JPMorgan Chase & Co. is concerned that Strategy’s new policy of selectively selling its Bitcoin holdings will introduce new risk to the crypto market.

On Monday, Strategy announced a BTC monetization program through which the company can sell a portion of its 847,363 BTC holdings to support its preferred dividend payments and buybacks.

The so-called Digital Credit Capital Framework followed months of criticism of Strategy’s capital position amid declines in the price of BTC and MSTR.

JPMorgan said the policy adds avoidable “two-way” flow risk to crypto markets.

In a Wednesday report, JPMorgan analysts led by Nikolaos Panigirtzoglou said Strategy has spent years as one of Bitcoin’s most consistent buyers, accounting for about 70% of total net digital asset inflows this year.

The policy, as such, introduces a new risk that the biggest BTC buyer could sell off its holdings at any moment.

Strategy should raise 24 to 36 months of cash reserve

JPMorgan suggests that Strategy raise its cash reserve by issuing common equity to shore up investors’ confidence that it won’t need to sell its Bitcoin holdings.

Strategy currently holds $2.55 billion in cash, enough to cover about 17 months of preferred dividend and interest obligations. The analysts believe the buffer is not wide enough.

They said, “a higher coverage of 24-36 months would be needed to make investors more comfortable with the idea that Strategy would not need to sell bitcoins in the foreseeable future.”

Analysts split on what comes next

Not everyone at the research desks shares JPMorgan’s caution. Benchmark Equity Research reiterated a Buy rating on MSTR with a $570 price target, implying more than 500% upside from recent levels, following the sales policy.

Analyst Mark Palmer called the capital framework “formal permission” to put Strategy’s capital machine into reverse during periods of market stress, framing it as a net positive for shareholders, as Cryptopolitan reported.

Meanwhile, the MSTR price has made gains since the policy. The shares rose 12.6% to $92.68 on Monday, while STRC gained roughly 10% to around $83.67 after trading below $75 the previous week.

By Wednesday, MSTR had pushed past $100, adding $5 billion in market cap and climbing 27% from Friday’s low.

At the time of writing, MSTR was trading at $100.83, a 7.93% increase on the day.

Michael Saylor pitted Strategy (MSTR) against the Magnificent 7 (Mag 7) on July 2, branding his company the “MoST inteResting” stock on Wall Street as shares recover from last week’s lows.

The comparison rests on derivatives positioning rather than price performance. According to a chart Saylor shared, MSTR options open interest equals 71.9% of the company’s market capitalization, several times higher than any Mag 7 member.

Michael Saylor Pits MSTR Against Mag7 Members as MicroStrategy Stock Stages July Recovery. Source: Saylor on X

MSTR Options Interest Dwarfs the Mag 7

Saylor’s post capitalized select letters in “MoST inteResting” to spell out the MSTR ticker. His chart put Tesla (TSLA) closest at 15.8% and Meta (META) at 10.8%, with the remaining Mag 7 members lower still. Notably, the numbers are Strategy’s own presentation and capture one snapshot in time.

The ratio captures how traders treat the stock. With a beta of 3.54, per S&P Global data, MSTR moves like a leveraged proxy for its $64 billion Bitcoin bet. Options remain the preferred vehicle for that exposure.

MicroStrategy’s latest filing shows 847,363 Bitcoin (BTC), over 4% of the circulating supply. The company paid $64.1 billion, an average of $75,646 per coin.

MSTR jumped 12.5% on Monday after unveiling its capital management overhaul. It then slid 6.2% to $86.93 on Tuesday as TD Cowen cut its target to $260 from $400.

On Thursday, shares climbed more than 7%, effectively recovering above $1009 to suggest a July recovery that is still pending confirmation.

The June 29 framework set aside a $2.55 billion cash reserve, covering 17.4 months of preferred dividends and interest. It also authorized up to $1.25 billion in Bitcoin sales and $2 billion in buybacks. Company leadership cast the change as deliberate.

“Strategy is evolving from one-way capital issuance to active capital management,” Phong Le, CEO of Strategy, said in the announcement.

Meanwhile, Wall Street’s response captures the tension. Citi kept its Buy rating but slashed the price target from $260 to $136, saying the plan buys time for Bitcoin to stabilize.

TD Cowen and BTIG also kept Buy ratings while lowering targets. Separately, Rosen Law Firm opened a securities probe into Strategy.

Saylor also reiterated the $100 STRC target as the preferred stock recovers from its June 26 record low of $71.25.

Supporters read the options dominance as conviction. In contrast, critics counter that the same leverage dragged the stock from a 52-week high of $457.22 to $81.81.

Whether derivatives fervor converts into durable equity performance still hinges on Bitcoin holding above $60,000. Strategy reports earnings on July 30, the first test of the new playbook in action.

MicroStrategy’s $64 billion Bitcoin (BTC) bet has become a stress test for everyone who funded it. BTC now trades below $60,000, and the renamed company, Strategy, sits at a discount to its own holdings.

The question dividing investors is no longer whether Strategy gets liquidated tomorrow. It is who absorbs the losses while the company keeps its coins and keeps paying to hold them.

How the Bitcoin Flywheel was Built

By June 22, Strategy held 847,363 BTC bought for $64.1 billion, an average of $75,651 each. That is the largest corporate Bitcoin position anywhere.

MicroStrategy Bitcoin Purchases in 2026. Source: Strategy

The model runs like a flywheel. The company sells stock and debt, buys more Bitcoin, and its shares climb when BTC rises. However, falling prices spin the machine in reverse.

BTC has fallen below $60,000 this week, its lowest level since 2024. The stock has slid with it, dropping under the value of the Bitcoin on its books.

A new accounting standard made the pain visible. Since 2025, FASB rule ASU 2023-08 forces firms to mark Bitcoin to fair value each quarter. As a result, Strategy booked a $14.46 billion unrealized loss in early 2026. That produced a $12.54 billion net loss, or $38.25 for every diluted share.

Michael Saylor’s Strategy currently has a $14 billion unrealized loss on bitcoin.

Tom Lee’s Bitmine currently has a $10.5 billion unrealized loss on ETH.

This is why it’s foolish to follow the smart money and not take profit.

They can survive a crypto winter, most of will not!

The bill does not fall on Strategy alone. As the flywheel slows, the cost spreads to five groups, in rough order of exposure.

Common shareholders

They stand first in line. When the stock trades below the value of its Bitcoin, the company still raises cash by selling new shares. Each sale buys less Bitcoin than it hands away.

“If we decide to sell $1 billion of MSTR stock and buy $1 billion of Bitcoin… when you do it at 1.0x MNAV… it is dilutive. It is a minus 48 basis point yield. It costs the shareholders $310 million,” Michael Saylor, Executive Chairman, Strategy, said during Q1 2026 earnings call.

Existing owners are left holding a smaller claim on the same coins, and that dilution is how the strategy gets funded.

Investors in other treasury companies

The copycats have fared worse than the original. Their shares once traded far above the Bitcoin they held, lifted by hype.

As that premium faded, many Bitcoin treasury company stocks fell much harder than Bitcoin itself, leaving late buyers deep underwater.

“If that’s not already a bubble burst, how would that bubble burst?” Tom Lee, Chairman of BitMine, said while many treasury stocks traded below net asset value.

Passive and index fund investors

This group never chose the bet. MSCI has proposed removing companies whose digital assets exceed half their total assets from its global indexes.

“Feedback from the consultation confirmed institutional investor concern that some DATCOs exhibit characteristics similar to investment funds, which are not eligible for inclusion in the MSCI Indexes,” MSCI said in its official announcement earlier this year.

Strategy clears that bar with ease. An exclusion would force index funds and pension trusts to sell automatically, whatever the price, just to keep tracking the benchmark.

Convertible bondholders and preferred shareholders

These investors lent on the assumption that MicroStrategy could always refinance. If Bitcoin stays depressed into 2027, that assumption breaks.

“Proceeds from the bitcoin sales are expected to be used to fund distributions on preferred stock,” Strategy indicated in the June 1 Form 8-K.

Bondholders can demand cash, and preferred holders still expect dividends, both drawing on a reserve of just $1.4 billion.

MicroStrategy itself

The company is the backstop of last resort. On its first quarter 2026 earnings call, Michael Saylor again framed Strategy as a net buyer that never sells.

“We will probably sell some Bitcoin to fund a dividend just to inoculate the market, just to send the message that we did it.”

Yet if financing freezes while debt and dividends come due, keeping that vow could become impossible.

“We will sell Bitcoin when it is advantageous to the company. We are not going to sit back and just say we will never sell the Bitcoin,” Strategy co-CEO Phong Le added.

The Real Test Arrives in 2027

MicroStrategy faces no margin call today. Its main debt is unsecured, so a falling price alone cannot trigger a forced sale. The threat is a date, not a level.

Holders of a $1.01 billion convertible note can demand repayment on September 15, 2027. If the shares sit below the conversion price, that claim becomes a cash bill the company must cover.

Strategy has neared this edge before. A 2022 Silvergate loan backed by Bitcoin carried a margin call near $21,000 before the firm repaid it. Moving to unsecured notes and preferred stock removed the automatic trigger, but not the obligation.

Microstrategy took a loan to buy more #bitcoin a few months ago using 19,000 $BTC as collateral.

For now, no forced sale looms. The pressure has simply moved from a price trigger to a calendar. The number that matters is no longer $60,000, but the September 2027 repayment date.

Rosen Law Firm has launched an investigation into Strategy (formerly MicroStrategy), inviting investors who purchased the company’s securities to participate in a potential class action lawsuit.

The law firm said it is examining whether Strategy and certain executives made materially misleading statements regarding the company’s business operations, Bitcoin treasury strategy, profitability, and the risks associated with its aggressive Bitcoin accumulation model.

Details of the MicroStrategy Lawsuit

The investigation covers several Strategy-linked securities, including MSTR, STRF, STRC, STRK, and STRD. Rosen has created a dedicated webpage allowing affected investors to join the probe.

Rosen Law Firm Launches Probe Into MicroStrategy. Source: Press Release

The development follows a period of heightened scrutiny around Strategy’s capital structure and its growing reliance on multiple classes of securities to fund Bitcoin purchases.

One security attracting particular attention is STRC, Strategy’s perpetual preferred stock. Blockchain analytics platform Arkham recently addressed comparisons between STRC and the collapsed Terra ecosystem, arguing that the situations are fundamentally different.

“IS STRC THE NEXT LUNA? Short answer – not quite,” Arkham wrote in a post on X.

The firm stressed that Strategy is under no legal obligation to maintain STRC’s market price, distinguishing it from algorithmic stabilization mechanisms that contributed to Terra’s collapse.

“Unlike Terra LUNA, Saylor cannot ‘get liquidated’ if STRC falls in value,” Arkham said, adding that “the price of STRC simply reflects the market’s view of how likely Saylor is to continue paying dividends.”

Arkham also highlighted a key risk facing preferred shareholders, noting that dividend payments remain discretionary.

“Crucially: Strategy does not legally have to pay these dividends,” the analytics firm wrote. “If Strategy gets in trouble, Saylor does not have to prioritise STRC shareholder dividends.”

According to Arkham, maintaining STRC’s current dividend structure could require roughly $1.2 billion annually, raising questions about the long-term sustainability of Strategy’s expanding financing model if market conditions deteriorate.

Strategy has not publicly responded to Rosen’s investigation.

The Bitcoin treasury company spent $1.5 billion in May repurchasing convertible notes, reducing its debt but also draining cash that investors viewed as a backstop for its preferred-stock dividends. Weeks later, its Variable Rate Series A Perpetual Stretch Preferred Stock, known as STRC, fell to a record low of $82.50, or 17.5% below its $100 stated value.

Strategy has since started rebuilding the reserve by selling common shares. However, the response has sharpened a conflict at the center of Michael Saylor’s financing model: money retained to support STRC cannot simultaneously be spent buying Bitcoin, while raising that cash through MSTR sales dilutes existing common shareholders.

CryptoQuant said the pressure has become severe enough that the Saylor-led firm should suspend Bitcoin purchases until it restores its cash reserves and dividend coverage. Benchmark Equity Research, by contrast, views STRC’s decline as a market-driven repricing of the yield investors demand rather than evidence that the structure is failing.

The disagreement marks the clearest strain yet on Saylor’s effort to transform Strategy from a software company into an issuer of Bitcoin-backed “digital credit.”

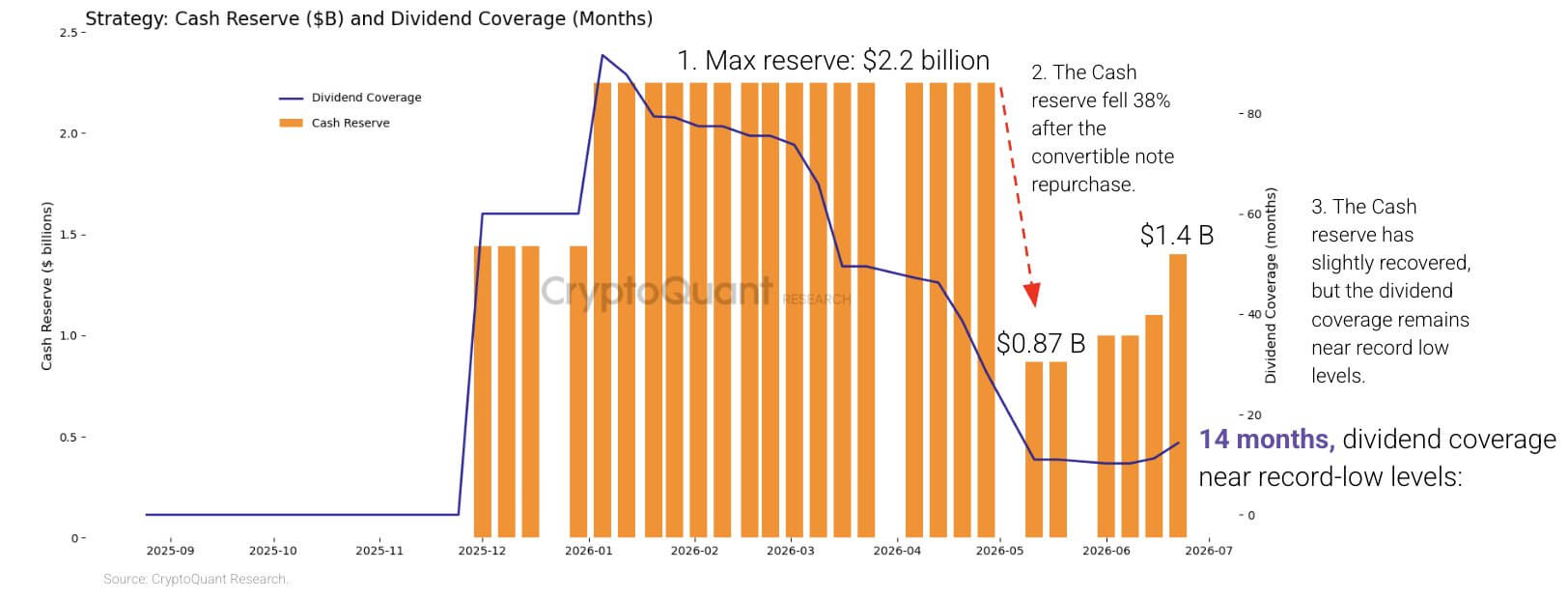

Dividend costs outrun the cash reserve

STRC was launched in July 2025 as a perpetual preferred security designed to trade near $100. Strategy can adjust its dividend rate monthly to make the shares more attractive when they fall below that level.

The security has since become an important source of funding for Strategy’s Bitcoin purchases. That expansion, however, has created a rapidly growing recurring obligation.

CryptoQuant estimated that Strategy’s annualized preferred-dividend obligations have nearly quadrupled from about $300 million at the start of 2026 to $1.2 billion.

At the same time, the company’s cash reserves declined by 38% from the beginning of the year, with the sharpest reduction following the May repurchase of its 0% convertible notes due in 2029.

While retiring the notes removed a future claim from the balance sheet, it also reduced the pool of liquid funds available to cover dividends during a period when Bitcoin prices and Strategy’s securities were under pressure.

CryptoQuant said the company entered 2026 with enough cash to cover more than seven years of dividends. The firm estimated that coverage had fallen to about 14 months after Strategy rebuilt its cash position to $1.4 billion.

Strategy Cash Reserve and Dividend Coverage (Source: CryptoQuant)

The analytics company estimated that Strategy would need about $2.8 billion to restore a 24-month reserve.

STRC allows Strategy to defer its dividends, but the payments are cumulative, meaning skipped distributions remain payable. A suspension could temporarily preserve cash while undermining investor confidence and making future preferred-stock issuance more expensive.

Strategy, therefore, has few painless options. Raising STRC’s dividend could support demand but would increase its cash burden. Retaining more capital would slow Bitcoin purchases, while additional MSTR sales would transfer more of the cost to common shareholders through dilution.

Meanwhile, Strategy’s Bitcoin treasury provides another potential source of liquidity, but using it now would also come at a cost.

CryptoQuant estimated that the holdings carried an unrealized loss of about $10.6 billion at prevailing prices. Selling during the downturn would crystallize some of those losses and challenge the company’s longstanding accumulation narrative.

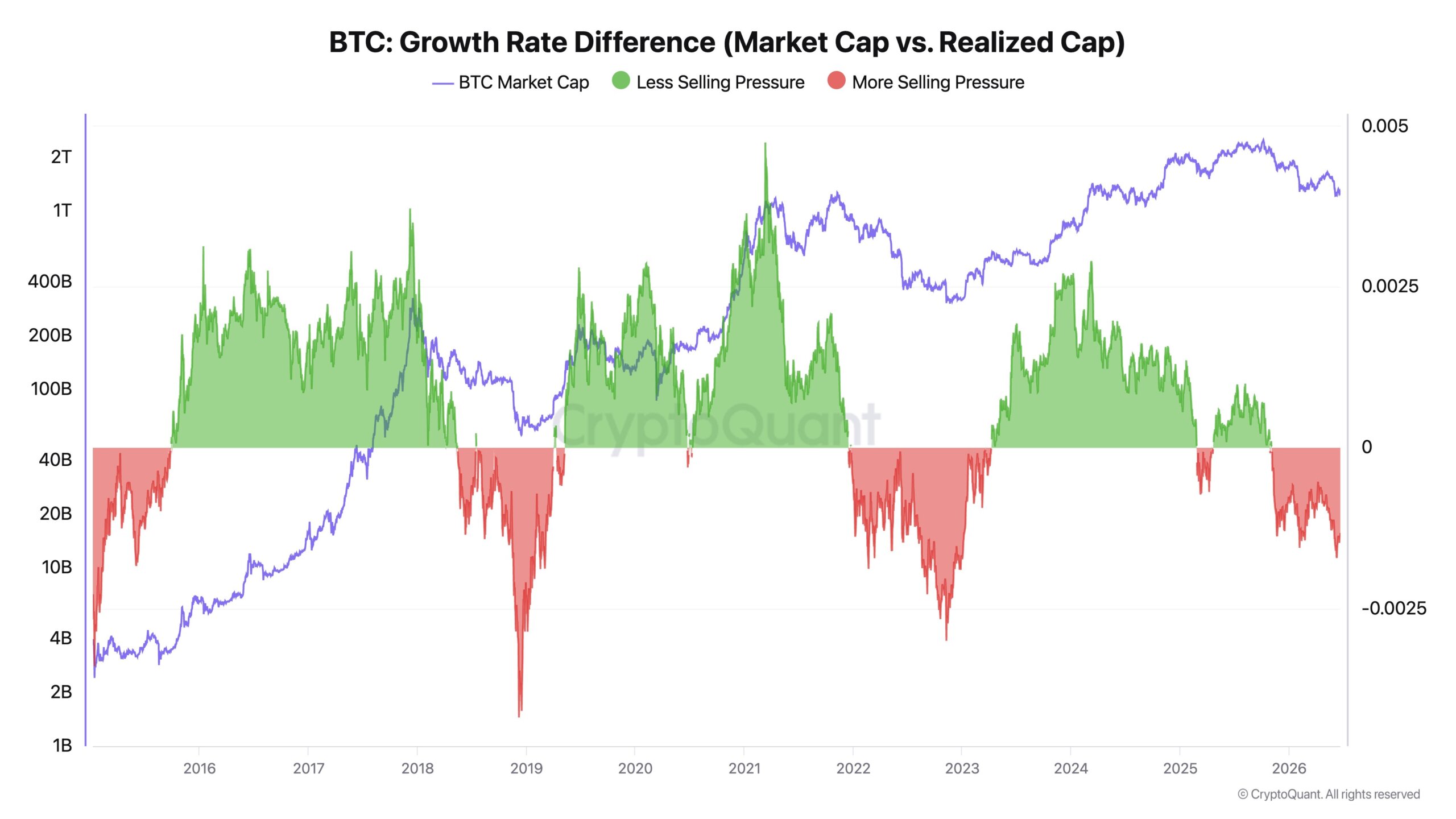

CryptoQuant Chief Executive Ki Young Ju saidStrategy’s recent Bitcoin purchases appeared to be absorbing capital without producing a sustained increase in the cryptocurrency’s price.

He described the buying as more of a “liquidity sink” than a price catalyst and said the company should prioritize cash coverage before making further acquisitions.

Ju noted that Bitcoin’s realized capitalization had increased by $467 billion over the previous two years, even as its price declined by about 1%. He argued that the divergence showed fresh capital was largely allowing coins to change hands rather than driving a broad revaluation of the market.

Bitcoin Growth Rate (Source: CryptoQuant)

Under conditions of limited selling, large institutional purchases can move prices sharply, Ju said. When selling pressure is elevated, the same demand may do little more than support an existing trading range.

He urged Strategy to replace its practice of buying whenever capital becomes available with a model-driven acquisition framework. He also called for rules that would allow the company to sell portions of its holdings during future market peaks, arguing that limited sales could reduce leverage, realize value for shareholders, and free up capital for purchases during later downturns.

Such an approach would represent a sharp departure from Saylor’s public commitment to persistent Bitcoin accumulation.

Common shareholders become the backstop

Meanwhile, Strategy’s latest fundraising showed which option management is currently prepared to use.

The allocation showed that rebuilding liquidity had temporarily taken priority over maximizing Bitcoin purchases. Strategy still expanded its holdings to 847,363 Bitcoin, purchased for about $64.01 billion at an average price of $75,651.

The cash injection also came with a larger share count. Strategy’s diluted shares increased to about 388.6 million from 386.1 million a week earlier. Its year-to-date BTC Yield, a company metric measuring changes in Bitcoin holdings relative to assumed diluted shares, fell to 11.8% from 13% four weeks earlier.

The decline does not mean Strategy owns less Bitcoin. It shows that Bitcoin holdings per assumed diluted share are increasing more slowly as the company issues additional equity.

That dynamic could become more pronounced if STRC remains substantially below $100. Issuing more preferred shares at unfavorable prices would become harder or require higher payouts, leaving common equity as Strategy’s most readily available source of capital.

MSTR shareholders would then be financing both the company’s Bitcoin purchases and the cash reserve supporting securities with senior claims on the balance sheet.

Supporters of Strategy’s model dispute the conclusion that its common-stock sales have weakened investors’ economic position.

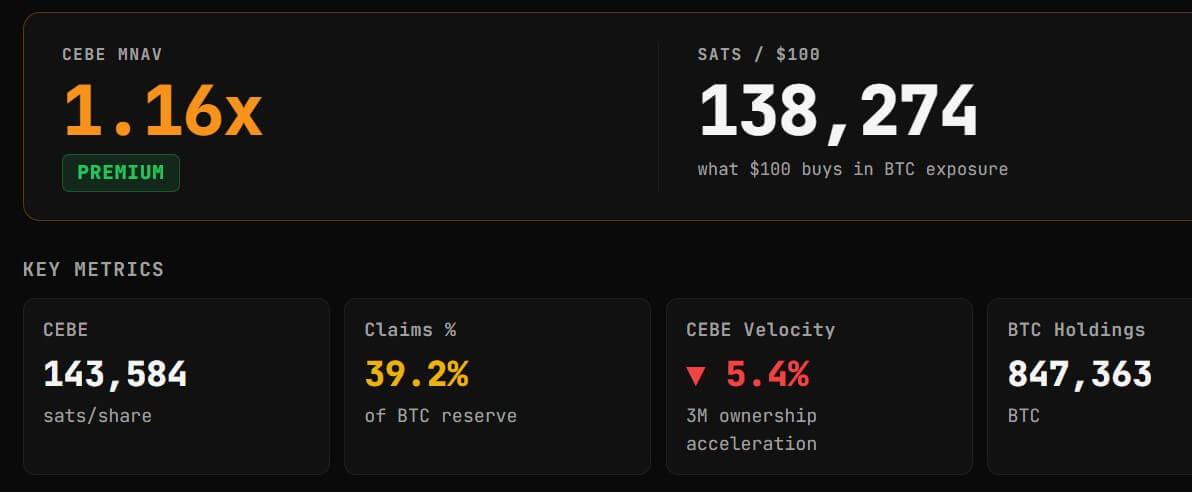

Adam Livingston, a pro-Strategy analyst, said the company added about 24,029 satoshis of Common Equity Bitcoin Exposure per basic share during the year despite issuing additional stock.

Common Equity Bitcoin Exposure, or CEBE, attempts to calculate the Bitcoin attributable to common shareholders after deducting debt, preferred stock, and other senior obligations. Livingston argued that Strategy used the proceeds from new shares to acquire enough Bitcoin to increase the net exposure supporting each basic share.

That does not mean the issuance was not dilutive. Existing shareholders still own a smaller percentage of the company after new stock is sold. Livingston’s argument is instead that the assets attributable to each share rose by enough to offset the increase in the share count.

Livingston’s conclusion also differs from the decline in Strategy’s reported BTC Yield because the two measures use different methodologies. Strategy’s metric relies on assumed diluted shares, while Livingston’s calculation uses basic shares and adjusts Bitcoin holdings for senior claims.

Data from CEBE Tracker placed Strategy’s CEBE multiple to net asset value at about 1.15 times, meaning MSTR continued to trade at a premium to the estimated net Bitcoin exposure attributable to common holders.

Strategy’s CEBE Metrics (Source: CEBEtracker.io)

That premium remains central to Strategy’s model. As long as the company can issue stock above the value of the Bitcoin backing each common share and use the proceeds accretively, advocates argue that new issuance can increase rather than destroy per-share exposure.

The risk is that the premium narrows while cash requirements and preferred obligations continue to rise. Under those conditions, Strategy could still raise capital, but each transaction would generate less incremental value for existing common shareholders.

Meanwhile, this market pressure has impacted MSTR’s price performance. Yahoo Finance data shows MSTR has fallen below the $100 mark, its lowest price level since March 2024.

Investors disagree over whether the model is breaking

CryptoQuant views STRC’s discount as evidence that Strategy’s liquid resources have failed to keep pace with its obligations. Benchmark analyst Mark Palmer sees the same decline as a conventional adjustment in the yield investors require.

Palmer rejected comparisons between STRC and failed stablecoins such as TerraUSD, noting that STRC is a perpetual preferred stock rather than an asset supported by an algorithmic peg. Strategy has said it intends to manage STRC near $100 but has not guaranteed that price.

At about $87, a dividend calculated at roughly 11.5% of the $100 stated value gives buyers a market yield of more than 13%. That suggests investors are demanding greater compensation for Strategy’s Bitcoin exposure, cash requirements and increasingly complex capital structure.

Benchmark maintained its buy rating on MSTR and a $570 price target, arguing that elevated STRC trading volumes showed active repricing rather than structural deterioration. The firm also pointed to Strategy’s Bitcoin treasury, worth roughly $55 billion at the prices used in its analysis, and the company’s continued ability to adjust dividends and raise capital.

Charles Edwards, founder of Capriole Investments, offered a more severe assessment. He said a business model dependent on continued Bitcoin appreciation to support dividends and yield products would eventually become unsustainable.

He noted:

“As long as his business model requires Bitcoin ‘number go up’ to survive and pay yield or dividends, it’s a ticking time bomb. Maybe not this cycle, but the music will stop.”

Edwards argued that Strategy should reduce its liabilities, unwind its yield products, and return to holding a less encumbered Bitcoin position. He also proposed acquiring digital-asset treasury companies trading at large discounts to their net asset values and eventually building operating businesses around Bitcoin lending, borrowing, and settlement.

Those proposals would involve significant obstacles. Repaying Strategy’s liabilities could require selling Bitcoin, issuing more equity, or both. A move into lending would also introduce regulatory, credit, and counterparty risks beyond those of a treasury company holding Bitcoin on its balance sheet.

Still, Edwards’ criticism captures the longer-term question facing the company: whether Strategy can continue expanding its capital structure without becoming increasingly dependent on higher Bitcoin prices and uninterrupted access to equity markets.

The competing assessments are not entirely incompatible. Strategy may hold sufficient assets to meet its obligations over the long term, even as it faces a near-term shortage of cheap, liquid capital.

Its latest fundraising decision reflects that distinction. Strategy could still access the common-stock market, but it had to direct most of the proceeds to rebuilding cash rather than accelerating Bitcoin purchases.

That trade-off is likely to define the next phase of Saylor’s experiment. Raising the STRC dividend would increase costs. Selling more MSTR would dilute shareholders. Selling Bitcoin could lock in losses. Suspending payments could undermine confidence in Strategy’s preferred-stock franchise.

For now, the company is choosing cash and dilution and asking common shareholders to absorb the cost of keeping its Bitcoin funding machine intact.

Strategy (formerly MicroStrategy) added another $100 million of Bitcoin to its balance sheet last week, extending a buying campaign that has made the company the world’s largest corporate holder of the digital asset while sharpening a debate over what its common shareholders actually own.

On June 15, Michael Saylor, the company’s chairman, said Strategy bought 1,587 BTC at an average price of $63,024 per token, which lifted its total holdings to 846,842 BTC.

That position is equal to more than 4% of Bitcoin’s fixed 21 million supply cap, a level that has turned Strategy from a software company into one of the market’s most closely watched Bitcoin financing vehicles.

However, the latest purchase landed at a more difficult moment for the company’s equity story. Bitcoin has fallen sharply from recent highs, Strategy’s stock has come under increased pressure, and the company’s preferred per-share metric for tracking Bitcoin ownership moved lower following the transaction.

That decline has reopened a question that has followed Strategy through several rounds of capital raising: Is the company still increasing value for common shareholders, or is it asking them to accept a smaller claim on its Bitcoin stack in exchange for a larger and more complex balance sheet?

Bitcoin stack grows, BTC yield falls

According to the SEC filing, Strategy financed the latest purchase through sales of its Class A common stock.

The company said it sold 1.7 million MSTR shares last week for about $209 million. It used roughly $100 million to buy Bitcoin and allocated another $100 million to its dollar reserve, lifting that reserve to about $1.1 billion.

The company still has $25.75 billion of MSTR shares available for sale under its at-the-market program. It has also expanded its capital markets platform to include up to another $21 billion of common stock, $21 billion of STRC preferred stock, and $2.1 billion of STRK preferred stock.

The scale of those programs has made each new transaction a test of how investors should measure dilution.

Strategy’s BTC Yield, which tracks the change in Bitcoin holdings per assumed diluted share, slipped from 13.0% on June 1 to 12.8% on June 8. It fell again to 12.5% after the latest purchase. The decline came even as Strategy’s Bitcoin holdings rose from 843,706 BTC to 846,842 BTC over the same period.

Strategy’s Bitcoin Per Share (Source: Strategy)

For critics, that is the core issue. Strategy bought more Bitcoin, but common shareholders appear to own less Bitcoin per share when measured using the company’s own Bitcoin-per-share framework.

Matthew Kratter, a Bitcoin advocate and frequent Strategy critic, argued that the drop in BTC Yield showed the transaction was dilutive. He wrote on X:

“Congratulations to Saylor and Strategy for diluting MSTR shareholders once again over the weekend! Bitcoin per share dropped yet again, and the Saylor simps are too st#pid to understand what’s happening to them.”

Saylor defends Strategy against dilution arguments

Saylor has rejected the view that the latest transaction should be judged only by BTC Yield, arguing that the metric captures Bitcoin per share but does not account for the cash Strategy added to its balance sheet.

His defense rests on a broader framework built around common equity Bitcoin exposure (CEBE).

Under that approach, investors distinguish between Bitcoin per share before senior claims and Bitcoin exposure available to common shareholders after accounting for debt, preferred stock, and cash reserves.

Saylor has described BPS as the growth metric for common equity, while CEBE BPS is the more conservative risk measure because it adjusts for senior claims. BTC Yield, in his view, measures execution on the BPS side of the equation but does not fully capture the company’s residual equity value.

That distinction matters more as Strategy’s capital structure becomes more layered. If obligations are short-dated or expensive, CEBE becomes more important because those claims can quickly weigh on common shareholders.

However, when liabilities are longer dated, and Bitcoin appreciates faster than the company’s financing costs, Saylor argues that BPS better reflects the upside available to common equity.

In view of this, he described the gap between BPS and CEBE BPS as “amplification.” Without debt or preferred stock, the two measures would be the same, and a Bitcoin treasury company would more closely track Bitcoin itself. As liabilities increase, the measures diverge, creating both the possibility of outperformance and the risk of underperformance.

For Saylor, that means Strategy’s liabilities should not be treated as a single risk category. Short-duration, high-cost obligations can turn leverage into a drag, while long-duration, low-cost financing can increase common equity upside if Bitcoin’s annual return exceeds the company’s cost of capital.

In that framework, the latest transaction can look dilutive under a Bitcoin-per-share measure while still appearing accretive when cash reserves and senior claims are included.

On this basis, Saylor argued that a well-capitalized Bitcoin treasury company can outperform Bitcoin over time, provided the asset appreciates faster than the cost of financing the structure.

Market analysts remain split over the balance sheet

Despite Saylor’s detailed defense of the capital structure, institutional analysts remain sharply divided on whether Strategy is creating or destroying value.

Quinn Thompson, chief investment officer at Lekker Capital, criticized the continued equity issuance, arguing that Strategy should strengthen its balance sheet rather than use new capital to buy more Bitcoin.

Thompson said MSTR common trades at about 0.8 times net asset value after accounting for debt and preferred equity liabilities.

He wrote:

“They’re selling MSTR shares that are worth 80 cents on the dollar to buy $1 bills.”

In his view, the issue is not whether common equity issuance can improve the capital structure for creditors. It is whether common shareholders benefit when a company with negative cash flow relies on capital markets to service debt and preferred equity obligations while continuing to buy Bitcoin.

Nic Puckrin, CEO of Coin Bureau, made a similar point, saying Strategy has few clean options left if its common stock trades below the value of its Bitcoin holdings.

According to him, issuing more stock can dilute Bitcoin per share, while issuing more preferred shares would add to future cash obligations. At the same time, selling Bitcoin could damage market confidence, while suspending dividends could drive preferred holders away.

However, Dylan LeClair, director of Bitcoin strategy at Metaplanet, pushed back on that view. He argued that once debt and preferred stock are deducted, the common equity can still trade at a premium because Strategy’s enterprise value exceeds its Bitcoin net asset value.

From that perspective, issuing common stock can be positive for the capital structure. LeClair said the move can increase US dollar net asset value per share and reduce leverage, even if it puts some pressure on Bitcoin per share.

Adam Livingston, an independent market analyst, also supported Saylor’s broader framework. He argued that the latest transaction was accretive once Strategy’s new Bitcoin and larger cash reserve were both included.

By Livingston’s calculation, the 1,587 BTC purchase and roughly $100 million reserve increase added about 3,146 BTC-equivalent to the common residual. That lifted common equity Bitcoin exposure from 145,142 satoshis per share to 145,319 satoshis per share.

He said:

“BTC-only looked dilutive. BTC plus cash was accretive.”

His argument mirrors Saylor’s broader case: Common shareholders do not own only the latest Bitcoin purchase. They own the residual claim on Strategy’s entire balance sheet after debt, preferred stock, and other senior claims are considered.

MSTR’s harder test is investor confidence

The dispute reflects a broader shift in how investors are judging Strategy. During Bitcoin rallies, the company’s model was easier to defend: raise capital, buy Bitcoin, and trade at a premium to the value of its holdings.

However, the current market has been less forgiving. Bitcoin’s decline has compressed that premium, while preferred dividends, debt, and future financing needs have become a larger part of the investment case.

That is why today’s $100 million purchase has drawn attention beyond its size. BTC Yield fell, reinforcing the dilution argument. Cash reserves rose, supporting Saylor’s claim that Strategy’s broader residual value improved.

The next test is whether investors continue to accept that framework. Strategy can keep buying Bitcoin as long as capital markets remain open. The harder question is whether common shareholders will continue to treat the strategy as accretive when their direct per-share Bitcoin claim is declining.

Bitcoin’s latest upward move has sparked debate among market participants, and some believe the rally may have little to do with the purchase announcement that received the most attention. While the acquisition is generally viewed as constructive for the broader market, it is not necessarily the type of development that would justify a significant upward move in Bitcoin price.

Why The Latest Purchase May Not Be Driving Bitcoin Rally

The Bitcoin’s recent move higher is being misinterpreted as a direct reaction to purchase news, when in reality the drivers appear to be more technical in nature. Crypto analyst Aylo has explained on X that the BTC bounce is likely the result of an oversold market finding relief after sweeping key February lows.

Another factor supporting the move higher is the easing of concerns surrounding Strategy and its Bitcoin holdings. The company’s recent sale of a relatively small 32 BTC sparked fears that it could become a larger seller in the future.

Aylo suggests that while the current low may hold in the near term, it remains plausible that BTC could form a slightly lower low in June before a rally, particularly if the broader equity markets experience further weakness. Any deeper stock market shakeout could temporarily drag the price lower before a more sustained recovery begins. This level will be temporary before Bitcoin sees a low later in the year.

Furthermore, the fear that Michael Saylor and Strategy may be forced to liquidate a significant portion of their BTC holdings is likely overstated. The company may need to sell limited amounts to meet specific obligations, but the narrative that a major liquidation event from their supply will be driven more by bearish sentiment.

What The Recent Breakdown Could Mean For The Market

Bitcoin’s recent price action appears to be following a market structure that has played out before during previous corrective phases. A crypto trader known as Max Trades pointed out that roughly a month ago, BTC was entering a distribution phase of this pattern, and the outlook has since played out with notable accuracy.

In this bear market, BTC first formed an accumulation range, where price consolidated before breaking higher and sweeping out the liquidity above the previous highs. However, instead of continuing its upward trajectory, the asset price has transitioned into distribution. Since then, BTC has experienced a significant decline, falling more than 20% from its previous highs.

According to Max Trades, what makes the current setup particularly noteworthy is the comparison to a previous distribution phase that ultimately resulted in substantially deeper downside after the initial breakdown. If the current structure continues to mirror that historical pattern, it could imply that the recent decline is not yet complete.

Andrei Grachev, co-founder of DWF Labs, warned on X that Strategy (formerly MicroStrategy) and BitMine could trigger the largest crypto market crash in history, urging investors to imagine Bitcoin falling to $10,000-$20,000.

This warning lands at one of the most fragile moments for both companies.

A crypto treasury crash happens when major corporate holders are forced to liquidate large positions, pushing prices into a self-reinforcing downward spiral. Grachev believes MicroStrategy and BitMine could become exactly that kind of trigger event.

He framed his post as a thought exercise. The DWF Labs co-founder said he hopes the scenario does not unfold, yet he wants investors to genuinely consider their trading strategy if Bitcoin slides toward the $10,000-$20,000 range.

BitMine and Strategy have all the chances to create the largest market crash in the history of crypto Fingers crossed that it won’t happen, but if it did, what’s your strategy for BTC crash to 10-20k$?

Grachev has consistently warned about leverage and structural risk. He previously described the October 2025 cascade as a “nuclear bomb” event and has spoken about ongoing “liquidity wars” that keep wiping out billions across crypto markets repeatedly.

His core argument focuses on concentration. Two corporate giants now hold massive crypto positions, and any forced selling under financial pressure could amplify weakness across already fragile market conditions and trigger panic among retail and institutional holders.

🚨RETAIL HAS VANISHED FROM THE CRYPTO MARKET

CEX spot volume collapsed to $679 billion, the lowest level since October 2023, as per CryptoQuant.

Spot trading is now down 46% YoY, a staggering -67% drawdown from its October 2025 peak.

Why MicroStrategy and BitMine Sit at the Center of the Storm

MicroStrategy recently incurred approximately $13 billion in unrealized Bitcoin losses, its largest paper loss ever recorded. The firm holds more than 843,000 BTC across its corporate balance sheet.

The pressure runs through its capital stack. Strategy’s variable-rate perpetual preferred stock STRC slipped below $95, according to TradingView data. Meanwhile, MSTR shares have pulled back sharply, and the company recently sold 32 BTC for the first time since 2022.

BitMine sits on a similar problem. The Ethereum-focused treasury holds around 5.28 million ETH and carries over $10 billion in unrealized losses, after acquiring its stack at an average price near $3,500 per token.

FTX Imploded In 2022 And Left Customers With Over $8 Billion In Losses.

Today, Tom Lee’s Ethereum Position Is Down More Than $10 Billion. That’s Over $2 Billion Worse Than One Of Crypto’s Biggest Disasters.

Grachev does not predict the crash. He simply asks investors to mentally prepare for a scenario in which two corporate Bitcoin and Ethereum giants tip the market toward levels not seen since the previous deep bear-cycle low.

Michael Saylor doubled down on his Bitcoin conviction today, but while he did that, his MicroStrategy CEO, Phong Le, sold roughly $11.1 million in company stock tied to the same exposure.

The timing drew attention across crypto markets. Saylor frames Bitcoin as the premier long-term asset, yet the executive running his company trimmed shares that give investors leveraged exposure to that same bet.

Michael Saylor’s Conviction Meets an Inconvenient Sale

He argued the AI capital boom validates Bitcoin rather than threatening it.

“The AI buildout is absorbing capital at historic scale, creating temporary pressure across global markets. That does not weaken Bitcoin. It strengthens the case for scarce, liquid, digital capital. Bitcoin remains the premier asset for the long term,” Saylor explained.

It comes amid market uncertainty as the pioneer crypto continues to show weakness. Some associate that weakness with the latest MicroStrategy BTC sale, a move seen as a symbolic crack in the “never sell” fortress.

To worsen the matter, a regulatory filing shows that on June 5, Le filed to sell 93,738 MicroStrategy (MSTR) shares at a weighted average near $118.73. The proceeds came to about $11.1 million.

It is imperative to note that the sale may not necessarily be a bearish call.

It covered the tax bill on 190,740 performance stock units that vested on June 3. Le still holds 119,925 Strategy shares. Notwithstanding, the timing raises concerns.

“Not a good time to do this,” analyst Ted Pillows remarked.

Why the Optics Sting

The vesting itself sharpens the irony. Those units paid out at 200% because Strategy’s three-year total return ranked in the top quartile of the Nasdaq Composite. The reward for years of outperformance landed in the worst week of the year.

MicroStrategy trades as a leveraged Bitcoin proxy. Investors buy it for the firm’s huge BTC treasury and Saylor’s refusal to sell.

The sales ran through a Rule 10b5-1 plan set in May 2024, so the timing was automatic rather than chosen.

Michael Saylor conceded that the recent Bitcoin selloff reflects a rotation of capital toward AI rather than weakness in the pioneer crypto itself.

He pointed to roughly $4 billion in Bitcoin ETF outflows since May 14, with the king of crypto trading near $64,000 at the time, down about 4% on the day and nearly 49% below its October 2025 record.

Analysts peg 2026 capital budgets at the largest US tech firms above $600 billion. That scale gives his rotation argument some footing.

He cast the ETF redemptions as temporary repositioning, not a structural problem. MicroStrategy holds 843,706 Bitcoin at an average cost near $75,702, per Strategy’s record Bitcoin holdings.

That average now sits well above the market price. With Bitcoin near $64,000, the 843,706 coins are worth about $54 billion against a cost basis near $63.9 billion.

That leaves MicroStrategy about $10 billion underwater on the largest corporate Bitcoin treasury. The loss is unrealized, yet it pressures a stock that trades as a leveraged proxy for the token.

The strain is already visible. A June 1 filing shows Strategy sold 32 BTC to fund preferred-stock dividends, its first sale since 2022. The move was small, yet it showed those obligations now drawing on the same balance sheet.

“Capital markets are funding the AI buildout at historic scale: ~$400B over 6 months. Bitcoin ETFs have seen ~$4B of outflows since May 14, pressuring $BTC. This is a capital rotation, not a Bitcoin impairment. Volatility creates opportunity,” Michael Saylor indicated.

The framing carries an irony, give Michael Saylor rode the same dot-com wave that once broke his company.

MicroStrategy peaked at $333 on March 10, 2000, the day the Nasdaq Composite also topped out. The stock then fell from $260 to $86 on March 20, a one-day drop above 60%.

MicroStrategy (MSTR) Stock Performance in 2000. Source: TradingView

That restatement erased about $66 million in revenue and turned reported profits into losses. Saylor and two executives later paid roughly $11 million to settle fraud charges, without admitting wrongdoing.

Analysts at PFR Capital now explore a possibility where Saylor could rattle markets again.

“In March 2000, MicroStrategy…changed its revenue recognition method…investors started doubting the revenue, profits, accounting quality, and so on of other companies. What happened after that, everyone knows. So you could say MicroStrategy single-handedly crashed the entire market. 26 years have passed. Will MicroStrategy be able to replay its market-crashing magic? Let’s wait and see,” PFR Capital’s Jayson Hu posed.

The parallel is imperfect, however, since the 2000 collapse stemmed from accounting. The current bet rests on transparent, on-chain purchases.

— The Kobeissi Letter (@KobeissiLetter) June 4, 2026

Competing Reads on the Outflows

However, not everyone shares Saylor’s calm. CNBC’s Mad Money host Jim Cramer weighed in as the selling spread. He had touted doomed “new economy” stocks days before the 2000 top.

“Saylor suboptimal move roiling Crypto. Some wags pondering it was only up in the 90s because of Saylor… Seems extreme but it is all i hear,” he noted.

Bloomberg analyst Eric Balchunas described the stretch bluntly, while noting lifetime ETF inflows still top $55 billion. May marked the heaviest Bitcoin ETF outflows of 2026.

BAD TIMES: Bitcoin ETFs in a big step back mode.. $4.4b out over past month which sent the YTD number negative again (it had worked hard to get positive too). That said, some silver lining: $IBIT & a few others STILL positive YTD (unreal) and total net lifetime is still +$55b… pic.twitter.com/VzaijnWhx8