Nigel Farage has resigned as the member of parliament for Clacton-on-Sea on Tuesday, saying that he will contest the by-election his own departure creates, a gamble that pauses two parliamentary standards inquiries into undeclared financial support from crypto backers.

The Reform UK leader announced the decision on his YouTube channel, casting the coming contest as a fight with his opponents.

“This will be a people versus the establishment by-election,” he said, adding that “the people of Clacton should be the judges of my actions.”

He denied breaking any rule, saying, “I have done nothing wrong. I have not broken the law in any way at all.” Farage told reporters that he had followed parliamentary rules on good legal advice.

Are the two inquiries on Farage tied to crypto money?

Farage was already being examined by the Parliamentary Commissioner for Standards over a personal gift of £5 million ($6.7 million) that he received from billionaire Christopher Harborne before the July 2024 election, but did not register.

Harborne, who is currently based in Thailand, holds an estimated 12% stake in Bitfinex and is an early backer of Tether, the company behind the USDT stablecoin. Farage says that the money was for personal security and qualified as a personal gift, which is a category MPs are not required to declare.

On Tuesday, July 7, he confirmed a second inquiry is now open, and this one concerns George Cottrell, a longtime friend who is a convicted fraudster with ties to crypto gambling.

Cottrell reportedly covered Farage’s private security, drivers, social media staff, and accommodation in the 12 months before his election, benefits that Commons rules require new MPs to register when they exceed £300 and relate to political activity.

Farage only declared a £9,253 trip to Belgium and a £15,276 flight as funded by Cottrell, and nothing else.

Cottrell, 32, served eight months in a US prison after pleading guilty to wire fraud following a 2016 arrest at Chicago’s O’Hare airport, where he was traveling with Farage. He has also been linked to Tether.bet, an offshore bookmaker that accepts wagers in cash and in Tether’s USDT.

A spokesperson for Farage called that reporting “baseless and contrived,” stating that the support predated his time as an active politician.

A leader who has bet on Bitcoin

In March, Farage took a 6.31% stake in Stack BTC Plc, a UK-listed Bitcoin treasury firm, buying around £2 million in shares through his investment vehicle Thorn In The Side Ltd. That purchase made him the first sitting UK party leader to publicly buy Bitcoin.

His party, Reform, has since published a draft bill to deregulate crypto and cut taxes on digital asset transactions, and Farage has floated a Bank of England Bitcoin reserve and a capital gains tax cut on crypto.

Liberal Democrat deputy leader Daisy Cooper asked the Financial Conduct Authority (FCA) in April to examine whether Farage’s promotion of digital assets amounts to market abuse.

Future funds from his donors are also about to take a hit as the government recently confirmed that it will close a loophole that lets people sidestep the cap on foreign political donations by moving to the UK.

Harborne and BitMEX co-founder Ben Delo, two of Reform’s largest funders, are reportedly relocating to Britain following the announcement of the cap. However, returning donors will be held to a £100,000 limit for a year after they arrive, a rule that could hit.

Reform raised £9.3 million in the first quarter of 2026, more than Labor and the Conservatives combined, with Harborne and Delo supplying most of it.

Farage’s resignation likely freezes both standards inquiries; however, they could resume after the by-election if regulators judge it proportionate.

Liberal Democrat leader Ed Davey said Farage should pay for the Clacton contest himself and not spend public money, calling the resignation a “stunt.”

Rupert Lowe, the former Reform MP now leading the rival Restore Britain party, said Farage “should have declared that five million pounds.”

Farage won Clacton in 2024 with a majority of 8,400, on his ninth attempt at a Westminster seat after seven earlier defeats. He could face tactical voting from an alliance of progressive parties and a challenge from Restore Britain.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

USDT issuer Tether and crypto lender Ledn have laid out plans to let holders of Tether Gold (XAUT) borrow against the it later in the year, which would open a lending channel taking advantage of the stablecoin issuer’s $23 billion physical gold reserve.

Tether partners with Ledn

Lending platform Ledn announced it will add XAUT to its platform alongside Bitcoin (BTC) and Tether’s dollar-pegged stablecoin USDT. This is expected to go live before the end of 2026, and would let XAUT holders use their holdings as collateral for loans instead of selling off the gold they own.

Each XAUT token represents one troy ounce of physical gold stored in Swiss vaults, according to Tether.

The structure of this product mirrors Ledn’s handling of bitcoin-backed lending for the past few years. Client collateral is held on a 1:1 basis and is not lent out or used to generate yield, the company said.

Gold-backed lending has been controlled by central banks, large financial institutions, and bullion dealers since forever. Tether and Ledn’s partnership is betting on bringing the same concept on-chain, giving holders access to liquidity without forcing the sale of their gold assets.

“As digital assets become an increasingly important part of the global economy, demand is growing for solutions that combine long-term ownership with financial flexibility,” Tether CEO Paolo Ardoino said in a statement.

Tether expands past the dollar

Profits from USDT, the world’s largest stablecoin, have funded expansion into areas well beyond dollar-pegged tokens.

The company has invested in precious metals marketplace Gold.com, partnered with crypto financing firm Antalpha on XAUT lending and physical redemption, and has also backed AI infrastructure provider Northern Data. Tether has also put massive amounts of capital into bitcoin mining and multiple renewable energy projects.

The lending product backed by Tether’s physical gold reserves is expected to expand Ledn’s collateral options beyond its current supported assets.

As at the time of writing, XAUT traded at $4,070.34 per token.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Bitcoin dropped to around $61,500 in recent days, its weakest level in roughly four months, and Peter Schiff wasted no time connecting that slide to a broader argument he has been making about stablecoins.

A Stablecoin On The Move

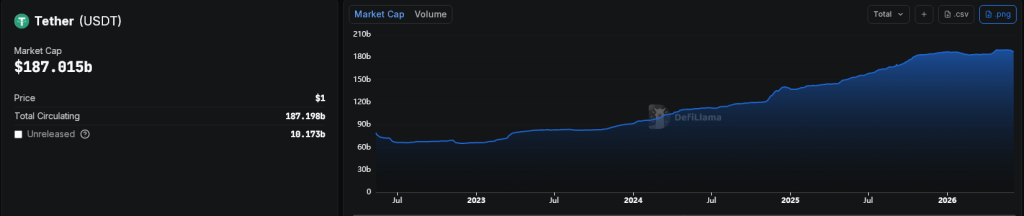

Tether’s USDT has already climbed to a market capitalization of nearly $188 billion, according to data from DeFiLlama, closing the gap with Ethereum to just under $26 billion. Schiff, the economist and longtime Bitcoin critic, says the numbers point to an inevitable outcome.

“The market cap of Tether will soon surpass the market cap of Ethereum,” Schiff wrote on X. “It will eventually surpass the market cap of Bitcoin, too. The only question is how long it will take.”

USDT has become a dominant tool for moving money across crypto markets, and its reach now extends into payments, remittances, and digital dollar transfers — a trend he says supports his case.

USDT holds a one-dollar peg, setting it apart from Bitcoin and Ethereum, and that stability makes it the go-to choice for users who want to move money without taking on price risk.

The market cap of Tether will soon surpass the market cap of Ethereum. It will eventually surpass the market cap of Bitcoin too. The only question is how long it will take.

Schiff has been sounding alarms about Bitcoin for years. His latest comments include a prediction that BTC could eventually fall below $20,000, which would represent a drop of roughly 80% from its October 2025 peak near $126,200.

He has also pointed to weakness in tech stocks as a pressure point for Bitcoin, noting that the crypto asset has relied on the broader tech rally for support.

“It looks like the correction in tech stocks has finally begun,” Schiff said. “As tech stocks sell off, Bitcoin should crash. Gold will likely head in the opposite direction.”

Bitcoin recently suffered a sharp hourly decline of more than $2,000, briefly touching $61,460, as selling pressure spread across the market and triggered over $1 billion in leveraged liquidations.

USDT’s Growing Reach

Reports indicate Ethereum’s position as the second-largest crypto asset is now under pressure from a stablecoin rather than another blockchain competitor.

At current figures, USDT would need to grow by roughly 15% to pull ahead of Ethereum, while matching Bitcoin’s $1.28 trillion market cap would require a far larger expansion of nearly seven times its present size.

Schiff’s prediction has drawn attention not just for its boldness but for its timing, arriving as stablecoin adoption continues rising and crypto markets face renewed turbulence.

Whether the prediction holds up remains an open question, though the narrowing gap between USDT and Ethereum suggests the first part of his forecast may not be far off.

Featured image from Unsplash, chart from TradingView

Tether has applied for seven trademarks in South Korea, including for its company name and logo, in a move that market observers see as a hint of the firm expanding into the South Korean market.

The issuer of the largest stablecoin in the world, USDT, is also expanding its reach into Africa and Asia by partnering with Lemfi. Meanwhile, Tether’s rival Circle (NYSE: CRCL) has already been meeting with major financial institutions in South Korea, setting up a potential showdown between number one and two in the stablecoin issuance business.

Tether and Circle are lining up entry into the South Korean market

Tether, the company behind the world’s largest stablecoin USDT, is making progress in its plans to enter the South Korean market. The Korea Intellectual Property Rights Information Service (KIPRIS) recently received multiple trademark applications from Tether, totaling up to seven.

Tether’s previous filings in the country focused on stablecoin product names, but this batch includes the corporate brand itself and its gold-backed stablecoin Tether Gold (XAUT).

South Korea’s proposed Digital Asset Basic Act is expected to require foreign stablecoin issuers to maintain a domestic branch if they want to distribute their tokens locally, and Tether appears to be positioning itself ahead.

Before Tether’s latest filings, Circle’s CEO Jeremy Allaire visited Seoul in April and met with executives from KB Financial Group, Shinhan Financial Group, and Hana Financial Group to discuss stablecoin payment cooperation and real-world asset tokenization.

Allaire acknowledged the potential in the South Korean market and shared Circle’s plans to establish a Korean subsidiary and obtain a license if the final regulatory framework accepts foreign issuers.

Circle has also signed partnerships with Korean exchanges Dunamu, which operates Upbit, and Bithumb to expand USDC adoption on domestic trading platforms.

Cryptopolitan reported earlier that Hana Card, part of Hana Financial Group, launched a pilot in March allowing foreign visitors to pay at local merchants using USDC through a partnership with Circle and Crypto.com. Other Korean financial firms, including BC Card and KB Kookmin Card, have been testing stablecoin payment infrastructure as well.

Tether has been on an expansion trail

Tether also recently announced an investment in LemFi, a cross-border payments platform that works across communities in the UK, US, Canada, and Europe to recipients in Africa and Asia. The deal will integrate USDT as a settlement layer across LemFi’s payment corridors, replacing multi-day SWIFT-based transfers with blockchain settlement.

Tether’s CEO Paolo Ardoino said in the announcement that the goal of the partnership is to expand financial access for its estimated 585 million users globally.

Cryptopolitan previously reported that Tether recorded $1.04 billion in profit for Q1 2026. The company holds excess reserves of $8.23 billion; enough capital to invest in distribution partners and pursue market entry in jurisdictions like South Korea.

South Korea is home to an estimated 18 million crypto investors. Exchanges in the country recorded over $663 billion in trades through mid-2025, and the country’s retail traders remain a significant part of altcoin markets.

Beyond Tether and Circle, multiple projects are building won-denominated stablecoins. Cryptopolitan reported that the Bank of Korea has been advancing “Project Han River,” its wholesale CBDC initiative, which entered a second phase of real-transaction testing earlier this year.

Regulators are still debating whether or not stablecoin issuance should be restricted to commercial banks or follow a more flexible licensing model. The discussion has been postponed until after South Korea’s June local elections.

Tether and LemFi, two financial juggernauts in different sectors, have announced a partnership. Tether, the issuer of popular stablecoin USDT, announced on Monday that it had invested in the fintech app used to transfer funds from Europe and the Americas to Africa and Asia.

The deal will embed USDT as a system for payments across LemFi’s operating regions, replacing slower bank-to-bank transfer chains with stablecoins and the blockchain.

The Tether-LemFi deal and what it means

Unlike conventional cross-border payment systems, stablecoin-based transfers allow funds to move directly across blockchain networks with fewer delays and lower operation costs. This model will enhance the speed and efficiency of international payments, especially in newly emerging markets.

According to Tether’s statement, the partnership is expected to support the wider adoption of Tether across LemFi’s platform, which could then extend the stablecoin-powered systems into other payment and financial service offerings.

The move reflects a broader trend among fintech firms and stablecoin issuers seeking to position blockchain infrastructure as an alternative to traditional banking rails for global payments, savings, and digital financial services.

The executives have their say

CEO of Tether, Paolo Ardoino, has said the investment aligns with Tether’s strategy of expanding financial access for its estimated 585 million users globally.

Ardoino framed the partnership as part of the company’s effort to strengthen the real-world utility of Tether by integrating blockchain-based settlement into everyday financial services, particularly in regions that rely heavily on cross-border payments and remittances.

“Our investment in LemFi reflects our shared vision on how money moves across borders, prioritizing speed, cost, and transparency,” Ardoino said in Tether’s announcement. “By supporting LemFi’s growth and innovation roadmap, we are helping bring the benefits of a stable digital asset to more people who rely on remittances in their daily lives.”

LemFi CEO and co-founder Ridwan Olalere called the deal “a validation of the direction we are heading.” Olalere added that integrating USDT into LemFi’s infrastructure “brings us closer to that reality” of a financial system that works regardless of where a user lives or sends money, according to Tether’s press release.

Neither company has disclosed the size of the investment.

How does this improve stablecoins’ standing?

For Tether, the LemFi deal extends the company’s push to position USDT as a practical payments infrastructure rather than just a trading instrument. The company reported $1.04 billion in profit for Q1 2026 and holds excess reserves of $8.23 billion, according to Binance Square. This financial position gives Tether capital to invest in distribution partners like LemFi that can help to put the stablecoin in front of non-crypto-native users.

LemFi, on its own part, gains access to Tether’s deep USDT liquidity pool and the technical backing to build a settlement layer on blockchain. The company described its customer base as consisting of “millions of people who live and work across borders,” many of whom, it said, have historically been underserved by traditional financial institutions.

A joint collaboration between Tether, TRON and blockchain analytics firm TRM Labs called the T3 Financial Crime Unit has announced on Wednesday that it has frozen more than $450 million in USDT suspected to be acquired through illicit, criminal means since the initiative launched in September 2024.

The frozen funds by the crime unit involve investigations into various illicit operations including money laundering, crypto exchange hacks, North Korea-linked cyber operations, terrorist cells financing, drug trafficking, and violent crimes including kidnappings and extortion, according to a statement published by Tether.

The T3 FCU has enlisted the help of multiple law enforcement agencies in its fight against illicit activity in the crypto community. These agencies span five different continents, with countries like the U.S., Spain, Germany, the Netherlands and Bulgaria having the highest volume of assets frozen.

Tether’s T3 puts in the work

The T3 FCU reported that it helped in the recovery of 43.9% more illicit proceeds in 2025 compared to the previous year. The unit claimed it can execute asset freezes within 24 hours of a request by law enforcement regarding an investigation, a pace that traditional banks and services find hard to match.

The group pointed to several high-profile cases where it helped with asset freezing and recovery. One involved the freezing of about $26.4 million allegedly connected to a European money-laundering ring that was dismantled alongside Spain’s Guardia Civil in early 2025.

Another case was “Operation Lusocoin”, a Brazilian Federal Police investigation that froze more than 3 billion Brazilian reais in crypto assets, of which 4.3 million USDT linked to a criminal network was a part, according to Tether’s statement. Additional freezes targeted wallets tied to North Korean cyber activity and funds traced to the Bybit hack, with nearly $9 million in crypto funds identified.

In addition, Tether confirmed a $344 million USDT freeze on TRON in April 2026 following intelligence-sharing with U.S. and international law enforcement.

T3 FCU breaks higher ground amid international recognition

The Financial Action Task Force cited T3 FCU earlier this year as an “invaluable resource for law enforcement agencies worldwide.” The FATF highlighted the unit alongside TRM Labs’ Beacon Network as leading examples of public-private partnerships for combating criminal activity in the crypto community.

The recognition comes amid a sharp rise in illicit cryptocurrency activity, with blockchain-related criminal activity reaching a record $158 billion in 2025, according to estimates from TRM Labs. The figures underscore the growing pressure on stablecoin issuers and blockchain platforms to strengthen compliance frameworks as regulators intensify the crypto sector’s scrutiny.

“Compliance is not an option; it is a part of our commitment to protect our users and stop any illicit behaviors,” said Paolo Ardoino in the announcement. “This $450 million milestone is just the beginning of what T3 is capable of,” he added.

Chris Janczewski, who previously served as a special agent with the IRS Criminal Investigation division, said the initiative combines “real-time intelligence and expertise with coordinated public-private action to disrupt illicit activity as it happens.”

The comments reflect an intensified industry effort to ensure stronger oversight and enforcement capabilities.

Is crypto decentralization a myth?

The scale of the recent asset freezes has reignited debate over the level of control centralized stablecoin issuers retain within blockchain ecosystems that are often said to be ‘decentralized’.

Tether includes issuer-level controls that allow Tether to blacklist specific wallet addresses and freeze associated funds, which goes against the intent behind cryptocurrencies like Bitcoin.

According to onchain data compiled by BlockSec, more than $500 million worth of USDT was frozen over a recent 30-day period. This amount extends beyond the activity linked to the T3 Financial Crime Unit in the statement and proves Tether is doing even more blacklisting on multiple blockchains.

FROZEN — Tether’s $344M USDT Lockdown | Crypto Coin Show

Sanctions Enforcement · Stablecoins · Iran

Frozen $344 Million in USDT Locked on Tron

In one of the largest single compliance actions in crypto history, Tether moved to freeze

$344 million worth of USDT across two Tron blockchain wallets at the request of U.S. authorities — wallets now linked by U.S. officials to the Iranian regime.

Crypto Coin Show Editorial Desk|April 24, 2026|Exclusive Analysis

$344M

Total USDT Frozen

2 Wallets

Blacklisted on Tron

$4.4B+

Total Tether Freezes to Date

340+

Global Agency Partners

A Landmark Freeze — and an Iran Connection

On Thursday, April 23, 2026, Tether — the issuer of the world’s largest stablecoin by volume — announced it had frozen $344 million in USDT across two blockchain addresses on the Tron network. The action was carried out in coordination with the U.S. Office of Foreign Assets Control (OFAC) and multiple federal law enforcement agencies, following intelligence that the wallets were tied to illicit financial activity.

Within 24 hours, the story grew considerably larger. U.S. officials told CNN on Friday that the frozen funds carried material links to the Iranian regime, including transaction trails running through Iranian exchanges and intermediary wallets connected to accounts associated with Iran’s Central Bank. Treasury Secretary Scott Bessent confirmed the sanctions action, framing it as part of a broader Trump administration campaign to cut off Tehran’s financial lifelines as nuclear diplomacy stalls.

USDT is not a safe haven for illicit activity. When credible links to sanctioned entities or criminal networks are identified, we act immediately and decisively.

— Paolo Ardoino, CEO, Tether · April 23, 2026

📊 Key Figures

Total USDT Frozen

$344M

Wallet 1 (TNiq9…)

~$213M

Wallet 2 (TTiDL…)

~$131M

Network

Tron (TRC-20)

Coordination

OFAC + FBI

Alleged Nexus

Iran / CBoI

Action Date

Apr 23, 2026

🌐 Tether Compliance Scale

Total Assets Frozen ($4.4B)

U.S.-Linked Cases ($2.1B)

This Action ($344M)

Global Agency Partners

340+

Countries

65

Cases Supported

2,300+

The Two Wallets

Blockchain security firm PeckShield flagged the two addresses after they appeared on Tether’s blacklist on April 23, before any official explanation was given. Together, the wallets held slightly more than $344 million in USDT at the time of the freeze.

🔒 Locked

TNiq9AXBp9EjUqhDhrwrfvAA8U3GUQZH81

~$213M

USDT · Tron Network

🔒 Locked

TTiDLWE6fZK8okMJv6ijg42yrH6W2pjSr9

~$131M

USDT · Tron Network

According to Chainalysis, the two Tron addresses were regularly active years ago — moving tens of millions of dollars in single transfers, often to private wallets. U.S. officials noted the behavior mirrored patterns seen in other known IRGC-linked addresses. The wallets were blacklisted at the smart contract level, meaning no further movement of the funds is possible until cleared by authorities.

⚠ Iran’s Crypto Strategy

According to the U.S. Treasury Department, Iran’s central bank has increasingly leaned into digital assets — particularly stablecoins on the Tron network — to mask cross-border transactions and support trade flows under sanctions pressure. Blockchain analytics firms TRM Labs and Chainalysis estimate that Iran-related crypto flows reached billions of dollars in 2025 alone.

🔍 Context: Tron & Iran

The Tron blockchain has become a preferred rail for sanctions-evasion activity due to its low fees and high USDT liquidity. U.S. authorities have increasingly focused enforcement actions on Tron-based USDT wallets linked to Iranian exchanges, IRGC-associated entities, and intermediary networks routing funds through complicit third-country actors.

How Tether Can Freeze Funds

Unlike decentralized tokens, USDT is a centralized stablecoin — meaning Tether retains the technical ability to freeze or blacklist any wallet at the smart contract level. The company describes this as a feature, not a flaw: public blockchains create a visible transaction trail that investigators can follow in near-real time, something traditional cash networks cannot provide.

When OFAC or a law enforcement partner flags an address, Tether’s compliance team can restrict the wallet within hours — preventing any further transfer of funds. The frozen USDT remains in the address but is effectively inert, unable to be spent, sent, or swapped, until legal proceedings determine its fate.

A Growing Compliance Empire

This action does not exist in isolation. Tether has been systematically expanding its compliance infrastructure over the past several years, and Thursday’s move is a statement of that ambition. The company now reports collaborating with more than 340 law enforcement agencies across 65 countries, having assisted in more than 2,300 investigations globally — over 1,200 of which involve U.S. authorities.

Cumulatively, Tether has now frozen more than $4.4 billion in USDT to date, including $2.1 billion specifically tied to U.S. law enforcement cases. The $344 million freeze on April 23 ranks as one of the single largest compliance actions the company has ever executed.

A Pattern of Major Freezes

November 2023

~$225M frozen — Wallets linked to a Southeast Asia human-trafficking and “pig butchering” scam ring. One of the first major cooperative actions with U.S. DOJ.

January 2026

~$182M frozen — Five Tron wallets restricted in another coordinated action with OFAC. Linked to sanctions evasion networks.

April 2026 (Current)

$344M frozen — Two Tron wallets blacklisted at the request of U.S. authorities. Linked within 24 hours to the Iranian regime and Central Bank of Iran intermediaries. Largest single action to date.

The Stablecoin Compliance Debate

The freeze arrives amid a broader, heated debate about what stablecoin issuers owe the public — and regulators — when it comes to stopping illicit financial flows. The controversy was reignited earlier this month when the Drift Protocol was exploited for $285 million. Critics argued that Circle, the issuer of the competing USDC stablecoin, moved too slowly to freeze funds connected to the exploit.

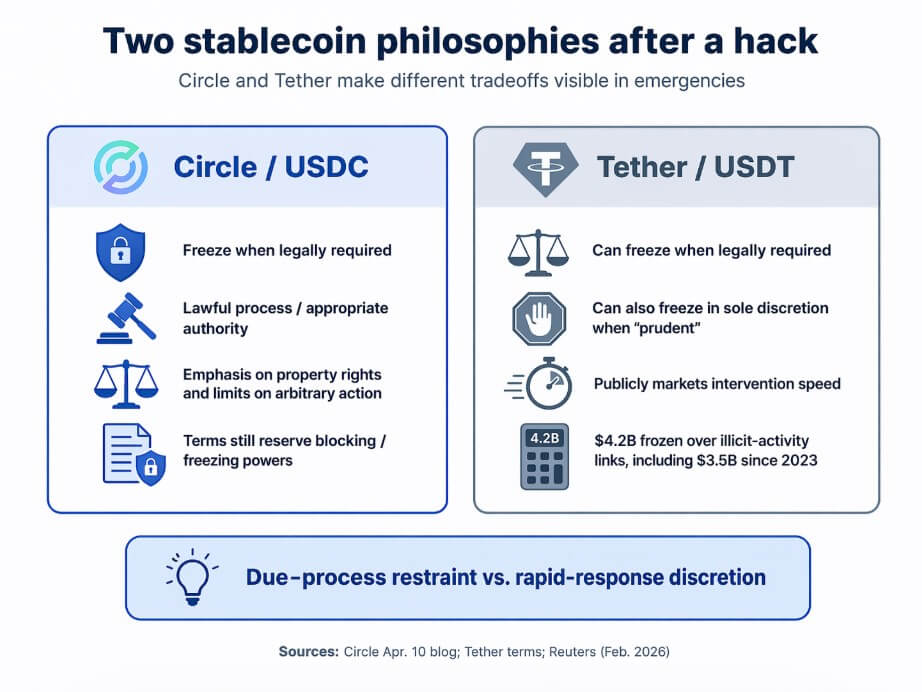

Circle pushed back, with Chief Strategy Officer Dante Disparte stating that the company only freezes funds when the law explicitly requires it or when court orders mandate action — not through unilateral judgment. Tether has taken the opposite stance, positioning itself as a proactive partner to law enforcement even before formal legal orders arrive.

The way to get at Iran at this point — because Iran is truly sanctioned out — is to go with the third-country actors enabling them.

— Daniel Tannebaum, Atlantic Council · Senior Fellow

⚖️ Circle vs. Tether

Tether Freeze Philosophy

Proactive

Circle Stance

Court Order Only

Drift Protocol Fallout

Circle Sued

Drift Adopted

USDT (Tether)

The fallout from Drift was swift: the protocol announced it would dump USDC in favor of USDT, citing Tether’s more assertive compliance posture. A class-action lawsuit against Circle followed. The episode cemented Tether’s narrative as the enforcement-friendly stablecoin — and its April 23 action is a deliberate reinforcement of that brand.

Geopolitical Dimensions

The Iran link elevates this story beyond a routine compliance action. Treasury Secretary Scott Bessent confirmed the sanctions in a statement framing it as part of the Trump administration’s escalating economic campaign against Tehran — describing Washington’s intent to “follow the money” as diplomatic efforts around the conflict stall.

Iran has spent years developing techniques to route funds through third-country actors, shell companies, and now increasingly through decentralized blockchain infrastructure. Earlier in 2026, both Tether and Circle were involved in blacklisting a hot wallet belonging to Iranian exchange Wallex, while U.S. authorities sanctioned additional platforms accused of routing IRGC funds through USDT on the Tron network.

Some analysts caution against overstating the impact. Experts note that Iran has decades of experience adapting to economic pressure, and that the more consequential choke point may be the third-country jurisdictions — particularly China — that continue to enable Iranian trade flows. Still, the ability to surgically freeze $344 million in a matter of hours marks a significant expansion of the U.S. sanctions toolkit into the digital asset space.

What Comes Next

Tether has confirmed it is expanding further into the U.S. domestic market. The company recently launched USAT — a new stablecoin token built for compliance with emerging federal stablecoin regulation — in partnership with federally regulated crypto bank Anchorage Digital. The initiative is led by former White House crypto advisor Bo Hines.

Regulators and lawmakers are watching closely. With stablecoin legislation advancing on Capitol Hill, the question of whether issuers like Tether should be required — rather than just permitted — to freeze funds linked to sanctions is becoming a central policy debate. For now, Tether is volunteering. And with $344 million locked on Tron, Washington appears to appreciate the help.

Crypto rhetoric has long prized the ability to transact without gatekeepers, to move value across borders without asking permission, and to hold assets no institution could seize.

Crypto culture treated these as design virtues, properties that builders embedded with ethical weight by deliberate architectural choice. Then the Drift exploit happened, and the backlash told a different story.

On Apr. 1, Drift suffered a major exploit. Circle later described the publicly reported losses as exceeding $270 million, while other reports put the figure around $285 million and documented criticism that Circle had not frozen stolen USDC as it moved across its cross-chain rails.

The attacker routed roughly $232 million in USDC from Solana to Ethereum using Circle’s Cross-Chain Transfer Protocol. The backlash stemmed from users and observers wanting to know why Circle had not intervened sooner.

Days later, Tether CEO Paolo Ardoino posted that Tether had frozen 3.29 million USDT tied to the Rhea Finance attacker, framing the intervention as proof that “Tether cares.”

Circle published its formal response on Apr. 10, and its core argument was that USDC freezes occur when the law requires action. Circle is legally compelled by an appropriate authority through a lawful process.

Circle pushed back on the idea that an issuer should act as an ad hoc chain police force, arguing that open access to permissionless infrastructure is a feature, and that the bigger problem is that legal frameworks have not yet kept pace with the speed of on-chain exploits.

The stablecoin issuer also made a property-rights argument, claiming that arbitrary freezes set dangerous precedents for lawful users, and the power to freeze is a compliance obligation, constrained by lawful process and legal compulsion, authorized only through formal legal channels.

The complication is that Circle’s own legal documents tell a more layered story.

USDC terms state that transfers are irreversible and that Circle carries no obligation to track or determine the provenance of balances.

Those same terms also reserve Circle’s right to block certain addresses and, for Circle-custodied balances, freeze associated USDC in its sole discretion when it believes those addresses may be tied to illegal activity or terms violations.

Circle holds meaningful freeze power and frames it as a tightly bound compliance function, constrained by legal process and compulsion.

Ardoino’s Rhea post was a boast, and Tether’s terms grant it broad discretion by stating that the company may freeze tokens as required by law or whenever it determines, in its sole discretion, that doing so is prudent, and authorizing it to blacklist token addresses.

In February, Tether froze approximately $4.2 billion in USDT due to links to illicit activity, with $3.5 billion of that since 2023.

Circle freezes USDC only when legally compelled, while Tether reserves sole discretion to freeze and has frozen $4.2 billion over illicit-activity links.

The feature nobody advertised

What Drift and Rhea forced into the open is a question that stablecoin competition had not yet fully surfaced: in a hack, what do users actually want from an issuer?

The anti-censorship instincts that shaped crypto’s early culture tend to lose their force the moment users need an emergency brake. Affected protocols, exchanges holding stolen funds, and victims watching their balances drain want to know who can stop the thief.

That reframes freeze capacity as more of a consumer-protection feature.

Tether has been accumulating a record of intervention and visibility. Ardoino’s Rhea post was designed to be read as a product statement, and in the context of a fresh exploit, it worked.

The emotional and practical logic is accessible, showing that one issuer froze stolen funds the same day an attacker moved them, while another issuer said legal timelines tied its hands.

This makes optics difficult for Circle regardless of the legal merits of its position.

Stablecoins are quietly differentiating themselves in emergency governance, alongside reserve composition and exchange liquidity.

The cost of the feature

The case for Circle’s position is real and does not require dismissing the Drift backlash to hold. Broad issuer discretion over freezes creates risks that extend far beyond hack scenarios.

An issuer that can freeze tokens in its sole discretion when it determines it is prudent can freeze tokens for reasons unrelated to protecting victims. Politically contentious addresses, disputed transactions, regulatory scrutiny from a single jurisdiction, or simple operational error can all trigger freezes under terms as broad as Tether’s.

The same capacity that lets an issuer stop a thief also lets it stop a protester, a dissident from a sanctioned country, or a business whose activity it finds inconvenient.

Circle’s public writing on the Drift exploit is, among other things, a defense against that risk. The argument that emergency intervention needs new legal frameworks and safe-harbor structures is also an argument that the current situation is a problem, even when the targets are criminals.

The absence of defined standards means an issuer can act generously today and overreach tomorrow, with no formal mechanism to distinguish the two.

Tether’s freeze record has not yet produced a major documented wrongful-freeze controversy, but that record is also vast and not fully transparent.

Reports on the $4.2 billion in frozen USDT withhold the details of each decision, the legal process underlying each freeze, and the error rate across thousands of enforcement actions.

Fast intervention looks different in the abstract when the process generating those interventions is opaque.

Benefit of fast freezes

Cost of broad freeze discretion

Can slow or stop stolen funds

Can enable arbitrary intervention

May improve recovery odds

Can affect lawful users

Helps exchanges/protocols in crises

Can reflect political or regulatory pressure

Looks like consumer protection in hacks

Process may be opaque

Becomes a due-diligence feature

Wrongful-freeze risk may be hard to challenge

Two paths from here

The bull case for intervention-first issuers runs in a world where hacks keep coming, and recoverability keeps rising on the priority list.

More regulatory scrutiny on exchanges to show they take asset protection seriously, and more institutional users who need to demonstrate due diligence in custody and recovery. These are factors that push emergency freeze capacity to the center of stablecoin evaluation.

In that scenario, Tether’s public freeze record and broad discretionary terms become genuine competitive assets. Exchanges and protocols that have experienced exploits now treat fast-intervention capacity as a due diligence criterion when choosing which stablecoin to hold as primary liquidity.

Circle has to either act faster through new legal mechanisms or accept that some market segments will treat its rule-of-law posture as a liability in crises. Ardoino’s Rhea post, in retrospect, looks like an early entry in a competition that the market eventually formalizes.

The bear case for that same model runs through wrongful freezes, regulatory backlash, and the discovery that broad discretion is often a liability as much as a virtue.

A high-profile incorrect freeze, such as an address flagged as malicious that belongs to a legitimate user, a jurisdiction-specific enforcement action that appears to be politically targeted at users in other markets, or an operational error that freezes clean funds during a market stress event, turns the same emergency-governance story toxic.

In that world, Circle’s insistence on lawful process and defined standards looks like principled restraint, a deliberate commitment to defined limits over speed, and users place a real premium on an issuer whose freeze decisions carry formal accountability.

The crypto community’s historical skepticism toward centralized control reasserts itself as hard-won practical wisdom, grounded in the documented costs of unchecked issuer discretion.

The stablecoin winners in that scenario are the ones whose intervention power is real but bounded. Issuers who can act in genuine emergencies and demonstrate they held back in ambiguous ones.

Stablecoin governance splits between intervention-first issuers gaining crisis goodwill and bounded-discretion issuers winning users who reprice centralization risk, per Circle and Tether materials.

As stablecoins deepen their role in institutional payments, treasury workflows, and regulated financial infrastructure, governance under stress becomes as material as reserve quality or distribution reach.

The question that Drift and Rhea put on the table of how much control users want an issuer to have has no clean universal answer. Institutions with large exposures and recovery obligations may want emergency brakes, while individuals holding stablecoins across politically sensitive jurisdictions may want the opposite.

Protocols with mixed user bases need to answer for both.

The real contest now is for the version of stablecoin governance that earns enough trust from enough users to become the default.