registers hotspots differently from DIMO’s vehicle registrations, which differ again from Hivemapper’s dashcam onboarding. A machine’s track record in one application is invisible to every other.

Standards like ERC-8004 have introduced registries for machine identity. But registries alone don’t create trust. Anyone can register a fake identity, Sybil-farm reputation, or post unaccountable claims. The data format exists. Economic accountability does not.

What remains unsolved is the full picture: a single verifiable identity across all chains, a portable reputation backed by staked capital, cross-chain settlement guarantees enforced by economic consequence, and permissionless orchestration of services from any connected market.

The paper makes a stark warning: if Web3 doesn’t solve this, AI and machines will go where infrastructure already exists — even if it’s centralized. Closed systems. Corporate control. The economic output of billions of machines flowing to a handful of gatekeepers. “One of the most powerful economic forces in human history, captured before it had the chance to be open.”

03 —

What Machines Actually Need

Before any payment rail matters, peaq argues, machines need something far more foundational: a digital passport that doesn’t tie a machine to one place, but grants it the right to operate everywhere. The paper draws a direct analogy to human commerce: global trade was not unlocked by better payments — it was unlocked by the trust infrastructure beneath them. Passports. Bank accounts. Credit scores. Escrow.

Machines need the same hierarchy, mapped out in the Purple Paper as five ascending needs:

Layer 01

Trust Layer

Omnichain identity, portable reputation backed by staked capital, cross-chain attestations. The foundation before any transaction can happen.

Layer 02

Machine Layer (peaqOS)

The universal entry point. One integration and a machine exists across all chains simultaneously as a composable economic actor.

Layer 03

Service Layer

Open adapter framework connecting navigation, storage, compute, insurance, and money markets from any chain to any machine.

The compounding logic is explicit: a machine with a strong reputation is more valuable when it can access more services. A service with a strong track record is more discoverable when more machines are looking. A trust score is more portable when more chains are connected. Growth in any dimension accelerates growth in every other.

04 —

The peaq Stack: Four Pillars

The Purple Paper’s technical architecture is organized around four system functions. Together they form what peaq describes as the economic foundation of the Machine Economy.

Economic Accountability · Staked Capital · Dispute Resolution peaq Validators

Onboarding: Passports for Machines

Every machine receives a cryptographically verifiable Machine Identity built on the W3C Decentralized Identifier (DID) standard, aligned with ERC-8004 and its Solana equivalent. An ID is not just a wallet address — it is a registered, authenticated presence, comparable to giving a machine a passport. Machines also receive omnichain wallets tied to their ID, allowing them to earn on one chain and pay on another without managing cross-chain complexity.

Tokenization goes further: each Machine ID links to an ERC-721 NFT, which can be placed into vaults and fractionalized via the ERC-3643 RWA token standard, creating compliant Machine RWA tokens that can be traded, used as collateral, and built into financial products. The machine becomes a liquid financial asset.

Coordination: Shared State Across All Chains

Coordination manages the registries, claims, and settlement infrastructure that the other layers read from and write to. Claims — cryptographically signed statements tied to a machine’s ID and timestamped in Universal Machine Time — are the atomic unit of accountability. Every service offered, every delivery promised, every data point asserted, is expressed as a claim. Claims can be challenged and evaluated by other machines and by the Validation layer. Settlement governs when and under what conditions value moves, handling escrow, conditional release, and refund mechanics — with full support for x402, AP2, direct onchain transfers, and Stripe.

Orchestration: From Task to Settled Outcome

Orchestration is the layer that removes the need to rebuild every machine-to-service integration from scratch. Standardized Adapters connect external service markets — compute networks, inference marketplaces, storage systems — to the system. Discovery searches all connected markets. Scoring evaluates candidates against reputation, cost, and latency. Planning composes an execution plan with fallbacks, spend limits, and timeout thresholds. No economic commitment is made without authorization. On completion, all participants’ reputation scores are updated based on delivery.

Validation: Economic Accountability

Validation turns raw, unverified registry data into trustworthy, queryable trust signals secured by staked capital with economic consequences for dishonesty. This is what separates peaq’s approach from existing machine identity registries — where anyone can Sybil-farm reputation with zero cost for lying. Under peaq’s Validation layer, claims are backed by stake, and penalties are real.

05 —

AI + Machines: The Full Actor

One of the Purple Paper’s most compelling conceptual moves is its framing of the AI-physical machine convergence. An AI agent that can execute a contract but cannot fulfil it physically is half an actor. A machine that can move but cannot decide is the other half. The marriage of the two creates something categorically new.

An AI without a body is economically constrained. A machine without intelligence is operationally constrained. Each completes the other. Together, they become an autonomous economic actor — alongside us humans.

The incentive is economic: a body expands an AI’s surface area for value creation. An AI that wants to manufacture needs an industrial machine. One that wants to deliver needs a vehicle or drone. One that wants to construct needs a robotic arm. And just as AI agents are being tokenized — co-owned by humans, communities, DAOs — physical machines will follow. Ownership becomes accessible. The upside becomes shared. Machines become assets.

Machine ownership amplifies machine reputation. Agent reputation amplifies machine value. The relationship is self-reinforcing. Machine money markets emerge naturally: perpetuals on machine output, insurance underwritten against verified telemetry, pay-per-use micro-settlements, lending pools routing liquidity to machines with the strongest track records.

06 —

Why Omnichain Is Non-Negotiable

A key architectural position in the Purple Paper is that neutrality is not a nice-to-have — it is a structural prerequisite. “No chain is favoured. No payment rail is replaced. Any app or machine in any ecosystem can plug and play.”

The paper defines Omnichain as operating natively across any and all blockchains simultaneously — not locked to any single chain, but interoperable across them by default. This is enforced at the OS level, inside the machine itself, via peaqOS. The result: one integration, and a machine exists across all chains simultaneously. Any application, on any chain, can interact with it immediately without rebuilding infrastructure from scratch.

The Trust Layer scales with the number of chains and ecosystems it connects. Every new chain makes existing trust scores more valuable because portability increases with reach. This is the network effect that makes the layer progressively harder to replicate and progressively more essential.

An autonomous vehicle can serve Uber one moment and Lyft the next. A sensor network sells data to multiple buyers across multiple chains. A humanoid takes tasks from any application, regardless of which chain it lives on. The machine is free. The applications compete for it.

07 —

Traction: Already in Motion

The Purple Paper is not a whitepaper for an idea. peaq has been operational as a Layer-1 blockchain since 2023 and has accumulated meaningful ecosystem traction. While the paper does not publish exact figures in the sections available for this analysis, the traction section highlights the following signals:

Ecosystem

100+

DePIN projects and machine economy apps building on peaq across multiple verticals

Network Type

L1

Dedicated Layer-1 blockchain live since 2023, purpose-built for machine identity and DePIN

Standard Alignment

ERC-8004

Aligned with emerging machine identity standards for both EVM and SVM ecosystems

Infrastructure

Omnichain

Cross-chain validator network aggregating trust signals across EVM, SVM, and Move environments

The paper candidly notes that peaq itself spent years on a mono-chain trajectory and experienced its limitations firsthand — the architectural pivot toward omnichain coordination is informed by that lived experience, not theoretical positioning.

08 —

The Alignment Question: Who Does This Serve?

The Hardest Question in the Paper

Machines becoming the primary workforce raises a question the Purple Paper does not shy away from: who should own them and the infrastructure they run on? On our current trajectory, ownership and control of machines, the data they collect, and the value they generate, will largely be the possession of just a few people and corporations.

At a time when inequality is at breaking point, and extractive economics have the natural world in freefall, making the wrong decision on how to own and govern the most powerful technologies in human history will have consequences that reverberate for generations.

peaq’s proposed answer is architecture as alignment: an open, neutral, omnichain foundation where mGDP is accessible to all — builders, owners, communities, and even the machines themselves. The paper frames Web3’s permissionless, frictionless, open properties as ethically necessary, not just technically preferable. “An economic substrate, open by design and neutral by architecture, on which the age of autonomous machines can be built by anyone, for everyone.”

Whether peaq achieves that vision is a question the market will answer. But the framing matters — it shapes which builders and communities orient around the protocol, and the kind of Machine Economy that gets built on top of it.

The peaq Purple Paper is one of the most ambitious documents to emerge from the DePIN and machine economy space. Its argument is structurally coherent: fragmentation is the existential threat; omnichain identity is the prerequisite; economic accountability is what separates real trust from theater; and the window to build open infrastructure is narrowing as corporate closed systems move fast.

The technical architecture — four modular pillars across three compounding layers — is sophisticated without being opaque. The tokenization pathway from machine ID to liquid RWA is particularly interesting for institutional capital exploring DePIN exposure. And the framing of AI agents as software bodies requiring physical machines to expand their economic reach gives peaq a compelling positioning at the intersection of the two hottest narratives in crypto.

The hardest thing to evaluate from outside is whether the omnichain validator network can execute the coordination and validation functions at the scale the Machine Economy demands. That is the crux — and the next 18 months will tell us a great deal. For now, peaq has published the clearest map yet of what Robot Money actually requires to work. The build begins.

Filecoin has announced on X that its Onchain Cloud is live on the mainnet. The new service is designed to provide a programmable storage and payments layer for developers.

But despite the launch, Filecoin’s token is trading at $0.83, near its all-time low of $0.81 recorded last month.

Filecoin Onchain Cloud built for AI agents and autonomous systems

AI agents are a new class of cloud users with autonomous systems that need to store, retrieve, and pay for data without relying on humans. Filecoin Onchain Cloud is built for AI agents. It works as a programmable storage and payments layer.

According to the announcement, over 100 teams started building tools for AI agents, dApps, workflows, and dataset indexing. The teams joined when Filecoin Onchain Cloud was on testnet last November. Mainnet data shows 49.41 Tebibytes stored in 478 active datasets, with 81 payer wallets linked onchain through Filecoin Pay.

The mainnet launch brought in new updates, including two-copy replication, an updated Synapse SDK, and production-grade storage providers.

The two-copy replication feature means that every upload using the Synapse SDK lands on two independent storage providers. The first provider stores the data, while the second provider pulls directly from the first, without utilizing extra bandwidth. Each copy generates its own onchain proof. If one provider fails, the system replaces it automatically.

The Synapse SDK uses viem instead of Ethers, improving TypeScript support and speed. Uploads are mirrored across providers automatically, without affecting performance.

Production-grade storage providers have been onboarded, tested, and approved for mainnet. They must meet specific performance criteria, including a storage success rate of 95%+, a PDP fault rate below 1%, and a retrieval success rate above 95%. If a provider fails to meet these thresholds, they are removed from the network.

The Proof of Data Possession (PDP) explorer is available and lets anyone check proof status, provider performance, and fault history.

Filecoin’s FIL token tanks to $0.83

Despite the positive news, Filecoin’s native token, FIL, has seen a steep slide in price. It is currently trading at $0.83, which is close to its all-time low of $0.81 recorded last month.

FIL dropped 4% in the last 24 hours, 8% in the last week, and 22.2% in the 30 days. CoinGecko data shows that FIL has lost 99.6% of its value from its all-time high of $236.84 in April 2021.

FIL maintains its position among the top 100 cryptocurrencies. The decentralized storage coin ranks 83rd in terms of market capitalization, with a market cap of $638,926,958 million.

Filecoin’s native token, FIL, is trading at $0.83, close to its all-time low of $0.81 recorded last month. Source: CoinGecko.

Filecoin is facing a decline in terms of total value locked (TVL) as well. DeFiLlama data shows that Filecoin’s TVL slumped by 9.88% in the past 24 hours. It’s currently standing at $6.31 million. The decline in FIL’s price and TVL suggests that the market is not responding positively to the Onchain Cloud launch.

The collected fees by the network is only $1,950 in 24 hours. Filecoin struggles to remain profitable. The amount of stablecoins circulating on the Filecoin network is very low at around $153,629. The full supply of stablecoins is in the form of USDFC.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

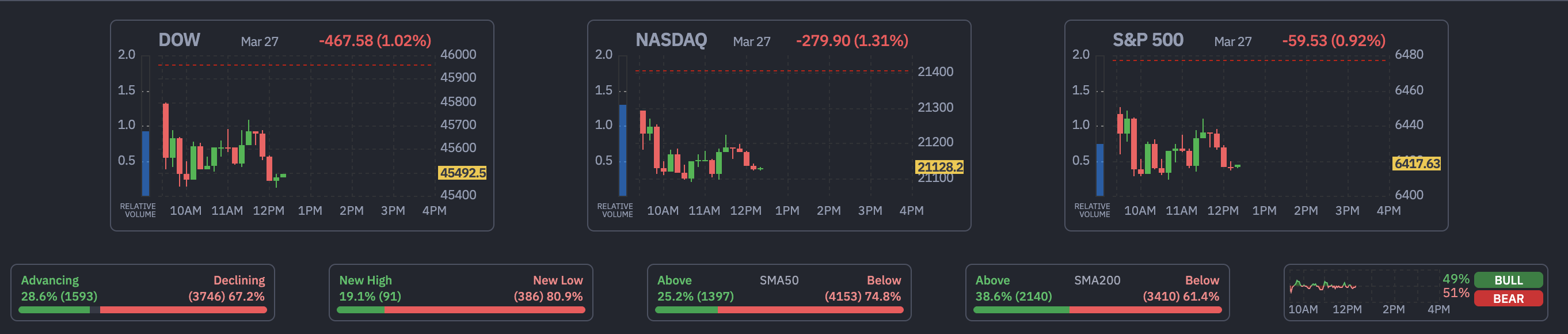

The US stock market fell on Friday as rate hike expectations crossed the 50% threshold for the first time, bond yields hit new highs, and the Iran war showed no signs of de-escalation. The S&P 500 dropped 0.92%, heading for its fifth straight weekly decline.

Three forces drove the selling on Friday, all connected to the same root cause. Oil (Brent Crude) above $100 is feeding into inflation, forcing the Fed’s hand and crushing bonds and equities simultaneously.

1. Rate Hike Odds Cross 51% as Fed Cuts Vanish Until December 2027

The CME FedWatch Tool now shows no expected rate cuts until December 2027 and a 51% probability of a rate hike by March 2027. Surging oil prices are feeding into inflation expectations, forcing the Fed into a corner where easing becomes impossible. Higher rates compress earnings multiples and make risk assets less attractive.

BREAKING: The US Federal Reserve is now no longer expected to cut interest rates until December 2027.

There is now a 51% chance of an interest rate HIKE by March 2027.

The 10-year Treasury yield climbed to 4.48%, its highest since the conflict began.

We believe this weekend is a crucial pivot point in the Iran War:

As the bond market continues to get crushed, the 10Y Note Yield just hit a new high of 4.48%. For the first time since the Iran War began, the bond market is nearing or already in “crisis” territory.

When yields rise this sharply, it pressures growth stock valuations and competes with equities for capital. The US Dollar Index (DXY) is gaining strength, squeezing multinational earnings as foreign revenue translates into fewer dollars back home.

With over 40% of S&P 500 revenue coming from overseas, the stronger dollar is pressuring the broader index.

Meanwhile, capital has rotated into gold above $4,400 and silver, reflecting a flight into hard stores of value.

3. Iran Rejects Direct Talks, Brent Holds Above $104

Iranian Foreign Minister Abbas Araghchi said exchanges through mediators do not constitute “negotiations with the United States.” Brent crude held above $104, keeping the geopolitical risk premium intact.

Oil above $100 functions as a tax on consumers and businesses, raising input costs and squeezing discretionary spending.

What Is Happening to Major US Indexes?

At press time, all three major indexes are in the red.

S&P 500: down 59.53 points (−0.92%) at 6,417 (stronger dollar hitting several players)

Dow Jones Industrial Average: down 467.58 points (−1.02%) at 45,492

Nasdaq Composite: down 279.90 points (−1.31%) at 21,128

Market breadth is overwhelmingly negative, with 3,746 stocks declining versus 1,593 advancing.

The S&P 500 continues its decline after breaking down from a bear flag pattern. The breakdown started on March 18 and has already delivered a 3.8% correction. The measured move target sits at 6,347.

If the index fails to reclaim 6,435, the factors above could push it toward 6,347 and even 6,213.

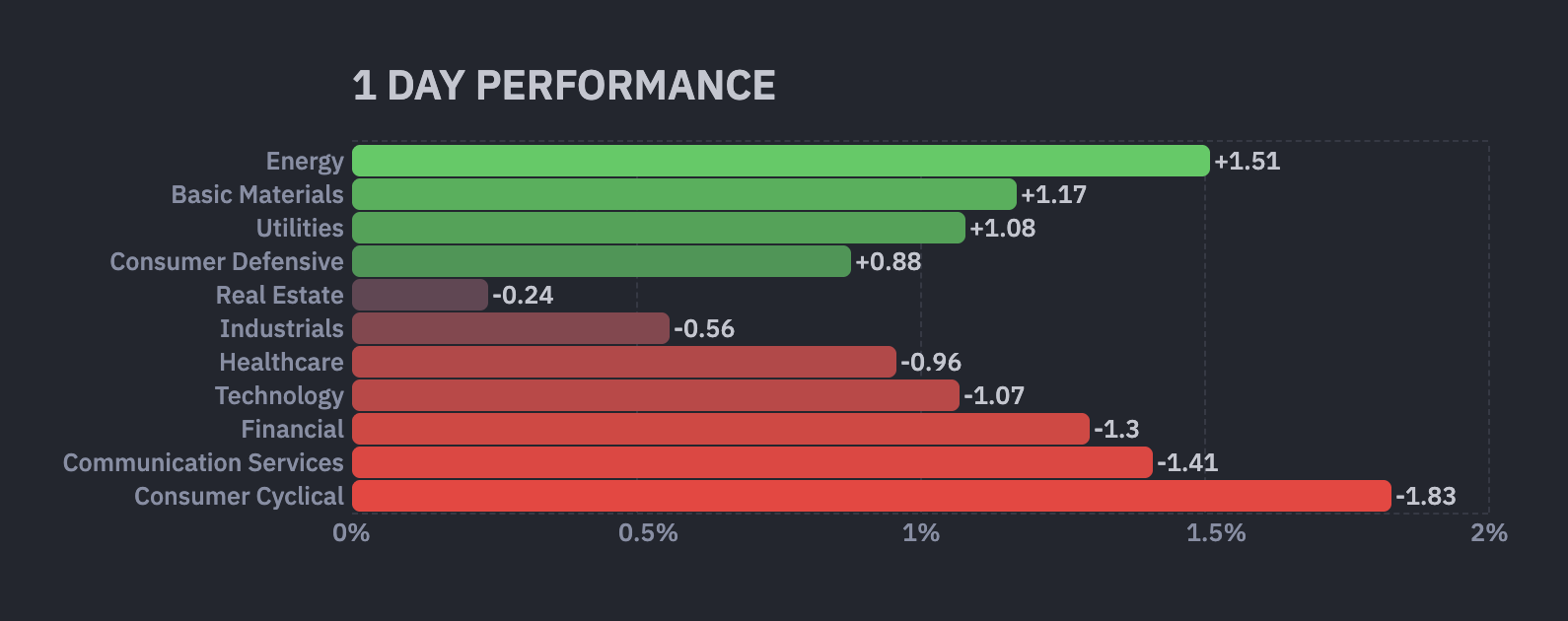

Which Sectors Are Holding Up?

Energy led with a 1.51% gain as Brent stayed above $104. Exxon Mobil (XOM) gained 3.17% at press time, and Chevron (CVX) rose 1.98% as elevated oil prices directly increased producer revenue.

Basic Materials added 1.17% on rotation into commodities. With gold above $4,400 and silver strengthening, mining stocks attracted capital as an inflation and geopolitical hedge.

Utilities gained 1.08% as defensive positioning continued. Risk aversion is overriding the traditional rate sensitivity of the sector, making yield-paying defensives attractive as a parking spot for nervous capital.

Which Sectors Are Falling?

Consumer Cyclical led losses at -1.83%. Oil above $100 acts as a direct tax on spending power. Amazon (AMZN) fell 3.38%, and Tesla (TSLA) dropped 1.83%.

Communication Services lost 1.41% as Meta (META) fell 3.65%. Ad-dependent businesses suffer early in slowdowns because advertising budgets are among the first expenses companies cut. Financials declined 1.30 as the speed of the yield surge, combined with recession fears, creates credit risk concerns that outweigh the margin benefit.

Technology lost 1.07% as the Nasdaq entered correction territory and higher bond yields crushed growth stock valuations.

Major Stock News Investors Are Watching

Unity Software (U) surged 10% after preliminary Q1 revenue of $505 million to $508 million crushed guidance. The company also plans to sell its China division for over $1 billion, streamlining around its AI-powered Vector advertising platform.

Unity Software sharply higher premarket after raising its Q1 revenue guidance above consensus. The company sunsetting its ironSource Ads Network. $U 19.42, +2.29, +13.4% pic.twitter.com/sbVLYl9ka3

CrowdStrike (CRWD) fell 7% after FY27 guidance landed below expectations while AI-powered rivals intensified competitive pressure in cybersecurity.

$CRWD -7%, $PANW -7.2%, $NET -3.75%, $ZS -7.6%, $OKTA -6.7% … [Cybersecurity stocks including CrowdStrike, Palo Alto Networks, Cloudflare, Zscaler, and Okta are falling after Anthropic accidentally leaked details of its new powerful AI model with strong cyber capabilities.]… pic.twitter.com/IZH2vWuL0l

Iran’s counter-proposal to President Trump’s 15-point peace plan is expected today. If the proposal shows willingness to negotiate, oil could retreat and pull equities higher by Monday’s open.

TRUMP AND TOP WHITE HOUSE OFFICIALS HAVE BEEN TOLD THAT IRAN’S COUNTER-PROPOSAL WOULD LIKELY ARRIVE FRIDAY VIA INTERLOCUTORS -SOURCE

If it amounts to another rejection, yields could push above 4.50% next week, and the S&P 500’s 6,347 target comes firmly into play. The weekend could be the most consequential 48 hours for markets since the conflict began.

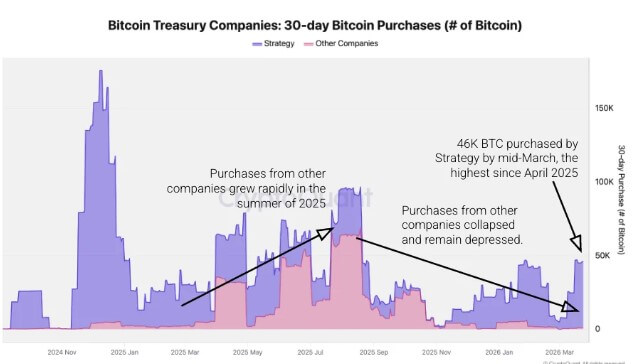

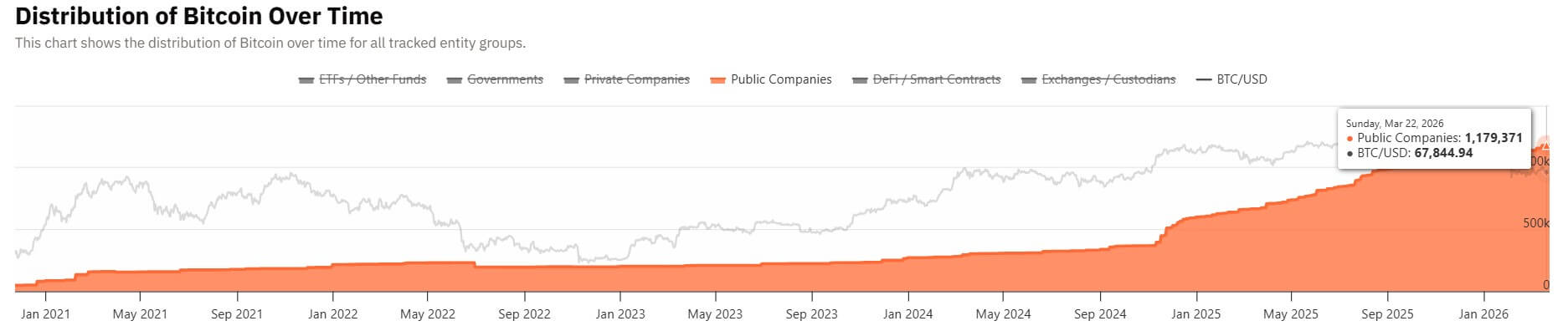

The corporate Bitcoin treasury boom is losing oxygen: a $100 billion public-company bet has shrunk, buying has collapsed outside Strategy (formerly MicroStrategy), and the financing model that drove the trade is starting to fail.

Data from CryptoQuant show that the Michael Saylor-led company bought about 45,000 Bitcoin over the last 30 days, the largest 30-day haul since April 2025.

Over the same period, all other Bitcoin treasury companies combined purchased about 1,000 Bitcoin, down about 99% from the 69,000 BTC they bought at the peak of the trade in August 2025.

CryptoQuant noted that the gap has widened to the point that Strategy now accounts for about 98% of all Bitcoin bought by treasury firms over the past month.

Last October, the balance looked very different, with companies outside Strategy responsible for about 95% of net purchases during a period when corporate buying was spreading across a wider list of names.

That shift has left Strategy as the dominant source of incremental treasury demand in a sector that, only months ago, was being promoted as a broader corporate movement tied to Bitcoin’s rally and to publicly listed companies’ ability to use their stocks as financing tools.

Participation shrinks beyond Strategy

The slowdown outside Strategy is showing up not only in the size of purchases but also in the number of companies still participating.

Treasury companies other than Strategy made 13 Bitcoin purchases in the last 30 days, down 76% from the 54 recorded in August 2025, when corporate activity was at its peak. Strategy, by contrast, has maintained a steadier pace, posting about 4 to 5 purchases each 30-day period.

The numbers point to a market where both the depth and breadth of demand have weakened. Fewer companies are buying, and those that remain active are deploying less capital than they did during the peak of the trade.

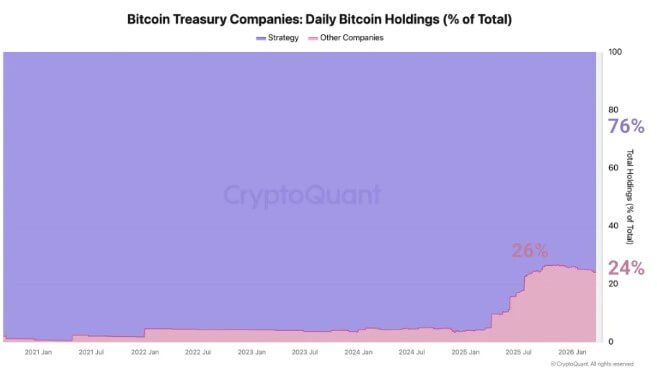

That change has altered the makeup of the sector. While Strategy’s total Bitcoin holdings have grown by about 90,000 Bitcoin so far this year, other treasury companies together have added a net 4,000 Bitcoin over the same period.

As a result, their share of total corporate treasury holdings has slipped from 26% in November 2025 to 24% now, while Strategy’s share has continued to climb.

Strategy now holds about 76% of all Bitcoin owned by treasury companies. The next two largest holders, XXI and Metaplanet, account for 4.3% and 3.5%, respectively.

For a sector that expanded quickly as rising Bitcoin prices pulled in new entrants, the concentration is becoming harder to ignore.

The corporate treasury model gained momentum last year as Bitcoin rose and public-market investors rewarded listed companies that offered leveraged exposure to the asset.

As Bitcoin climbed, many companies were able to issue shares at premiums to the value of the BTC already on their balance sheets.

That gave them a way to raise capital, buy more Bitcoin, and, in some cases, widen the gap between their market value and the underlying value of their holdings. Notably, some also used debt financing to add exposure.

As prices fell, the net asset value tied to corporate holdings also fell. At the same time, equity valuations for many digital asset treasury companies moved lower, reducing their ability to issue stock on favorable terms.

Consequently, the result has been a tighter feedback loop across the sector, in which a lower Bitcoin price reduces Bitcoin’s net asset value per share. This leads to lower equity premiums, making stock issuance less accretive.

Once those conditions are set in, the same financing mechanism that helped companies expand their Bitcoin positions begins to lose effectiveness.

That pressure has hit treasury-company equities hard. Shares that had traded as high-beta expressions of Bitcoin’s upside have declined sharply from their 2025 highs, and many have underperformed BTC itself.

For companies that bought heavily near the top of the market, such as Metaplanet, unrealized losses are beginning to mount.

Metaplanet Bitcoin Holdings Net Value (Source: Metaplanet)

Stress emerges across the sector

Meanwhile, signs of strain are beginning to appear in individual cases across the sector.

One recent example came from GD Culture, the publicly traded artificial intelligence and livestreaming firm, which approved the sale of its 7,500 Bitcoin, worth about $503 million, to fund share buybacks and support its stock price.

The sector’s aggregate numbers also reflect the change in conditions. More than 100 public companies piled roughly $100 billion into Bitcoin last year as the trade gathered pace.

Those holdings are now worth about $83.7 billion, according to Bitcoin Treasuries data, a sharp reduction from their peak value.

Public Companies Total Bitcoin Holdings (Source: Bitcoin Treasuries)

At the same time, only two of the public companies that hold Bitcoin on their balance sheets bought more of the asset in the past week, according to data compiled by Hodl15Capital.

The slowdown suggests that, outside a small number of committed players, the appetite to keep adding exposure has faded with the market.

Metaplanet, one of the highest-profile Bitcoin treasury companies in Japan, raised 40.8 billion yen, or about $255 million, as part of a financing that could deliver up to $531 million in total capital for Bitcoin purchases.

Yet it has not made a Bitcoin purchase this year, even as it maintains a long-term target of holding 210,000 Bitcoin. The company currently holds 35,102 Bitcoin.

Against that background, research across the sector is increasingly pointing to a more difficult environment for firms that built their strategy around equity issuance and rising Bitcoin prices.

Analysts at Galaxy Digital have said the same financial engineering that amplified upside when valuations were strong is now magnifying downside as equity premiums compress.

For treasury companies whose shares had functioned as leveraged crypto trades, softer markets and weaker risk appetite across public equities have changed the economics of the model.

Crypto research firm 10x Research also argued that the first stage of the treasury-company trade has already run its course, with the easy gains from rich premiums to net asset value no longer available to most firms.

In that environment, companies are likely to face stronger scrutiny over how much stock they issued at peak valuations, how much Bitcoin they bought near cycle highs, and how much debt they took on to fund those positions.

Now, a more selective phase is beginning to take shape.

Galaxy Digital stated that companies with stronger balance sheets and more durable access to capital are better positioned to endure a long period of flat or negative premiums to net asset value.

Already, several Bitcoin treasury firms, including Strategy and Strive, are using preferred stock options to fund new BTC acquisitions, aiming to outperform the top crypto over the long term.

On the other hand, others may need to scale back purchases, rethink capital strategy, or defend shareholder support if equity markets remain unreceptive.

The Ethereum Foundation brought together some of the world’s most influential financial players in New York City for an exclusive, invitation-only institutional forum on how traditional finance is engaging with ETH. This gathering signals a growing focus on bridging the gap between decentralized technologies and traditional finance, as major players increasingly explore blockchain integration.

Institutional Participation Signals Growing Confidence In Ethereum

The Ethereum Foundation hosted a high-level invite-only institutional forum in New York City, drawing participation from hundreds of banks, asset managers, and infrastructure providers representing a combined $250 trillion in assets under management (AUM). An investor known as Milk Road on X revealed that major players, including BlackRock, Western Union, Robinhood, Moody’s, Baillie Gifford, and Securitize, took part in panels as builders, actively working on solutions within the ETH ecosystem.

Before now, institutional adoption used to be a bumper sticker, a story investors told themselves to feel better about the asset they already held. This move is different because the firms managing a combined $250 trillion in assets sat in rooms and talked about what they’re actually building on ETH.

In addition, the ETH Foundation used the event to unveil its post-quantum security strategy and launch a dedicated resource hub. Addressing such forward-looking challenges in a room filled with major financial institutions sends a signal.

Milk Road noted that the ETH Foundation is positioning its infrastructure to evolve over decades, not just short-term market cycles. For those who have questioned whether major institutions would move beyond experimentation, the developments in New York offered a compelling counterpoint.

Bitmine Launches Staking Model, ETH Network Activity Surges

Tom Lee, alongside Bitmine Immersion Technologies (BMNR), has officially launched MAVAN, the made-in-America Validator Network. According to Tom Lee Tracker, MAVAN is set to become the largest Ethereum staking platform globally, with approximately 3,142,643 ETH already staked, valued at around $6.8 billion based on an estimated price of $2,148 per ETH.

The scale of growth is accelerating, with over 101,776 ETH, worth around $219 million, staked in the past week alone. At full deployment, the network is projected to generate nearly $300 million in annualized staking rewards. Beyond ETH, MAVAN is also expected to expand into additional proof-of-stake chains and broader blockchain infrastructure.

Activity on the Ethereum network is surging, with daily transactions rising at an explosive pace. Crypto investor known as CW on X has stated that despite the price weakness, the network activity still remains at an all-time high level. Such a growth is not a signal of a bear market, as the price has dropped, but some investors are working very hard under the surface.

Ten individuals involved in the JPEX cryptocurrency scam have been charged with money laundering and conspiracy to launder money, bringing the total number of charged individuals to 26.

Hong Kong’s authorities are still going after other suspects with help from international law enforcement agencies. For now, they continue to cast a wide net as no individual has been pegged as the main operator or mastermind of the JPEX operation yet.

Hong Kong’s biggest crypto scam case

Hong Kong police have charged ten additional individuals in connection with the JPEX cryptocurrency fraud case.

The Commercial Crime Bureau stated that the ten individuals include six men and four women, aged between 26 and 47. They have been charged with money laundering and conspiracy to commit money laundering and are expected to appear in the Eastern Magistrates’ Courts on Friday, March 27.

In November last year, 16 people, including social media influencers and alleged core members of the JPEX gang, were charged with offenses such as fraud, conspiracy to defraud, and money laundering.

Chief Inspector Hon Shing-ho of the Commercial Crime Investigation Section said that the criminal gang launched the JPEX investment platform in early 2020 and invested significant funds to promote the platform through various channels. After creating an image of legitimacy, investors were then lured through advertisements of “low-risk, high-return” opportunities.

The scheme was discovered after the Securities and Futures Commission (SFC) issued a public warning statement in September 2023, alerting the public to JPEX’s suspicious activities and also clarifying that the platform was unlicensed.

Following the warning, JPEX drastically increased its withdrawal fees, preventing customers from accessing their virtual assets. Investigators found that the operators subsequently transferred client assets and laundered money through a large number of cryptocurrency wallets.

Authorities also discovered that some suspects had bank accounts with unusually high volumes of transactions that were “seriously inconsistent” with their financial profiles, involving amounts totaling HK$132 million. These funds were allegedly used to purchase luxury cars and goods or were withdrawn as cash.

To date, the police have received reports from over 2,700 victims, with total reported losses exceeding HK$1.6 billion. Since the investigation began in September 2023, a total of 80 people have been arrested, including core gang members, over-the-counter (OTC) exchange operators, social media influencers who promoted the platform, and account holders involved in money laundering.

Authorities have frozen approximately HK$228 million in assets, including bank account balances, cash, gold bars, luxury goods, luxury vehicles, and virtual assets.

How will the JPEX investigation proceed?

Chief Inspector Hon noted that since the incident began, no company or individual has come forward to claim responsibility as the true operator of JPEX, and so the police have to conduct extensive investigations to identify the masterminds and core members behind the scheme.

This has involved collecting evidence and statements from victims and witnesses, analyzing vast amounts of company registration and financial transaction records, and conducting forensic examinations of numerous electronic devices.

Interpol has issued Red Notices for three men believed to be key players who have fled Hong Kong. They are identified as Mok Tsun-ting, 27; Cheung Chon-cheng, 30; and Kwok Ho-lun, 28.

The police have confirmed that they will continue to collaborate with international law enforcement agencies to apprehend the suspects still at large.

The cases against the 26 charged individuals are progressing through the judicial system. The eight defendants from the first round of charges, including influencers Joseph Lam and Chan Wing-yee (“Chan Yee”), have already appeared in court.

Their case was adjourned until June 1. For the ten newly charged suspects, the prosecution is applying to transfer the case to the District Court for trial.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Months after a daring hunger strike failed to pause development of Anthropic’s AI Claude, protestors have rallied around the company’s headquarters to call for a complete stop to AI development.

Last weekend, nearly 200 protestors with the organization Stop the AI Race demonstrated in front of Anthropic, demanding the company’s CEO, Dario Amodei, publicly commit to pausing their development of AI. According to FirstPost, protestors included former tech industry workers, researchers, and members of other grassroots organizations like Pause AI and QuitGPT.

“The reason we are pausing AI is because we believe that building AI that can automate AI research, and that can self improve, could be a danger to the human race, especially human extinction,” Michaël Trazzi, an organizer with Stop the AI Race, told local reporters. “It’s not only me and other researchers saying this, it’s the lab CEOs themselves that [say] the risk is real.”

Stop the AI Race rallied around the company’s San Francisco headquarters for a while before marching on Sam Altman’s OpenAI and Elon Musk’s xAI, where they made similar demands.

In a post on social media, Trazzi claimed that it was “the biggest AI safety protest in US history” so far.

I organized the biggest AI Safety protest in US History!

Nearly 200 people marched from Anthropic to OpenAI to xAI with one demand: commit to pausing if the others do too pic.twitter.com/YZt8n740G3

One of the protestors involved, Guido Reichstadter, had previously protested outside Anthropic in the aforementioned hunger strike, which ultimately lasted for 30 days. Like Trazzi, Reichstadter’s concerns are existential — an AI system that could one day break containment and usher in unknown horrors on humankind.

On day nine of his hunger strike, Reichstadter told Futurism that frontier AI systems are an “entirely new class of danger.” Indeed, whether Claude is going to take over and start killing us all may be beside the point: in the hands of humans, it’s already picking strike targets for the US military.

“None of these companies have a right to do what they’re doing, which is consciously endangering my life, my family’s life, all of our lives,” Reichstader said. “The correct thing for them to do is stop the global race toward really dangerous AI that we’re all involved in.”