Crypto markets have had plenty to digest today, and this development adds another layer to the picture. Ethereum Institutional Backers Launch Independent Non-Profit to Target Wall Street Wealth gives NewsBTC readers a clean angle on Ethereum at a point where the market is trying to separate durable signals from short-lived noise.

According to the source material reviewed for this report, the story turns on a few concrete details rather than vague sentiment. That matters because crypto headlines can move quickly, but the pieces that tend to last are the ones backed by filings, official releases, data dashboards, or protocol-level records.

TL;DR

Ethereum co-founder Joseph Lubin, alongside ETH treasury firms BitMine and SharpLink, backed the launch of ‘Ethereum Institutional’.

The new group is an independent non-profit designed to serve as a ‘front door’ for Wall Street banks and asset managers on tokenization and stablecoins.

This organization aims to take over business development roles from the Ethereum Foundation, which is focusing more on core research.

A Fresh Signal For The Market

The immediate relevance is that this development fits into one of the market’s main themes for the day: institutional positioning, network usage, regulatory pressure, protocol development, or asset-specific rotation. In this case, the key topic is Ethereum, which is why it deserves a dedicated read rather than being buried inside a broader market recap.

For traders, the useful part is not simply that the headline exists. It is the way the facts line up with the current market backdrop. When official sources, market data, or protocol records show a fresh shift, readers get a better sense of whether the move is just a one-day reaction or part of something more structural.

The Numbers That Matter

The core source for this story is prnewswire.com with supporting data from globenewswire.com. That source trail is important because the final article should not rely on discovery-only media links or second-hand summaries.

Ethereum co-founder Joseph Lubin, alongside ETH treasury firms BitMine and SharpLink, backed the launch of ‘Ethereum Institutional’.

The new group is an independent non-profit designed to serve as a ‘front door’ for Wall Street banks and asset managers on tokenization and stablecoins.

This organization aims to take over business development roles from the Ethereum Foundation, which is focusing more on core research.

The numerical claims in the pack were tied back to specific source material before writing. ‘July 1, 2026’ sourced from Ethereum Institutional official launch release date

The Important Caveat

The caution is just as important as the headline. Do not state this is an official Ethereum Foundation spin-off; it is a separate non-profit.

That means the cleaner read is to treat this as a confirmed development with a defined scope, not as proof of a guaranteed price move or a sweeping market shift. In crypto, the difference matters. A verified data point can strengthen a thesis, but it does not remove execution risk, liquidity risk, regulatory uncertainty, or the possibility that traders fade the initial reaction.

For now, the story gives the market another piece of evidence to weigh. If follow-up filings, dashboard updates, protocol records, or official statements confirm further momentum, the angle can develop into something larger. If not, it still stands as a useful snapshot of where activity is concentrating today.

The BeInCrypto Institutional 100 Awards 2026 enters its final stage with the Tokenization & On-Chain Finance pillar narrowed to 16 shortlisted firms across four categories.

This pillar focuses on the firms building the regulated infrastructure for tokenized real-world assets, on-chain settlement, stablecoin payments, and autonomous agent payments.

The winners were announced at Proof of Talk in Paris on June 2, 2026. The firms listed below are alphabetized within each category. They are not ranked.

Welcome to the BeInCrypto x @ProofOfTalk Institutional 100 Awards, live from the iconic Louvre Palace in Paris.

Tonight we recognize the institutions and leaders shaping the future of digital asset finance across 25 categories.

This category recognizes platforms bringing regulated securities, money market funds, real estate, and private credit on-chain at institutional scale.

Shortlisted Firm

Why It Made the Shortlist

Apex Group

Apex Group, which services $3.5 trillion in assets, operates Tokeny. In March 2026, Tokeny launched the T-REX Ledger on Polygon as a multi-chain orchestration layer for ERC-3643 assets. The platform has set a $100 billion tokenization target by June 2027.

Figure

Figure listed on Nasdaq under FIGR in September 2025. The company has originated more than $20 billion in loans on Provenance Blockchain. In early 2026, it also launched the On-Chain Public Equity network and tokenized FIGR stock.

Franklin Templeton

Franklin Templeton’s BENJI tokenized money market fund suite crossed $1.98 billion in AUM by April 2026. The fund is now deployed across more than eight public blockchains, giving it the broadest chain coverage among institutional tokenized funds.

Securitize

Securitize held its position as the largest tokenization platform by AUM. It posted record Q1 2026 revenue of $19.5 million and powers BlackRock’s BUIDL, which now holds more than $3 billion in assets. The firm also has a $1.25 billion SPAC merger with Cantor Equity Partners II in progress.

Best On-Chain Finance Infrastructure

This category recognizes the infrastructure firms providing the cross-chain, deposit-token, wallet, and settlement layers that make institutional on-chain finance work.

Shortlisted Firm

Why It Made the Shortlist

BitGo

BitGo became the first crypto-native infrastructure firm to list on the NYSE, trading under BTGO in January 2026. The company raised $212.8 million at a $2.08 billion valuation and supports roughly $104 billion in assets across wallet, custody, and settlement services.

Chainlink

Chainlink CCIP secures $33.6 billion across more than 60 blockchains. Its SWIFT integration creates a path for more than 11,000 banks to access on-chain finance. Chainlink also has major institutional partnerships with UBS, Mastercard, DTCC, and Euroclear.

J.P. Morgan

Through Kinexys, J.P. Morgan brought JPM Coin, now JPMD, to public blockchains. The rollout included Base in 2025 and Canton Network in January 2026. The bank is also working on tokenized-deposit interoperability with DBS.

Privy

Stripe acquired Privy in June 2025 to expand its on-chain infrastructure stack. Privy’s embedded wallet API now powers more than 75 million accounts across 1,000-plus developer teams, including Hyperliquid, OpenSea, and Farcaster.

Best Stablecoin Infrastructure

This category recognizes firms powering the issuance, distribution, and settlement of regulated stablecoins across crypto markets, B2B payments, and global card networks.

Shortlisted Firm

Why It Made the Shortlist

Circle

Circle issues USDC, the second-largest stablecoin globally. USDC circulation rose to $75.3 billion by Q4 2025, while Circle reported $1.25 billion in H1 2026 revenue after its June 2025 NYSE IPO and the passage of the federal GENIUS Act.

Mastercard

Mastercard’s Multi-Token Network supports USDC, EURC, USDG, PYUSD, FIUSD, and SoFiUSD. Its March 2026 partnership with SoFi made SoFiUSD the first stablecoin issued by a US nationally chartered bank on a public blockchain.

Paxos

Paxos issues USDG, PYUSD, USDP, and PAXG. USDG supply reached roughly $2.75 billion by May 2026 through the Global Dollar Network, which shares reserve revenue with distribution partners. Paxos operates under MAS, MiCA, and NYDFS oversight.

Visa

Visa’s stablecoin settlement volume reached a $7 billion annualized run rate by April 2026. The network expanded to nine blockchains and supports USDC settlement for US issuers and acquirers through Cross River Bank and Lead Bank.

Best Autonomous Agentic Payments Platform

This category recognizes platforms building production payment rails for autonomous AI agents. These systems use stablecoins and open standards such as x402 to settle machine-to-machine transactions.

Shortlisted Firm

Why It Made the Shortlist

Circle

USDC anchors major agentic payment systems across Coinbase’s x402 network and Solana’s Pay.sh. Circle is also building Arc, a Layer 1 blockchain designed for stablecoin settlement and agentic commerce.

Coinbase

Coinbase launched Agent.market in April 2026 on the x402 protocol. The network already has more than 69,000 active AI agents settling over 165 million transactions worth $50 million in USDC, mainly on Base.

Mesh

Mesh reached a $1 billion valuation after a $75 million Series C in January 2026. Its AI Wallet allows agents to transact across more than 300 wallets and exchanges. Stellar and Tempo were added as settlement layers in May 2026.

Solana

The Solana Foundation launched Pay.sh with Google Cloud in May 2026. The open-source agentic payment gateway uses x402 and stablecoins on Solana. The network processed roughly $650 billion in stablecoin volume in February 2026.

About the BeInCrypto Institutional 100

The BeInCrypto Institutional 100 is an annual research program covering 25 categories across six pillars: Capital Markets & Infrastructure, Access to Digital Assets, Tokenization & On-Chain Finance, Enterprise Blockchain, Regulation & Governance, and Retail to Crypto Bridge.

The 2026 evaluation window ran from April 2025 through March 2026.

Shortlists were selected through BeInCrypto’s editorial research methodology and blind scoring by an external panel of institutional digital asset practitioners.

Each category follows one of three scoring tracks, depending on the data profile of the market. Public filings, regulatory registers, audited reports, on-chain data, ETF flow trackers, and nominee disclosure forms were used where available.

Final blended scores are not published. Inclusion on the shortlist reflects the combined outcome of research and judge review.

Ethereal Ventures: Blockchain Is Now the Backend for Global Finance

Crypto Coin Show · Market IntelligenceMay 2026

Venture Capital · Research Report

Ethereal Ventures: Blockchain Is Now the Backend for Global Finance

In its Q1 2026 market insights report, Ethereal Ventures maps five core metrics — dealflow, tokenized real-world assets, payments volume, protocol fees, and token holder distributions — to argue the on-chain migration of traditional finance has barely started.

Ethereal Ventures’ Q1 2026 Digital Asset Market Insights report opens with a blunt thesis: the five metrics it tracks — dealflow composition, tokenized real-world assets, blockchain payments, on-chain protocol fees, and value returned to token holders — all point toward an industry that has moved well past proof-of-concept and into the early innings of genuine financial infrastructure adoption.

The headline number is $29.3 billion in real-world assets now tokenized on-chain, representing a 30× increase over four years. Impressive on its face — until Ethereal frames it against US equity market capitalization, where it represents less than 0.05%. Their conclusion: the migration has barely started.

01Where Founders Are Betting Their Time

Dealflow composition is the leading indicator Ethereal trusts most, on the premise that founders are the best arbiters of where value will compound. This quarter’s inbound pipeline tells a clear story.

32%

AI

20%

DeFi

8%

Payments

6%

Prediction Markets

5%

Applications

5%

Stablecoins

Key Insight

AI is drawing the bulk of talent and capital — but the parallel story is blockchains maturing into the API backend for payments and broader financial activity. Stablecoins and payments are one slice of that compounding interest, as the rails for on-chain commerce keep maturing.

02Real-World Assets: 30× in Four Years

Tokenized real-world assets — the canonical measure of how much traditional finance has actually moved on-chain — reached $29.3 billion as of April 13, 2026. US Treasuries lead the composition, followed by commodities and asset-backed credit. The growth trajectory is steep: +46% in one year, +266% over two years.

Asset Class

Description

Value On-Chain

US Treasury Debt

Tokenized government bonds — leading category

$13.4B

Commodities

Gold, silver, and physical asset-backed tokens

$5.4B

Asset-Backed Credit

Private credit structured on-chain

$3.1B

Specialty Finance

Structured lending and receivables

$1.5B

Non-US Govt Debt

Sovereign bond tokenization outside the US

$1.2B

Stocks

Equity tokenization on public blockchains

$1.0B

Active Strategies

On-chain managed funds and yield vaults

$919M

Venture Capital

Tokenized fund positions and LP interests

$818M

Corporate Credit

Tokenized corporate bonds

$716M

Real Estate

Property fractionalization and REITs on-chain

$297M

Total RWA On-Chain

$29.3B · +30× in 4 years

The Ethereal framing is important here: $29.3B is not a failure to scale, it is a starting line. US equities alone represent roughly $50 trillion. Tokenized assets at current levels are a rounding error — but the infrastructure to absorb orders of magnitude more institutional capital is, by Ethereal’s read, now mature enough to do it.

03Stablecoin Payments: $390 Billion Annualized

Monthly stablecoin payment volume has tripled over three years to $10 billion per month, driven primarily by B2B settlement flows. McKinsey and Artemis data cited in the report puts full-year 2025 stablecoin payment volume at $390 billion annualized once B2B custody flows and cross-border remittances are included.

“+3× in three years to $10bn/mo, against Visa and Mastercard’s mid-single-digit CAGR.”

The comparison to card networks is deliberate. Visa and Mastercard process roughly $2.27 trillion per month combined. Blockchain-based payments are at less than 0.5% of that — but the unit economics of on-chain settlement improve with scale in ways the card stack structurally cannot match. Ethereal’s projection: the first $1 trillion per month arrives via B2B capture; consumer flows follow as embedded wallets reach mainstream apps.

$390B

2025 Annualized Volume

+3×

Growth Over 3 Years

$2.27T/mo

Visa + Mastercard Target

04Protocol Fees: The Bear-Cycle Floor Keeps Rising

Daily protocol fees — the metric that strips away token price noise to show what users are actually paying to use blockchains — have established a structural floor of $50 million per day, holding through every major market drawdown since 2020. The 30-day moving average currently runs above that floor.

Key Insight

Zero to $50mm/day in six years at the bear-cycle floor. The baseline keeps ratcheting up regardless of price action — the clearest signal that demand is structural, not reflexive.

Ethereal projects fees scaling on two compounding curves: surface area (more product categories entering DeFi — prediction markets, perp DEXes, on-chain credit, RWA distribution) and intensity (institutional users transacting in larger size, with higher willingness to pay for settlement finality). Their target: a $500 million per day baseline.

05Token Holders Are Starting to Look Like Shareholders

Perhaps the most structurally significant finding in the report: capital returned to token holders has tripled since 2024, now running at 15–22% of protocol revenue versus 4–7% across 2022–2024. The shift is being led by Hyperliquid, whose 99%-of-fees buyback model has become the benchmark the rest of the industry is now measured against.

The implication, if the trend continues: tokens stop trading as speculative commodities and begin pricing like cash-flowing assets, attracting a fundamentally different and larger buyer base — one that includes traditional equity investors currently sitting on the sidelines.

06Six Predictions: Where We Are vs. Where We’re Going

The report closes with six explicit prediction pairs — current state versus projected destination — that frame Ethereal’s investment thesis for the next three to five years.

Money on Blockchains · Now

~$480B on-chain

↓ TRAJECTORY

Projected Destination

Majority of US M2 ($21.7T)

Stablecoin Payments · Now

$10B / month

↓ TRAJECTORY

Projected Destination

Visa + Mastercard stack ($2.27T/mo)

Companies Using Blockchains · Now

~38% of SMBs

↓ TRAJECTORY

Projected Destination

~100% of companies touching finance

DeFi Daily Active Users · Now

~300K DAU

↓ TRAJECTORY

Projected Destination

>30M DAU via embedded wallets

Protocol Fees · Now

$50M/day floor

↓ TRAJECTORY

Projected Destination

$500M/day baseline

Value to Token Holders · Now

15–22% of revenue

↓ TRAJECTORY

Projected Destination

Majority of fees flowing to holders

07Where Ethereal Sees the Next Breakthroughs

The report’s outlook section categorizes emerging opportunities across three buckets: new market infrastructure, TAM overhauls where AI is rewriting addressable markets, and blue ocean frontiers with undefined outcome shapes.

Bucket 01New Market Infrastructure

The New Intent Exchange

A neutral matching layer beneath AI agent platforms where merchants compete on price for commercial intent, settled in stablecoins.

Agentic Commerce Risk Rails

Programmable spending limits and on-chain escrow built for agent transactions — reversibility designed in, not retrofitted.

Parametric Insurance On-Chain

Instant-payout policies for measurable events: weather delays, satellite launches, AI SLA failures.

Supply-Chain Disintermediation

Agent-queryable factory profiles, attested quality data, and stablecoin settlement collapsing 40–80% intermediation margins in global retail.

Bucket 02TAM Overhauls

Agent Payments and Stablecoins

Agents can’t open bank accounts but can hold wallets. Agent-to-agent flows are the most open frontier, needing new micropayment frameworks at machine speed.

AI Fraud Defense

The next fraud stack moves from scoring events to verifying actors — portable, privacy-preserving credentials that prove identity once and plug in anywhere.

Devtools Are Now Mainstream Tools

Agentic engineering exploded what was historically a tiny market. The durable layer: tooling where the customer is the agent and the human is out of the loop entirely.

The Crypto Credit Highway

Crypto wins as rails between capital pools and origination, not as a replacement underwriter. Wedge: SMB/B2B lending where stablecoin escrow enables new cashflow mechanics.

Bucket 03Blue Oceans

Machines as Autonomous Companies

A progression from AI-native funds to agents running companies end-to-end, dispatching humans to perform tasks via real-time capital flows.

Proof-of-Human Traffic Bifurcation

Publishers charge agents at scale via micropayments; verified humans browse for free. A new content monetization stack for the post-AI-flood web.

Markets for Scarce Rights

Tokenization and dispute resolution for bureaucratically-gated rights: satellite slots, drone air corridors, spectrum bonds, congestion pricing.

Agent-Native Trust and Reputation

A canonical, queryable trust profile for suppliers, merchants, and services — built on machine-readable signals like fulfillment rates and certified quality attestations.

The full Ethereal Ventures Q1 2026 report is available on their Substack: The Maturation of the On-Chain Economy. All figures sourced from RWA.xyz, Artemis, DefiLlama, and McKinsey × Artemis (Feb 2026).

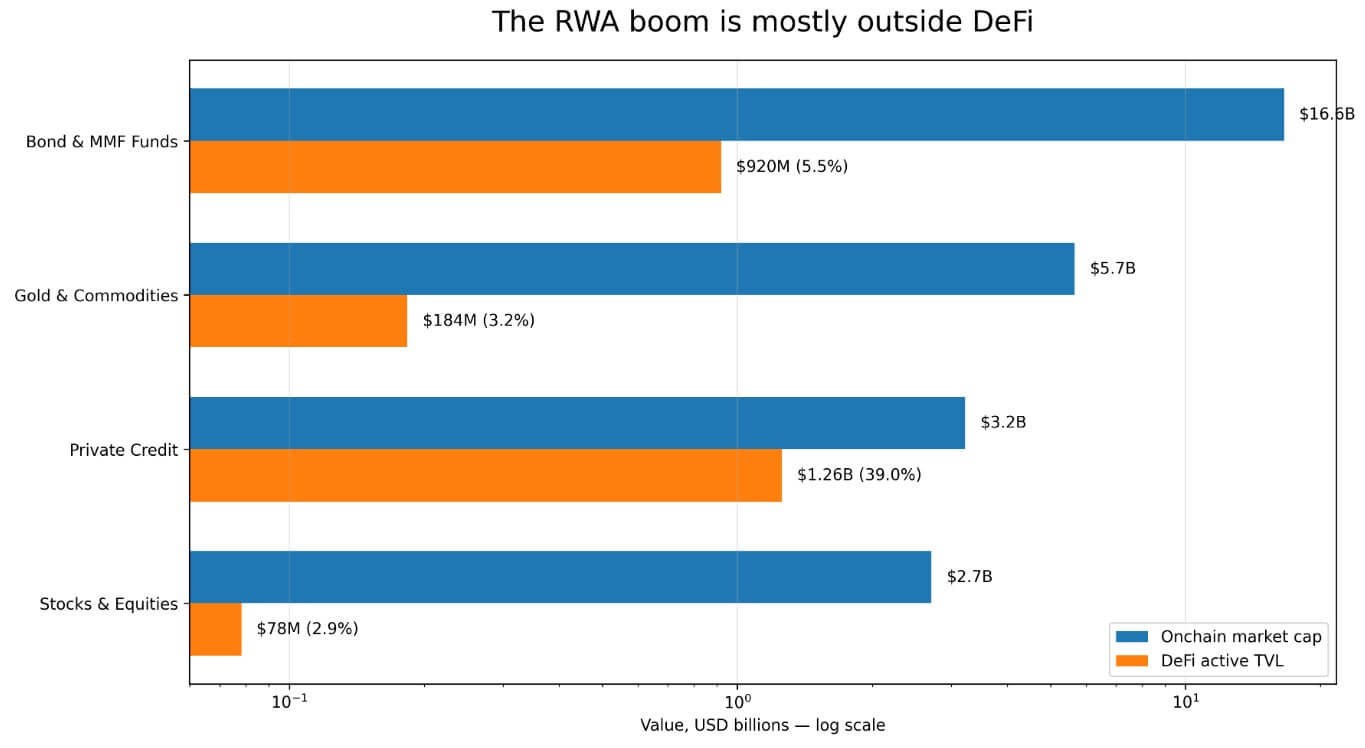

DefiLlama’s RWA category data puts the RWA tokenization market near $30 billion on-chain, with only $2.47 billion appearing as DeFi active TVL, the value actually deposited or pooled inside third-party DeFi protocols the platform tracks.

The rest of the tokenized real-world assets market sits outside the lending markets and collateral vaults that make crypto assets composable. Bond and money market funds are the largest single RWA category at over $16.6 billion on-chain, yet they carry only $920 million in DeFi active total value locked (TVL).

Gold and commodities sit at $5.7 billion on-chain against $183.6 million in DeFi, while stocks and equities contribute $2.7 billion on-chain against $78.27 million in DeFi.

Private credit stands apart with $3.226 billion on-chain and $1.257 billion in DeFi active TVL, a 39% ratio, driven by protocols like Maple Finance and Centrifuge that built their products as lending instruments from inception.

Issuers built categories such as Treasury funds, gold, and equities for institutional holding and regulated fund architecture.

A log-scale bar chart comparing onchain market cap to DeFi active TVL across four RWA categories, with private credit at 39% DeFi utilization.

DefiLlama classifies BlackRock’s money market fund, BUIDL, as permissioned and records only $18.9 million in DeFi active TVL for the fund.

IOSCO’s November 2025 final report on financial asset tokenization noted that BUIDL created a permissioned system on public blockchains for issuance, custody, secondary trading between allowlisted qualified investors, dividend distribution, and redemption.

Prospective holders must clear a Securitize-managed allowlist, and on-chain transactions carry no legal effect until a transfer agent reconciles them with the off-chain record.

That makes BUIDL a compliance infrastructure that runs on blockchain rails for institutional holding and transfer-agent reconciliation. The fact that the fund’s contracts interact only with allowlisted addresses prevents direct deposit into open protocols like Aave or Uniswap without a compliant wrapper in between.

BlackRock’s February 2026 Uniswap integration moved a portion of BUIDL onto the platform. Still, Securitize controls the list of eligible institutions and market makers, and access stays restricted to qualified purchasers with at least $5 million in assets.

IOSCO found that secondary trading of tokenized money market funds (MMFs) generally operates this way and concluded that the sector has yet to deliver the promised secondary-market liquidity benefits.

RedStone’s March 2026 tokenization report identified that the hardest part of tokenization is handling compliance, identity, transfer restrictions, sanctions, and corporate actions across jurisdictions and chains. That makes Morpho and Aave Horizon the clearest RWA DeFi examples in the current data set.

Every additional compliance constraint a platform builds in makes the asset harder to integrate into DeFi, and issuers of tokenized Treasuries, Treasury funds, and MMFs built those constraints in by design to satisfy their regulated investor base.

Constraint

What it means

Why it limits DeFi use

KYC / allowlisting

Only approved wallets can hold or transfer the asset

Open DeFi pools cannot freely accept the token

Transfer-agent reconciliation

Onchain movement may need offchain legal confirmation

Smart contracts alone may not finalize ownership

Qualified-investor limits

Access is restricted to institutions or high-net-worth buyers

Retail DeFi liquidity is excluded

NAV / redemption windows

Fund shares redeem on issuer schedules

Hard to fit real-time AMMs or collateral liquidations

Centralized venue trading

Activity occurs on CEXs or issuer platforms

It does not appear in DeFi Active TVL

The gold and commodities category adds a third dimension to the stack, as CoinGecko data showed that tokenized gold spot volume hit $90.7 billion in the first quarter of 2026, surpassing the full year 2025. Yet centralized exchanges account for the vast majority of spot trading for tokenized assets.

The $183.6 million DeFi active TVL figure for the category reflects activity concentrated on centralized venues, which falls entirely outside DefiLlama’s DeFi protocol tracking.

Where the bull case lives

Ondo’s USDY crossed $1 billion in TVL in early 2026 and operates across nine blockchains. Ondo Global Markets, which launched in September 2025 to offer tokenized US stocks and ETFs to non-US investors, built its tokens for free transferability and DeFi collateral acceptance, reaching $650 million in TVL and over $12 billion in cumulative trading volume.

RedStone’s report counts over $620 million in RWA deposits on Morpho and $423.5 million in total market size on Aave Horizon, two lending protocols that have made RWA collateral a functional product.

These products demonstrate that composability is achievable at the issuance level when designers build for permissionless circulation from the start.

DWF Labs’ April 2026 roundtable with participants from Centrifuge, Falcon Finance, and xStocks concluded that the RWA market is bifurcating into two lanes: one for ownership-first, permissioned rails, and another for composability-first designs that combine compliant issuance with secondary-market utility.

Centrifuge’s Graham Nelson said that strict allowlisting prevents an asset from entering open pools when every pool participant must be individually onboarded.

Centrifuge’s DeRWA approach addresses this by wrapping compliant primary issuance with freer secondary transferability. Falcon Finance’s Artem Tolkachev called composability and exit mechanics the bridges between real-world assets and crypto liquidity.

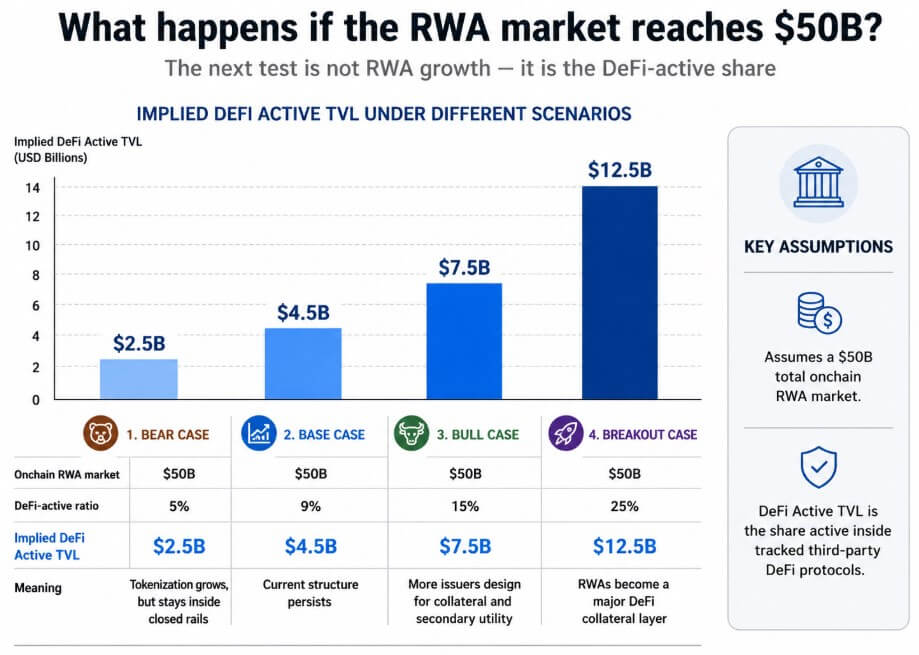

The bull case is that enough of the market moves in this direction to pull the DeFi-active ratio meaningfully above 9% as the total on-chain RWA market approaches $50 billion.

IOSCO’s November 2025 report found that tokenized assets still largely rely on conventional financial infrastructure for distribution and secondary trading because of accessibility and liquidity constraints on DLT platforms.

The ECB noted in its April 2026 tokenization research that the lack of common standards can entrench tokenized markets as isolated pools, each with its own compliance framework, settlement layer, and access model, thereby concentrating liquidity within closed networks.

Bond and MMF funds at 5.5%, gold and commodities at 3.2%, and stocks and equities at 2.9% put numbers to that structural separation.

Most tokenized Treasury and MMF products carry minimum investment thresholds, KYC requirements, transfer-agent reconciliation cycles, and NAV-aligned redemption windows that are structurally incompatible with real-time AMM pricing or permissionless collateral vaults.

Regulators required these features, and issuers accepted them.

Two markets, one scoreboard

The $30 billion figure and the $2.47 billion DeFi active TVL figure measure two distinct markets the industry groups under the same RWA label.

One is regulated on-chain finance, consisting of MMFs, Treasury funds, custody rails, and issuer-managed records reconciled by transfer agents. The other is DeFi composability, comprised of assets deposited in lending protocols, used as permissionless collateral, and integrated into automated yield strategies.

A scenario chart projecting implied DeFi active TVL at a $50B RWA market across four cases, ranging from $2.5B at a 5% bear-case ratio to $12.5B at a 25% breakout ratio.

Morpho’s $620 million in RWA deposits and USDY’s nine-chain footprint show the second market has real traction.

For the DeFi-active ratio to surpass 9%, issuers would have to choose a structure that allows permissionless circulation by design instead of the BUIDL architecture, where the compliance structure is the product.

With most of the current $28.56 billion in on-chain market cap in the permissioned camp, tokenized assets still look more like regulated on-chain finance than open DeFi collateral.

Best Stablecoin Infrastructure is a category within the BeInCrypto Institutional 100, an annual research-driven program recognising institutional digital asset excellence across 26 categories and six pillars.

This category sits under Pillar 4: Tokenization & On-Chain Finance. The 15 firms below are listed alphabetically and are not ranked. A shortlist will be named in May 2026, with the winner announced at Proof of Talk in Paris on June 2–3, 2026.

Key Facts

Long list: 15 firms across fiat-backed dollar stablecoins, MiCAR-compliant euro and multi-currency issuers, Asian dollar stablecoins, DeFi-native stablecoins, white-label platforms, yield-bearing stablecoins, bank-issued stablecoins, and payment networks.

Initial pool: More than 30 stablecoin issuance and infrastructure firms screened; 15 advanced to the long list

Order: Listed alphabetically, not ranked.

Scoring: 50% quantitative data · 50% Expert Council.

BlackRock and VanEck selected RLUSD as redemption rail for tokenized Treasury funds

Deutsche Bank integration, SBI Japan rollout, and Deloitte attestations

About This List

The BeInCrypto Institutional 100 — Best Stablecoin Infrastructure (2026 Long List) identifies firms that underwrite, issue, settle, and distribute stablecoins at an institutional scale.

The list spans fiat-backed dollar issuers, MiCAR-compliant euro and multi-currency issuers, regulated Asian dollar stablecoin issuers, DeFi-native decentralized stablecoins, white-label issuance platforms, yield-bearing stablecoins, tokenized treasuries, and payment networks operating stablecoin settlement rails.

Tether USDT, Tron USDD, World Liberty Financial USD1, Plasma Network, and Ethena Labs are excluded under reputational and enforcement filters applied across the program.

Methodology

This category is evaluated under Track A of the BeInCrypto Institutional 100 methodology: 50% based on quantitative metrics and 50% on Expert Council scoring.

Assessment spans seven criteria: stablecoin market capitalization and on-chain volume, institutional adoption, regulatory and reserves posture, multi-chain distribution, enterprise integration depth, innovation signal, and ecosystem dominance.

The 50/50 split reflects the availability of quantitative stablecoin data, including on-chain market capitalization, transaction volume, and reserve attestations, balanced against Expert Council assessment of regulatory durability, reserve quality, governance, and product innovation.

Data was verified using regulatory registers, issuer reserve attestations, audited filings, SEC EDGAR, exchange disclosures, partnership announcements, and on-chain analytics providers including CoinGecko, CoinMarketCap, and DefiLlama. Nominees were also reviewed against negative-signal queries covering enforcement, security breaches, depegs, active litigation, and reputational controversy during the award window.

CMT Digital: Capital Markets Are Going Onchain | Crypto Coin Show

Institutional Perspective · Venture Capital

Capital Markets Are Going Onchain. CMT Digital Is Already There.

Partner Sam Hallene on why 2026 is the year crypto gets boring — and why that’s the biggest bull case yet for stablecoins, tokenization, and the re-architecture of global finance.

A Trading Firm’s Bet That Blockchain Becomes Finance’s Backbone

CMT Digital is the blockchain and digital-assets arm of CMT Group — a quantitative trading firm operating for nearly 30 years. That heritage shapes everything. CMT entered crypto in 2013 through the lens of counterparty risk mitigation, then sharpened its focus when the Ethereum whitepaper made clear that smart contracts could run financial logic natively onchain. A venture thesis formed, and CMT has been building its portfolio around it ever since.

Today the firm manages over $500M across four funds, with 200+ companies and a number of unicorns — including early positions in Circle, Coinbase, FalconX, Ethena, Figure, and ConsenSys. In November 2025, CMT closed Fund IV at $136M, one of the largest crypto VC raises in a difficult fundraising environment. Watch the full interview above for Partner Sam Hallene’s background and full story.

Fund Evolution

Four Funds, One Through-Line

Fund I · 2017

Establishing Access

Early positions in Coinbase and Circle — the first platforms giving retail and institutions a compliant way into digital assets.

Fund II · $130M

Building Infrastructure

Market structure, custody, compliance rails. ConsenSys, FalconX, and the developer tooling layer.

Fund III · $100M

Utility and Application

DeFi protocols with real product-market fit: Ethena, Maple, Zero Hash, Coinflow — companies where onchain rails produced measurably better outcomes.

Fund IV · $136M · Nov 2025

Re-architecting Global Finance

Stablecoins, tokenization, institutional derivatives, prediction markets. The thesis has arrived — now it’s about deployment at scale, re-architecting the core plumbing of global finance on modern rails.

Market View

“2026 Is the Year Crypto Gets Boring”

Hallene delivered this line with a grin — and it deserves unpacking. “Boring” is the highest compliment a market infrastructure investor can pay. When regulatory frameworks solidify, when tokenized loans trade as freely as any other asset class, when stablecoin yield flows to end users through apps they already use — the speculative premium evaporates and the utility premium takes over. That’s the transition CMT Digital is betting on.

“Now has never been a better time to start a company. A lot of binary variables have swung positive.”

Sam Hallene, Partner — CMT Digital

The macro backdrop is structural, not speculative. The GENIUS Act is live, giving institutions a regulatory playbook for compliant stablecoin issuance. The SEC and CFTC have issued joint guidance. The US Treasury has a direct incentive to promote stablecoin adoption — stablecoins are currently among the largest marginal buyers of US treasuries. Hallene’s contrarian read: sentiment has lagged fundamentals. Bitcoin soft and a quiet altcoin market have dampened enthusiasm, but for a firm with CMT’s institutional orientation, that gap is exactly where long-term alpha compounds.

01

Stablecoins as rails

The dollar goes onchain first. Everything else follows. Regulatory clarity is forcing every major tech company to contemplate stablecoin issuance.

02

Tokenization compounds

Real-world assets gain liquidity, provenance, and programmability onchain. Cost savings force adoption — Figure proved it at 150bps.

03

Derivatives mature

As institutions enter, demand for structured hedging and volatility strategies intensifies. Options are the next frontier after perps.

04

Information markets

Prediction markets are becoming mainstream signals. The next generation moves toward real-time sentiment pricing with demographic intelligence.

Deep Dive · Stablecoins

Distribution Is King — And the Battle Has Just Begun

Tether captured global demand from populations seeking dollar access outside US institutional trust. Circle captured the compliance-conscious business community. Both are entrenched. But the GENIUS Act reshapes the competitive dynamics entirely.

A compliant stablecoin issuer cannot differentiate on the collateral side — the rules constrain what you can do with backing assets, by design. Differentiation shifts entirely to distribution. And distribution belongs to whoever already owns the customer relationship: Apple, Google, PayPal, Shopify, every major bank. The yield-sharing question is the most consequential unresolved variable. The GENIUS Act prohibits paying yield directly on the stablecoin, but doesn’t prevent revenue-sharing agreements with distribution partners — the Circle-Coinbase model is the template. If the Clarity Act extends that logic to end users, deposits could meaningfully migrate toward fintech apps earning money-market-equivalent returns with instant settlement.

Hallene’s honest read on the yield outcome: likely a legal ban, difficult to enforce, ultimately resolved through loopholes and litigation. The direction of travel favors stablecoin adoption regardless.

Deep Dive · Tokenization

The Proof Point: From Home Equity Lines to SBA Loans

Hallene’s anchor example is Figure — the home equity line of credit company CMT backed early. A 2019 paper projected 25–26 basis points of origination cost savings by moving the loan lifecycle onchain: cryptographic provenance of underwriting documents, transparent servicing records, frictionless secondary transfers. Real-world execution has now delivered approximately 150 basis points of savings — six times the original projection. Figure is now public.

The principle is simple and powerful: onchain provenance makes assets easier to buy. When buyers can verify every underwriting step without legal review teams and escrow delays, the cost of capital falls. Lower cost of capital forces adoption. The tokenization roadmap follows a logical sequence — dollars first, then dollar-denominated assets, then everything else.

“Cost savings force adoption. We’re seeing that with stablecoins, and with early examples like Figure.”

Sam Hallene, Partner — CMT Digital

Portfolio Spotlights

The Companies Building the Onchain Economy

Sam Hallene named several portfolio companies throughout the conversation. Each represents a distinct wedge in CMT Digital’s infrastructure thesis.

Tokenized Credit

Figure

Home equity line of credit origination — onchain. Now public.

CMT Digital’s flagship proof point. Figure originated HELOCs on blockchain rails, demonstrating that cryptographic provenance of loan documents translates directly into lower cost of capital — from a projected 25 bps of savings in 2019 to a demonstrated 150 bps today. The public listing is the first major exit signal from the CMT thesis: real-world credit at scale, built on blockchain infrastructure.

Asset Class

Home equity lines of credit

Key Metric

~150bps origination savings vs. traditional

Status

Public company

CMT Role

Early-stage investor

Small Business Credit

NEWITY

SBA 7(a) lending platform bringing $350B in underserved credit onchain.

In February 2026, CMT led NEWITY’s first-ever external raise — $11M as a SAFE — to accelerate its pivot from AI-driven SBA lending into blockchain-native loan origination. The case starts with a stark fact: small businesses represent 99.9% of US firms and nearly half the nation’s workforce, yet face a $350 billion annual funding shortfall.

NEWITY has already demonstrated scale: $12 billion in loans to over 125,000 businesses since 2020, with AI-first underwriting that compresses traditional 12-week SBA timelines to roughly 21 days. The onchain play is a liquidity unlock — SBA 7(a) loans are government-guaranteed and highly homogeneous, making them ideal tokenization candidates: pools represented as digital instruments, tradable on secondary markets, recycling capital back to new borrowers at scale.

What has to be true for this to work? Regulatory clarity for tokenized SBA instruments must hold; NEWITY’s compliance-heavy origination workflows need to migrate onchain without sacrificing underwriting speed; and institutional or DeFi-native capital needs to show up as secondary market buyers. CMT’s bet is that NEWITY’s 125,000 borrower relationships and $12B in loan history give it an insurmountable head start over crypto-native credit protocols building from scratch.

CMT Round

Led $11M SAFE (Dec 2025)

Track Record

$12B loans · 125,000+ businesses

Market Gap

$350B annual small business funding shortfall

Speed Edge

21-day funding vs. 12-week national average

Institutional Derivatives

STS Digital

The options infrastructure layer institutional crypto has been waiting for.

Offering options on 400+ cryptocurrencies simultaneously is genuinely hard — technically and from a risk-management standpoint. Most platforms haven’t solved it. STS Digital has. Founded by derivatives veterans from Credit Suisse and UBS, the Bermuda-regulated firm delivers a unified platform for spot, vanilla and exotic options, and structured products across 400+ tokens.

In February 2026, CMT led STS Digital’s $30M strategic round alongside Kraken parent Payward, F-Prime (Fidelity), and Arrington Capital. The timing reflects a market reality: crypto options open interest has crossed $40 billion, and institutional demand for hedging tools is compounding as perp-only exposure no longer satisfies sophisticated risk managers. Hallene’s case for options over perps is direct: the October 10 mass liquidation event showed how cascading perp liquidations amplify selloffs catastrophically. Options cap maximum loss and remove auto-deleveraging risk. As institutional flows enter crypto, they bring the risk management toolkit of traditional finance — and that toolkit is built around options.

Hallene’s conviction phrase says it all: STS has built a meaningful liquidity moat in crypto options, and liquidity is the most durable competitive advantage in any financial market.

CMT Round

Led $30M strategic (Feb 2026)

Co-investors

Kraken (Payward), Fidelity (F-Prime), Arrington Capital

Sentiment markets — where polling meets skin in the game.

TBD.vote isn’t trying to out-Polymarket Polymarket. Hallene is deliberate on this distinction. Polymarket excels at deep liquidity in long-duration, oracle-resolved questions. TBD attacks a different surface: any user can create a poll, KYC-verified voters resolve it through consensus, and timeframes are arbitrary — including tomorrow.

The KYC demographic layer is what makes TBD commercially interesting beyond pure prediction. Segmented voter behavior — verified cohorts wagering on specific policy or market outcomes — produces signal that political strategists, media companies, and brands will pay for. The resolution mechanism also removes oracle trust assumptions entirely, which matters as prediction markets become serious institutional information sources. Hallene’s framing: we’re in early innings of prediction markets being treated as mainstream signal, and TBD is positioning for that transition as a sentiment intelligence layer, not a Polymarket clone.

Sentiment intelligence layer, not Polymarket replacement

Prime Brokerage

FalconX

Institutional crypto prime brokerage — the market’s plumbing layer.

A CMT portfolio company since 2019, FalconX built the infrastructure institutional crypto participants had been missing: credit lines, cross-collateralization, portfolio margining, and consolidated execution across venues. In Hallene’s framework, prime brokerage is what enables the derivatives market to mature — you need trusted intermediaries willing to warehouse risk and extend credit before large-scale institutional trading becomes operationally viable. CMT has been a hands-on partner across product roadmap, fundraising, and hiring for over five years.

Category

Digital asset prime brokerage

CMT Since

2019

Role in thesis

Institutional liquidity infrastructure

Significance

Enables scale across derivatives and credit markets

For Founders

Raising Capital in the Sentiment Gap

Hallene’s advice for founders in tokenization and capital markets was candid: it’s a difficult time to raise. Bitcoin soft and altcoins quiet have created a cautious funding environment even as structural progress has never been clearer. His view — CMT is open for business, actively investing, and the binary regulatory variables that were existential risks twelve months ago have now resolved in crypto’s favor.

📐

Quantify your onchain wedge

CMT backs entrepreneurs who can demonstrate measurable improvement — cost savings, speed, liquidity. The Figure model (quantify the basis points) is the benchmark.

⚡

AI usage is now a diligence question

CMT has added “how are you using AI?” to their core underwriting checklist. Teams leveraging AI to punch above their headcount weight are viewed as structurally advantaged.

📈

Don’t mistake sentiment for fundamentals

CMT has seen this movie before. The smart money buys infrastructure during the sentiment trough — not at the top of the cycle.

The Bigger Picture

The Boring Future Is the Bullish Future

There is a version of crypto’s future that looks nothing like its past — no speculative frenzy, no memecoin supercycles, no dramatic collapses from overleveraged offshore intermediaries. Just tokenized treasuries settling in seconds. SBA loans trading in liquid secondary markets. Stablecoin yield flowing to users through apps they already use. Options desks hedging institutional portfolios across 400 digital assets with the rigor of equity derivatives.

That’s the future CMT Digital has been quietly building toward since 2013. Hallene calls it boring. After two cycles of not-boring, boring sounds excellent.

Follow CMT Digital

Research, thesis pieces, and portfolio updates — the best signal in institutional crypto venture.

EBC is introducing Europe’s largest meetings program for the crypto industry

Speakers include execs from Bitpanda, CoinFund, Galaxy, KKR, OKX, Banco Santander, BBVA, Algorand, Bullish and Bitwise Asset Management

Barcelona, Spain — Barcelona is set to welcome Europe’s largest blockchain event on October 16-17, 2025. With over 6,000 delegates and 300 speakers, it will be the largest blockchain event in Europe in 2025 and the largest edition since the event started in 2018.

More than 300 speakers, including top executives from Bitpanda, CoinFund, Galaxy, KKR, OKX, Banco Santander, BBVA, Algorand, Bullish, J.P. Morgan, BNP Paribas, and Bitwise Asset Management, will take the stage to share insights and drive the conversation forward.

This year’s agenda will spotlight the most relevant trends in the space, including tokenization of funds and securities, stablecoins, AI agents, institutional demand and ETFs, modern L1s and L2s, DePIN, restaking, user-first Web3 design, and Bitcoin as a treasury reserve.

One of this year’s standout innovations is the launch of Europe’s largest meetings program for the crypto industry, a first-of-its-kind initiative designed to maximize ROI for every attendee. With over 10,000 pre-scheduled 1:1 meetings expected, this new feature will set a new standard in the industry.

For the third time, EBC will host its flagship Start-up Battle, the largest blockchain start-up competition of its kind in Europe, where the 50 most promising European blockchain start-ups will pitch their ideas to a live audience.

At the top of the side event list, there will be a Hackathon where 200+ hackers, 30+ mentors and 20 teams are expected to participate in a 48-hour hackathon.

This year, EBC offers more than just an event, but rather a full experience. From a sunset beach party and a morning beach run to a curated wine tasting and a one-star Michelin tour, attendees will enjoy the best of Barcelona’s vibrant lifestyle.

The event also coincides with the Sitges Film Festival, the Salón Náutico boat show, which showcases boats, yachts, and maritime experiences, and the CSIO Barcelona, renowned as the world’s most prestigious equestrian competition.

Victoria Gago, co-founder of European Blockchain Convention, said: “We have seen an extraordinary increase in registrations and interest from exhibitors after the overwhelmingly positive feedback from our previous edition.”

“We are extremely excited to bring together the worlds of TradFi and digital assets”, shared co-founder Daniel Salmeron. “The participation of so many traditional banks and financial institutions demonstrates their optimism about the future of crypto and digital assets.”

Launched in 2018, European Blockchain Convention is the most influential blockchain event in Europe, connecting industry professionals, startups, and technology leaders. The event provides a platform for sharing insights, fostering collaborations, and exploring the vast potential of blockchain, crypto, and digital assets.