The Bank for International Settlements (BIS) has reported its assessment of stablecoins based on specific variables, and has concluded that they do not function as money was originally intended. The institution has warned in its latest 2026 Annual Economic Report that dollar-pegged tokens are driving a new form of dollarization in emerging economies.

The report was based on an assessment using multiple criteria for money, and made a distinct comparison of stablecoins to ETFs.

BIS report on stablecoins

The umbrella institution for central banks evaluated stablecoins on four criteria considered essential for entities described as money. These criteria include singleness, elasticity, interoperability, and integrity. Stablecoins were said to have failed all four, according to the report.

Singleness translates to the concept of one unit always being equal to one unit of the underlying currency regardless of the issuer. Stablecoin prices on secondary markets tend to drift from their $1 peg, sometimes just slightly.

Elasticity requires the supply of any entity seen as money to increase and decrease with economic demand. Stablecoins use a model where issuers mint tokens only after receiving equivalent cash deposits, which prevents this flexible expansion according to demand from happening.

The BIS compared stablecoins to ETFs, stating that stablecoins behave more like shares in an exchange-traded fund instead of cash deposits.

Dollar dominance has increased globally

Over 99% of the roughly $320 billion stablecoin market, as of the end of May 2026, is denominated in US dollars. Tether’s USDT and Circle’s USDC account for most of that figure. A separate BIS research paper from May 5 estimated dollar dominance in stablecoin value at approximately 98%.

The report states that this concentration is a structural problem for emerging markets and developing economies. The BIS calls this “stablecoin dollarization” and warns it mirrors the historical pattern of deposit dollarization, where savings are shifted into foreign bank accounts during crises, happening at a faster pace since crypto operates outside traditional banking infrastructure.

Countries including Turkey, Argentina, and Nigeria have already had a lot of stablecoin adoption as citizens seek dollar exposure outside formal channels.

Several emerging economies have imposed restrictions on cross-border stablecoin use. The BIS has expressed skepticism on how well these restrictions can hold, since controls that function against traditional bank deposits do not translate well to self-custodial crypto tokens.

Potential negative economic effects of stablecoins

The BIS created a model exploring possible happenings if the stablecoin market cap grew to between $1 trillion and $3 trillion, and concluded that the net effect on economic output would still be “modestly negative.”

As deposits migrate from traditional banks to stablecoin issuers (who park reserves in US Treasuries and money market instruments), banks continue to lose a cheap funding source. To compete, they would need to raise deposit rates, which would increase lending costs, and slow economic activity.

The BIS has recommended building what it calls a “unified ledger” for central bank monies, aiming to combine tokenized central bank reserves with commercial bank money on a shared infrastructure. The report cited Project Agora, a cross-border payments prototype, as evidence that this “unified” approach is technically feasible, according to Binance News.

Ouinex Launches Multi-Asset Exchange Combining Crypto and TradFi Infrastructure

Crypto Exchange · News

Ouinex Launches Multi-Asset Exchange Merging Crypto and Traditional Finance Infrastructure

The Swiss-based platform lets traders use Bitcoin and USDT as collateral to trade stocks, forex, commodities, and indices — with liquidity drawn from TradFi infrastructure rather than crypto perpetuals.

Crypto Coin ShowJune 2026ExchangeTradFi · DeFi

500xMax Leverage

$9M+Raised

5,000+Community Investors

0VC Investors

37Person Team

5+Regulatory Jurisdictions

100xDeeper Liquidity vs Perps

7xCheaper Spreads

$0.1334TGE Price

50%+Tokens Already Staked

3yrStaking Cliff

Mid-June 2026TGE

500xMax Leverage

$9M+Raised

5,000+Community Investors

0VC Investors

37Person Team

5+Regulatory Jurisdictions

100xDeeper Liquidity vs Perps

7xCheaper Spreads

$0.1334TGE Price

50%+Tokens Already Staked

3yrStaking Cliff

Mid-June 2026TGE

Ouinex, a live and regulated multi-asset exchange, is positioning itself as the first platform to give crypto-native traders direct access to global financial markets — stocks, indices, forex, commodities, and gold — using their existing crypto holdings as collateral, without converting to fiat or opening a separate brokerage account.

The Fragmented Trader Problem

For the past decade, active traders have been forced to maintain parallel accounts across multiple platforms: a crypto exchange for spot and perpetuals, a traditional broker for equities and forex, and increasingly, separate apps for commodities and indices. Every transfer between platforms introduces friction, cost, and delay — particularly damaging during fast-moving market events.

Ouinex CEO Ilies Larbi, who spent 20 years in traditional finance before founding the exchange, identified this fragmentation as the core problem in 2022. “The user journey was super fragmented,” Larbi noted. “At the end of the day, it’s all trading. The question was whether you could build a product that merges the two.”

The result is a platform that handles spot crypto trading alongside derivatives on traditional financial assets — all within the same account, using the same collateral pool.

₿

Crypto Spot

BTC, ETH, altcoins

∞

Crypto Perps

Leveraged perpetuals

📈

Equities

NASDAQ, DAX, Dow

€

Forex

EUR/USD, GBP/JPY+

🛢

Commodities

Oil, gold, and more

◈

Indices

S&P 500, global

Why TradFi Infrastructure Changes the Liquidity Equation

The central technical distinction between Ouinex and competitors entering the multi-asset space is its decision not to build traditional financial products on top of crypto perpetual infrastructure — the approach taken by platforms like Hyperliquid, Binance, and others rolling out stock or commodity perps.

When crypto exchanges offer gold or forex exposure via perpetuals on a central limit order book, they are starting from scratch on the liquidity side. Market makers must be recruited specifically for each instrument, pricing is inefficient in the early stages, and the result is wider spreads and shallower order books compared to the established TradFi equivalents.

Ouinex routes its TradFi instrument trading through existing financial market infrastructure — the same pipes that have underpinned institutional currency and commodities trading for decades. The consequence, according to the company, is measurably better execution for retail traders.

“We’re about seven times cheaper and approximately 100x deeper in liquidity on instruments like Euro Dollar — versus platforms using the crypto perpetual approach. That’s not small. They’re a billion-dollar company. We’re barely a startup.”

Ilies Larbi — CEO and Founder, Ouinex

On the EUR/USD order book specifically, Ouinex claims its top five layers hold approximately $10 million in available liquidity, compared to roughly $500,000 on competing crypto-native platforms offering the same instrument as a perpetual. The spread advantage, the company states, is around seven times in the trader’s favour.

Metric

Crypto-Native Perp Approach

Ouinex TradFi Infrastructure

EUR/USD liquidity (top 5 layers)

~$500k

~$10M

Spread vs TradFi benchmark

~7x wider

At par

Commission on TradFi instruments

Variable

Zero

Collateral accepted

USDT / stablecoins

USDT, USDC, BTC+

Max leverage (EUR/USD)

Up to 100x

Up to 500x

The 500x maximum leverage figure, while striking, applies specifically to low-volatility instruments like major forex pairs. Larbi has been explicit that volatility-adjusted risk on a 500x EUR/USD position is materially lower than a 100x position on a cryptocurrency perpetual, where daily price swings can easily exceed the margin threshold.

Crypto Collateral for Global Markets

A key feature of the Ouinex architecture is the ability to use crypto assets as collateral for TradFi positions without liquidating those holdings into fiat. Currently, traders can deposit USDT and USDC to fund their margin accounts. A forthcoming update will extend this to native crypto assets including Bitcoin.

The practical implication is that a trader holding Bitcoin during a period of low crypto volatility — or wanting to hedge their exposure — can use that same BTC as margin to take a position in oil, forex, or an equity index. The capital does not need to leave the crypto ecosystem at any point, and no traditional bank wires or card deposits are required.

This removes one of the primary structural barriers to crypto traders participating in TradFi markets: the friction of fiat on-ramps, which typically involve delays, fees, and banking system dependencies that crypto-native users are specifically trying to avoid.

$9M+Raised from community

5,000+Investor base

0VC investors

37Full-time team

Community-Funded, Zero Venture Capital

Ouinex has raised over $9 million from more than 5,000 retail investors — a deliberate strategy to avoid venture capital entirely. The company ran a multi-phase community pre-sale of its $OUIX token, using each round to demonstrate ongoing product delivery before asking investors to commit further capital.

The decision to exclude VCs is structural rather than ideological. Larbi has been direct about the mechanics: VC token allocations often come fully unlocked, creating immediate incentive to liquidate at listing. The result is a predictable pattern of sell pressure that disproportionately affects retail buyers who entered on the back of the project’s hype at launch.

“The crypto industry is mature enough now to understand what VCs do. We’ve seen those wicks. We know how it happens. There was also no need — we had a community ready to believe in the product.”

Ilies Larbi — CEO and Founder, Ouinex

Ouinex applied the same logic to its market maker relationship, opting for a retainer model rather than granting a token allocation. Under the retainer structure, the market maker has no inventory of $OUIX to sell, eliminating one of the most common vectors for token price manipulation in new listings. The exchange itself serves as the primary listing venue, meaning no tokens need to be surrendered to a tier-one exchange as a listing fee.

Ouinex is approaching its token generation event (TGE), set for mid-June 2026, with $OUIX priced at $0.1334. The token serves several functions within the exchange ecosystem: reduced trading fees, cash back on derivatives volume credited in USDT every 24 hours, enhanced APY on the platform’s earn offering, and improved allocation access through the Ouinex launchpad.

A buy-and-burn mechanism allocates a percentage of exchange revenue to repurchasing and destroying $OUIX tokens, creating a deflationary supply dynamic that ties token value directly to platform trading volume. Critically, this revenue stream is drawn from every asset class on the platform — crypto, forex, stocks, commodities, and indices — giving $OUIX a broader revenue surface than exchange tokens tied purely to crypto trading.

TGE Price

$0.1334

TGE Date

Mid-June 2026

Already Staked

50%+

Staking Cliff

3 Years

Revenue Sources

Crypto · Forex · Stocks · Commodities · Indices

Mechanism

Buy & Burn

More than 50% of the total token supply is already staked under a three-year cliff — an unusually strong signal of long-term holder conviction ahead of listing. For context, the three-year cliff means the majority of current token holders cannot sell for at least three years from their staking date, structurally constraining near-term sell pressure beyond the typical lock-up periods seen in comparable exchange token launches.

Investors in the community pre-sale fall into two categories: token holders, who participated in the $OUIX pre-sale, and equity shareholders, who took a direct stake in the operating company. The dual structure gives the project both a token-aligned community and a cap table of shareholders with economic interest in the underlying business.

Market Context: Why Now

The timing of Ouinex’s launch aligns with a visible shift in how major crypto exchanges approach traditional financial assets. Binance has introduced stock tokens; HyperLiquid has added an S&P 500 instrument; MexC and BitMEX have made similar moves. The direction of travel is clear — the largest exchanges are converging on multi-asset coverage.

The distinction Ouinex draws is one of infrastructure: building on top of proven TradFi liquidity rails rather than adapting crypto perpetual infrastructure to handle instruments it was not originally designed for. Whether that architectural choice translates into sustained competitive advantage will depend on execution at scale — but the early benchmarks on spreads and order book depth suggest the model is functioning as intended.

High commodity volatility in 2026 — driven by geopolitical events including Iran-related oil market movements — has also provided near-term validation. Ouinex has reported that oil has overtaken EUR/USD as its highest-volume instrument in recent periods, a cross-sell pattern that demonstrates traders are actively using the multi-asset functionality rather than treating it as a secondary feature.

“Bitcoin is consolidating around the 70s. But look at the oil market — amazing opportunities, lots of movement. Volatility means opportunity. The platform exists precisely for that moment.”

Ilies Larbi — CEO and Founder, Ouinex

The platform is live, regulated across five or more jurisdictions, and accepting users globally. US access is available for most features. The team consists of 37 full-time staff, and the company is accepting platform feedback directly — with confirmed rewards for bug reports and feature suggestions submitted via the platform.

Watch

Blockchain Interviews: Ilies Larbi, CEO of Ouinex — Full Interview with Ashton Addison

Bitcoin dropped to around $61,500 in recent days, its weakest level in roughly four months, and Peter Schiff wasted no time connecting that slide to a broader argument he has been making about stablecoins.

A Stablecoin On The Move

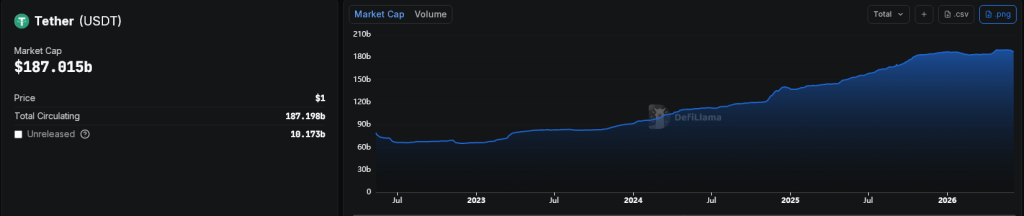

Tether’s USDT has already climbed to a market capitalization of nearly $188 billion, according to data from DeFiLlama, closing the gap with Ethereum to just under $26 billion. Schiff, the economist and longtime Bitcoin critic, says the numbers point to an inevitable outcome.

“The market cap of Tether will soon surpass the market cap of Ethereum,” Schiff wrote on X. “It will eventually surpass the market cap of Bitcoin, too. The only question is how long it will take.”

USDT has become a dominant tool for moving money across crypto markets, and its reach now extends into payments, remittances, and digital dollar transfers — a trend he says supports his case.

USDT holds a one-dollar peg, setting it apart from Bitcoin and Ethereum, and that stability makes it the go-to choice for users who want to move money without taking on price risk.

The market cap of Tether will soon surpass the market cap of Ethereum. It will eventually surpass the market cap of Bitcoin too. The only question is how long it will take.

Schiff has been sounding alarms about Bitcoin for years. His latest comments include a prediction that BTC could eventually fall below $20,000, which would represent a drop of roughly 80% from its October 2025 peak near $126,200.

He has also pointed to weakness in tech stocks as a pressure point for Bitcoin, noting that the crypto asset has relied on the broader tech rally for support.

“It looks like the correction in tech stocks has finally begun,” Schiff said. “As tech stocks sell off, Bitcoin should crash. Gold will likely head in the opposite direction.”

Bitcoin recently suffered a sharp hourly decline of more than $2,000, briefly touching $61,460, as selling pressure spread across the market and triggered over $1 billion in leveraged liquidations.

USDT’s Growing Reach

Reports indicate Ethereum’s position as the second-largest crypto asset is now under pressure from a stablecoin rather than another blockchain competitor.

At current figures, USDT would need to grow by roughly 15% to pull ahead of Ethereum, while matching Bitcoin’s $1.28 trillion market cap would require a far larger expansion of nearly seven times its present size.

Schiff’s prediction has drawn attention not just for its boldness but for its timing, arriving as stablecoin adoption continues rising and crypto markets face renewed turbulence.

Whether the prediction holds up remains an open question, though the narrowing gap between USDT and Ethereum suggests the first part of his forecast may not be far off.

Featured image from Unsplash, chart from TradingView

U.S. Treasury Secretary Scott Bessent announced today that America has now seized a cumulative total of approximately $1 billion in Iranian cryptocurrency assets under its escalating sanctions campaign.

Cumulative Total Hits $1 Billion

The figure represents the running total seized to date, not a single new action announced today.

Bessent had previously reported nearly $500 million in late April, with today’s update reflecting additional freezes accumulated since then.

Operation Economic Fury Accelerates

Launched in March 2025, Operation Economic Fury targets Iran’s sanctions-evasion networks. Iran has relied on stablecoins, particularly USDT on Tron, to move funds for oil sales and IRGC operations.

The U.S. works with issuers like Tether and blockchain analytics firms to identify and immobilize wallets.

Assets are held “on behalf of the Iranian people” and some face claims from terrorism victims.

Expect continued OFAC wallet designations and potential forfeitures in coming months. Iran’s economy already grapples with rial devaluation, banking strains, and reduced oil revenue.

This cumulative milestone marks a significant escalation in financial warfare, showing how traceable blockchain activity can be weaponized against sanctions evasion.

Tether has applied for seven trademarks in South Korea, including for its company name and logo, in a move that market observers see as a hint of the firm expanding into the South Korean market.

The issuer of the largest stablecoin in the world, USDT, is also expanding its reach into Africa and Asia by partnering with Lemfi. Meanwhile, Tether’s rival Circle (NYSE: CRCL) has already been meeting with major financial institutions in South Korea, setting up a potential showdown between number one and two in the stablecoin issuance business.

Tether and Circle are lining up entry into the South Korean market

Tether, the company behind the world’s largest stablecoin USDT, is making progress in its plans to enter the South Korean market. The Korea Intellectual Property Rights Information Service (KIPRIS) recently received multiple trademark applications from Tether, totaling up to seven.

Tether’s previous filings in the country focused on stablecoin product names, but this batch includes the corporate brand itself and its gold-backed stablecoin Tether Gold (XAUT).

South Korea’s proposed Digital Asset Basic Act is expected to require foreign stablecoin issuers to maintain a domestic branch if they want to distribute their tokens locally, and Tether appears to be positioning itself ahead.

Before Tether’s latest filings, Circle’s CEO Jeremy Allaire visited Seoul in April and met with executives from KB Financial Group, Shinhan Financial Group, and Hana Financial Group to discuss stablecoin payment cooperation and real-world asset tokenization.

Allaire acknowledged the potential in the South Korean market and shared Circle’s plans to establish a Korean subsidiary and obtain a license if the final regulatory framework accepts foreign issuers.

Circle has also signed partnerships with Korean exchanges Dunamu, which operates Upbit, and Bithumb to expand USDC adoption on domestic trading platforms.

Cryptopolitan reported earlier that Hana Card, part of Hana Financial Group, launched a pilot in March allowing foreign visitors to pay at local merchants using USDC through a partnership with Circle and Crypto.com. Other Korean financial firms, including BC Card and KB Kookmin Card, have been testing stablecoin payment infrastructure as well.

Tether has been on an expansion trail

Tether also recently announced an investment in LemFi, a cross-border payments platform that works across communities in the UK, US, Canada, and Europe to recipients in Africa and Asia. The deal will integrate USDT as a settlement layer across LemFi’s payment corridors, replacing multi-day SWIFT-based transfers with blockchain settlement.

Tether’s CEO Paolo Ardoino said in the announcement that the goal of the partnership is to expand financial access for its estimated 585 million users globally.

Cryptopolitan previously reported that Tether recorded $1.04 billion in profit for Q1 2026. The company holds excess reserves of $8.23 billion; enough capital to invest in distribution partners and pursue market entry in jurisdictions like South Korea.

South Korea is home to an estimated 18 million crypto investors. Exchanges in the country recorded over $663 billion in trades through mid-2025, and the country’s retail traders remain a significant part of altcoin markets.

Beyond Tether and Circle, multiple projects are building won-denominated stablecoins. Cryptopolitan reported that the Bank of Korea has been advancing “Project Han River,” its wholesale CBDC initiative, which entered a second phase of real-transaction testing earlier this year.

Regulators are still debating whether or not stablecoin issuance should be restricted to commercial banks or follow a more flexible licensing model. The discussion has been postponed until after South Korea’s June local elections.

Tether and LemFi, two financial juggernauts in different sectors, have announced a partnership. Tether, the issuer of popular stablecoin USDT, announced on Monday that it had invested in the fintech app used to transfer funds from Europe and the Americas to Africa and Asia.

The deal will embed USDT as a system for payments across LemFi’s operating regions, replacing slower bank-to-bank transfer chains with stablecoins and the blockchain.

The Tether-LemFi deal and what it means

Unlike conventional cross-border payment systems, stablecoin-based transfers allow funds to move directly across blockchain networks with fewer delays and lower operation costs. This model will enhance the speed and efficiency of international payments, especially in newly emerging markets.

According to Tether’s statement, the partnership is expected to support the wider adoption of Tether across LemFi’s platform, which could then extend the stablecoin-powered systems into other payment and financial service offerings.

The move reflects a broader trend among fintech firms and stablecoin issuers seeking to position blockchain infrastructure as an alternative to traditional banking rails for global payments, savings, and digital financial services.

The executives have their say

CEO of Tether, Paolo Ardoino, has said the investment aligns with Tether’s strategy of expanding financial access for its estimated 585 million users globally.

Ardoino framed the partnership as part of the company’s effort to strengthen the real-world utility of Tether by integrating blockchain-based settlement into everyday financial services, particularly in regions that rely heavily on cross-border payments and remittances.

“Our investment in LemFi reflects our shared vision on how money moves across borders, prioritizing speed, cost, and transparency,” Ardoino said in Tether’s announcement. “By supporting LemFi’s growth and innovation roadmap, we are helping bring the benefits of a stable digital asset to more people who rely on remittances in their daily lives.”

LemFi CEO and co-founder Ridwan Olalere called the deal “a validation of the direction we are heading.” Olalere added that integrating USDT into LemFi’s infrastructure “brings us closer to that reality” of a financial system that works regardless of where a user lives or sends money, according to Tether’s press release.

Neither company has disclosed the size of the investment.

How does this improve stablecoins’ standing?

For Tether, the LemFi deal extends the company’s push to position USDT as a practical payments infrastructure rather than just a trading instrument. The company reported $1.04 billion in profit for Q1 2026 and holds excess reserves of $8.23 billion, according to Binance Square. This financial position gives Tether capital to invest in distribution partners like LemFi that can help to put the stablecoin in front of non-crypto-native users.

LemFi, on its own part, gains access to Tether’s deep USDT liquidity pool and the technical backing to build a settlement layer on blockchain. The company described its customer base as consisting of “millions of people who live and work across borders,” many of whom, it said, have historically been underserved by traditional financial institutions.

A third-party provider failure caused Revolut’s app to show wildly inaccurate crypto prices on Friday, the company confirmed, after users flooded social media with screenshots of Bitcoin listed at just 2 cents.

Third-Party Provider Blamed For Pricing Chaos

Revolut acknowledged the problem in a public statement, saying engineers were working on a fix and urging customers to check its status page for updates.

Hi. We want to help resolve the issues you’re facing with the Bitcoin price notification. We’re currently experiencing issues affecting some of the app’s functionalities. Please be assured that our colleagues are working on this as we speak. Please keep an eye on our status page…

The glitch wasn’t limited to Bitcoin. Users reported seeing simultaneous price drops across XRP, Solana, and even stablecoins like USDT and USDC — assets designed to hold steady at one dollar.

Screenshots shared on X and Reddit showed Bitcoin’s 24-hour chart registering a roughly 50% intraday plunge, with the price briefly anchoring near $39,900 before snapping back.

Some users also received push notifications warning that BTC had hit a 52-week low of 2 cents.

According to Revolut, The price of Bitcoin has just dropped to $0.02

Pricing data on major aggregators showed nothing unusual during the same window. Bitcoin’s price on CoinMarketCap and CoinGecko held steady, with no sign of any crash in derivatives markets either. The anomaly appeared entirely contained within Revolut’s app.

Ranveer Arora, a former PwC quantitative trading lead and co-founder of Altura.trade, told reporters two explanations are in play.

The first is a corrupt data tick pushed through Revolut’s pricing system — a single bad data point that briefly anchored the chart before being corrected.

Because Revolut is not an exchange and pulls prices from outside providers, one faulty input can be enough to produce exactly this kind of chart distortion.

The second possibility is a transient liquidity gap. Revolut’s order book is shallower than what you’d find on a full exchange, so a large sell order could theoretically exhaust available bids and print a sharp downward wick before prices recover.

Arora noted, however, that the lack of matching prints on any other platform makes the data feed explanation more likely.

Why Retail Apps Face Unique Data Risks

Marc Tillement, director of blockchain price oracle Pyth Data Association, said the episode shows how quickly a single bad data point can distort price perception — particularly in retail-facing systems where users may not think to cross-check what they’re seeing.

Tillement said that as markets grow more data-dependent, the reliability of pricing infrastructure becomes central to how much traders can trust what’s in front of them.

Transparent, verifiable data layers, he argued, are what separate a glitch from a crisis.

Featured image from Pixabay, chart from TradingView

FROZEN — Tether’s $344M USDT Lockdown | Crypto Coin Show

Sanctions Enforcement · Stablecoins · Iran

Frozen $344 Million in USDT Locked on Tron

In one of the largest single compliance actions in crypto history, Tether moved to freeze

$344 million worth of USDT across two Tron blockchain wallets at the request of U.S. authorities — wallets now linked by U.S. officials to the Iranian regime.

Crypto Coin Show Editorial Desk|April 24, 2026|Exclusive Analysis

$344M

Total USDT Frozen

2 Wallets

Blacklisted on Tron

$4.4B+

Total Tether Freezes to Date

340+

Global Agency Partners

A Landmark Freeze — and an Iran Connection

On Thursday, April 23, 2026, Tether — the issuer of the world’s largest stablecoin by volume — announced it had frozen $344 million in USDT across two blockchain addresses on the Tron network. The action was carried out in coordination with the U.S. Office of Foreign Assets Control (OFAC) and multiple federal law enforcement agencies, following intelligence that the wallets were tied to illicit financial activity.

Within 24 hours, the story grew considerably larger. U.S. officials told CNN on Friday that the frozen funds carried material links to the Iranian regime, including transaction trails running through Iranian exchanges and intermediary wallets connected to accounts associated with Iran’s Central Bank. Treasury Secretary Scott Bessent confirmed the sanctions action, framing it as part of a broader Trump administration campaign to cut off Tehran’s financial lifelines as nuclear diplomacy stalls.

USDT is not a safe haven for illicit activity. When credible links to sanctioned entities or criminal networks are identified, we act immediately and decisively.

— Paolo Ardoino, CEO, Tether · April 23, 2026

📊 Key Figures

Total USDT Frozen

$344M

Wallet 1 (TNiq9…)

~$213M

Wallet 2 (TTiDL…)

~$131M

Network

Tron (TRC-20)

Coordination

OFAC + FBI

Alleged Nexus

Iran / CBoI

Action Date

Apr 23, 2026

🌐 Tether Compliance Scale

Total Assets Frozen ($4.4B)

U.S.-Linked Cases ($2.1B)

This Action ($344M)

Global Agency Partners

340+

Countries

65

Cases Supported

2,300+

The Two Wallets

Blockchain security firm PeckShield flagged the two addresses after they appeared on Tether’s blacklist on April 23, before any official explanation was given. Together, the wallets held slightly more than $344 million in USDT at the time of the freeze.

🔒 Locked

TNiq9AXBp9EjUqhDhrwrfvAA8U3GUQZH81

~$213M

USDT · Tron Network

🔒 Locked

TTiDLWE6fZK8okMJv6ijg42yrH6W2pjSr9

~$131M

USDT · Tron Network

According to Chainalysis, the two Tron addresses were regularly active years ago — moving tens of millions of dollars in single transfers, often to private wallets. U.S. officials noted the behavior mirrored patterns seen in other known IRGC-linked addresses. The wallets were blacklisted at the smart contract level, meaning no further movement of the funds is possible until cleared by authorities.

⚠ Iran’s Crypto Strategy

According to the U.S. Treasury Department, Iran’s central bank has increasingly leaned into digital assets — particularly stablecoins on the Tron network — to mask cross-border transactions and support trade flows under sanctions pressure. Blockchain analytics firms TRM Labs and Chainalysis estimate that Iran-related crypto flows reached billions of dollars in 2025 alone.

🔍 Context: Tron & Iran

The Tron blockchain has become a preferred rail for sanctions-evasion activity due to its low fees and high USDT liquidity. U.S. authorities have increasingly focused enforcement actions on Tron-based USDT wallets linked to Iranian exchanges, IRGC-associated entities, and intermediary networks routing funds through complicit third-country actors.

How Tether Can Freeze Funds

Unlike decentralized tokens, USDT is a centralized stablecoin — meaning Tether retains the technical ability to freeze or blacklist any wallet at the smart contract level. The company describes this as a feature, not a flaw: public blockchains create a visible transaction trail that investigators can follow in near-real time, something traditional cash networks cannot provide.

When OFAC or a law enforcement partner flags an address, Tether’s compliance team can restrict the wallet within hours — preventing any further transfer of funds. The frozen USDT remains in the address but is effectively inert, unable to be spent, sent, or swapped, until legal proceedings determine its fate.

A Growing Compliance Empire

This action does not exist in isolation. Tether has been systematically expanding its compliance infrastructure over the past several years, and Thursday’s move is a statement of that ambition. The company now reports collaborating with more than 340 law enforcement agencies across 65 countries, having assisted in more than 2,300 investigations globally — over 1,200 of which involve U.S. authorities.

Cumulatively, Tether has now frozen more than $4.4 billion in USDT to date, including $2.1 billion specifically tied to U.S. law enforcement cases. The $344 million freeze on April 23 ranks as one of the single largest compliance actions the company has ever executed.

A Pattern of Major Freezes

November 2023

~$225M frozen — Wallets linked to a Southeast Asia human-trafficking and “pig butchering” scam ring. One of the first major cooperative actions with U.S. DOJ.

January 2026

~$182M frozen — Five Tron wallets restricted in another coordinated action with OFAC. Linked to sanctions evasion networks.

April 2026 (Current)

$344M frozen — Two Tron wallets blacklisted at the request of U.S. authorities. Linked within 24 hours to the Iranian regime and Central Bank of Iran intermediaries. Largest single action to date.

The Stablecoin Compliance Debate

The freeze arrives amid a broader, heated debate about what stablecoin issuers owe the public — and regulators — when it comes to stopping illicit financial flows. The controversy was reignited earlier this month when the Drift Protocol was exploited for $285 million. Critics argued that Circle, the issuer of the competing USDC stablecoin, moved too slowly to freeze funds connected to the exploit.

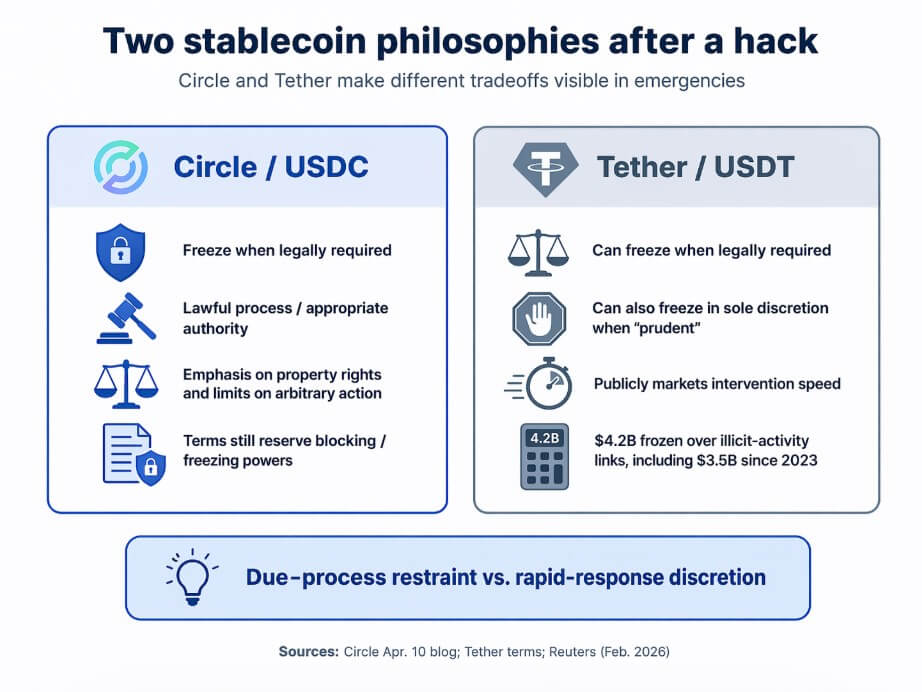

Circle pushed back, with Chief Strategy Officer Dante Disparte stating that the company only freezes funds when the law explicitly requires it or when court orders mandate action — not through unilateral judgment. Tether has taken the opposite stance, positioning itself as a proactive partner to law enforcement even before formal legal orders arrive.

The way to get at Iran at this point — because Iran is truly sanctioned out — is to go with the third-country actors enabling them.

— Daniel Tannebaum, Atlantic Council · Senior Fellow

⚖️ Circle vs. Tether

Tether Freeze Philosophy

Proactive

Circle Stance

Court Order Only

Drift Protocol Fallout

Circle Sued

Drift Adopted

USDT (Tether)

The fallout from Drift was swift: the protocol announced it would dump USDC in favor of USDT, citing Tether’s more assertive compliance posture. A class-action lawsuit against Circle followed. The episode cemented Tether’s narrative as the enforcement-friendly stablecoin — and its April 23 action is a deliberate reinforcement of that brand.

Geopolitical Dimensions

The Iran link elevates this story beyond a routine compliance action. Treasury Secretary Scott Bessent confirmed the sanctions in a statement framing it as part of the Trump administration’s escalating economic campaign against Tehran — describing Washington’s intent to “follow the money” as diplomatic efforts around the conflict stall.

Iran has spent years developing techniques to route funds through third-country actors, shell companies, and now increasingly through decentralized blockchain infrastructure. Earlier in 2026, both Tether and Circle were involved in blacklisting a hot wallet belonging to Iranian exchange Wallex, while U.S. authorities sanctioned additional platforms accused of routing IRGC funds through USDT on the Tron network.

Some analysts caution against overstating the impact. Experts note that Iran has decades of experience adapting to economic pressure, and that the more consequential choke point may be the third-country jurisdictions — particularly China — that continue to enable Iranian trade flows. Still, the ability to surgically freeze $344 million in a matter of hours marks a significant expansion of the U.S. sanctions toolkit into the digital asset space.

What Comes Next

Tether has confirmed it is expanding further into the U.S. domestic market. The company recently launched USAT — a new stablecoin token built for compliance with emerging federal stablecoin regulation — in partnership with federally regulated crypto bank Anchorage Digital. The initiative is led by former White House crypto advisor Bo Hines.

Regulators and lawmakers are watching closely. With stablecoin legislation advancing on Capitol Hill, the question of whether issuers like Tether should be required — rather than just permitted — to freeze funds linked to sanctions is becoming a central policy debate. For now, Tether is volunteering. And with $344 million locked on Tron, Washington appears to appreciate the help.

Crypto rhetoric has long prized the ability to transact without gatekeepers, to move value across borders without asking permission, and to hold assets no institution could seize.

Crypto culture treated these as design virtues, properties that builders embedded with ethical weight by deliberate architectural choice. Then the Drift exploit happened, and the backlash told a different story.

On Apr. 1, Drift suffered a major exploit. Circle later described the publicly reported losses as exceeding $270 million, while other reports put the figure around $285 million and documented criticism that Circle had not frozen stolen USDC as it moved across its cross-chain rails.

The attacker routed roughly $232 million in USDC from Solana to Ethereum using Circle’s Cross-Chain Transfer Protocol. The backlash stemmed from users and observers wanting to know why Circle had not intervened sooner.

Days later, Tether CEO Paolo Ardoino posted that Tether had frozen 3.29 million USDT tied to the Rhea Finance attacker, framing the intervention as proof that “Tether cares.”

Circle published its formal response on Apr. 10, and its core argument was that USDC freezes occur when the law requires action. Circle is legally compelled by an appropriate authority through a lawful process.

Circle pushed back on the idea that an issuer should act as an ad hoc chain police force, arguing that open access to permissionless infrastructure is a feature, and that the bigger problem is that legal frameworks have not yet kept pace with the speed of on-chain exploits.

The stablecoin issuer also made a property-rights argument, claiming that arbitrary freezes set dangerous precedents for lawful users, and the power to freeze is a compliance obligation, constrained by lawful process and legal compulsion, authorized only through formal legal channels.

The complication is that Circle’s own legal documents tell a more layered story.

USDC terms state that transfers are irreversible and that Circle carries no obligation to track or determine the provenance of balances.

Those same terms also reserve Circle’s right to block certain addresses and, for Circle-custodied balances, freeze associated USDC in its sole discretion when it believes those addresses may be tied to illegal activity or terms violations.

Circle holds meaningful freeze power and frames it as a tightly bound compliance function, constrained by legal process and compulsion.

Ardoino’s Rhea post was a boast, and Tether’s terms grant it broad discretion by stating that the company may freeze tokens as required by law or whenever it determines, in its sole discretion, that doing so is prudent, and authorizing it to blacklist token addresses.

In February, Tether froze approximately $4.2 billion in USDT due to links to illicit activity, with $3.5 billion of that since 2023.

Circle freezes USDC only when legally compelled, while Tether reserves sole discretion to freeze and has frozen $4.2 billion over illicit-activity links.

The feature nobody advertised

What Drift and Rhea forced into the open is a question that stablecoin competition had not yet fully surfaced: in a hack, what do users actually want from an issuer?

The anti-censorship instincts that shaped crypto’s early culture tend to lose their force the moment users need an emergency brake. Affected protocols, exchanges holding stolen funds, and victims watching their balances drain want to know who can stop the thief.

That reframes freeze capacity as more of a consumer-protection feature.

Tether has been accumulating a record of intervention and visibility. Ardoino’s Rhea post was designed to be read as a product statement, and in the context of a fresh exploit, it worked.

The emotional and practical logic is accessible, showing that one issuer froze stolen funds the same day an attacker moved them, while another issuer said legal timelines tied its hands.

This makes optics difficult for Circle regardless of the legal merits of its position.

Stablecoins are quietly differentiating themselves in emergency governance, alongside reserve composition and exchange liquidity.

The cost of the feature

The case for Circle’s position is real and does not require dismissing the Drift backlash to hold. Broad issuer discretion over freezes creates risks that extend far beyond hack scenarios.

An issuer that can freeze tokens in its sole discretion when it determines it is prudent can freeze tokens for reasons unrelated to protecting victims. Politically contentious addresses, disputed transactions, regulatory scrutiny from a single jurisdiction, or simple operational error can all trigger freezes under terms as broad as Tether’s.

The same capacity that lets an issuer stop a thief also lets it stop a protester, a dissident from a sanctioned country, or a business whose activity it finds inconvenient.

Circle’s public writing on the Drift exploit is, among other things, a defense against that risk. The argument that emergency intervention needs new legal frameworks and safe-harbor structures is also an argument that the current situation is a problem, even when the targets are criminals.

The absence of defined standards means an issuer can act generously today and overreach tomorrow, with no formal mechanism to distinguish the two.

Tether’s freeze record has not yet produced a major documented wrongful-freeze controversy, but that record is also vast and not fully transparent.

Reports on the $4.2 billion in frozen USDT withhold the details of each decision, the legal process underlying each freeze, and the error rate across thousands of enforcement actions.

Fast intervention looks different in the abstract when the process generating those interventions is opaque.

Benefit of fast freezes

Cost of broad freeze discretion

Can slow or stop stolen funds

Can enable arbitrary intervention

May improve recovery odds

Can affect lawful users

Helps exchanges/protocols in crises

Can reflect political or regulatory pressure

Looks like consumer protection in hacks

Process may be opaque

Becomes a due-diligence feature

Wrongful-freeze risk may be hard to challenge

Two paths from here

The bull case for intervention-first issuers runs in a world where hacks keep coming, and recoverability keeps rising on the priority list.

More regulatory scrutiny on exchanges to show they take asset protection seriously, and more institutional users who need to demonstrate due diligence in custody and recovery. These are factors that push emergency freeze capacity to the center of stablecoin evaluation.

In that scenario, Tether’s public freeze record and broad discretionary terms become genuine competitive assets. Exchanges and protocols that have experienced exploits now treat fast-intervention capacity as a due diligence criterion when choosing which stablecoin to hold as primary liquidity.

Circle has to either act faster through new legal mechanisms or accept that some market segments will treat its rule-of-law posture as a liability in crises. Ardoino’s Rhea post, in retrospect, looks like an early entry in a competition that the market eventually formalizes.

The bear case for that same model runs through wrongful freezes, regulatory backlash, and the discovery that broad discretion is often a liability as much as a virtue.

A high-profile incorrect freeze, such as an address flagged as malicious that belongs to a legitimate user, a jurisdiction-specific enforcement action that appears to be politically targeted at users in other markets, or an operational error that freezes clean funds during a market stress event, turns the same emergency-governance story toxic.

In that world, Circle’s insistence on lawful process and defined standards looks like principled restraint, a deliberate commitment to defined limits over speed, and users place a real premium on an issuer whose freeze decisions carry formal accountability.

The crypto community’s historical skepticism toward centralized control reasserts itself as hard-won practical wisdom, grounded in the documented costs of unchecked issuer discretion.

The stablecoin winners in that scenario are the ones whose intervention power is real but bounded. Issuers who can act in genuine emergencies and demonstrate they held back in ambiguous ones.

Stablecoin governance splits between intervention-first issuers gaining crisis goodwill and bounded-discretion issuers winning users who reprice centralization risk, per Circle and Tether materials.

As stablecoins deepen their role in institutional payments, treasury workflows, and regulated financial infrastructure, governance under stress becomes as material as reserve quality or distribution reach.

The question that Drift and Rhea put on the table of how much control users want an issuer to have has no clean universal answer. Institutions with large exposures and recovery obligations may want emergency brakes, while individuals holding stablecoins across politically sensitive jurisdictions may want the opposite.

Protocols with mixed user bases need to answer for both.

The real contest now is for the version of stablecoin governance that earns enough trust from enough users to become the default.

Stablecoin tax treatment in the U.S. is at the center of a new legislative push to exempt qualifying daily transactions involving regulated payment stablecoins from tax.

The latest version of the PARITY Act would stop gain or loss recognition on certain stablecoin sales unless a taxpayer’s basis falls below 99% of the token’s redemption value, marking a direct attempt to treat routine stablecoin spending more like cash payments. The proposal also revises rules on staking rewards and digital asset wash sales, while lawmakers in Washington continue to debate broader crypto legislation.

Stablecoin payments provision removes small transaction tax burden

The bill is grounded on the past discussion drafts issued in December 2025 and on March 26, 2026. The earlier proposal recommended a $200 limit on payments made with regulated payment stablecoins, as in the de minimis section.

That structure was altered in the March 2026 draft. Instead of using a de minimis criterion, the text states that no gain or loss would be recognized on the sale of a regulated payment stablecoin unless the taxpayer’s basis in that stablecoin is less than 99% of its redemption value.

Another standard eliminated by the draft was the previous $200 standard. In addition, it created a deemed basis of $1 for exchanges, which the text treats separately from the stablecoin’s sales. That development solves one of the long-term problems of crypto users. The current tax treatment states that any payment made using USDC or USDT can result in a taxable event, even when the change in value is minimal.

Meanwhile, the bill creates a distinction between passive staking and other activities, such as trading. It would also enable taxpayers to decide when to record staking rewards, upon receipt or after a deferral period of not more than 5 years, as indicated in the material. To qualify under the proposed stablecoin treatment, the asset must be regulated under the GENIUS Act and remain within 1% of its $1 peg.

Stablecoin debate comes alongside ongoing crypto policy pressure

The tax proposal comes following pressure on other digital asset legislation, including the CLARITY Act. Senator Cynthia Lummis recently pointed out that the bill could remain stalled until 2030 if the Senate fails to act before the 2026 election cycle.

At the same time, as reported by Cryptopolitan, the Trump White House has pushed back on concerns over stablecoin yield provisions. A Council of Economic Advisors report dated April 8 said the effect on bank lending would be limited, estimating a 0.02% increase, or about $2.1 billion.

The same report said community banks would face about $500 million in additional obligations, equal to a 0.026% increase over current lending activity. It concluded that banning yield would provide little protection for bank lending while giving up consumer benefits tied to competitive returns on stablecoin holdings.

Your bank is using your money. You’re getting the scraps. Watch our free video on becoming your own bank