Is it not enough to simply watch the beautiful game, unadorned?

These days you might use an AI chatbot to keep abreast of what’s happening in the World Cup. And that AI chatbot, in a sign of the times, might try to shove prediction market odds in your face as another way of ostensibly keeping you up to speed. Because are you really getting the full picture if you don’t know where a bunch of gamblers fall on the outcome?

This is exactly what OpenAI is doing. The Sam Altman-led company quietly struck a deal with Kalshi, which lets you bet on outcomes far beyond sports, to show its prediction market data in ChatGPT, the New York Times reported.

It’s perhaps the inevitable melding of two of the most divisive innovations to come out of the tech industry in recent years.

Searching France and Spain on ChatGPT ahead of their quarterfinal clash on Tuesday returned a graphic that showed that Les Bleus had a 60 percent chance of winning, according to the reporting. (We hope no one acted on that information.) Asking about the England and Argentina game on Wednesday showed that the Three Lions had a 54 percent chance of coming out on top.

Neither side promoted the deal, and the graphic is tellingly light on branding. There are no logos and no outbound links. The only sign of the collab is a small notice in the bottom left corner stating, “Source: Kalshi.”

This is the first partnership of its kind for OpenAI. The company recently updated its help page to stress that users “cannot place bets through ChatGPT,” with the Kalshi data being limited to “queries related to the 2026 World Cup,” according to the NYT.

Zooming out, it’s another sign of prediction markets laundering their image by glomming themselves onto other, more credible brands. In January, Kalshi partnered with CNN to provide its real-time prediction data on the news network’s broadcasts. Its rival Polymarket entered into a similar partnership with Dow Jones, the publisher of The Wall Street Journal, that same month. Both have also partnered with Google to show their data in search results.

Their fuzzy legal framework, plus their Wild West approach to gambling, has led to numerous controversies. Suspiciously timed bets on massive events like the US’s capture of ousted Venezuelan president Nicolás Maduro have raised concerns of rampant insider trading and put pressure on lawmakers to crackdown on the platforms. Arrests have been madein some cases, but these have been rare.

Put simply, for OpenAI, it may be somewhat risky to associate itself with all this baggage, which might be why the Kalshi collaboration is very limited — at least for now.

Bitcoin approached $65,000 on July 14 as a sharper-than-expected slowdown in US inflation weakened the case for another near-term Federal Reserve interest rate increase.

Data from CryptoSlate showed that BTC rose as high as $64,832 once the report landed, gaining about 4% from its intraday low and coming within $200 of a threshold it has struggled to hold over the past month.

This price performance followed the consumer price index falling 0.4% in June, its largest monthly decline since April 2020, the Labor Department said. Prices were 3.5% higher than a year earlier, down from 4.2% in May and below economists’ forecast for a 3.8% increase.

Core CPI, which excludes food and energy, was unchanged for the month and increased 2.6% from a year earlier. That was also below expectations and marked a slowdown from the 2.9% annual rate recorded in May.

Jake Kennis, senior research analyst at Nansen, told CryptoSlate that the reading represented a clear improvement but stopped short of establishing that inflation was on a sustained downward path.

Kennis said:

“The softness was led largely by energy, which eases near-term pressure on the Fed heading into the July FOMC and helped risk assets bid. That said, this is a cooler print rather than confirmation of durable disinflation.”

The energy decline behind CPI has already reversed

The inflation catalyst could lose force quickly because Bitcoin is responding to an inflation report that accurately describes June, a month whose conditions offer only a rough guide to the price conditions building in July.

This is because the improvement that pushed Bitcoin higher came from an oil market that had changed substantially before the inflation report reached investors.

BLS data show that energy prices fell 5.7% in June, while gasoline prices declined 9.7%, making the largest contribution to the monthly drop in the headline CPI. Those decreases followed a retreat in crude prices as a temporary agreement between Washington and Tehran raised hopes that traffic through the Strait of Hormuz would recover.

That reprieve now has unraveled as the US has reinstated a naval blockade on Iran after Tehran said it had closed the strait, following a third consecutive night of attacks on Iranian targets by US forces, which Iran met by launching missiles at US allies and striking commercial vessels moving through the waterway.

Brent crude rose above $87 per barrel on July 14, then pared its gains, trading near $85. West Texas Intermediate (WTI) found an intraday high at $80.53 after both benchmarks reached their highest levels in about a month.

Patrick De Haan, head of petroleum analysis at GasBuddy, described the June CPI as a “rearview mirror,” saying the decline reflected prices from several weeks earlier, and the latest escalation pushed crude and retail fuel costs higher.

The timing raises the possibility that headline inflation could rebound as July gasoline, diesel, and transportation expenses are incorporated into the data. Higher crude prices could also spread through freight, aviation, agriculture, and manufacturing supply chains.

A renewed energy shock would complicate Bitcoin’s attempt to move through $65,000, as it could revive expectations that the Fed will keep interest rates elevated or raise them again before the end of the year.

He said the central bank had no tolerance for persistently elevated inflation and stayed committed to restoring price stability.

According to Warsh:

“The Fed’s number one objective is to get monetary policy right—or as near to it as we possibly can. That is our clear and constant aim, the star we steer by. And if we get policy right—and we will—the inflation surge of the last five years will be a thing of the past.”

The Fed held its benchmark rate at 3.5%-3.75% in June after several officials raised concerns that energy costs could keep inflation elevated. The July 14 report weakened the case for a July increase, leaving the outlook for September and later meetings still unresolved.

Warsh described the CPI report as one data point and rejected the suggestion that it represented “mission accomplished.”

The restraint also limited how far traders could extend the post-CPI rally on expectations of easier monetary policy, and Bitcoin stayed below the resistance area that has capped several recovery attempts since June.

Bitcoin must now convert its post-CPI advance into a sustained move through the $65,000-$66,000 resistance area, building on the momentum it is forming.

BTC held near $62,000 through repeated US attacks on Iran and avoided the broad liquidation cascade that followed earlier geopolitical shocks.

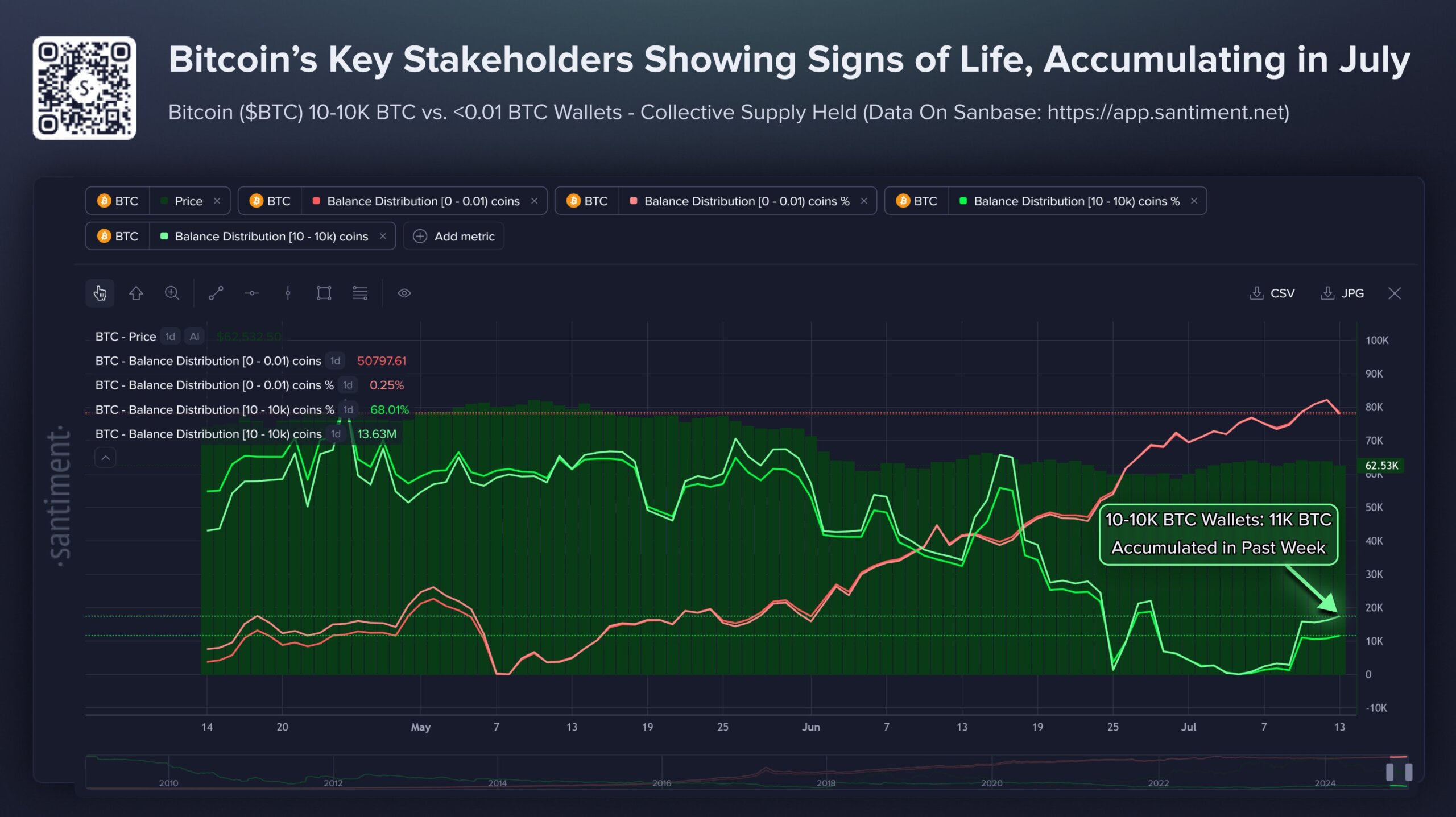

Data from Santiment also showed that key Bitcoin stakeholders were exhibiting bullish behavior and accumulating the top crypto.

According to the firm:

“Wallets holding 10–10,000 BTC have added roughly 11,000 BTC over the past week, a meaningful shift because this tier of whales and sharks has historically tracked closely with price direction. Small retail wallets are still mainly accumulating too, which shows dip-buying interest remains alive even after weeks of volatility.”

A Santiment chart shows Bitcoin wallets holding 10 to 10,000 BTC accumulated roughly 11,000 BTC over the past week, tracking price direction.

That accumulation helped Bitcoin respond quickly when CPI weakened the dollar and Treasury yields, and it could also provide support if higher oil prices begin challenging the inflation outlook again.

Lacie Zhang, a research analyst at Bitget Wallet, told CryptoSlate that the CPI report provided the liquidity-driven catalyst Bitcoin needed to break higher, noting that renewed disruption around the Strait of Hormuz made the advance more vulnerable to reversal.

She placed near-term support at $62,000 to $63,000 and resistance at $65,000 to $66,000, and a sustained break above that zone would take Bitcoin beyond the range that has contained it through much of June and July.

Such a move may require an easing of oil tensions, further ETF inflows, or a softer policy signal from the Fed, which could give buyers the confidence needed to absorb profit-taking near $65,000.

Renewed attacks around the Strait of Hormuz would keep the oil-risk premium elevated. Higher fuel costs could lift inflation expectations, restore bets on another rate increase, and weigh on Bitcoin before it establishes support above the resistance zone.

Lucid Group (LCID) shares crashed nearly 50% on Tuesday after a report raised bankruptcy fears. The stock fell so fast that exchanges paused trading three times.

The report claimed the electric vehicle (EV) maker may go private or file for bankruptcy. Lucid quickly denied it, yet the panic erased about half of its market value in one day.

Lucid Group (LCID) Stock Performance. Source: TradingView

Why the Lucid Stock Crash Ran So Deep

The panic started with a report from industry outlet EV. It said turnaround firm AlixPartners will soon present options to Lucid’s board. Two of those options reportedly stand out.

The first is going private, meaning Lucid would leave the stock market.

The second is Chapter 11 bankruptcy, a legal process that lets a company keep operating while it reworks its debts.

The adviser also reportedly wants Lucid to pause its push into Europe and pour its energy into the Gravity SUV. That vehicle has struggled with quality problems since production began in late 2024.

BREAKING: Lucid $LCID crashes 49% after report says the company is considering bankruptcy.

The Saudi-backed EV maker brought in restructuring adviser AlixPartners, which has been asked to report to the board before its next meeting.

The market reaction was brutal. Shares sank as much as 55% and hit a record low of $2.37. At that price, Lucid’s 330 million shares were worth under $800 million.

Lucid Group (LCID) Stock Performance. Source: Google Finance

In November 2021, the company was valued near $90 billion, briefly more than Ford. Nerves were already raw after the SpaceX stock crash.

Lucid Pushes Back as August 4 Earnings Loom

Lucid called the rumors completely false. It said AlixPartners is helping the company run more efficiently, not preparing a court filing.

“AlixPartners has not recommended bankruptcy to management or the Board,” the company shared the statement on Tuesday.

It added it has enough cash to last well into next year.

$LCID The rumors are completely false. The company has sufficient liquidity to carry its operations well into next year, as recently published in its last quarterly filings, and it has not formed any special Board committee to explore the scenarios reported today. Our focus is…

Twork serves as Chief Communications Officer at Lucid Motors. The clarification likely explains the ongoing LCID stock recovery.

However, the fear has roots in Lucid’s own numbers. The company lost $2.7 billion in 2025, per its filings. It lost another $1.03 billion in the first quarter of 2026, nearly triple the year before. That quarter, building cars cost $594 million against $282 million in sales.

That gap explains the constant need for fresh money. Lucid raised about $1.05 billion in April, including $200 million from robotaxi partner Uber. In July, it reportedly borrowed $800 million more from an affiliate of Saudi Arabia’s Public Investment Fund, its majority owner.

Silvio Napoli, the former Schindler boss who became CEO on June 1, has been cutting costs and jobs since.

Today we announced that Silvio Napoli has assumed the role of Lucid CEO, effective immediately.

Napoli was previously announced as incoming CEO in April and brings decades of global industrial leadership experience spanning large-scale operations, financial management, and… pic.twitter.com/6VkID0e3Cb

Donald Trump delivered three major policy shocks between July 6 and July 11. He declared the Iran ceasefire over, sending Brent crude oil up 5.2%. The POTUS also ordered a halt to trade with Spain, pushing Spain’s stock market index IBEX 35 down 2.6%.

Trump said the interim agreement with Iran was “over” after renewed attacks on commercial ships and US facilities in the Gulf. American forces then launched fresh strikes against Iranian targets.

Oil markets reacted immediately. Brent settled 5.2% higher, while WTI gained 4.4% and reached a two-week high. The S&P 500 and Dow closed lower, while the STOXX 600 recorded its steepest decline since March.

The surge in oil also pushed Treasury yields higher as investors priced in greater inflation risk. Higher fuel costs could make it harder for the Federal Reserve to lower interest rates.

However, Trump later said the US would continue talks with Iran and played down the prospect of another full-scale war.

Oil just went through one of its most volatile months in years.

The reason is the US-Iran war, which restarted in February after everyone assumed it had ended with last year’s ceasefire.

Since then, oil has swung from $58 to $119 and back down to $71, driven almost entirely by… pic.twitter.com/qtk4mxom6U

Markets will now focus on shipping through the Strait of Hormuz, which carries around one-fifth of global oil supply.

Spain Trade Threat Hits Stocks and Bonds

Trump also ordered Treasury Secretary Scott Bessent to halt trade and visits with Spain. He accused Madrid of failing to spend enough on defence and obstructing the US campaign against Iran.

Spanish markets fell sharply after the comments. The IBEX 35 lost 2.6%, making it Europe’s worst-performing major index that day.

IBEX 35 is Spain’s Benchmark Stock Market Index in Madrid. Source: Yahoo Finance

Santander shares dropped 4.3%, BBVA fell 3% and Zara owner Inditex declined 3.6%. Spain’s 10-year government bond yield rose nine basis points as investors demanded a higher return for holding its debt.

It remains unclear whether Trump can impose a complete bilateral embargo. The European Union handles trade policy for its members, and US-Spain commerce has continued despite earlier threats.

Still, prolonged uncertainty could weigh on Spanish banks, exporters, airlines and tourism companies.

BREAKING: President Trump says the US is “cutting off all trade with Spain.”

— The Kobeissi Letter (@KobeissiLetter) July 8, 2026

Trump Hardens His Position on Russia

Trump made a significant shift on Ukraine during the NATO summit in Ankara. He said the US would license Ukraine to manufacture Patriot air-defence systems, technology Kyiv has requested for years.

Days later, US senators announced an agreement with the Trump administration to advance tougher sanctions against Russia. The legislation could target countries that continue buying Russian oil and gas.

Markets have yet to show a clear reaction because Congress has not approved the final bill. Its impact will depend on the sanctions, exemptions and enforcement measures included in the final text.

President Trump said Wednesday the U.S. will give Ukraine a production license to build its own Patriot missile interceptors for defense, granting a major request from Ukrainian President Volodymyr Zelenskyy amid the ongoing war with Russia. pic.twitter.com/BkG2GIOCRq

Strong secondary sanctions could disrupt Russian oil flows to China, India and Turkey. That would place further pressure on energy prices while increasing demand for alternative supplies.

Meanwhile, the Patriot decision could support defence manufacturers and suppliers. It also signals that Washington may apply greater military and economic pressure on Moscow.

Donald Trump’s latest financial disclosure showed how closely digital-asset policy, personal financial interests, branded tokens, and presidential power now sit together.

His highly scrutinized recent filing points to a governance problem that extends well beyond any one politician, because crypto can convert access, symbolism, and regulatory attitudes into value faster than older business interests ever could.

Presidential financial disclosures usually draw attention because of the total. However, the more important issues concern how the income was generated, which entities carried it, what products sat behind it, and how sensitive those products are to decisions made by the same federal government linked to the disclosure.

That’s what makes Trump’s crypto exposure more serious than other ethics disputes involving his hotels, licensing deals, or marketable securities. Crypto compresses several functions into one domain: it’s an investable asset class, a fundraising mechanism, a branded consumer product, a policy target, and a global market-structure debate all at once.

When a president is economically tied to ventures inside that domain, the overlap between public action and private benefit becomes much bigger.

While the line items matter, they are only part of the narrative. The filing shows a political economy in which the president appears linked to ventures whose value, distribution, and commercial prospects move with the government’s stance on crypto.

Politics can become a price signal for crypto

Traditional businesses usually take longer to respond to public policy, but crypto responds faster and across multiple channels at once. A favorable enforcement signal can improve sentiment across a network, and looser banking regulation can widen the commercial room available to issuers and intermediaries.

A White House summit, executive order, or reserve announcement can change how institutions interpret the asset class and how counterparties value the ventures attached to it.

Crypto businesses often react even faster to political shifts. Tokens can be launched quickly, traded globally, marketed continuously, and tied to communities that react almost immediately to political cues.

A branded token, a stablecoin, or a governance-linked venture can simultaneously accumulate value through distribution, licensing, treasury reserves, trading activity, and network effects.

In that environment, the line between policy climate and private upside grows much thinner than it looks in older sectors.

All of this makes Trump’s crypto disclosure more of an institutional problem than a scandal.

Stablecoin law, the SEC’s and CFTC’s positions, banking access, federal policy toward digital assets under Executive Order 14178, and the White House’s attitude all shape the commercial environment around crypto.

When the president and his family hold visible interests in that environment, the market has good reason to view policy through a personal financial lens. That view can then take hold even when a policy position has a defensible public-interest rationale of its own.

That’s also why disclosure alone feels less reassuring here than it often does in older ethics disputes. Disclosures give the public a map of exposure, which is useful, but they don’t resolve the deeper problem when the underlying assets can reprice rapidly in response to political proximity.

Older presidential conflicts offer only a loose comparison. Hotels, licensing deals, and passive investments can raise serious ethics concerns, but they rarely react to political events with the speed or reach of a crypto venture.

Crypto trades around the clock across global venues, and that speed makes it super sensitive to politics. Public office becomes a more immediate input into private financial ecosystems.

Trump’s crypto disclosure shows the industry loses something when the boundaries blur

The crypto industry wants pension funds, advisers, banks, payment companies, and lawmakers to treat digital assets as durable financial infrastructure.

That effort gets harder when the most visible political figure tied to the sector also appears to be a major financial beneficiary of crypto-linked ventures. Once that association hardens, every favorable policy move risks being read as self-dealing, even when the underlying policy argument stands on respectable ground.

That comes at a high cost for crypto. Stablecoin legislation can be viewed through the interests of connected issuers and ventures, while a Strategic Bitcoin Reserve announcement can lift confidence in Bitcoin and the wider sector.

Even broadly applicable policies can therefore attract suspicion when politically connected businesses stand to benefit.

Any kind of enforcement pullback can easily look like a general policy reset while still inviting suspicion that proximity and access played some part. The industry may gain regulatory breathing room in that environment and still lose the institutional trust it needs for broader adoption.

The filing is best understood as a warning about governance in the digital-asset era. Crypto has created markets in which influence, affiliation, and value interact with unusual speed and efficiency.

That helps explain the sector’s energy and growth, but it also makes conflict risk more immediate because political proximity can become part of the asset itself, and markets can price that proximity long before legal rules are refined enough to contain it.

Any serious response has to go beyond disclosure formalities. Conflict rules for digital assets would need to address counterparty transparency, recusal expectations around sector-specific policy, direct and indirect token-linked monetization while in office, and the treatment of governance rights or revenue claims held through affiliated entities.

The older blind-trust framework reaches only part of that issue because many crypto ventures derive value from branding, access, and regulatory climate in ways that remain economically potent even when day-to-day management is delegated.

You can see the significance of that shift without taking a partisan political view. A sector that wants to be treated as financial infrastructure needs clearer separation between public power and private token economics.

Trump’s disclosure shows how difficult that separation becomes once a president’s economic interests sit inside a fast-moving, policy-sensitive digital market.

Bitcoin’s more than $10 billion corporate credit market is still attracting new entrants after a June selloff triggered margin calls and drove its leading preferred shares far below par.

A new report from BitcoinTreasuries.net described the downturn as the sector’s first meaningful stress test, offering an early measure of whether companies can reliably build financing structures around their cryptocurrency reserves.

The selloff showed how quickly supposedly stable products can buckle when too much leverage piles in. Yet the market emerged bruised but operational. Dividend payments continued, secondary-market volumes reached record levels, and corporate treasuries kept adding Bitcoin to their balance sheets.

That resilience has drawn praise from industry proponents and sustained interest from prospective issuers, which are advancing plans for new yield-paying products across the US, Europe and Asia.

Investors are now betting that corporate Bitcoin holdings can support a wider market for preferred shares and similar debt-like products.

How leverage turned a stable trade into a cascade

Leverage piled into preferred shares that looked stable, then unwound in a rush of liquidations.

Strategy, the largest Bitcoin holding company with over 800,000 BTC, and Strive have used preferred shares to raise capital without relying entirely on common-stock sales or conventional debt. The securities typically carry a $100 stated value, pay fixed or variable dividends, and have no maturity date.

For issuers, the structure provides long-term capital that can be directed toward Bitcoin purchases or other corporate needs. Investors receive income above the yield available from many traditional fixed-income products without having to hold Bitcoin directly.

Strategy’s STRC and Strive’s SATA emerged as two of the largest instruments in the market. Strategy can adjust STRC’s dividend to keep the shares trading near $100, while SATA offers a variable payout and distributes dividends daily.

For months, both securities traded within relatively narrow ranges around par. That stability encouraged some investors to borrow money to increase their positions and amplify dividend income, BitcoinTreasuries.net said in its June corporate adoption report.

The strategy worked as long as the shares remained stable and the dividends exceeded the cost of financing the trade.

That calculation began to break down as Bitcoin fell below $60,000 in June and selling pressure spread across companies and securities tied to the cryptocurrency.

Beginning June 18, STRC and SATA moved sharply below par. Falling prices triggered margin calls for leveraged STRC holders, forcing them to sell into an already weakening market and driving further liquidations.

SATA also declined under pressure from its own market conditions and spillover from STRC’s selloff.

STRC eventually fell to about $75, roughly 25% below its stated value, while SATA declined to around $88. Bitcoin’s slide weighed on investor sentiment, even though preferred shares continued to pay their scheduled dividends.

Leverage turned products built for steady income into another source of volatility. Higher dividends might draw buyers after a selloff, but they offered little protection once indebted investors had to exit.

Raising the dividend also made the financing more expensive for the issuer. Strategy responded by increasing STRC’s annual payout to 12% and introducing a broader capital framework that included a $2.55 billion cash reserve, authority to repurchase preferred shares, and permission to sell some Bitcoin under specified conditions.

The company said the reserve was sufficient to cover about 17 months of expected preferred dividends and interest payments. It also acknowledged that STRC could remain substantially below its target range, leaving the market to determine whether the higher payout would be enough to restore demand.

Prices rebound as Bitcoin buying continues

Despite the June sell-off, the market stabilized faster than initial liquidations suggested, with prices rebounding, trading volumes hitting record highs, and corporate treasuries continuing to buy Bitcoin.

As of publication, STRC had recovered to about $87 from a low near $75, while SATA had climbed back to roughly $97.

The uneven rebound suggested investors were distinguishing between the two securities rather than abandoning the broader market.

Trading activity also accelerated during the turmoil. Combined June volume for STRC and SATA exceeded $10 billion, even as both products traded below their $100 stated values.

STRC accounted for $8.7 billion of that total, its highest monthly volume on record, and posted two of its five busiest trading weeks. SATA generated nearly $1.5 billion, almost twice its May volume, with three of its four strongest weeks occurring during the month.

Trading held up through the sharp repricing. Buyers absorbed shares from leveraged sellers, keeping the market open and dividend payments uninterrupted.

However, the heavy secondary-market activity did not translate into fresh capital for the issuers. Neither STRC nor SATA was able to raise funds through at-the-market sales in June, as most transactions involved existing shares changing hands between investors.

Strategy added a net of 3,625 Bitcoin during the month, while Strive acquired 3,364 Bitcoin. Each spent about $200 million, leaving the two companies responsible for most of June’s corporate Bitcoin purchases.

Supporters saw the continued buying as evidence that June’s turmoil stemmed from excessive leverage in the securities, rather than fading confidence in corporate Bitcoin accumulation.

New entrants push the model beyond the US

The recovery in trading and continued corporate Bitcoin buying are now encouraging treasury companies to explore whether the credit model can expand beyond the US.

On July 10, Metaplanet provided the latest sign by announcing a joint study on tokenized credit instruments in Japan.

The Tokyo-listed company will work with Siiibo Securities, the yen stablecoin issuer JPYC, and the regulated security-token platform Progmat to examine products that use Bitcoin as a backing asset or as a source of credit support. Metaplanet recently acquired Siiibo for $13 million.

According to the firm:

“Digital credit backed by Bitcoin could evolve into instruments traded and settled globally on a 24/7/365 basis, with interest and distributions accruing on a daily prorated basis according to the holding period.”

The initiative targets longstanding barriers in Japan’s corporate credit market, where smaller and growing companies can face high costs for product design, distribution, investor administration, interest payments and redemptions.

Metaplanet and its partners said digital infrastructure could reduce some of those costs. Their proposal combines stablecoins for payments and distributions, security tokens for recording ownership and transfer rights, and Bitcoin as an asset supporting the securities.

The structure could calculate interest based on how long an investor holds a product, reducing reliance on conventional record dates. It could also allow trading and settlement outside regular market hours.

The project remains at an early stage, with no issuance date, return, distribution plan, or final structure in place. The companies have yet to decide whether to run a proof of concept.

Metaplanet has also not specified whether investors would have a direct legal claim to the designated Bitcoin. That detail will determine whether the products function as formally secured instruments or rely more broadly on the issuer’s balance sheet and cryptocurrency reserves.

Metaplanet holds 43,000 Bitcoin, ranking third among publicly traded companies by BTC holdings.

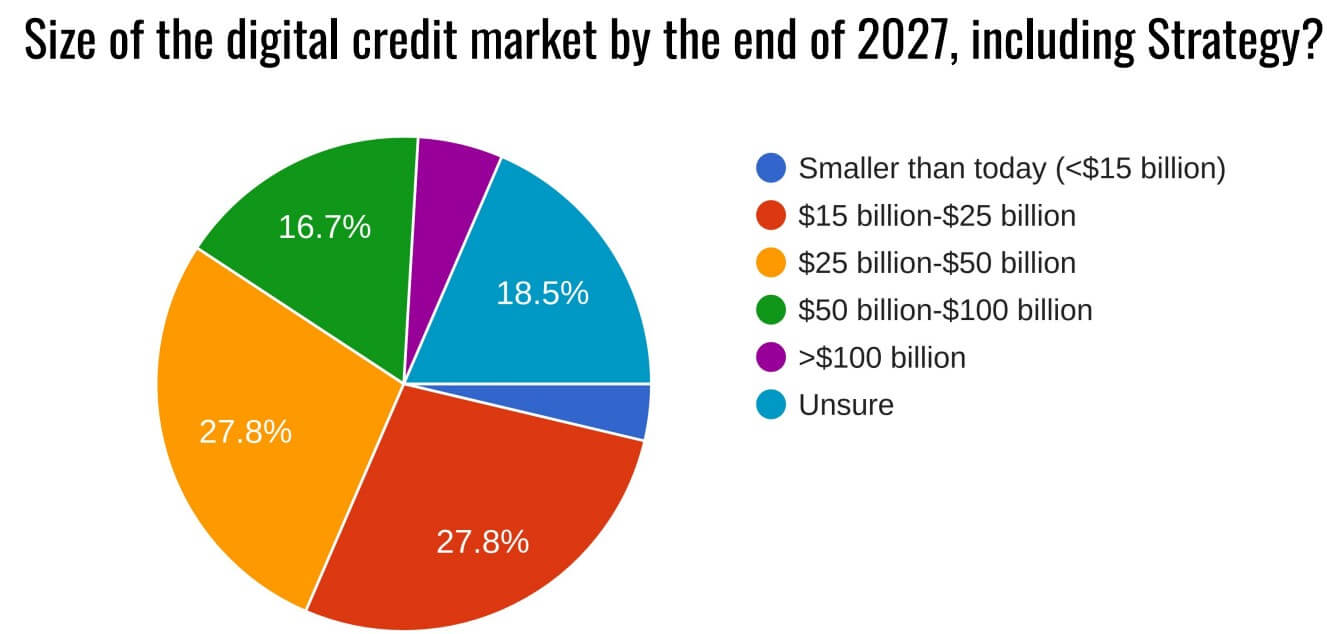

Bitcoin digital credit growth forecasts meet a more demanding market

Metaplanet’s planned entry adds weight to expectations that Bitcoin-backed credit will expand, though June’s selloff has given investors a clearer view of the risks behind those forecasts.

A BitcoinTreasuries.net survey found that 78% of respondents expect the digital credit market to grow through the end of 2027. Another 22% projected that outstanding supply could exceed $50 billion, with some expecting it to surpass $100 billion.

Bitcoin Digital Credit Market (Source: BitcoinTreasuries.Net)

The results, however, reflect a group already predisposed to support the products. The report found that 87% of respondents viewed digital credit favorably and 72% had invested in the sector. About 76% also expected similarly sharp price declines to occur again.

That mix of confidence and caution offers a more measured assessment of June. Investors remain optimistic about the market’s long-term potential, even as they acknowledge that leverage and liquidity can drive large departures from par.

Michael Saylor has argued that Bitcoin makes digital credit easier to assess because its primary market risk is tied to a globally traded and continuously observable asset. Investors can track Bitcoin’s price and volatility in real time and incorporate those movements into their valuation models.

June proved Bitcoin-backed credit could survive a liquidation shock. Its next hurdle is persuading investors to fund new issuance after watching leading products trade below par.

World, a Chainlink-powered prediction market launched in the Phantom wallet on Solana on July 1, said recently that it is moving to Robinhood Chain.

The move shifts the project from Solana’s crypto-focused users to Robinhood’s roughly 28 million customers, prompting some users to accuse it of using Solana to gain attention before leaving.

After more than two years of teasers, the concept debuted in Phantom, a well-known Solana wallet. It allowed players to wager on the price of Bitcoin and the 2026 FIFA World Cup, with rewards issued in Phantom’s CASH stablecoin and results validated by Chainlink.

The announcement gave no reason for the shutdown, mentioned no technical issues, and did not explain what would happen to open bets.

The move was unexpected, as World had recently said it planned to expand into markets for economic data, elections, and major sports leagues in the coming weeks.

Why Robinhood makes more sense

Robinhood appears to be the more likely reason for the move.

The brokerage has already launched tokenized U.S. stocks and ETFs for European users and plans to move them from Arbitrum to Robinhood Chain.

Robinhood reported 27.4 million funded customer accounts in the first quarter of 2026, giving World access to a much larger base of retail investors.

Chainlink is also part of Robinhood Chain’s infrastructure, allowing World to keep its existing settlement system.

Robinhood CEO Vlad Tenev has also shown users how to move funds from Solana to Robinhood Chain by bridging USDC and swapping it for the network’s Paxos-backed USDG stablecoin.

Polymarket has applied to offer margin trading in the U.S., which would allow users to fund only part of a wager.

National Futures Association records show that PM Derivatives LLC filed applications on July 3 for futures commission merchant status, NFA membership, and swap firm registration on behalf of Polymarket-linked entity Coming Home GBA LLC.

The company would still need approval from the Commodity Futures Trading Commission before launching margin trading.

That would move Polymarket beyond simple yes-or-no markets and closer to a leveraged trading platform. Adding borrowed funds would increase both potential gains and losses for everyday users.

The move also intensifies competition with Kalshi, which is further ahead in the U.S.

Both platforms reported record trading volumes in June, with Kalshi reaching $33 billion and Polymarket, including its U.S. platform, nearing $14 billion. Both also launched crypto perpetual futures earlier this year.

Polymarket’s U.S. expansion has faced challenges. The company is under investigation by the Commodity Futures Trading Commission and is also facing a lawsuit over its marketing, though its margin trading application signals it plans to keep expanding.

The company is collaborating with regulators to create never-expiring futures linked to gold, foreign exchange, and energy, Chief Risk Officer Udesh Jha told Reuters.

In addition to institutional investors, retail traders account for a sizable portion of Kalshi’s user base, hence he claimed that gold is a top focus.

Kalshi would be in direct rivalry with the world’s biggest derivatives exchange, CME Group, as a result of that development.

Due to the CFTC’s decision to let Kalshi and Coinbase to offer perpetual futures, CME has already filed a lawsuit against the organization and its chairman, Michael Selig.

The decision is a “disaster waiting to happen,” according to Terry Duffy, the departing CEO of CME, who cautioned that retail traders might not fully understand the risks.

If Kalshi’s growth is permitted, it will directly compete with major exchanges such as CME, Nasdaq, Cboe, and Intercontinental Exchange, which owns the New York Stock Exchange. According to reports, the corporation plans to go public between late 2027 and early 2028.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

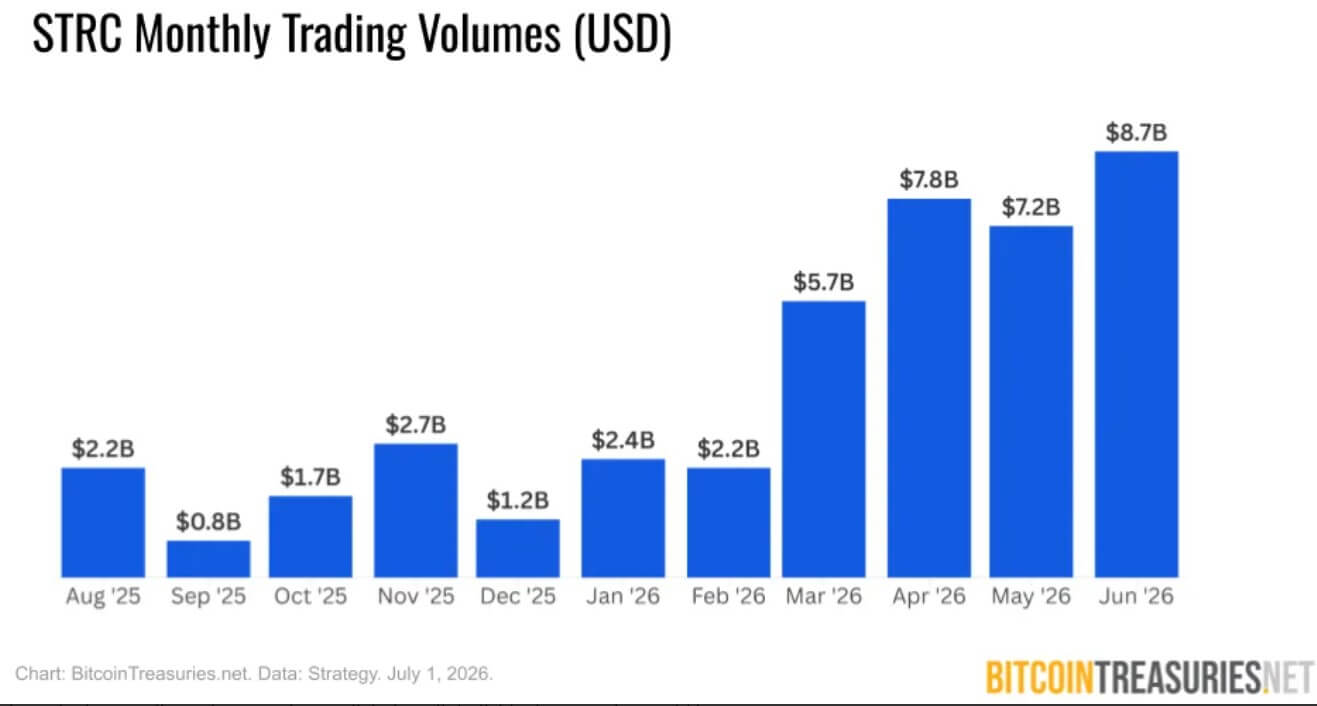

Bitcoin-backed preferred shares STRC and SATA posted their highest combined monthly trading volume on record in June, surpassing $10 billion amid a BTC sell-off that pushed both below their $100 par value.

According to data from BitcoinTreasuries.net (BTN), Strategy’s STRC generated $8.7 billion in trading volume last month, while Strive’s SATA recorded $1.5 billion, and this happened with the price of BTC falling near the $57,000 level.

June Trading Sets New Preferred Stock Record

BitcoinTreasuries’ latest corporate adoption report shows that the $8.7 billion recorded by STRC represented a 20.8% jump from the $7.2 billion in May and 11.5% above April’s $7.8 billion. The amount was also more than 52% higher than what the shares generated in March after a much quieter start to the year.

Strategy’s perpetual preferred stock volumes had reached $2.2 billion in February before climbing 159.1% in March. January recorded $2.4 billion, following $1.2 billion in December 2025.

The BTC treasuries market aggregator pointed to June as the first major stress test for the digital credit products after STRC and SATA both dropped well below their $100 par value beginning June 18. According to the firm, margin calls forced STRC and SATA leveraged traders to liquidate positions after an extended period of trading near par.

After weathering Bitcoin’s fall to a price level below $60,000, STRC recovered to about $87 by July 2 after falling as low as $75, while SATA traded near $97. A survey by BTN found that investors were quite headstrong despite the volatility, with more than half of respondents saying that the price decline was not a significant concern. 84% did not sell either of the stocks during the decline, and 52% bought one or both of them after June 18.

“The instinct after June 18 is to ask whether STRC and SATA are safe,” the survey read. “That is the wrong question. Strategy holds 847,363 BTC acquired at an average cost of approximately $75,651. The dividend obligation is a cash flow question, not a solvency question.”

It also pointed out that none of the issuers had missed a payment, and none of them had seen their credit quality change from mid-June.

Strategy, Strive, Metaplanet Lead in Issuer Confidence

In the investor confidence part of the BTN study, respondents projected the strongest issuance potential for Strategy, with the most common expectation placing new digital credit issuance between $10 billion and $30 billion for the Michael Saylor-led firm by the end of 2027.

Strive came in second place on a forecast between $2 billion and $5 billion in additional issuance, followed by Metaplanet, Smarter Web Company, and Bitmine, respectively.

When asked which digital credit issuers appeared most promising, 78.4% of those who took the poll ranked Strategy first, 74.5% tapped Strive second, and Metaplanet took third spot with 49%.

World, a week-old Solana (SOL) prediction market, staged a fake exit. On July 8, it said it was leaving Solana for Robinhood Chain, then admitted the whole thing was a crypto prank the following day.

The gag drew millions of views and briefly fooled parts of the crypto industry. It also divided opinion on whether staged deception is smart marketing or a costly gamble for a young platform.

How the Crypto Prank Spread

World went live on Solana on July 1 inside the Phantom wallet, with Chainlink (LINK) handling data and settlement. Solana’s official account had promoted the debut just a week earlier.

Days later, the project told followers it was leaving for Robinhood Chain. It thanked the Solana Foundation and posted a polished logo for the supposed move.

The target made the fake believable. Robinhood Chain is a real Arbitrum-based Layer 2 that launched on July 1 for tokenized stocks.

That same week, the network set a record daily volume of $563.9 million, according to DefiLlama. Meme coins, not tokenized stocks, drove the frenzy. It was arguably crypto’s hottest new chain.

Several outlets reported the migration as fact. Within a day, World revealed the joke.

The reception split. Solana co-founder Anatoly Yakovenko amplified the gag, and CoinGecko co-founder Bobby Ong called it sharp marketing.

“I’m still trying to figure out if they moved to Robinhood Chain or staying at Solana. I think this is a parody and they are actually staying on Solana. I guess it triggered many folks and got them the attention that they really want, which is all that matters in consumer tech,” Ong remarked.

Critics, however, saw a bait-and-switch that erodes trust in a product handling real bets.

The on-chain record complicates any victory claim. An independent dashboard built by analyst ario_57 tracks World’s activity. It shows roughly $4.37 million in notional volume. Daily users peaked near 3,000 since the July 1 launch.

World’s daily on-chain volume, showing the pre-prank peak. Source: Dune/ario_57

Yet that volume crested around July 6, two days before the stunt. The cumulative totals cover the full launch week, not one viral afternoon. The prank coincided with World’s momentum. It did not create it.

The 2.3 million views were World’s own tally, a measure of attention rather than adoption. Meanwhile, prediction markets face fresh scrutiny, raising the cost of any misstep in trust.

For now, World has crypto’s attention and a working product behind the gag. Whether that attention becomes lasting users is the question the coming weeks will answer.

A New York federal court has returned prediction-market access to state hands just weeks before the CFTC closes comments on national event-contract rules.

In a July 7 opinion and order, Judge Analisa Torres of the Southern District of New York denied KalshiEX LLC’s request for a preliminary injunction to block New York gaming officials from enforcing state gambling law against its sports-event contracts while the case proceeds.

The decision is preliminary. It leaves the merits open, but it rejects Kalshi’s bid for immediate relief on the argument that the Commodity Exchange Act preempts New York’s gambling laws as applied to those contracts.

The access risk now has two tracks: whether the Commodity Futures Trading Commission accepts event contracts at the federal level, and whether states can force platforms to block, limit, or redesign access before the federal framework is finished.

The order landed while the CFTC’s proposed prediction-market rules remain open for comment. The agency’s June 12 Federal Register notice gives interested parties until July 27 to comment on proposed public-interest determinations for event contracts, including contracts involving gaming or activity unlawful under federal or state law.

A related CFTC release said the framework would apply to growth in event contracts, including those referencing sporting events.

Torres’s order sharpened the access issue before that process closes. The court rejected Kalshi’s argument that CFTC-designated contract market rules requiring impartial access effectively require nationwide access to sports contracts.

It also treated the cost of geolocating users on a state-by-state basis as an ordinary regulatory compliance burden, undercutting Kalshi’s irreparable harm argument.

That part of the ruling carries the most operational weight for venues. Geofencing may be expensive, disruptive, and inconsistent with a national market, but the order leaves room for states to keep pressing their gambling-law theories while platforms litigate.

The order binds Kalshi’s New York case. The product category is already broader.

Crypto.com describes its sports-event trading as a CFTC-regulated derivatives feature. Coinbase says its prediction markets are available to U.S. residents, but not in Nevada.

CryptoSlate has previously tracked how state-vs-CFTC fights can turn prediction-market compliance into refunds, blocked access, and venue-by-venue risk. New York adds a new pressure point because the court said state gambling law can complement federal commodities law, at least at this stage.

The next signal is whether the CFTC’s final rule reduces that fragmentation or leaves platforms with a national listing process and local access map. Until then, prediction markets can win federal recognition and still face state-by-state limits on who can actually trade.

![World's daily on-chain volume, showing the pre-prank peak, Source: Dune/ario_57]](https://assets.beincrypto.com/img/-avHN9_82Fzf-o66hJTGVAYBSIg=/smart/9bf00bf07a9042d7bfc0990ea56902d6)