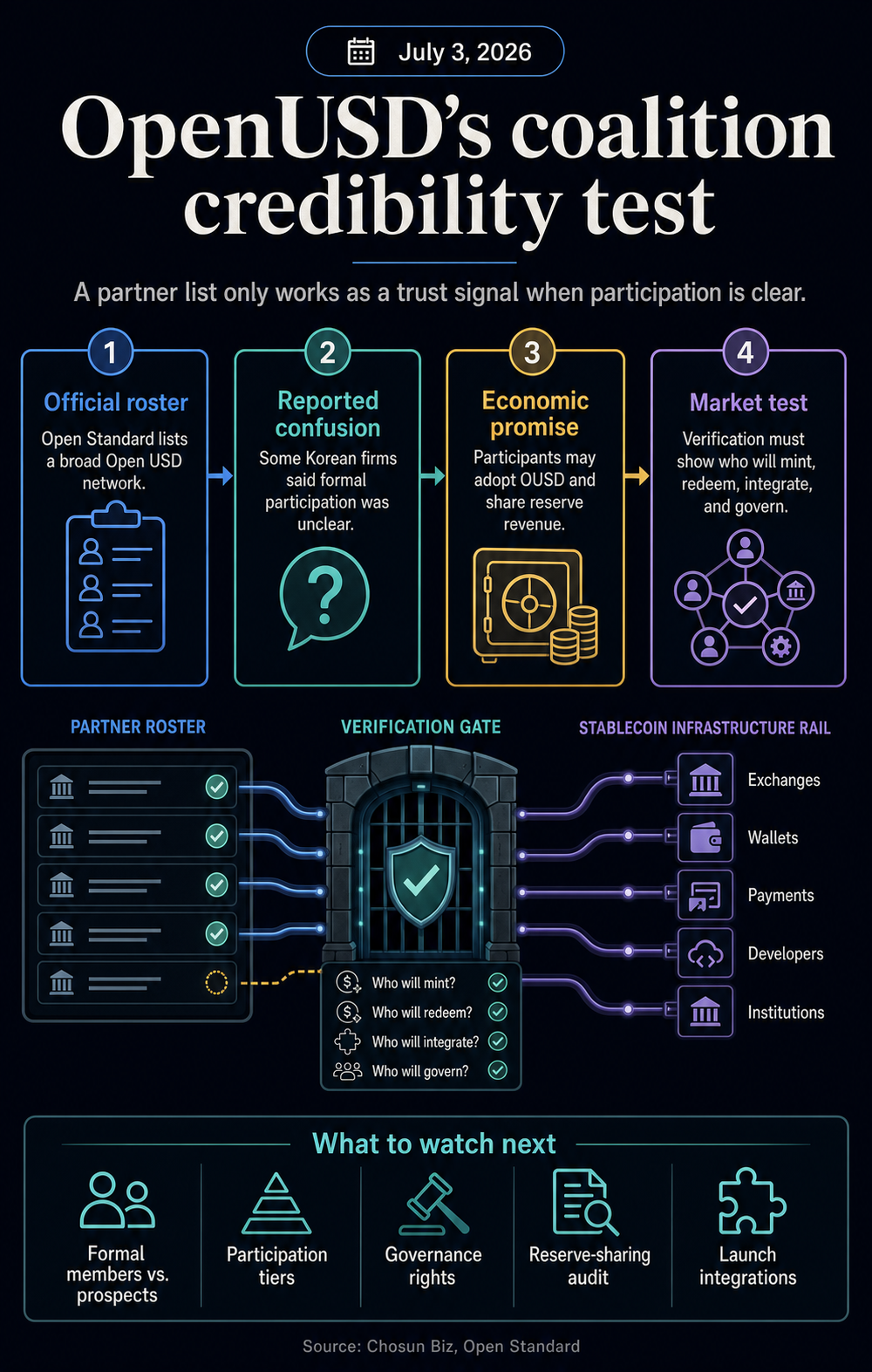

OpenUSD’s first proof point is a formal commitment. The project launched around a sweeping corporate roster, but the roster itself is now the part Open Standard has to explain.

A July 3 Chosun Biz report said several Korean companies named in connection with the OUSD alliance had neither held official consultations with the issuer nor expressed a willingness to review participation.

The report named Samsung Electronics, Shinhan Financial Group, Dunamu, Kbank, and other Korean firms in describing the confusion over how their names appeared in the context of the consortium.

At the same time, Open Standard’s official site still presents Open USD as shared stablecoin infrastructure and displays a long list of global companies under a “backed by” section.

The site positions OUSD as a dollar-stablecoin for financial activity, says Open Standard is the independent company that governs and operates it, and describes participation as adopting OUSD as a core transactional asset, with integration support and the opportunity to earn revenue based on usage.

The tension is now clear. A coalition stablecoin cannot use a large partner count as proof of institutional distribution unless the market can tell which names are formal participants, which are prospects, which are reviewing the model, and which are prepared to put the stablecoin into actual payments, trading, settlement, or treasury workflows.

Why the partner list carries more weight than the launch number

The original pitch positioned OpenUSD as more than another dollar token. Its public positioning points to a different stablecoin model, one built around companies that move money and share in the economics of adoption rather than a single issuer capturing most of the upside from reserve income.

Open Standard says OUSD is designed as open infrastructure for global financial activity. The site says the stablecoin is meant to give businesses the economics, governance and reliability needed to move money, with nearly all reserve economics shared with companies that grow adoption.

It also says reserves are maintained at major financial institutions in compliance with US regulatory requirements and that OUSD is expected to launch later this year.

That makes the roster more than a marketing asset. If participants are expected to adopt OUSD as a core transactional asset, receive technical documentation, receive integration support, and earn revenue based on usage, then the difference between formal participation and informal interest is material.

Chosun Biz’s July 3 report created that distinction in public. Samsung Electronics was cited as saying there had been no official consultations and that it did not know what role it would play.

Shinhan Financial Group, Dunamu, and Kbank were described as saying that Open Standard had asked about their willingness to participate and that they would review it, but their names were included as consortium members.

Another company representative said they learned through Korean media that they had been included.

That confusion does not make OpenUSD’s model impossible. It does make the next credibility threshold much higher. Open Standard can still have a large network, but the useful signal is no longer the list’s size. It is the clarity behind the list.

The distinction is central: partner verification is the bridge between announcement and adoption.

A stablecoin can advertise hundreds of potential distribution points, but users and counterparties need to know which of those points will actually support minting, redemption, settlement, payments, custody, trading, or treasury use.

Without that map, the roster tells readers that conversations happened, not that infrastructure is ready.

Reserve sharing needs verified distribution

Reserve economics are the mechanism that makes OUSD’s partner story significant. In the traditional stablecoin model, the issuer receives dollars, mints tokens, and earns income on reserve assets, subject to its own operating, regulatory, and market structure.

Chosun Biz described OUSD’s model differently: a participating corporation deposits a dollar into Open Standard’s reserve account, Open Standard mints one OUSD, and the corporation can redeem by returning the token for the dollar in its bank account.

The report said participating companies can mint and redeem without stated fees or issuance limits.

Open Standard’s site adds the economic pitch. It says OUSD is designed to return most reserve-generated revenue, minus a small management fee, to participants that adopt and distribute the stablecoin.

In plain terms, the network is asking businesses to treat the stablecoin less as an external product and more as shared financial infrastructure whose use can feed revenue back to the companies that distribute it.

That idea speaks directly to the stablecoin market‘s current bottleneck. USDT and USDC dominate not only because users recognize the tickers, but because liquidity, venue support, redemption confidence and integrations reinforce each other.

OpenUSD’s answer is that a broad set of payment companies, fintechs, exchanges, banks and consumer platforms can create distribution more quickly if they share the economics.

The roster challenge cuts into that answer. If a listed company is merely considering participation, it cannot yet be counted as distribution. If a company has not agreed on its role, it cannot yet signal the depth of its governance.

If a firm does not know whether it is expected to mint, redeem, integrate, settle, or promote OUSD, its name does not tell the market how the stablecoin will reach users.

That is why the Korean confusion is more than a regional communications issue. It tests whether coalition stablecoins can turn brand-name association into verified infrastructure.

The more a stablecoin relies on partner scale as a trust signal, the more precise the public record must be about what each partner has agreed to do.

Governance now becomes part of the product

The governance question is just as important as the partner question. Chosun Biz reported that participating companies would not join through a DAO structure or as shareholders.

Open Standard’s site says Open USD is governed and operated by Open Standard, an independent company with an ownership and corporate governance structure designed to make decisions in the collective interest. It also says governance is collaborative and overseen by Open Standard’s independent management team.

Those statements can coexist, but they leave practical questions with greater weight now.

If listed companies are neither shareholders nor DAO participants, what rights do they have regarding reserve policy, technical changes, compliance standards, partner admission, revenue allocation, or launch timing?

If governance is collaborative, what process turns a participant’s view into a decision? If the roster includes companies at different stages of commitment, do they all have the same role, or are there tiers?

For an issuer-led stablecoin, users mostly ask whether the issuer can maintain the peg, manage reserves, support redemptions, and comply with applicable rules. For a coalition stablecoin, the credibility surface is wider.

The market has to evaluate the issuer and the network together.

That is the part OpenUSD cannot solve with a longer list. A partner roster is only useful if it maps to obligations, incentives, and operating roles. Otherwise, the list risks becoming a soft signal attached to a hard financial product.

The next useful disclosure would be simple: a roster that separates formal participants from companies reviewing participation, a definition of each role, and a clear account of what adoption means before launch.

Open Standard could also clarify whether participants have governance authority, economic participation only, technical access, future integration rights, or some mix of those categories.

Those disclosures would help separate operational readiness from reputational reach. A payment company that will settle OUSD flows is different from a firm that is examining the economics.

A bank or card issuer with a defined minting and redemption path is different from a company listed because it joined exploratory talks. Coalition stablecoins need that distinction to avoid turning every future roster into a due diligence exercise for the market.

The next test is verification, not scale

OpenUSD’s opportunity remains obvious. Stablecoins are moving from crypto-native trading rails into payments, remittances, merchant settlement, fintech balances and institutional money movement.

A neutral asset backed by companies that already touch those flows could challenge the idea that stablecoin distribution has to be issuer-led.

But that opportunity depends on trust signals that survive scrutiny. A reserve-sharing model asks partners to help grow usage. An institutional distribution model asks the market to believe those partners can bring real payment and settlement volume.

A collaborative governance model asks readers to believe that decisions will be made by more than a single sponsor behind a long list of logos.

The partner confusion reduces all three claims to a single near-term test. Open Standard does not need to publish every commercial agreement to keep the OUSD thesis alive.

It does need to make the public meaning of participation clear enough that a company name cannot be mistaken for a commitment the company itself does not recognize.

OpenUSD now turns on a more practical question: whether the companies on the list are committed in a way that users, counterparties, and other institutions can understand.

For coalition stablecoins, that may become the rule beyond OUSD. Partner count can open the door, but verification decides whether the market treats the coalition as infrastructure or as a launch roster still waiting to become real distribution.

The post OpenUSD’s partner mix-up puts its stablecoin alliance under scrutiny appeared first on CryptoSlate.