Crypto exchange balances saw a notable withdrawal wave heading into July 1, with USDC and Bitcoin leading approximately $850 million in net outflows from centralized platforms. The move adds another layer to a market already watching liquidity, ETF flows, and investor positioning closely.

TL;DR

Centralized exchanges reportedly saw around $850 million in net withdrawals over 24 hours.

USDC led stablecoin outflows with about $503 million leaving exchanges.

Bitcoin recorded around $352.7 million in net withdrawals over the same period.

Exchange outflows are wallet movements, not direct evidence of spot buying or selling.

Exchange flows are useful because they show where traders are moving assets, but they need careful interpretation. A withdrawal does not tell us exactly what the owner plans to do next. It may reflect self-custody, institutional settlement, collateral movement, treasury management, or DeFi deployment.

USDC leads the stablecoin move

The largest reported component of the outflow was USDC, with roughly $503 million leaving centralized exchanges. Stablecoin withdrawals can mean several things. Sometimes traders are moving dollars on-chain to use in DeFi. Sometimes market makers are shifting liquidity between venues. Sometimes funds are simply being pulled into custody after a trading period ends.

Because USDC is widely used as a settlement asset, its movement can offer clues about where liquidity may appear next. If stablecoins leave exchanges and move into wallets or protocols, that may support on-chain activity. If they move into custody and stay idle, the signal is more defensive.

Bitcoin withdrawals add a second signal

Bitcoin also saw significant reported withdrawals, with around $352.7 million in net outflows during the same 24-hour window. BTC leaving exchanges is often interpreted as a sign of holding conviction because coins moved into self-custody are usually less immediately available for sale.

That reading is useful, but it should not be pushed too far. Large holders can move coins between wallets for operational reasons. Institutions can rebalance custody arrangements. Traders can withdraw funds without making a long-term investment statement. The signal is strongest when exchange outflows persist across several days and align with improving price action.

A market looking for cleaner signals

The latest outflow wave comes as Bitcoin and the wider crypto market are searching for direction after a difficult June. Spot ETF flows have weakened, US demand indicators remain mixed, and traders are watching liquidity closely. In that environment, exchange reserve data can help show whether investors are preparing to sell or moving assets away from trading venues.

For now, the takeaway is balanced. USDC and Bitcoin withdrawals suggest capital is moving off centralized exchanges, which can be constructive if it reflects custody confidence or on-chain deployment. But the data does not prove immediate buying pressure. It is one piece of the market puzzle, and it becomes more meaningful if the trend continues through the next several sessions.

For readers, the cleanest takeaway is to separate the raw data from the market interpretation. The figures are useful because they show how capital is moving, but they should still be read alongside price action, liquidity conditions, and the wider risk environment.

This report is based on information from CryptoQuant.

This article was written by the News Desk and edited by Samuel Rae.

The Bank for International Settlements (BIS) has reported its assessment of stablecoins based on specific variables, and has concluded that they do not function as money was originally intended. The institution has warned in its latest 2026 Annual Economic Report that dollar-pegged tokens are driving a new form of dollarization in emerging economies.

The report was based on an assessment using multiple criteria for money, and made a distinct comparison of stablecoins to ETFs.

BIS report on stablecoins

The umbrella institution for central banks evaluated stablecoins on four criteria considered essential for entities described as money. These criteria include singleness, elasticity, interoperability, and integrity. Stablecoins were said to have failed all four, according to the report.

Singleness translates to the concept of one unit always being equal to one unit of the underlying currency regardless of the issuer. Stablecoin prices on secondary markets tend to drift from their $1 peg, sometimes just slightly.

Elasticity requires the supply of any entity seen as money to increase and decrease with economic demand. Stablecoins use a model where issuers mint tokens only after receiving equivalent cash deposits, which prevents this flexible expansion according to demand from happening.

The BIS compared stablecoins to ETFs, stating that stablecoins behave more like shares in an exchange-traded fund instead of cash deposits.

Dollar dominance has increased globally

Over 99% of the roughly $320 billion stablecoin market, as of the end of May 2026, is denominated in US dollars. Tether’s USDT and Circle’s USDC account for most of that figure. A separate BIS research paper from May 5 estimated dollar dominance in stablecoin value at approximately 98%.

The report states that this concentration is a structural problem for emerging markets and developing economies. The BIS calls this “stablecoin dollarization” and warns it mirrors the historical pattern of deposit dollarization, where savings are shifted into foreign bank accounts during crises, happening at a faster pace since crypto operates outside traditional banking infrastructure.

Countries including Turkey, Argentina, and Nigeria have already had a lot of stablecoin adoption as citizens seek dollar exposure outside formal channels.

Several emerging economies have imposed restrictions on cross-border stablecoin use. The BIS has expressed skepticism on how well these restrictions can hold, since controls that function against traditional bank deposits do not translate well to self-custodial crypto tokens.

Potential negative economic effects of stablecoins

The BIS created a model exploring possible happenings if the stablecoin market cap grew to between $1 trillion and $3 trillion, and concluded that the net effect on economic output would still be “modestly negative.”

As deposits migrate from traditional banks to stablecoin issuers (who park reserves in US Treasuries and money market instruments), banks continue to lose a cheap funding source. To compete, they would need to raise deposit rates, which would increase lending costs, and slow economic activity.

The BIS has recommended building what it calls a “unified ledger” for central bank monies, aiming to combine tokenized central bank reserves with commercial bank money on a shared infrastructure. The report cited Project Agora, a cross-border payments prototype, as evidence that this “unified” approach is technically feasible, according to Binance News.

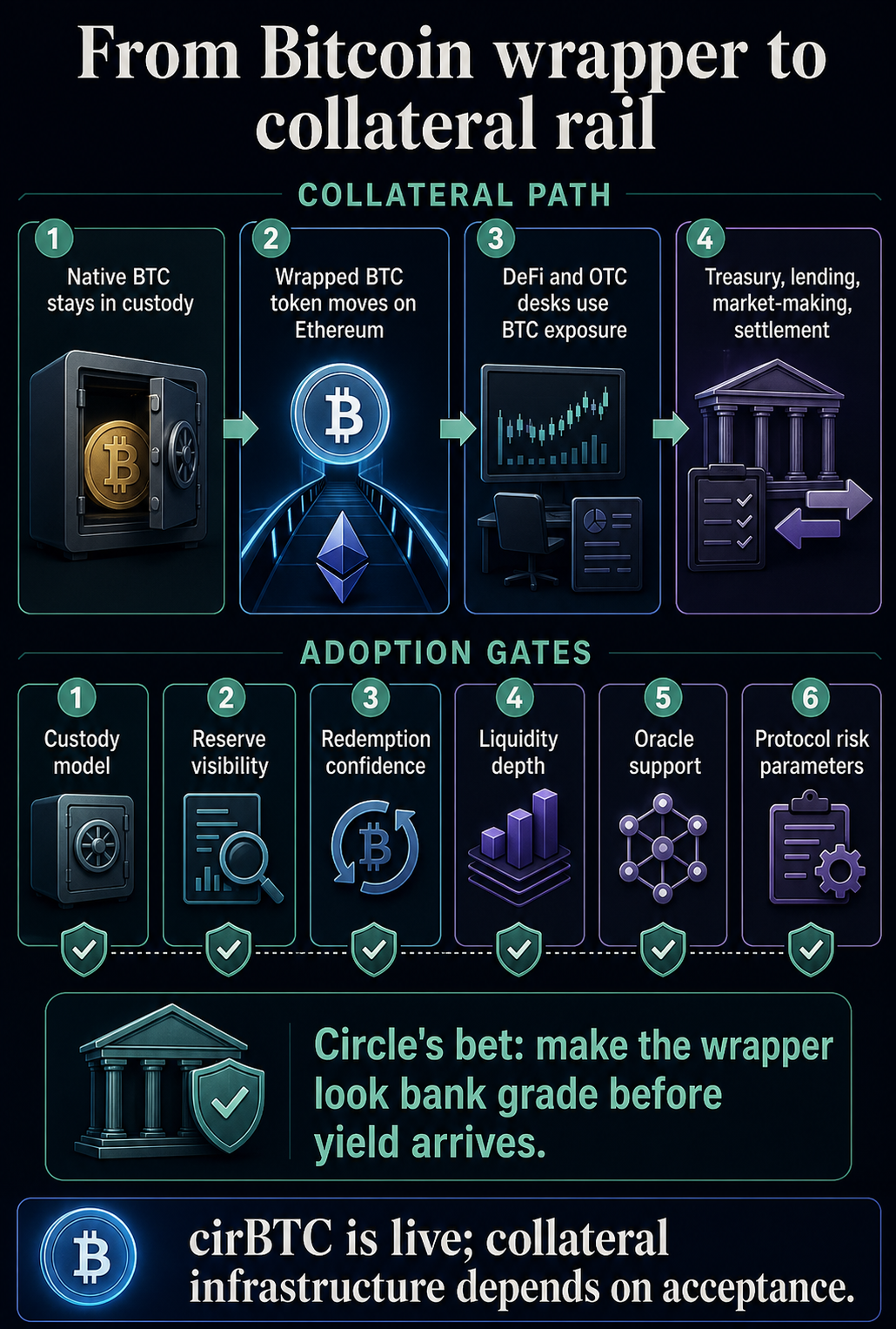

Circle has launched cirBTC on Ethereum, but the larger play is to make wrapped Bitcoin look like collateral infrastructure institutions can route through DeFi, OTC desks, lending markets, treasury systems, market makers, and settlement flows.

cirBTC is live on Ethereum and backed 1:1 by native BTC, according to Circle’s launch materials. The company says the underlying Bitcoin is held through a Circle entity, segregated from corporate assets, and designed for onchain reserve visibility.

The product also sits inside Circle’s existing stack. Circle is positioning cirBTC around Circle Mint, USDC workflows, Ethereum DeFi, and planned support for Arc and other chains.

This moves wrapped Bitcoin into an issue of trust. BTC itself does not move natively through Ethereum contracts, so any wrapped version asks users to trust a claim on Bitcoin held somewhere else.

For retail DeFi users, that can be a bridge decision. For institutions, it is a collateral decision: who holds the keys, how reserves are checked, what happens during redemption, and whether the operational process can survive internal risk review.

Circle is selling custody before yield

Circle’s cirBTC pitch starts with the same basic promise as other wrapped Bitcoin products: one token for one BTC. The difference is the operating package around that promise.

Its materials say cirBTC is backed by native BTC, reserves are separated from corporate assets, and counterparties can verify reserves onchain. Circle also ties the product to the same institutional interface many firms already use for USDC issuance and redemption.

A desk that already moves USDC through Circle Mint could, in theory, add BTC collateral to the same account-and-settlement relationship instead of stitching together a separate custodian, wrapper, exchange, bridge, and DeFi access point.

The proof-of-reserve component supports that positioning. Proof of Reserve systems can help tokenized assets and DeFi protocols monitor backing data onchain and build safeguards around undercollateralization.

For cirBTC, the next live signal is the reserve feed or dashboard counterparties can use for the token itself.

That leaves counterparty trust in place. cirBTC still depends on custody, redemption, reserve controls, and user confidence in Circle’s process.

The institutional pitch is that those assumptions can be packaged in a cleaner way, with the BTC claim, reserve visibility, and Circle account relationship pointing in the same direction.

The comparison is clearest against cbBTC and WBTC.

Coinbase’s cbBTC is also a 1:1 BTC-backed wrapped asset, held in Coinbase custody and available across Base, Ethereum, Solana, and Arbitrum.

Coinbase also maintains a proof-of-reserves page, giving users a public reserve and supply reference for the product. Availability and terms can vary by jurisdiction.

WBTC remains the incumbent Bitcoin wrapper in Ethereum DeFi. Its own site presents WBTC as backed 1:1 by Bitcoin, with a public reserve dashboard and proof-of-reserve context.

Circle’s opportunity sits in the trust bundle it can offer: the USDC issuer, Circle Mint, reserve transparency, Ethereum access, and future Arc support under one institutional brand.

Product

Main trust promise

What is known now

Open test

cirBTC

Circle-backed BTC collateral for institutional workflows

Live on Ethereum, backed 1:1 by native BTC, with Circle stating reserve segregation and onchain visibility

Whether liquidity, protocol listings, and reserve feeds make it usable as collateral at scale

cbBTC

Coinbase custody and exchange-account workflows

Backed 1:1 by BTC held by Coinbase, with listed support across Base, Ethereum, Solana, and Arbitrum

Whether Circle can compete with Coinbase distribution and Base-native lending activity

WBTC

Incumbent DeFi collateral with public reserves

Backed 1:1 by BTC with a public reserve dashboard and proof-of-reserve context

Whether institutions prefer an incumbent DeFi asset or a Circle-controlled operating model

The comparison shows why cirBTC is more than a token launch. Wrapped Bitcoin products increasingly compete on the legal and operational identity of the issuer, the visibility of reserves, and the pathways by which collateral enters lending markets.

Coinbase has already tied cbBTC to lending through Base. CryptoSlate reported that Coinbase and Morpho introduced Bitcoin-backed loans on Base, using cbBTC and USDC in a consumer-facing borrowing flow.

That comparison shows the distribution Circle has to challenge if cirBTC is to become more than another Ethereum asset.

Circle’s Arc ambitions give cirBTC a second layer of meaning.

Arc is being pitched as infrastructure for stablecoin finance, with USDC fees, settlement tooling, privacy controls, and institutional use cases around payments, foreign exchange, tokenized assets, and capital markets.

Circle has described Arc as a chain purpose-built for stablecoin finance, and CryptoSlate has previously reported how the network pushes Circle deeper into territory also occupied by Coinbase and Base.

In that context, cirBTC could become the Bitcoin leg of a broader Circle stack. USDC provides the dollar asset. Circle Mint provides issuance and redemption access. Ethereum provides current DeFi reach.

Arc, if it develops as planned, could give Circle a venue where tokenized dollars, BTC collateral, and settlement workflows operate with fewer handoffs.

The record remains early. Circle says cirBTC is live on Ethereum and points to planned Arc and multichain support. Its launch materials stop short of showing broad DeFi protocol adoption, live Arc usage for cirBTC, or a supply figure that would show market depth.

A token can be fully backed and still fail to become preferred collateral.

Institutions and DeFi protocols still need liquidity, risk parameters, redemption confidence, oracle support, and a clear reason to add another BTC wrapper beside existing options.

The broader market context is already moving in that direction. CryptoSlate recently framed a Morgan Stanley and Galaxy arrangement as part of Bitcoin’s next institutional test in lending collateral.

The cirBTC launch fits that same issue: Bitcoin can become useful collateral for institutions when the custody and risk controls around the token are strong enough to satisfy the people managing the real BTC.

Arc also gives the Coinbase comparison more weight. Coinbase can route cbBTC through Base and its own account system; Circle is trying to offer a parallel route built around USDC, Mint, and Arc.

The adoption contest centers on which issuer can turn custody relationships into liquidity.

Acceptance decides whether the wrapper becomes infrastructure

Circle has the right ingredients for a bank-grade wrapper: a known issuer, reserve language, onchain verification, institutional access, USDC proximity, and an Arc roadmap.

Collateral infrastructure comes later, when counterparties use those ingredients in production.

That means lenders need to accept the asset, market makers need to quote it, treasury teams need clean redemption, DeFi protocols need collateral parameters, and risk desks need confidence in the reserve process.

Users also need to move between BTC exposure and dollar liquidity without wondering where the real Bitcoin sits.

That is where cirBTC will face WBTC and cbBTC. WBTC has incumbent DeFi familiarity. Coinbase has distribution, custody, and Base workflows.

Circle has USDC, Mint, compliance credibility, and an ambition to own more of the settlement stack through Arc.

Circle can turn wrapped Bitcoin into institutional collateral infrastructure if cirBTC becomes the wrapper institutions choose because the custody, reserve, and redemption model lowers operational friction.

If liquidity stays elsewhere and Arc remains future context, cirBTC will still read as a product launch rather than infrastructure.

For now, Circle has changed the frame around wrapped BTC. The debate now centers on who institutions trust to hold the Bitcoin while the token moves through programmable finance.

Tether has applied for seven trademarks in South Korea, including for its company name and logo, in a move that market observers see as a hint of the firm expanding into the South Korean market.

The issuer of the largest stablecoin in the world, USDT, is also expanding its reach into Africa and Asia by partnering with Lemfi. Meanwhile, Tether’s rival Circle (NYSE: CRCL) has already been meeting with major financial institutions in South Korea, setting up a potential showdown between number one and two in the stablecoin issuance business.

Tether and Circle are lining up entry into the South Korean market

Tether, the company behind the world’s largest stablecoin USDT, is making progress in its plans to enter the South Korean market. The Korea Intellectual Property Rights Information Service (KIPRIS) recently received multiple trademark applications from Tether, totaling up to seven.

Tether’s previous filings in the country focused on stablecoin product names, but this batch includes the corporate brand itself and its gold-backed stablecoin Tether Gold (XAUT).

South Korea’s proposed Digital Asset Basic Act is expected to require foreign stablecoin issuers to maintain a domestic branch if they want to distribute their tokens locally, and Tether appears to be positioning itself ahead.

Before Tether’s latest filings, Circle’s CEO Jeremy Allaire visited Seoul in April and met with executives from KB Financial Group, Shinhan Financial Group, and Hana Financial Group to discuss stablecoin payment cooperation and real-world asset tokenization.

Allaire acknowledged the potential in the South Korean market and shared Circle’s plans to establish a Korean subsidiary and obtain a license if the final regulatory framework accepts foreign issuers.

Circle has also signed partnerships with Korean exchanges Dunamu, which operates Upbit, and Bithumb to expand USDC adoption on domestic trading platforms.

Cryptopolitan reported earlier that Hana Card, part of Hana Financial Group, launched a pilot in March allowing foreign visitors to pay at local merchants using USDC through a partnership with Circle and Crypto.com. Other Korean financial firms, including BC Card and KB Kookmin Card, have been testing stablecoin payment infrastructure as well.

Tether has been on an expansion trail

Tether also recently announced an investment in LemFi, a cross-border payments platform that works across communities in the UK, US, Canada, and Europe to recipients in Africa and Asia. The deal will integrate USDT as a settlement layer across LemFi’s payment corridors, replacing multi-day SWIFT-based transfers with blockchain settlement.

Tether’s CEO Paolo Ardoino said in the announcement that the goal of the partnership is to expand financial access for its estimated 585 million users globally.

Cryptopolitan previously reported that Tether recorded $1.04 billion in profit for Q1 2026. The company holds excess reserves of $8.23 billion; enough capital to invest in distribution partners and pursue market entry in jurisdictions like South Korea.

South Korea is home to an estimated 18 million crypto investors. Exchanges in the country recorded over $663 billion in trades through mid-2025, and the country’s retail traders remain a significant part of altcoin markets.

Beyond Tether and Circle, multiple projects are building won-denominated stablecoins. Cryptopolitan reported that the Bank of Korea has been advancing “Project Han River,” its wholesale CBDC initiative, which entered a second phase of real-transaction testing earlier this year.

Regulators are still debating whether or not stablecoin issuance should be restricted to commercial banks or follow a more flexible licensing model. The discussion has been postponed until after South Korea’s June local elections.

Best Autonomous Agentic Payments Platform is a category within the BeInCrypto Institutional 100, an annual research-driven program recognising institutional digital asset excellence across 26 categories and six pillars.

This category sits under Pillar 4: Tokenization & On-Chain Finance. The 10 firms below are listed alphabetically and are not ranked. A shortlist will be named in May 2026, with the winner announced at Proof of Talk in Paris on June 2–3, 2026.

Key Facts

Long list: 10 firms across stablecoin agent stacks, x402 protocol ecosystems, full-stack agent payment platforms, agent identity standards, settlement layers, agentic onramps, and network-level payment rails

Initial pool: More than 30 firms screened; 10 advanced to the primary long list

Order: Listed alphabetically, not ranked

Scoring: 30% quantitative data · 50% Expert Council · 20% disclosed company data

Criteria assessed: Agentic transaction volume, agent integration depth, programmability, developer adoption, security and compliance, funding and viability, innovation signal

Eligibility: Each firm must have a verifiable AI-agentic product, program, fund, standard, or pilot live or announced during the award window

Firm

HQ

Agentic Platform / Sub-Segment

Reach

Representative Work

Ant Digital Technologies

Hangzhou, China

Agent-to-agent economy infrastructure platform

Anvita platform: Anvita TaaS and Anvita Flow

Supports x402 payments, Agent Store modules, OpenClaw, and Claude Code

Anvita launched Mar 31, 2026 at Real Up Cannes

USDC integration with Circle in progress; stablecoin licences pending in Hong Kong, Singapore, and Luxembourg

Circle Internet Group

New York, USA

Stablecoin issuer Agent Stack on USDC rails

USDC settles 99.8% of x402 agentic payments

Live on 11 EVM chains; Agent Marketplace launched with 500+ endpoints

Circle Agent Stack launched May 11, 2026

Includes CLI, Agent Wallets, Marketplace, Nanopayments, and Circle Skills

Coinbase

San Francisco, USA

x402 protocol layer and AgentKit developer ecosystem

About 69,000 active AI agents on x402

167M+ transactions and $50M volume as of Apr 21, 2026

x402 V2 launched Dec 2025 under Linux Foundation umbrella

Selected protocol layer for Amazon Bedrock AgentCore Payments

Crossmint

New York, USA

Full-stack agent payment platform

About $23.6M raised

40,000+ companies and developers; live across 40+ blockchains

Smart contract wallets across EVM, Solana, and Stellar

Virtual Visa and Mastercard cards for agents with spending caps

Ethereum Foundation (dAI Team)

Zug, Switzerland

Standards body for AI agent on-chain identity

Dedicated AI initiative launched Sept 15, 2025

Two-track mandate: AI Economy on Ethereum and Decentralized AI Stack

ERC-8004 finalized at Devconnect Buenos Aires

Creates on-chain identity and reputation layer for AI agents

Mesh

San Francisco, USA

Settlement layer for agentic commerce

$75M round in Jan 2026 at $1B valuation

400M users via partners across 100+ countries

Integrates Google AP2 for natural-language agent purchases

Visa Intelligent Commerce Connect launch pilot partner

MoonPay

Miami, USA

Agentic onramp and card-rail spending product

30M+ customers across 180 countries

NYDFS Trust Charter, BitLicense, and MiCA Netherlands registration

MoonAgents Card launched May 1, 2026

MoonPay Agents launched Feb 2026 with non-custodial AI wallets

Skyfire

San Francisco, USA

Agent identity and payment protocol

$9.5M raised

Customers include Anthropic, Cohere, Replicate, and Hugging Face

KYAPay built for verifiable agent identity and USDC settlement

F5 Networks partnership for enterprise agentic commerce

Solana Foundation

Zug, Switzerland

Network-level agentic payments rail

$650B stablecoin volume in Feb 2026

15M+ on-chain agent payments cleared to date

Pay.sh launched May 5, 2026 with Google Cloud

Solana Agent Kit provides 60+ pre-built actions

TRON DAO

Geneva, Switzerland

Sovereign agentic AI fund and payment rail

977M transactions in Q1 2026

$86B stablecoin supply and $26B TVL

AI Fund expanded from $100M to $1B in Mar 2026

B.AI launched on TRON with 8004 identity and x402 standard support

About This List

The BeInCrypto Institutional 100 — Autonomous Agentic Payments (2026 Long List) identifies firms that enable AI agents to hold assets, access wallets, sign transactions, and settle payments on crypto rails with minimal human intervention.

Coverage spans network-level rails, stablecoin issuer agent platforms, full-stack payment platforms, settlement layers, agent identity protocols, and agentic onramp or card-rail products. Pure AI agent frameworks without a dedicated payment module are out of scope.

Methodology

This category is evaluated under Track B of the BeInCrypto Institutional 100 methodology: 30% quantitative metrics, 50% Expert Council scoring, and 20% disclosed company data.

Assessment spans seven criteria: transaction volume on agentic rails, integration depth across AI frameworks, wallet programmability and policy controls, developer adoption, security and compliance, funding and viability, and innovation during the award window.

The higher Expert Council weighting reflects the early stage of the agentic payments category, where on-chain data exists for some platforms but many launches remain too recent for traditional financial metrics to capture their market importance.

Data was verified using regulatory registers, audited filings, on-chain analytics, x402 Foundation metrics, public company earnings transcripts, partnership announcements, and direct company disclosures.

Circle’s $222 million ARC token presale has given Wall Street a new way to value the USDC issuer, while raising a harder question for one of crypto’s most profitable alliances.

On May 11, Circle said investors led by a16z Crypto backed the presale of ARC, the native token for Arc, its planned public blockchain for institutional finance.

The sale valued the network at $3 billion on a fully diluted basis and came alongside first-quarter results that showed $694 million in total revenue and reserve income, up 20% from a year earlier.

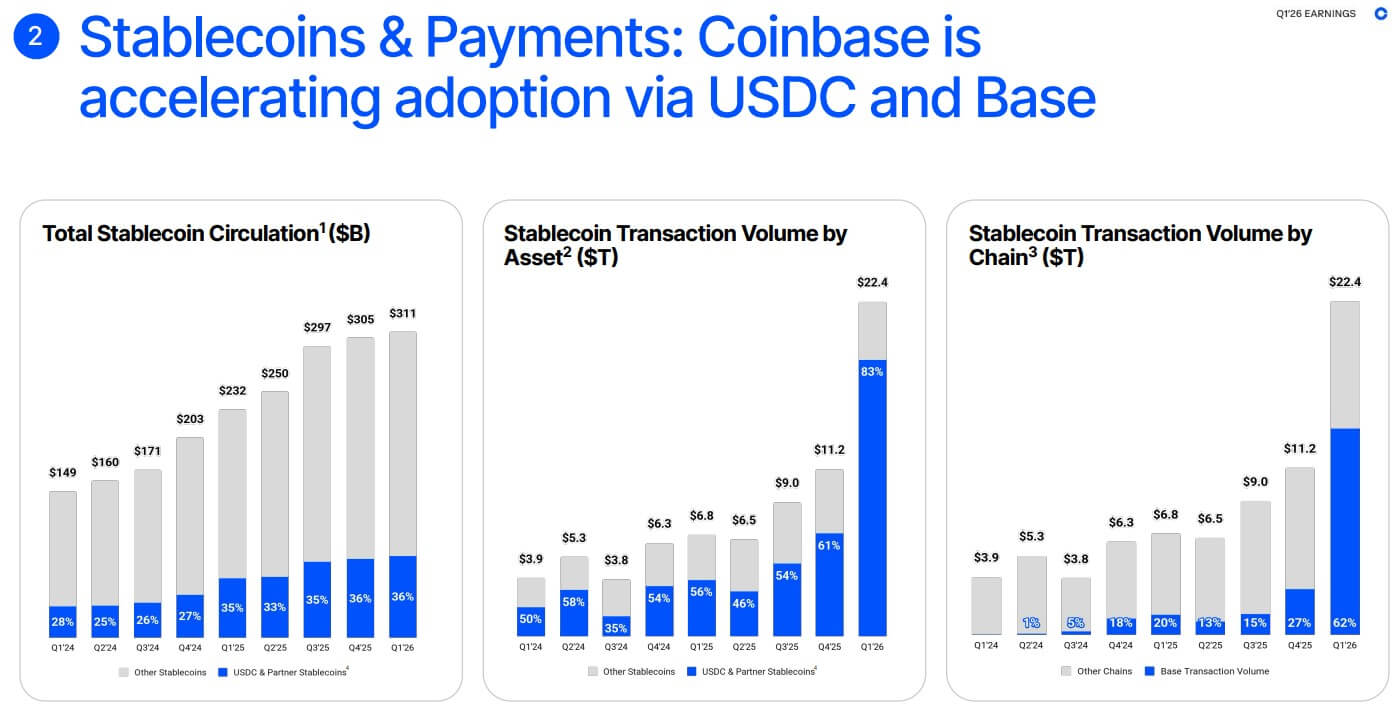

At the same time, USDC in circulation rose 28% to $77 billion, while on-chain transaction volume reached $21.5 trillion, up 263% year over year.

Circle’s Q1 Earnings Report (Source: Circle)

Those figures reinforced Circle’s position as one of the main issuers in the global stablecoin market, where tokenized dollars have become core infrastructure for trading, payments, and settlement.

However, the more important development was Circle’s attempt to move beyond issuance through its new blockchain network, Arc.

Arc gives the company a network-level growth story built around payments, tokenized assets, foreign exchange, capital markets, and AI-driven commerce.

That push places Circle closer to the terrain already occupied by Coinbase, its longtime USDC partner and the operator of Base, the Layer 2 network that the US-based exchange has positioned as a settlement layer for stablecoins, consumer payments, and agentic transactions.

Considering this, Circle’s aggressive expansion could bring a new competition to the crypto landscape: a looming, head-to-head battle with Coinbase.

Circle gives investors a wider story

Circle’s business has long been tied to the economics of stablecoin reserves. The company issues USDC, holds safe assets backing the token, and earns income on those reserves.

That model can be powerful when rates are elevated, but it also raises questions about how durable its earnings will be as interest income declines.

The company is pitching the network as an “economic operating system” for the internet, a shared environment where stablecoins, tokenized assets, and financial applications can operate on common infrastructure.

The chain is expected to be EVM-compatible, with stablecoin-native fees, deterministic sub-second finality, and configurable privacy designed for institutions that need auditability without exposing every transaction detail to the public.

Circle Chief Executive Jeremy Allaire framed the quarter around the convergence of AI platforms and on-chain money, saying:

“Circle’s first quarter reflected strong execution against a much bigger opportunity: the rapid convergence of AI platforms and economic operating systems into a new internet stack. With the ARC token presale, momentum behind the Arc network, and the launch of our Agent Stack, we are building trusted infrastructure for AI-native economic activity and a more programmable internet financial system.”

The investor list shows how far that pitch now reaches. a16z Crypto led the presale with a $75 million investment.

Other participants included BlackRock, Apollo Funds, Intercontinental Exchange, SBI Group, Janus Henderson Investors, Standard Chartered Ventures, General Catalyst,a IDG Capital, Haun Ventures, and Bullish.

The message to investors is clear: Circle wants to be valued less as a stablecoin issuer exposed to rate cycles and more as a full-stack infrastructure company for on-chain finance.

In a note shared with CryptoSlate, Clear Street analysts echoed that view, writing that Circle is “no longer a pure crypto play” and has built the Layer 1 network, application layer, and partner ecosystem required to become a critical infrastructure provider.

The firm raised its price target on the stock from $152 to $157, citing Arc, Agent Stack, Circle Payments Network, and regulatory momentum as potential sources of upside.

USDC already moves across more than 30 blockchains and is integrated throughout exchanges, wallets, fintech platforms, and institutional systems.

That distribution has been one of the stablecoin’s main strengths. Circle could grow as USDC became more widely used, regardless of where the activity settled.

Arc gives Circle a reason to bring more of that activity onto the infrastructure it controls.

The network is designed to support payments, lending, foreign exchange, capital markets, and tokenized assets. Circle has also positioned ARC as a coordination token for validators, builders, liquidity providers, exchanges, institutions, and users.

In that structure, USDC remains the transactional asset, while ARC is intended to help govern economic rules and align network participants.

That creates a broader economic layer around Circle’s core product. If Arc gains traction, investors will not only measure Circle by USDC circulation and reserve income.

They will also track transaction volume, developer adoption, institutional participation, validator activity, and the degree to which Circle can capture revenue from the infrastructure surrounding USDC.

Circle Payments Network adds another part of that strategy. Clear Street said CPN reached $8.3 billion in annualized total payment volume and approached $10 billion by May 7, with 136 financial institutions enrolled.

Managed Payments is intended to reduce friction for banks and payment service providers by handling licensing, liquidity, custody, and compliance burdens.

Taken together, Arc, Agent Stack, CPN, and Managed Payments give Circle a more ambitious public-market story. The company is trying to become the platform where digital dollars move, settle, and interact with software.

That ambition makes the Coinbase relationship more complicated.

Coinbase already controls much of the flow

However, Coinbase has its own claim to the USDC infrastructure story.

In its first-quarter report, the company described itself as the distribution engine for USDC, with more than 25% of total USDC in circulation, or about $19 billion on average, held across Coinbase products.

Coinbase said Base processed 62% of global on-chain stablecoin transaction volume during the quarter, more than all other chains combined.

At the same time, more than 100 million payments were processed through its x402 protocol, with more than 99% completed using USDC.

How Coinbase is Growing Stablecoin Adoption via USDC and Base (Source: Coinbase)

Those figures show why Arc is sensitive for Coinbase.

Coinbase is no longer merely a distribution channel for Circle’s stablecoin. It is building the rails around the asset.

Its stack includes USDC as the programmable dollar, Base as the low-cost settlement network, and Coinbase Developer Platform, AgentKit, and x402 as infrastructure for developers and AI-enabled payments.

Circle’s emerging stack points in the same direction. USDC provides the dollar asset, Arc provides the network, Agent Stack targets AI-native commerce, and CPN connects financial institutions and payment companies.

The companies remain commercially aligned around USDC growth. But their infrastructure strategies increasingly point toward the same flows.

The alliance gets a new scoreboard

For years, the Circle-Coinbase relationship was one of crypto’s cleanest partnerships. Circle issued USDC. Coinbase distributed it across its exchange, wallet, and institutional products. The stablecoin gained scale, and Coinbase shared in the economics.

That relationship helped make USDC one of the most important dollar assets in crypto. It also gave Coinbase a major stablecoin revenue line and helped turn USDC into a regulated alternative to Tether’s USDT for many US-based institutions.

However, Arc introduces a different incentive structure.

Omar Kanji, an investor at Dragonfly, captured the concern in a post asking how long the “marriage” between Circle and Coinbase can stay clean.

His argument was that the old model worked when Circle was the issuer, and Coinbase was the distributor. But Circle’s public-market demands and Arc’s token-backed network now require the company to show investors that it can own more customers, flows, and infrastructure directly.

That is where Arc overlaps with Base. Circle wants Arc to host USDC balances, tokenized assets, payments, settlement, and eventually foreign-exchange activity. Coinbase wants Base to serve as the main venue for stablecoin payments, on-chain consumer transactions, AI-agent activity, and institutional settlement.

The tension is already visible in adjacent products. Coinbase has cbBTC, a wrapped BTC product used across DeFi. Circle is preparing cirBTC, which is designed to integrate with Arc and Circle Mint.

While this overlap does not signal an immediate rupture, it shows that the companies are no longer staying in separate lanes and are beginning to compete on similar products.

AI payments raise the stakes

The competition becomes more significant when viewed through the lens of agentic commerce.

AI agents are expected to become a larger share of internet activity, handling tasks such as purchasing data, paying for software, settling invoices, managing subscriptions, and executing business processes.

Those transactions require programmable money, low-cost settlement, and infrastructure that can authorize spending without constant human intervention.

Stablecoins are well-suited to that environment because they operate continuously, settle quickly, and can be embedded directly into software. That has made agentic commerce one of the most attractive long-term narratives for stablecoin infrastructure providers.

Coinbase is already claiming early leadership. Its first-quarter materials pointed to Base’s share of on-chain agentic stablecoin transaction volume and the rapid growth of x402 payments. The company is presenting Base, USDC, AgentKit, and x402 as a ready-made stack for machine-driven economic activity.

Circle is moving to meet that opportunity with Agent Stack and Arc. Allaire has framed AI platforms and on-chain money as part of a new internet stack, and Circle’s product roadmap suggests the company wants USDC to become a settlement layer not only for humans and institutions, but also for software agents.

Considering this, Tom Wan, the head of data at Entropy Research, concluded:

“[Circle and Coinbase] business lines are converging across blockchain, tokenization, payments and stablecoins. A formal split is unlikely given the mutual benefits still on the table, but the trajectory is clear. Both sides are building toward a less dependent relationship, and the overlap will only create more friction over time.”

A third-party provider failure caused Revolut’s app to show wildly inaccurate crypto prices on Friday, the company confirmed, after users flooded social media with screenshots of Bitcoin listed at just 2 cents.

Third-Party Provider Blamed For Pricing Chaos

Revolut acknowledged the problem in a public statement, saying engineers were working on a fix and urging customers to check its status page for updates.

Hi. We want to help resolve the issues you’re facing with the Bitcoin price notification. We’re currently experiencing issues affecting some of the app’s functionalities. Please be assured that our colleagues are working on this as we speak. Please keep an eye on our status page…

The glitch wasn’t limited to Bitcoin. Users reported seeing simultaneous price drops across XRP, Solana, and even stablecoins like USDT and USDC — assets designed to hold steady at one dollar.

Screenshots shared on X and Reddit showed Bitcoin’s 24-hour chart registering a roughly 50% intraday plunge, with the price briefly anchoring near $39,900 before snapping back.

Some users also received push notifications warning that BTC had hit a 52-week low of 2 cents.

According to Revolut, The price of Bitcoin has just dropped to $0.02

Pricing data on major aggregators showed nothing unusual during the same window. Bitcoin’s price on CoinMarketCap and CoinGecko held steady, with no sign of any crash in derivatives markets either. The anomaly appeared entirely contained within Revolut’s app.

Ranveer Arora, a former PwC quantitative trading lead and co-founder of Altura.trade, told reporters two explanations are in play.

The first is a corrupt data tick pushed through Revolut’s pricing system — a single bad data point that briefly anchored the chart before being corrected.

Because Revolut is not an exchange and pulls prices from outside providers, one faulty input can be enough to produce exactly this kind of chart distortion.

The second possibility is a transient liquidity gap. Revolut’s order book is shallower than what you’d find on a full exchange, so a large sell order could theoretically exhaust available bids and print a sharp downward wick before prices recover.

Arora noted, however, that the lack of matching prints on any other platform makes the data feed explanation more likely.

Why Retail Apps Face Unique Data Risks

Marc Tillement, director of blockchain price oracle Pyth Data Association, said the episode shows how quickly a single bad data point can distort price perception — particularly in retail-facing systems where users may not think to cross-check what they’re seeing.

Tillement said that as markets grow more data-dependent, the reliability of pricing infrastructure becomes central to how much traders can trust what’s in front of them.

Transparent, verifiable data layers, he argued, are what separate a glitch from a crisis.

Featured image from Pixabay, chart from TradingView

Crypto rhetoric has long prized the ability to transact without gatekeepers, to move value across borders without asking permission, and to hold assets no institution could seize.

Crypto culture treated these as design virtues, properties that builders embedded with ethical weight by deliberate architectural choice. Then the Drift exploit happened, and the backlash told a different story.

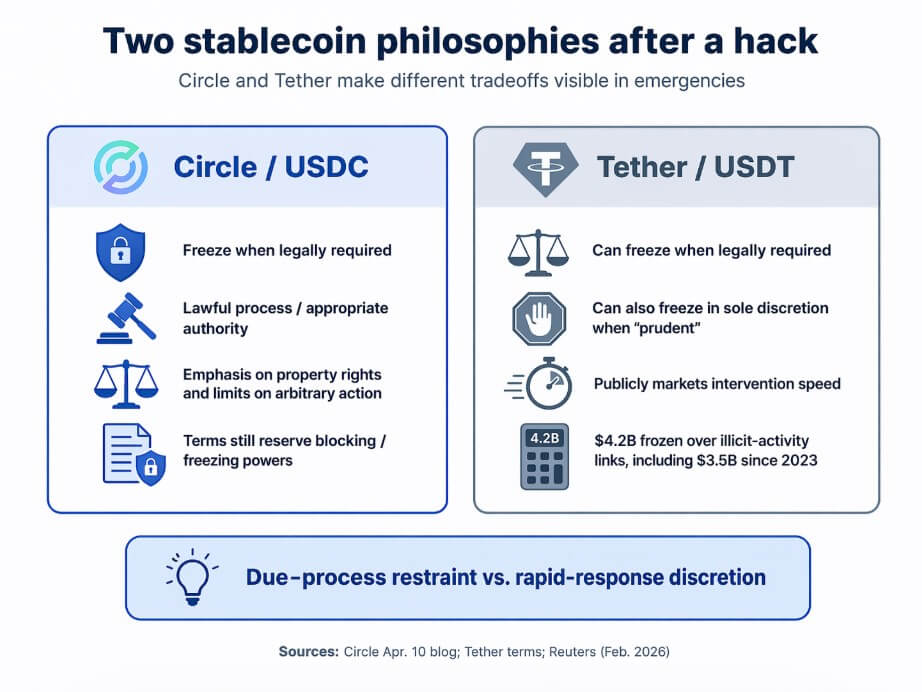

On Apr. 1, Drift suffered a major exploit. Circle later described the publicly reported losses as exceeding $270 million, while other reports put the figure around $285 million and documented criticism that Circle had not frozen stolen USDC as it moved across its cross-chain rails.

The attacker routed roughly $232 million in USDC from Solana to Ethereum using Circle’s Cross-Chain Transfer Protocol. The backlash stemmed from users and observers wanting to know why Circle had not intervened sooner.

Days later, Tether CEO Paolo Ardoino posted that Tether had frozen 3.29 million USDT tied to the Rhea Finance attacker, framing the intervention as proof that “Tether cares.”

Circle published its formal response on Apr. 10, and its core argument was that USDC freezes occur when the law requires action. Circle is legally compelled by an appropriate authority through a lawful process.

Circle pushed back on the idea that an issuer should act as an ad hoc chain police force, arguing that open access to permissionless infrastructure is a feature, and that the bigger problem is that legal frameworks have not yet kept pace with the speed of on-chain exploits.

The stablecoin issuer also made a property-rights argument, claiming that arbitrary freezes set dangerous precedents for lawful users, and the power to freeze is a compliance obligation, constrained by lawful process and legal compulsion, authorized only through formal legal channels.

The complication is that Circle’s own legal documents tell a more layered story.

USDC terms state that transfers are irreversible and that Circle carries no obligation to track or determine the provenance of balances.

Those same terms also reserve Circle’s right to block certain addresses and, for Circle-custodied balances, freeze associated USDC in its sole discretion when it believes those addresses may be tied to illegal activity or terms violations.

Circle holds meaningful freeze power and frames it as a tightly bound compliance function, constrained by legal process and compulsion.

Ardoino’s Rhea post was a boast, and Tether’s terms grant it broad discretion by stating that the company may freeze tokens as required by law or whenever it determines, in its sole discretion, that doing so is prudent, and authorizing it to blacklist token addresses.

In February, Tether froze approximately $4.2 billion in USDT due to links to illicit activity, with $3.5 billion of that since 2023.

Circle freezes USDC only when legally compelled, while Tether reserves sole discretion to freeze and has frozen $4.2 billion over illicit-activity links.

The feature nobody advertised

What Drift and Rhea forced into the open is a question that stablecoin competition had not yet fully surfaced: in a hack, what do users actually want from an issuer?

The anti-censorship instincts that shaped crypto’s early culture tend to lose their force the moment users need an emergency brake. Affected protocols, exchanges holding stolen funds, and victims watching their balances drain want to know who can stop the thief.

That reframes freeze capacity as more of a consumer-protection feature.

Tether has been accumulating a record of intervention and visibility. Ardoino’s Rhea post was designed to be read as a product statement, and in the context of a fresh exploit, it worked.

The emotional and practical logic is accessible, showing that one issuer froze stolen funds the same day an attacker moved them, while another issuer said legal timelines tied its hands.

This makes optics difficult for Circle regardless of the legal merits of its position.

Stablecoins are quietly differentiating themselves in emergency governance, alongside reserve composition and exchange liquidity.

The cost of the feature

The case for Circle’s position is real and does not require dismissing the Drift backlash to hold. Broad issuer discretion over freezes creates risks that extend far beyond hack scenarios.

An issuer that can freeze tokens in its sole discretion when it determines it is prudent can freeze tokens for reasons unrelated to protecting victims. Politically contentious addresses, disputed transactions, regulatory scrutiny from a single jurisdiction, or simple operational error can all trigger freezes under terms as broad as Tether’s.

The same capacity that lets an issuer stop a thief also lets it stop a protester, a dissident from a sanctioned country, or a business whose activity it finds inconvenient.

Circle’s public writing on the Drift exploit is, among other things, a defense against that risk. The argument that emergency intervention needs new legal frameworks and safe-harbor structures is also an argument that the current situation is a problem, even when the targets are criminals.

The absence of defined standards means an issuer can act generously today and overreach tomorrow, with no formal mechanism to distinguish the two.

Tether’s freeze record has not yet produced a major documented wrongful-freeze controversy, but that record is also vast and not fully transparent.

Reports on the $4.2 billion in frozen USDT withhold the details of each decision, the legal process underlying each freeze, and the error rate across thousands of enforcement actions.

Fast intervention looks different in the abstract when the process generating those interventions is opaque.

Benefit of fast freezes

Cost of broad freeze discretion

Can slow or stop stolen funds

Can enable arbitrary intervention

May improve recovery odds

Can affect lawful users

Helps exchanges/protocols in crises

Can reflect political or regulatory pressure

Looks like consumer protection in hacks

Process may be opaque

Becomes a due-diligence feature

Wrongful-freeze risk may be hard to challenge

Two paths from here

The bull case for intervention-first issuers runs in a world where hacks keep coming, and recoverability keeps rising on the priority list.

More regulatory scrutiny on exchanges to show they take asset protection seriously, and more institutional users who need to demonstrate due diligence in custody and recovery. These are factors that push emergency freeze capacity to the center of stablecoin evaluation.

In that scenario, Tether’s public freeze record and broad discretionary terms become genuine competitive assets. Exchanges and protocols that have experienced exploits now treat fast-intervention capacity as a due diligence criterion when choosing which stablecoin to hold as primary liquidity.

Circle has to either act faster through new legal mechanisms or accept that some market segments will treat its rule-of-law posture as a liability in crises. Ardoino’s Rhea post, in retrospect, looks like an early entry in a competition that the market eventually formalizes.

The bear case for that same model runs through wrongful freezes, regulatory backlash, and the discovery that broad discretion is often a liability as much as a virtue.

A high-profile incorrect freeze, such as an address flagged as malicious that belongs to a legitimate user, a jurisdiction-specific enforcement action that appears to be politically targeted at users in other markets, or an operational error that freezes clean funds during a market stress event, turns the same emergency-governance story toxic.

In that world, Circle’s insistence on lawful process and defined standards looks like principled restraint, a deliberate commitment to defined limits over speed, and users place a real premium on an issuer whose freeze decisions carry formal accountability.

The crypto community’s historical skepticism toward centralized control reasserts itself as hard-won practical wisdom, grounded in the documented costs of unchecked issuer discretion.

The stablecoin winners in that scenario are the ones whose intervention power is real but bounded. Issuers who can act in genuine emergencies and demonstrate they held back in ambiguous ones.

Stablecoin governance splits between intervention-first issuers gaining crisis goodwill and bounded-discretion issuers winning users who reprice centralization risk, per Circle and Tether materials.

As stablecoins deepen their role in institutional payments, treasury workflows, and regulated financial infrastructure, governance under stress becomes as material as reserve quality or distribution reach.

The question that Drift and Rhea put on the table of how much control users want an issuer to have has no clean universal answer. Institutions with large exposures and recovery obligations may want emergency brakes, while individuals holding stablecoins across politically sensitive jurisdictions may want the opposite.

Protocols with mixed user bases need to answer for both.

The real contest now is for the version of stablecoin governance that earns enough trust from enough users to become the default.

Stablecoin tax treatment in the U.S. is at the center of a new legislative push to exempt qualifying daily transactions involving regulated payment stablecoins from tax.

The latest version of the PARITY Act would stop gain or loss recognition on certain stablecoin sales unless a taxpayer’s basis falls below 99% of the token’s redemption value, marking a direct attempt to treat routine stablecoin spending more like cash payments. The proposal also revises rules on staking rewards and digital asset wash sales, while lawmakers in Washington continue to debate broader crypto legislation.

Stablecoin payments provision removes small transaction tax burden

The bill is grounded on the past discussion drafts issued in December 2025 and on March 26, 2026. The earlier proposal recommended a $200 limit on payments made with regulated payment stablecoins, as in the de minimis section.

That structure was altered in the March 2026 draft. Instead of using a de minimis criterion, the text states that no gain or loss would be recognized on the sale of a regulated payment stablecoin unless the taxpayer’s basis in that stablecoin is less than 99% of its redemption value.

Another standard eliminated by the draft was the previous $200 standard. In addition, it created a deemed basis of $1 for exchanges, which the text treats separately from the stablecoin’s sales. That development solves one of the long-term problems of crypto users. The current tax treatment states that any payment made using USDC or USDT can result in a taxable event, even when the change in value is minimal.

Meanwhile, the bill creates a distinction between passive staking and other activities, such as trading. It would also enable taxpayers to decide when to record staking rewards, upon receipt or after a deferral period of not more than 5 years, as indicated in the material. To qualify under the proposed stablecoin treatment, the asset must be regulated under the GENIUS Act and remain within 1% of its $1 peg.

Stablecoin debate comes alongside ongoing crypto policy pressure

The tax proposal comes following pressure on other digital asset legislation, including the CLARITY Act. Senator Cynthia Lummis recently pointed out that the bill could remain stalled until 2030 if the Senate fails to act before the 2026 election cycle.

At the same time, as reported by Cryptopolitan, the Trump White House has pushed back on concerns over stablecoin yield provisions. A Council of Economic Advisors report dated April 8 said the effect on bank lending would be limited, estimating a 0.02% increase, or about $2.1 billion.

The same report said community banks would face about $500 million in additional obligations, equal to a 0.026% increase over current lending activity. It concluded that banning yield would provide little protection for bank lending while giving up consumer benefits tied to competitive returns on stablecoin holdings.

Your bank is using your money. You’re getting the scraps. Watch our free video on becoming your own bank

RealFi Launches USDr — Turning Idle Stablecoins into Real-World Returns

Press Release — Embargo Lifted 09 April 2026, 11:00 BST

London · 09 April 2026 · DeFi & Real-World Assets

RealFi Launches USDr: Turning Idle Stablecoins into Real-World Returns

New crypto-native platform targeting up to 9%* APY, putting hundreds of billions in dormant stablecoins to work through real-world market investments

9%*Target APY

$1BTVL Target

USDrYield-Bearing Stablecoin

No Lock-UpLiquidity

RealFi today announced the launch of its platform alongside the introduction of USDr — a decentralised, yield-bearing stablecoin pegged to the US dollar that enables investors to put their dormant stablecoins to work, earning real returns backed by real-world market investments.

The Opportunity

RealFi is a crypto-native financial platform targeting one of the most underleveraged assets in digital markets: stablecoins. With hundreds of billions in circulation globally across high-growth markets including Nigeria, Vietnam, Kenya, Indonesia, Turkey, Brazil and Argentina, stablecoins have become DeFi’s most successful digital asset. Yet for most holders, they remain idle — preserving value but failing to work as an investment tool.

USDr changes that. Through exposure to real-world market investments rather than traditional banking infrastructure or passive fiat reserves, USDr enables investors to earn yields of up to 9%* APY with no lockup — delivering meaningful returns in a market increasingly focused on capital efficiency.

“Stablecoins are the most underleveraged asset class in crypto — hundreds of billions sit idle when they could be generating real returns for their holders. USDr changes that equation entirely. We’ve built a platform that is transparent, accessible and designed to deliver genuine value.”

— John O’Connor, CEO & Founder, RealFi

How It Works

The platform is designed for accessibility. Users can purchase USDC directly in their Lace wallet, convert it seamlessly into USDr, and stake to begin earning yield immediately — lowering the barrier to entry for retail users while remaining attractive to crypto treasuries and sophisticated DeFi participants.

USDr’s yield is backed by real-world economies: a diversified reserve of Money Market Funds and Corporate Floating Rate Bonds — meaning every dollar in USDr supports real businesses and real infrastructure, rather than relying on risky crypto-native leverage.

Infrastructure & Ecosystem

RealFi is currently entering a testnet phase alongside an initial institutional onboarding process, with broader availability anticipated later this year. The platform is supported by Input Output Global and follows the integration of USD Coin on the Cardano network in March, boosting DeFi capabilities across the network before expanding to other ecosystems.

RealFi is targeting $1 billion in TVL as it scales across Cardano, Ethereum and Bitcoin networks.

“We’re bringing investors and borrowers closer to the company, and closer to the rewards, whereas a traditional banking sector keeps them at arms length, in many cases depriving them of any kind of financial autonomy.”

— John O’Connor, CEO & Founder, RealFi

Early Participation

Early participants on the RealFi platform will have the opportunity to earn R-Points through active engagement and platform participation. R-Points recognise and reward community contribution during the platform’s early growth phase and distribution across chains. Further details regarding R-Points, including any future utility or conversion mechanics, will be communicated to participants in accordance with applicable regulatory requirements and platform terms.

Investors can register their interest now at realfi.co, as well as sign up for the testnet waitlist.

About RealFi

RealFi is a crypto-native stablecoin platform that bridges decentralised finance with real-world market investments. Through its flagship product USDr — a yield-bearing stablecoin pegged to the US dollar — RealFi enables stablecoin holders to earn sustainable returns. Built on the Cardano blockchain and integrated with the Lace wallet, RealFi is designed to make DeFi yields simple, transparent and accessible to users worldwide.

Important Notices & Disclaimers

Geographic Restrictions: RealFi products are not available to users in the United States (US), European Union (EU), United Kingdom (UK), Hong Kong (HK), or other restricted or sanctioned jurisdictions. It is the responsibility of each user to ensure compliance with the laws and regulations applicable in their jurisdiction prior to accessing the RealFi platform or any of its products.

Forward-Looking Statements: This press release contains forward-looking statements, including statements regarding anticipated product launch timelines, platform development milestones, and projected TVL targets. These statements reflect current expectations and targets only, and are subject to risks, uncertainties, and changes in circumstances that could cause actual outcomes to differ materially. RealFi undertakes no obligation to update or revise any forward-looking statement following publication of this release.

Risk Disclosure: USDr is a digital asset that provides exposure to a portfolio of real-world financial instruments. It is not a bank deposit, is not insured, and carries risk, including potential loss of principal. Returns are variable, based on market conditions, and are not guaranteed. Redemptions may be subject to timing delays, liquidity constraints, and market conditions. The value of underlying assets may fluctuate, and there is no assurance that USDr will maintain a constant value relative to the US dollar at all times. Access to the platform is subject to onboarding procedures, including identity verification and compliance with applicable anti-money laundering and sanctions regulations.

*APY is indicative, based on current rates, and subject to change. Not a guaranteed return. Capital at risk. *Indicative only