The Senate Banking Committee’s CLARITY Act is heading into Thursday’s markup, buried under opposition.

According to reports, Senator Elizabeth Warren alone filed more than 40 amendments before Tuesday’s 5 p.m. ET deadline, and American Bankers Association members sent over 8,000 letters to Senate offices in less than a week demanding changes to the bill’s stablecoin yield rules.

Over 100 Amendments Filed

The total number of proposed amendments going into Thursday is still being confirmed, but according to a list obtained by Politico, there have been more than 100 proposed. To put things in perspective, a total of 137 revisions were proposed before the markup scheduled for January, which was canceled.

Warren’s batch alone covers a wide range of restrictions. One amendment that stood out would bar the Federal Reserve from issuing master accounts to crypto companies, which would effectively cut such firms off from the core infrastructure of the US banking system.

The lawmaker also attacked the updated bill on X, arguing that it lacked ethics provisions tied to President Donald Trump’s crypto businesses.

“No bill should move through the Banking Committee without real ethics guardrails,” she wrote.

That dispute has become harder for negotiators to avoid. Late last month, analyst Simon Dedic claimed that Trump’s meme coin and his crypto-related dinners were part of the reason the CLARITY Act was going nowhere, with Democrats demanding conflict-of-interest language before backing the legislation.

Another revision, filed by Senator Jack Reed of Rhode Island, would prohibit crypto from being used as legal tender, including for paying taxes. That proposal runs directly counter to a bill Representative Warren Davidson introduced last year that would have allowed Bitcoin to be used for precisely that purpose.

Senators Reed and Tina Smith of Minnesota also filed a joint amendment that would incorporate bank-requested changes to the stablecoin yield language.

According to journalist Brendan Pedersen, the proposal will force senators to choose between crypto and the banks on a single vote, making it an uncomfortable moment for Republicans who tend to side with both.

Bankers Blitz Senators With 8,000 Letters

Elsewhere, members of the American Bankers Association have reportedly sent more than 8,000 letters to Senate offices since last Friday, pushing lawmakers to change the bill’s stablecoin yield compromise.

However, Stand With Crypto, the crypto advocacy group, responded with its own numbers on Tuesday, saying its advocates had called Congress 8,000 times and sent 300,000 emails over recent months to protect stablecoin rewards, and have contacted lawmakers nearly 1.5 million times in support of the CLARITY Act overall.

Those on the side of digital assets are framing the banking industry’s lobbying campaign as an attempt to block competition from yield-bearing stablecoins.

Senator Bernie Moreno accused banks of trying to “kill stablecoins that would let everyday Americans earn real yields on their own money.” He also described the banking industry as a “cartel” protecting low-interest deposit models.

But not everyone inside Washington thinks this fight ends at Thursday’s committee vote. According to reporter Sander Lutz, banking policy leaders are already preparing for another push on the Senate floor if they lose the markup battle over yield restrictions.

Meanwhile, crypto journalist Eleanor Terrett reported that Senate Minority Leader Chuck Schumer privately encouraged Democrats to work toward supporting the bill.

As the Senate Banking Committee prepares to mark up the long-anticipated CLARITY Act on Thursday, Coinbase CEO Brian Armstrong has argued that the newest version of the bill represents a workable “compromise” and could meaningfully improve the US financial system.

Speaking to FOX Business, Armstrong said the updated draft reflects concessions on both sides—what he described as the crypto industry meeting requests from bank lobbyists and lawmakers, while the banking sector also gave ground during negotiations.

Coinbase CEO’s CLARITY Act Pitch

Armstrong also highlighted one specific element tied to stablecoin rewards. He said the approach in the latest bill would only apply when there is “some sort of material activity on the account,” adding that he believes the overall package would make the system “more efficient.”

The claim is that the legislation would help streamline financial services, reduce friction, and make access easier for consumers and businesses—while still keeping the framework aligned with banking-sector concerns that were raised during talks.

Still, critics point to the banking industry’s pushback as evidence that the dispute is far from settled. As reported throughout the week by Bitcoinist, banking trade groups have opposed the CLARITY Act’s stablecoin-rewards provision, arguing that it could give crypto firms too much flexibility.

Their position is that the policy might also encourage deposits to shift away from traditional, insured banking channels rather than strengthening them.

Beyond the details of stablecoin rules, Coinbase CEO argued that the broader direction of the CLARITY Act reflects growing institutional interest in digital assets.

In his view, banks are increasingly integrating stablecoins and crypto-related services because customer demand is rising—an angle that suggests the bill, if passed in its current form, could provide the clearer structure institutions want before expanding further.

Can The Latest Crypto Bill Draft Survive?

Supporters of the bill are not limited to Coinbase. Ripple CEO Brad Garlinghouse also backed the current push, commenting on social media site X (previously Twitter) that the Senate Banking Committee is “putting in the work” to move the CLARITY Act forward.

Garlinghouse’s message emphasized that Ripple supports the bill because crypto businesses and major participants should have the “same rules and protections as every other asset class,” and because—if the US is serious about leading in crypto—this is the moment to finalize legislation and get it done.

Even with that backing, the legislative road ahead is not smooth. Politico reported that Senator Elizabeth Warren, a well-known crypto skeptic, is vowing to pursue extensive changes to the bill through amendments.

The reporting says Warren and others are preparing more than 100 amendments ahead of the markup, following the release of an updated 309-page draft that expands on an earlier 278-page version introduced in January.

According to the same reporting, Warren submitted more than 40 amendments on her own, with much of the rest attributed to Democratic members of the Banking Committee.

This mirrors earlier moves around the bill: the January markup session drew 137 amendments, and it was eventually cancelled after a period of resistance that included Armstrong and Coinbase withdrawing support for the bill at the time.

For now, the core question going into Thursday’s markup is whether the latest CLARITY Act draft can hold together.

Featured image created with OpenArt, chart from TradingView.com

A senior White House official has accused major banking trade leaders of refusing to join earlier talks on stablecoin rewards, escalating a dispute that has become one of the final pressure points ahead of the Senate Banking Committee taking up the CLARITY Act this week.

In a May 11 post on the social media platform X, Patrick Witt, executive director of the White House Presidential Advisory Committee on Digital Assets, said he had asked American Bankers Association President Rob Nichols and other bank trade CEOs to attend the February meetings aimed at resolving the question of stablecoin rewards and yield.

“I specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them?”

The criticism injected the White House more directly into a fight that has divided banks, crypto companies, and lawmakers ahead of a scheduled May 14 markup of the CLARITY Act.

The bill is designed to create a broader market structure framework for digital assets, but the treatment of stablecoin rewards has become a flashpoint over competition for deposits, consumer yield, and the future shape of dollar-based payments.

Witt’s comments also reframed the timing of the banking industry’s objections. Rather than a new technical concern emerging before a committee vote, the White House official cast the dispute as an unresolved issue that banking leaders had an opportunity to address months earlier.

Banks reopen stablecoin rewards fight before markup

Over the weekend, the American Bankers Association (ABA) urged bank executives and employees to press senators for tighter restrictions in the CLARITY Act before the committee vote, warning that the current bill could still allow crypto firms to offer reward structures that resemble interest on deposit-like products.

Nichols told bankers that lawmakers needed to hear from the industry before the legislation advanced.

The ABA’s concern is that stablecoin issuers, exchanges, or related companies could attract customer funds by offering returns on assets that compete directly with traditional bank deposits.

Banks rely on deposits as a funding base for loans to households, small businesses, farms, and corporations. If customers move cash into stablecoins that offer rewards, banks argue that lenders could face higher funding costs, tighter margins, and less capacity to extend credit.

The banking industry has described the current compromise language as leaving a loophole.

In its view, a ban on stablecoin issuers paying yield would be insufficient if affiliated exchanges, brokers, or other crypto platforms could deliver similar economic benefits through rewards, rebates, or incentive programs.

That position has put banks at odds with crypto companies that see the rewards language as a basic competition issue.

Stablecoin reserves are typically held in cash, short-term Treasuries, or other liquid instruments that generate income. The policy fight centers on whether consumers should be able to receive part of that return, and which type of institution should be allowed to offer it.

The recent Senate compromise has attempted to separate passive yield from activity-based rewards.

That distinction was meant to prevent stablecoins from becoming direct substitutes for interest-bearing deposits while preserving room for crypto platforms to reward users for participation, payments, or other services.

White House analysis undercuts the lending warning

The Council of Economic Advisers said in an April report that banning stablecoin yield would provide only a marginal lift to bank lending under its baseline assumptions. The CEA estimated that such a ban would increase bank lending by about $2.1 billion, equal to roughly 0.02% of total lending in the base case.

That finding gives the administration a counterweight to the banking sector’s claim that stablecoin rewards could meaningfully damage credit creation.

The report argued that most stablecoin reserves would not be permanently removed from the banking system. Instead, reserves held in cash, bank deposits, or Treasury instruments would continue to circulate through financial markets in different forms.

The CEA also said a more severe impact would require a much larger stablecoin market and more restrictive assumptions about how reserves are held. In the administration’s framing, stablecoin rewards may affect bank margins, but the baseline effect on lending capacity appears limited.

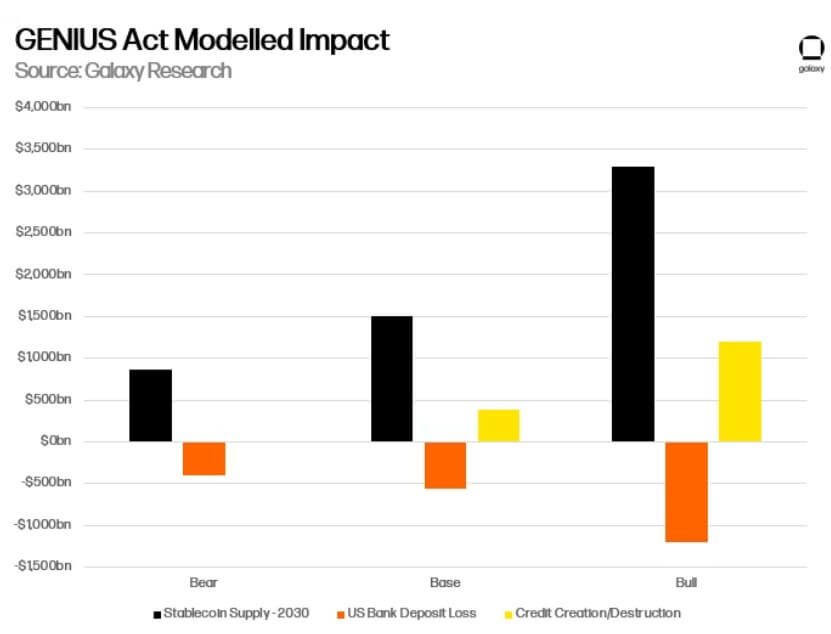

Moreover, a separate analysis by Galaxy Research furthered the argument by focusing on the international flow of dollars.

Galaxy said banks were overstating the risk that stablecoin growth would simply drain domestic deposits. Its model projected that much of the growth under a regulated stablecoin framework would come from offshore users seeking easier access to dollar-denominated assets.

That finding changes the economic lens. If stablecoins mostly draw funds from US bank accounts, banks face a direct deposit migration problem.

However, if much of the growth comes from foreign users moving into dollar stablecoins, the effect could be an inflow into US financial infrastructure rather than a one-way drain from domestic lenders.

Galaxy estimated that 60% to 70% of stablecoin growth under the GENIUS Act framework could originate offshore. It also projected that imported deposits from foreign demand could exceed domestic deposit migration by roughly 2:1.

The firm said each newly minted stablecoin dollar could generate about 32 cents of net US credit, with total credit expansion reaching about $400 billion through 2030 in its base case and as much as $1.2 trillion in a stronger growth scenario.

GENIUS Act Impact on Stablecoin (Source: Galaxy Digital)

It also projected that stablecoin reserve demand could compress Treasury bill yields by 3 to 5 basis points, potentially lowering federal borrowing costs.

Meanwhile, Galaxy did not dismiss the pressure on banks. The report said some low-cost deposits would likely migrate, funding costs could rise at the margin, and net interest margins could compress in business lines sensitive to rate competition.

Still, the firm concluded that stablecoins could pressure banks that rely on cheap deposits, increase demand for US Treasury bills, import offshore dollar capital, and expand the reach of the US financial system.

Crypto allies accuse banks of protecting margins

Crypto advocacy groups have seized on the ABA’s push as evidence that banks are trying to block competition days before the committee vote on the CLARITY Act.

Coinbase-backed Stand With Crypto urged supporters to contact senators, saying banking lobbyists were trying to weaken stablecoin rewards language before the markup.

The group framed the dispute as a consumer-rights issue, arguing that users should be able to earn returns on their own digital assets rather than have that value captured by intermediaries.

Cody Carbone, CEO of The Digital Chamber, said banks had months to negotiate over the issue and were now trying to force changes late in the process. He described the ABA campaign as an attempt to shield incumbents from competition after earlier opportunities to engage had passed.

Sen. Bernie Moreno, an Ohio Republican on the Banking Committee and a supporter of crypto legislation, used sharper language about the bank’s opposition to CLARITY Act.

He accused the “banking cartel” of trying to preserve a system in which banks pay depositors little while earning profits from lending and securities portfolios.

Moreno wrote on X:

“During the Biden era, these same banks worked hand-in-glove with Sen. Warren and her allies to debank Americans, including President Trump’s own family. They shut down accounts of conservatives, patriots, and anyone who dared challenge the regime, all while regulators applied pressure under schemes like Operation Choke Point 2.0. It wasn’t about risk. It was about political control. Now that innovative stablecoins threaten to break their monopoly and give you actual financial freedom? They’re running to Congress again, screaming about ‘threats to economic growth and financial stability.’”

Moreno’s statement showed how the stablecoin rewards dispute has moved beyond technical drafting.

The fight now carries a broader political message about financial competition, consumer returns, and resentment toward large banking institutions.

That rhetoric could help crypto advocates rally support, especially among Republicans who view stablecoins as part of a broader agenda around financial innovation and dollar competitiveness.

However, it also risks hardening opposition from lawmakers who are already concerned that crypto firms are seeking bank-like privileges without equivalent oversight.

Markup will test whether the stablecoin compromise can hold

If the committee advances the CLARITY Act with the current language largely intact, crypto firms will claim momentum, and banks will likely shift their campaign to the full Senate.

If lawmakers tighten the rewards provisions, the banking industry will have succeeded in reopening one of the most contested parts of the bill at the final stage before markup.

Meanwhile, the vote will also test the broader coalition behind the CLARITY Act. Republicans have pushed digital-asset legislation as a priority, while some Democrats have remained open to a market-structure bill if it includes stronger consumer protections, ethics, and anti-money-laundering provisions.

The stablecoin fight complicates that effort because it cuts across several policy lines at once. It raises questions about bank funding, consumer yield, Treasury demand, offshore dollar usage, and the role of crypto firms in payments.

That gives senators several reasons to demand changes, but also makes the issue difficult to settle cleanly.

Senator Bernie Moreno on Monday accused the U.S. banking lobby of full panic mode over CLARITY Act stablecoin yields. The American Bankers Association is urging bank CEOs to pressure senators against the provisions.

The Ohio Republican sits on the Senate Banking Committee. He published the criticism on X ahead of Thursday’s CLARITY Act markup.

ABA Letter Targets CLARITY Act Stablecoin Yield Language

ABA CEO Rob Nichols sent a Sunday letter to every bank CEO in the country. He called for “immediate engagement” on stablecoin yield policy.

Nichols warned that the current proposal would prompt deposit flight into payment stablecoins, citing risks to growth and stability. His note described what banks call a stablecoin loophole in the committee’s draft.

“we believe committee members may not be fully aware of the risks to the economy by the stablecoin loophole,” read an excerpt in the letter, citing Nicholas.

Moreno rejected that framing, saying the question was already litigated during the GENIUS Act debate led by Senator Bill Hagerty.

🚨 The banking cartel is in full panic mode. 🚨

While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill… pic.twitter.com/Phd6HsdBXR

The Senate Banking Committee marks up the CLARITY Act on Thursday, May 14, at 10:30 a.m. ET. Polymarket bettors now give the bill a 73% chance of becoming law this year.

Senators Thom Tillis and Angela Alsobrooks brokered the disputed compromise text. It bars yield “economically or functionally equivalent” to deposit interest. The provision still permits rewards from bona fide platform activity.

“I specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them? In their defense, I wouldn’t want to have to defend their position in public either,” he said.

A successful markup would advance the bill toward a full Senate floor vote. A stall could sideline U.S. crypto legislation for the rest of the session.

Washington is turning stablecoins into regulated payment instruments while trying to keep issuer-paid yield away from holders. That combination changesthe economics of digital dollars and puts the value of user balances up for grabs across the intermediary stack.

The GENIUS Act bars permitted payment stablecoin issuers and foreign payment stablecoin issuers from paying holders any form of interest or yield solely for holding, using, or retaining a payment stablecoin.

The FDIC’s April 7 proposal would turn parts of that law into operating standards for FDIC-supervised issuers, including reserves, redemption, capital, risk management, custody, pass-through insurance, and tokenized-deposit treatment.

That leaves a practical question for a market that reached roughly $320 billion in stablecoin supply in mid-April. If holders cannot receive direct issuer-paid yield, the value created by tokenized dollars still has to land somewhere.

The redistribution runs through the operating stack. The fight shifts to issuers, exchanges, wallets, custodians, banks, asset managers, card networks, and tokenized-deposit providers. They are the parties positioned to collect reserve income, distribution payments, custody fees, payment fees, settlement benefits, loyalty economics, or deposit economics.

The rulebook pushes yield into the plumbing

The stablecoin framework begins with reserves. GENIUS requires permitted issuers to maintain identifiable reserves backing outstanding payment stablecoins at least 1:1, with reserve categories that include cash, bank deposits, short-term Treasuries, certain repo arrangements, government money market funds, and limited tokenized reserve forms.

It also requires reserve disclosures and redemption policies, restricts reserve reuse, and calls for capital, liquidity, risk management, AML, and sanctions controls.

That makes compliant payment stablecoins look more like regulated cash-management products than free-form crypto instruments. Issuers can hold large pools of income-producing assets. At the same time, the statute blocks those issuers from paying stablecoin holders direct interest or yield merely for holding or using the token.

The economic trade-off looked uneven in the White House’s April 8 yield-prohibition note, which estimated a baseline $2.1 billion increase in bank lending from eliminating stablecoin yield, equal to a 0.02% lending effect, alongside an $800 million net welfare cost.

The same note said affiliate or third-party arrangements could remain unless CLARITY variants close that channel.

That caveat is where the post-CLARITY money map starts. A direct issuer-yield ban controls the issuer-holder relationship. It leaves open the harder economic question of how platforms, partners, payment apps, and bank structures treat the same value once it moves through distribution or product design.

CryptoSlate has already explored how the CLARITY fight is tied to stablecoin yield, regulatory control, market structure, and banking-sector pressure.

The commercial layer asks whether the law captures only the obvious form of yield, or also the ways a platform can turn stablecoin economics into something that feels like rewards, pricing power, or bundled financial service access.

The split runs through two layers. One side of the stack is statutory and prudential: reserve assets, redemption rights, capital standards, and supervision. The other side is commercial: distribution, wallet placement, exchange balances, merchant pricing, and settlement liquidity.

The policy debate becomes sharper when those layers are separated, because a ban at the issuer level can still leave value moving through the rest of the stack.

Issuers and exchanges already show the money trail

One clear example is USDC. Circle’s public filings describe a business built around reserve income, distribution costs, and partner economics. Its 2025 Form 10-K says Coinbase supports USDC usage across key products and that Circle makes payments to Coinbase tied principally to net reserve income from USDC.

The mechanics are more explicit in Circle’s S-1/A. The payment base is generated from reserves backing the stablecoin after management fees and other expenses.

Circle keeps an issuer portion, Circle and Coinbase receive allocations tied to stablecoins held in their own custodial products or managed wallets, and Coinbase receives 50% of the remaining payment base after approved participant payments.

That structure is the money map in miniature. A holder may see a stable dollar token. In the reserve and distribution structure, the reserve yield can move through issuer retention, platform-balance economics, ecosystem incentives, distribution agreements, and payments to approved participants.

Coinbase’s own filing shows why that channel is economically meaningful. Its 2025 Form 10-K reported stablecoin revenue as a business line and said a hypothetical 150 basis-point move in average rates applied to daily USDC reserve balances held by Circle would have affected stablecoin revenue by $540 million for 2025.

The point is specific: a large platform with distribution, balances, liquidity, and a deep issuer relationship can capture economics that the statute keeps away from holders in direct form.

Asset managers and custodial infrastructure sit on the same map. BlackRock’s Circle Reserve Fund showed a 3.60% seven-day SEC yield as of April 27, while Circle’s filing describes BlackRock as a preferred reserve-management partner and discusses the reserve-management relationship.

Stablecoin economics can accrue to the reserve stack, the manager, the custodian, the issuer, and the distributor before a user ever sees a token in a wallet.

Intermediary

Economic lane

User-facing form

Policy constraint

Issuer

Reserve income and issuance scale

Stable dollar token and redemption promise

Issuer-paid holder yield is barred under GENIUS

Exchange or wallet

Distribution payments, platform balances, loyalty incentives

Rewards, fee offsets, product access, liquidity

Third-party reward treatment remains the live CLARITY fork

Custodian or asset manager

Reserve management, custody, safekeeping

Operational trust and reserve transparency

FDIC and issuer rules shape permitted reserve and custody practices

Payment integration raises intermediation and resiliency questions

Bank or tokenized-deposit provider

Deposit economics and insured-bank balance-sheet activity

Deposit-like digital dollars with bank treatment

FDIC says qualifying tokenized deposits would be treated as deposits

Wallets and payment rails turn yield into product economics

The Fed’s April 8 FEDS Note gives the policy version of that table. It identifies complex intermediation chains, vertical integration, and accelerating retail adoption through wallet partnerships as structural stablecoin vulnerabilities.

It also points to integration with payment networks, banks, retail applications, broker-dealer funding, and card networks.

The Fed is studying a market where the issuer is only one node. Wallet providers, infrastructure firms, payment processors, brokers, banks, and card networks can all sit between the reserve asset and the user experience.

The company described instant crypto-to-stablecoin or fiat conversion, a 0.99% merchant transaction rate through July 31, 2026, support for more than 100 cryptocurrencies and wallets, and PYUSD rewards for funds held on PayPal at the time of the announcement.

That is a different economic shape from direct issuer yield. The holder sees payment access, merchant savings, wallet connectivity, or rewards attached to a platform. The platform can monetize conversion, distribution, customer balances, merchant pricing, and product stickiness.

Visa’s December 2025 USDC settlement launch shows the card-network version of the same intermediary lane. Visa said U.S. issuer and acquirer partners could settle VisaNet obligations in USDC, with Cross River and Lead Bank among initial banking participants.

It described more than $3.5 billion in annualized stablecoin settlement volume as of Nov. 30, 2025, and framed the product around seven-day settlement, liquidity timing, treasury automation, and operational resiliency.

Those benefits accrue through payment networks, issuing banks, acquiring banks, fintech partners, and corporate treasury operations. The user-facing return is payment access, faster settlement, or better pricing rather than issuer-paid yield.

That distinction is central to the policy fight. A yield ban can reduce the visible consumer return on a token while allowing platforms to compete through pricing, access, loyalty, and settlement benefits. The economics remain, but the claim on them becomes mediated by the platform relationship.

Banks gain leverage if the third-party channel closes

The banking lobby understands that channel. The Bank Policy Institute argued in August 2025 that GENIUS’s issuer-yield prohibition could be undermined if exchanges, affiliates, or distribution partners are still able to pay interest indirectly on stablecoins.

BPI framed that as a loophole that could increase deposit-flight risk and weaken credit creation.

Crypto trade groups answered from the other side. Their August 2025 response argued that third-party rewards are competitive consumer benefits rather than evasion of the statute.

The dispute determines whether the post-GENIUS stablecoin market becomes a platform-rewards market or a bank-protected payments market.

The FDIC proposal adds the second bank lane. It says tokenized deposits that satisfy the statutory definition of deposit would be treated no differently from other deposits under the Federal Deposit Insurance Act.

That gives banks a cleaner argument if stablecoin rewards face stricter limits: deposit tokens can keep the economics inside the banking perimeter, where interest, insurance, and lending relationships already have a legal home.

CLARITY’s market-structure section-by-section summary points to another intermediary layer. Digital commodity exchanges, brokers, and dealers would face registration, listing, custody, segregation, disclosure, and customer-election requirements.

Customers could elect into blockchain services such as staking under conditions, while access to the exchange could not be conditioned on that election.

Those provisions reinforce the same intermediary shift by moving economic activity into supervised channels. The contested issue is who owns distribution, customer balances, wallet access, custody, settlement, and optional services.

As of press time, USDT was around $189.71 billion in market capitalization and USDC around $77.63 billion.

CryptoSlate rankings also showed USDe around $3.79 billion, PYUSD around $3.42 billion, and RLUSD around $1.6 billion. That scale means the issuer-yield rule lands first on the largest payment-stablecoin rails.

The next test is the definition of indirect yield. If lawmakers and regulators allow third-party rewards, the advantage sits with platforms that own users, balances, payments, and distribution. If they limit those arrangements, banks and tokenized-deposit providers get a stronger path to keep digital-dollar returns inside deposit products.

The emerging U.S. framework decides whether stablecoin holders can receive yield and how much of the economics of digital dollars becomes visible to users. The rest is absorbed by the intermediaries that move, custody, package, and settle those dollars.

Bitcoin 2026 Begins. BTC Holds $78K. Hoskinson Sounds the Alarm.

90 minutes with the co-founder of Ethereum. Washington descends on Vegas. And BTC tests the most important level of the year.

Lead Story

Charles Hoskinson: The Clarity Act Would Make Ethereum Illegal at Birth

This week I sat down with Charles Hoskinson for ninety minutes. Co-founder of Ethereum, founder of Cardano, architect of Midnight. He’s been in this industry longer than most people have known what a blockchain is — and he did not pull a single punch.

“The incumbents escape because they already got big under ambiguity. Everyone who comes next gets crushed by the law the incumbents helped write. He called it what it is: a ladder being pulled up.”

His argument is surgical: under the current bill’s language, Ethereum would be a security. XRP would be a security. Cardano would be a security. The mature blockchain standard as written gives no viable path for a new project to grow into something decentralized — no exchange listings, no community building, no VC, no liquidity.

What makes the take land harder is that Charles openly admits the Clarity Act is good for him personally. Cardano gets a pass. Midnight gets a pass. He’s arguing against his own financial interest, and that’s rare enough in this industry to be worth paying attention to.

On Midnight Network: the concept most people are still underestimating is what he calls the agent economy. By 2035, the majority of internet commerce won’t be conducted by humans — it will be AI agents transacting on behalf of humans. Agents need a language to talk to each other. That language is proofs. Blockchains are the only trust engine that speaks proofs natively.

Charles Hoskinson — Full Interview · Crypto Coin Show · April 2026

Market Analysis — April 26, 2026

BITCOIN / USD4H

$78,106+5.81% this week

Cautiously Bullish

Bitcoin 4H — April 26, 2026 · Signals powered by EngineeringRobo AI

Bitcoin is trading at $78,106 this morning, up 5.81% on the week and holding above $78K for the second consecutive day — a level it hadn’t opened above since early February before the Iran conflict began. The breakout is real, but it’s contested. BTC hit its highest point since January on Wednesday before sellers stepped in just beneath $80,000. Futures open interest remains at historically elevated levels while funding rates have turned negative — a rare combination that some analysts are calling a “most hated” rally, meaning short pressure could accelerate the move if bears are forced to unwind.

The structure is constructive. Institutional flows remain the floor. BlackRock’s IBIT BTC ETF had inflows of $284M in a single session last week and institutions haven’t blinked. The Iran ceasefire extension on Wednesday gave BTC a clean run to $78,300. The question now is whether the $80K level holds as resistance or becomes support.

What I’m Watching

A confirmed daily close above $80,000 with conviction volume. That’s the line that opens the path to $85K–$90K. Failure to hold $76,500 on any pullback brings $73,800 back into focus.

Support

S1$76,500

S2$73,820

Resistance

R1$80,000

R2$85,000

ETHEREUM / USD4H

$2,352+2.73% this week

Neutral → Bullish, Patient

Ethereum 4H — April 26, 2026 · Signals powered by EngineeringRobo AI

ETH is at $2,352 this morning, up 2.73% on the week but underperforming Bitcoin meaningfully. BTC dominance has climbed to 58.1%, a clear signal that capital is rotating into Bitcoin as the defensive play within crypto while altcoins including ETH face 2–3% headwinds. ETH attempted $2,400 twice this week and was rejected both times. The structure isn’t broken, but ETH is in a wait-and-see posture.

ETH outperforming BTC on a percentage basis is the signal needed before getting more aggressive. Until then, the $2,300 floor is what matters. Hold it and the setup stays intact. Lose it and $2,121 becomes the next conversation.

What I’m Watching

The ETH/BTC ratio for confirmation that alts are ready to participate. A clean hold above $2,400 with volume would change the picture quickly.

Support

S1$2,300

S2$2,121

Targets

Target$2,701

Range High$3,519

Sponsored

XYO Network — The Original DePIN Protocol

10M+ nodes. A decade of proof-of-work. XYO’s Layer One is built for high-volume data, AI infrastructure, and real-world asset tokenization — with dual tokens $XYO and $XL1.

Washington Descends on Vegas. The Lineup Is Unlike Anything We’ve Seen.

The world’s largest Bitcoin conference kicks off today at The Venetian, running April 27–29. The big story this year is Washington showing up in force — Acting AG Todd Blanche and FBI Director Kash Patel are both confirmed, joining SEC Chairman Paul Atkins and CFTC Chairman Mike Selig. Having all four in the same room at a Bitcoin event is without precedent.

Senator Cynthia Lummis returns as the primary legislative voice for the BITCOIN Act. Michael Saylor, Jack Mallers, Adam Back, David Bailey, and Eric Trump are also confirmed. With BTC holding above $78K and the Clarity Act actively debated in Congress, the timing couldn’t be more charged.

Dylan LeClair (Metaplanet) · Brent Johnson (Santiago Capital)

Nakamoto Stage

Weekly Signal Recap

★★★

Bitcoin breaks above $79K for the first time since February. BTC hit its highest level since January, driven by ceasefire optimism and institutional ETF inflows. The $80K level is the next decision point — watch the daily close.

★★★

Hoskinson: The Clarity Act would make Ethereum, XRP, and Cardano securities. The most important regulatory take of the week. If this bill passes as written, there is no viable path for new American crypto projects to achieve liquidity or decentralization. Watch the full interview →

★★★

Senator Lummis confirms bipartisan support for crypto market structure legislation. The Clarity Act now has cross-party backing — the most positive legislative signal the industry has had in years.

US Admiral confirms the military is running a Bitcoin node. “We have a node on the Bitcoin network. We’re doing operational tests to secure and protect networks using the Bitcoin protocol.” — Admiral Paparo.

Treasury Secretary Bessent calls crypto a “very important payment rail.” Institutional legitimacy from the top of US Treasury.

Tesla confirmed it held all $900M in Bitcoin through Q1 2026 — zero sold.

Michael Saylor hints at another Strategy Bitcoin purchase. Posted “The ₿eat Goes On” Sunday morning.

BTC dominance climbs to 58.1% as altcoins underperform. Pattern typically precedes either broad altcoin capitulation or a BTC breakout that pulls alts higher.

Derivatives signal a “most hated” rally. Negative funding rates + historically elevated open interest near 775K BTC. Short squeeze risk elevated.

Fear & Greed Index at 46, third consecutive session in fear territory. Micro-sentiment deteriorating even as BTC holds structure.

Justin Sun sues Trump’s World Liberty Financial, alleging his tokens were frozen and voting rights stripped.

Tether freezes $344M in USDT following US law enforcement requests linked to Iran.

BTC ETF cumulative inflows exceed $56 billion — institutional floor under every dip remains intact.

Bitcoin has now broken above its two-month range. Fear & Greed is at 46. BTC dominance is at 58.1%. And Charles Hoskinson just told us on camera that the Clarity Act, if it passes, would have made Ethereum illegal at birth.

The structure is constructive. The macro overhang is real. The regulatory picture is more complicated than the headlines suggest. All three of those things can be true at the same time — and right now, they are.

The $80,000 level is the decision point. Watch the daily close. Everything else is noise until that resolves.

Just hours before attending another event in the White House from which he had to be evacuated after multiple gunshots were heard, US President Donald Trump delivered a 45-minute keynote speech at his own meme coin gathering at Mar-a-Lago.

According to attendees cited by several journalists, he spoke about several major hot topics, including the war in Iran, Joe Biden, and the CLARITY Act.

To Sign ‘Immediately’ But…

Introduced by House Committees on Financial Services and Agriculture in June last year, the Digital Asset Market Clarity Act of 2025 (or simply, the CLARITY Act) passed in the House months later, and moved to the Senate Banking Committee where it faced multiple delays as all parties involved continue to dispute over certain regulations, especially those related to stablecoins.

Some of the key features include splitting jurisdictions between the CFTC and the SEC, with the former regulating digital commodities and the latter overseeing investment contract assets (tokens sold via securities offerings). It also wants to enhance DeFi protection by regulating centralized intermediaries rather than software developers or decentralized protocols.

Arguably, the most divisive feature was the regulation of stablecoins and potential yields, with some industry experts calling it a ‘horrible’ bill, while Coinbase was blamed for undermining it.

Nevertheless, US President Donald Trump remains optimistic that it will be passed soon and, while speaking at the Mar-a-Lago event, reportedly said he would “sign it immediately” once it lands on his desk. He has been adamant in the past that this bill has to pass as soon as possible, and even lashed out at some of the parties that were allegedly blocking it.

The Catch

In case the catch isn’t obvious until now: even though the POTUS wants it passed and he pledged to sign it immediately, it still has a long way to go. It has been roughly nine months since the House did its job, and the reports coming within this timeframe have been promising, but to no avail so far.

Deadlines have slipped, interested parties have spoken against each other, while industry experts have weighed in on the potential impact once (or if) it passes. With the midterms approaching and the Democrats’ expected victory, uncertainty is likely to increase if there’s no official resolution by then.

Charles Hoskinson: The Clarity Act Will Kill American Crypto — CryptoCoinShow

Exclusive · Blockchain Interviews

Charles Hoskinson: “The Clarity Act Will Kill American Crypto”

The Cardano and Midnight Network founder says the landmark crypto legislation — if passed in its current form — doesn’t level the playing field. It pulls the ladder up. A wide-ranging conversation on the 1933 Securities Act, why AI agents live in blockchain land, and what real crypto regulation actually looks like.

By Ashton Addison · Crypto Coin ShowFull Interview AvailableRegulationMidnight Network

From our full Blockchain Interviews conversation — watch below or on YouTube and Refinitiv TV

“Cardano will get a pass. XRP will get a pass. Ethereum will get a pass. We’re already commodities. So it’s good for me. It’s horrible for the industry.”

— Charles Hoskinson, Co-Founder of Ethereum & Cardano

When Charles Hoskinson sat down with Crypto Coin Show’s Ashton Addison earlier this month, the expectation was a conversation about Midnight Network — the privacy infrastructure project he’s been quietly building for years. What emerged was something far more candid: a dissection of why the Clarity Act, the legislation many in the crypto industry are pinning their hopes on, may be the worst outcome crypto could ask for.

Hoskinson has lived through every cycle. He helped build Ethereum before walking away to found Cardano from scratch. He’s testified before regulators, drafted legislation in Wyoming, and watched a decade of Washington promises dissolve into nothing. When he speaks about the Clarity Act, he isn’t doing it as an outsider lobbyist. He’s doing it as someone who would personally benefit from its passage — and who’s still against it.

A Law Built for the Incumbents

The central problem, in Hoskinson’s view, isn’t just that the Clarity Act is flawed. It’s that it was built for the wrong people from the beginning.

“The reason Cardano and Bitcoin and Ethereum got to where they’re at is that ambiguity gave us the freedom to be ourselves.”

Under the bill’s current language, new crypto projects would be classified as securities by default. The path to escaping that designation — what the bill calls the “mature blockchain” standard — requires the kind of community growth, exchange listings, and venture capital backing that is structurally impossible to achieve if you’re already being treated as an unregistered security from day one.

Charles Hoskinson — 33:15

“Under this law, if Ripple was founded today, XRP would be a security. Ethereum would be a security. ADA would be a security. And a Gary Gensler-esque SEC would have the law on their side. They didn’t before. They had ambiguity. So they were losing court cases.”

The irony is sharp: the projects that fought the SEC for years under ambiguous law — and largely won — are now the incumbents who benefit from a “mature blockchain” carve-out. Anyone building behind them inherits a legal framework designed to prevent them from ever reaching the same scale.

Key Risk — As explained by Hoskinson

No VC investment if you’re a security by default. No exchange listings. No community building. No path to decentralization. You can never grow into a mature blockchain because the definition of maturity requires resources you can’t access when you’re pre-classified as a security.

“It’s a bill for the incumbents,” Hoskinson said plainly. “We were allowed to succeed, but then we pulled the ladder up.”

The 93-Year-Old Problem Nobody Wants to Fix

Hoskinson’s critique goes deeper than the current bill. The root of the problem, he argues, is that Congress is trying to regulate 2026 technology using a legal framework built for the Great Depression.

1933Year the Securities Exchange Act was passed

93Years old — and effectively unamendable

$10TReal-world assets that could enter crypto with proper legislation

The definition of a “security” hasn’t been meaningfully updated since FDR was president, JFK’s father was the first SEC chairman, and the United States was clawing its way out of the roaring twenties. The definition cannot be changed because of how deeply embedded it is across regulatory and legal infrastructure — and so every attempt to regulate crypto gets distorted by it.

Charles Hoskinson — 22:02

“The very first thing you need to do is start with the definition of a security and update and modernize it — add an extra category, a concept of a blockchain-based or digital security. Then once you have that, you can use the blockchain as a disclosure mechanism, and that’s a hook you can use for rulemaking to allow ZK disclosure and all these other things.”

The solution, in Hoskinson’s framework, is not a massive omnibus bill trying to do everything at once. It’s a targeted update to securities law that creates a new category for decentralized digital assets — one that allows compliance without requiring a centralized entity that must never dissolve.

Why the Process Was Broken From the Start

Beyond the substance of the bill, Hoskinson is scathing about how it was put together. The process failed on four fronts simultaneously: it was partisan, it was pay-to-play, it excluded technical experts entirely, and it ignored the global dimension of crypto.

Process failure #1 — Partisanship

Democrats were excluded from the drafting process. With no stake in the outcome, they have every incentive to kill the legislation when they return to power — which, Hoskinson argues, they will.

Process failure #2 — Patronage

Participation cost between one and five million dollars in donations. The people in the room were addressing their own business interests, not designing industry-wide infrastructure.

Process failure #3 — No engineers, no scientists

NIST — the National Institute of Standards and Technology — was never invited. Lawyers were left to define blockchain, cryptocurrency, and digital assets without any grounding in how these systems actually work.

Process failure #4 — No global coordination

Not once did US negotiators engage with MiCA architects in Europe, the JFSA in Japan, or Singapore’s MAS. Countries waiting for US leadership to harmonize their own frameworks were left without it.

The Sarbanes-Oxley Act, passed in the wake of Enron in 2003, offers a counterexample. When the US passed it, Australia and dozens of other countries passed equivalent legislation almost immediately — because they wanted to be interoperable with the world’s largest financial market. The US had the same leverage available with crypto. It chose not to use it.

— ✦ —

The Hidden Trap in the Bill’s Language

Even for those who accept the tradeoffs and just want to get something passed, Hoskinson has a warning that has largely gone unheeded. He has identified four distinct attack vectors buried in the current language of the Clarity Act that a future, hostile SEC could use to keep projects classified as securities indefinitely.

Charles Hoskinson — 43:23

“I made a video where I showed four different attack vectors using the existing language of the bill that the Securities Exchange Commission could use to keep things as a forever security under the current language of the Clarity Act they’re trying to pass. Does anybody care? No. Because they’re incompetent.”

The core vulnerability: if the Democrats regain control of the SEC’s rulemaking apparatus — which Hoskinson views as likely after the 2026 midterms — a hostile commission wouldn’t need to pass new legislation. They could simply use the levers already embedded in the bill to structurally prevent any new project from ever graduating out of security status.

What Good Legislation Actually Looks Like

Hoskinson isn’t simply against the Clarity Act. He has a blueprint — one he helped design in Wyoming, where he successfully pushed through over thirty cryptocurrency laws with bipartisan support, including the Stem Cell Freedom Act. His process was methodical: months of preparation, simultaneous engagement with regulators, industry, and technical experts, and a modular bill structure designed to pass section by section.

Charles Hoskinson

“To get Clarity done right, we’ve got to globalize it. We’ve got to get inter-agency alignment. It’s got to represent the non-financial use cases. We’ve got to update our securities law. The carrot for that is ten trillion dollars of real world assets entering our space.”

The SEC Has Already Done Something Right

In an interview full of sharp criticism, Hoskinson offered one note of genuine credit. SEC Chair Paul Atkins has released a framework clarifying what is and isn’t a security, and that framework may be more durable than any legislative outcome Congress is likely to produce this year.

“Once that gets rolling, it’s really hard for a future SEC to turn that back,” Hoskinson said. The implication: passing a deeply flawed Clarity Act may actually make things worse than staying in the current regulatory gray zone, where the SEC’s new posture under Atkins provides practical clarity without locking in language a hostile future administration could weaponize.

— ✦ —

The Bigger Picture

The Clarity Act debate is a proxy for a deeper question: whether the crypto industry wants to replicate the financial system it was built to replace, or build something genuinely different. Hoskinson’s argument is that incumbents — the projects that survived the ambiguous years and emerged as commodities — now have a structural incentive to close the door behind them.

For anyone building a new project in America today, the stakes are clear. If the bill passes as written, you begin as a security, with no path to the resources required to escape that status. If it fails, you wait until 2029, build under the Atkins framework, and fight again from a better position.

“I’d rather fight a court case with ambiguity than fight a court case where the law is not on my side,” Hoskinson said. Coming from the man who co-founded Ethereum and built Cardano through a decade of regulatory hostility, that’s not despair. It’s strategy.

Watch the full interview

Charles Hoskinson on Midnight Network, Crypto Regulation & the Future of Web3 — Blockchain Interviews

AA

Ashton AddisonHost of Crypto Coin Show and Blockchain Interviews. Covering the digital assets industry since 2012 across YouTube, Refinitiv TV (London Stock Exchange), and 10 podcast networks.

The cryptocurrency sector has been clamoring for regulatory clarity, but concerns about the contents of the CLARITY Act have risen.

Galaxy Digital’s (NASDAQ: GLXY) research head, Alex Thorn, highlighted sanctions data and surveillance concerns, warning that the CLARITY Act may not be all good news as the community is hoping.

Is the CLARITY Act a surveillance bill in disguise?

The U.S. Senate has returned from its recess, and debates regarding the Digital Asset Market CLARITY Act have begun; however, Alex Thorn, head of research at Galaxy Digital (NASDAQ: GLXY), has urged caution.

He warned in a January 2026 client note that while the industry has long wished for regulatory clarity, the current version of the bill contains “fine print” that represents the largest expansion of financial surveillance since the USA PATRIOT Act.

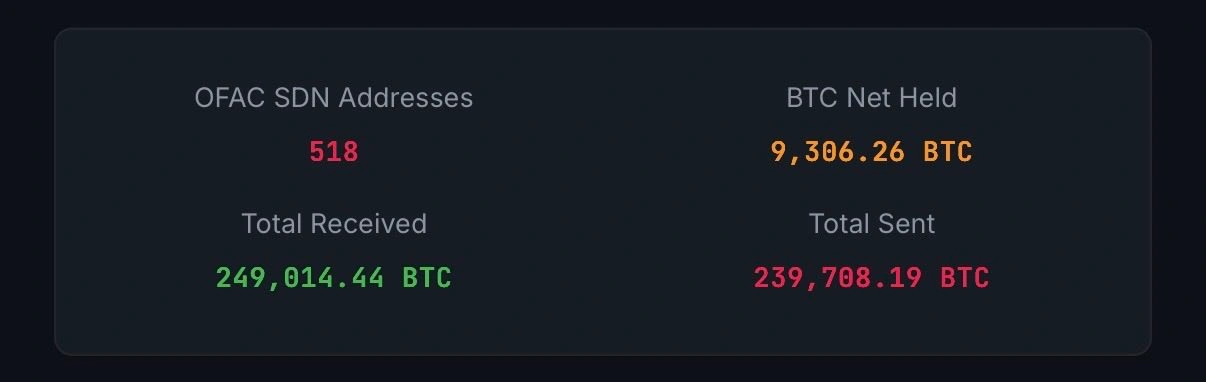

According to an analysis shared by Thorn, the U.S. Treasury’s Office of Foreign Assets Control (OFAC) has historically sanctioned 518 Bitcoin addresses. These addresses have cumulatively received 249,814 BTC, sent 239,708 BTC, and currently hold a net balance of approximately 9,306 BTC, worth roughly $707 million.

OFAC-sanctioned addresses. Source: Alex Thorn via X/Twitter

Thorn notes that OFAC’s Specially Designated Nationals (SDN) list is just one tool the Treasury uses today. However, the CLARITY Act would expand these powers significantly, giving the department new tools to intercept illicit assets.

Thorn warned in March that if the CLARITY Act does not pass committee by the end of April 2026, the odds of passage this year become “extremely low.” Reports indicate that negotiators are close to a deal on stablecoin yields, but other hurdles remain.

Supporters on the Senate Banking Committee argue the CLARITY Act is designed to “crack down on illicit finance” while protecting software developers and promoting innovation. The official summary states the bill gives law enforcement “new, targeted tools to combat money laundering, terrorist financing, and sanctions evasion.”

Aside Thorn, Cardano founder Charles Hoskinson argues the language goes too far. Hoskinson has warned that the legislation’s broad provisions could be exploited by future political administrations, regardless of which party is in power.

The fact that the bill automatically classifies new digital tokens as securities with virtually no pathway to reclassification is also an issue, as it stifles competition.

One independent analysis of a previous draft noted that while the bill includes a “Keep Your Coins Act” preventing bans on self-custody, it contains loopholes that still allow for government intervention regarding illicit finance.

The introduction of “Distributed Ledger Application Layers” in the draft could also create compliance obligations for software applications that could force DeFi interfaces to monitor users.

Who benefits from the new rules?

Wall Street giants, including JPMorgan Chase & Co. (JPM) and Citadel LLC, are actively lobbying the SEC to ensure tokenized securities do not receive special treatment.

In a recent letter to the SEC, Thorn argued that “forcing a new architecture to clone the old one” is not technology neutrality. Instead, he suggests that a decentralized automated market maker (AMM) should not be classified as an exchange because it is “autonomous code” and not an organization of persons operating a marketplace.

Thorn argues that liquidity providers (LPs) on AMMs are simply traders using their own balance sheets, not dealers serving customers.

He warns that banks and brokerages are playing a cynical game where they publicly back Bitcoin but use their Washington lobbyists to delay real integration that would threaten their control over market structure.

According to JPMorgan analysts, the legislative disputes have narrowed to two or three core questions, primarily revolving around stablecoin rewards.

The tentative compromise would ban passive “idle yield” on stablecoins, because banks fear it would drain deposits, while allowing activity-based rewards. However, critics like Ryan Adams argue that if banks succeed in killing yield provisions, it proves the Senate is prioritizing bank interests over the public.

Stablecoin Yield: Why Washington’s Battle Could Reshape Crypto Banking Forever

Regulation·28 March 2026·5 min read

Stablecoin Yield: Why Washington’s Battle Could Reshape Crypto Banking Forever

A single clause in the US CLARITY Act has sent Circle’s stock to its worst-ever single-day drop, alarmed Coinbase, and put stablecoin yield at the centre of a fight that will determine whether crypto platforms or traditional banks control the future of digital money.

AA

Ashton Addison

Founder & CEO · Crypto Coin Show · Since 2014

Syndicated via Refinitiv TV London Stock Exchange Group

A leaked draft of the Digital Asset Market Clarity (CLARITY) Act sent shockwaves through crypto markets on 24 March 2026, when provisions proposing to ban stablecoin platforms from offering yield on customer balances were reported by The Wall Street Journal. Circle Internet Group recorded its largest-ever single-day share price decline, while Coinbase also fell sharply — before both partially recovered the following day. By 25 March, Senate negotiators announced they had reached an agreement in principle with the White House on the disputed yield provisions, but the broader regulatory uncertainty remains unresolved.

Key Concept

Stablecoin Yield

Interest or rewards paid by a crypto platform to users who hold stablecoin balances — functioning similarly to a savings account interest rate, but often at significantly higher rates than traditional banks offer.

Key Concept

The CLARITY Act

US legislation currently before the Senate aimed at establishing a comprehensive regulatory framework for digital assets, covering market structure, stablecoin issuance, and the treatment of crypto platforms under existing financial law.

Context

The Fight Behind the Bill

The stablecoin yield dispute has been the single largest obstacle blocking the CLARITY Act’s advancement through the Senate. On one side, traditional banks — led by the American Bankers Association — have argued that allowing crypto platforms to pay yield on stablecoin balances risks triggering significant deposit flight away from savings accounts, ultimately threatening bank lending capacity. On the other, the crypto industry has maintained that restricting yield would leave US platforms uncompetitive against offshore alternatives and damage innovation domestically.

SEC Chairman Paul Atkins, speaking at the Blockworks Digital Asset Summit in New York on 24 March, described the prior week as “a historic week for America’s digital asset markets” and characterised recent regulatory actions as “the end of the beginning” — while cautioning that congressional legislation remains the only route to a durable framework. Atkins also criticised the prior administration’s enforcement-first approach, acknowledging that it had pushed crypto activity toward offshore jurisdictions.

Analysis

Who Wins, Who Loses if Yield Is Banned

The stakes of the yield debate extend well beyond compliance costs. If enacted in their strictest form, the CLARITY Act’s yield restrictions would align stablecoins more closely with traditional deposit products — effectively handing incumbent banks a structural advantage they have lobbied hard to preserve. For crypto-native stablecoin issuers, the consequences vary significantly by business model.

“

“The impact may be less about restriction and more about redistribution — determining who captures value and under what conditions.”

CCS Analysis · 28 March 2026

Circle, issuer of USDC and the most US-regulated of the major stablecoin operators, faces the most direct exposure given its business model’s reliance on yield-generating activities. Tether, by contrast, operates largely outside US jurisdiction and would face fewer direct constraints. This competitive asymmetry is one reason analysts suggest that a strict yield ban could paradoxically strengthen offshore operators while pressuring the more compliant, domestically-oriented platforms the legislation ostensibly aims to support.

Compounding the picture, the New York Stock Exchange announced on 24 March a collaboration with digital asset infrastructure firm Securitize to develop a blockchain-based trading platform capable of 24/7 settlement using stablecoin funding. If stablecoin yield is curtailed, the economic incentive underpinning much of that institutional infrastructure weakens alongside it.

What It Means

A More Proactive Regulatory Philosophy

What may distinguish the current regulatory moment from prior crypto policy cycles is not merely the content of the rules, but the approach underpinning them. Earlier frameworks largely focused on enforcement after misconduct, or on clarifying asset classifications as disputes arose. The CLARITY Act represents a more proactive posture — attempting to define market structure before it fully matures rather than reacting to crises once they develop.

Whether the Senate’s reported agreement in principle on stablecoin yield translates into final legislative language — and how that language is ultimately worded — will determine how value flows through digital asset markets for years to come. For crypto-native firms, the challenge is to demonstrate that innovation can operate within regulatory constraints. For traditional institutions, it is to move quickly enough to remain relevant in a market they did not build.

The CLARITY Act’s March deadline passed without a final signing. Institutional money has remained hesitant, and altcoin sentiment has stayed subdued as traders wait for Washington to deliver a definitive answer. The bill’s trajectory in the coming weeks will be one of the most consequential regulatory developments in digital assets since the FTX collapse in 2022.

")