Bitcoin just broke below $60,000. The Fear & Greed Index is sitting at 12 — Extreme Fear. One week ago it was near 52. That is a full swing from Greed to Extreme Fear in seven days.

I’ve been watching this market long enough to know what this kind of move feels like from the inside. It doesn’t feel like an opportunity. It feels like the bottom might fall out. That’s exactly why it’s worth paying close attention right now.

Let’s look at what the data actually says. The daily RSI is at 17, among the most oversold readings in years. Bitcoin is trading well below the 20-day, 50-day, and 200-day moving averages. That’s a structural breakdown, not a routine pullback. It doesn’t automatically mean we bounce. But it does mean the selling pressure is historically extreme.

“The fundamentals didn’t break. The sentiment did.”

What hasn’t changed: the GENIUS Act is law. Institutional capital is still moving on-chain. Stablecoin infrastructure is scaling. Neil Steinhardt at Nexo told me just a few weeks ago that the amount of institutions willing to work in this space increased considerably after the GENIUS Act passed — and that was before this dip.

Historically, the moments that feel like this — $60K with a Fear & Greed of 12 — are rarely the right time to panic out. They’re the moments that look obvious in hindsight. That said, no one rings a bell at the bottom. If you’re holding through this: know why you’re holding. If you’re watching from the sidelines: know what level brings you back in.

$60K is the line right now. How Bitcoin behaves around it over the next few sessions will set the tone for the weeks ahead.

Ashton Addison

CEO, Crypto Coin Show

🎤

This Week on CCS

Neil Steinhardt — COO & Principal, Nexo US

Is America Finally Open for Crypto? Nexo’s COO on the US Comeback, Regulation & What’s Next

The US is back open for crypto business, and the companies that survived the chaos are making their move. Neil Steinhardt walks Ashton through what a genuinely compliant re-entry into the US looks like from the inside, why the GENIUS Act changes everything for institutional adoption, and what it means that the Bank of America CEO is now recommending 20% digital assets in a portfolio. If you want to understand where the US crypto industry is headed, this is the conversation.

The internet can’t tell humans from AI agents at scale — How can we identify them?

World (formerly Worldcoin) just launched a “full-stack proof of human” upgrade, and the timing couldn’t be more relevant. DC Builder breaks down how World ID works as the identity layer for an AI-driven internet, the AgentKit launch with Coinbase that puts human verification at the core of AI agent commerce, and why proof-of-personhood is one of the most important infrastructure problems in crypto right now. A must-watch if you’re thinking about identity, AI, or both.

Private Credit is a $1.7 Trillion Market — and It’s Broken. Here’s How to Fix It Onchain

Benjamin built QiDAO from $0 to $400M in TVL and started his career at Citi, and now he’s bringing private credit markets on-chain with principal protection backed by Franklin Templeton. He explains why Celsius and BlockFi collapsed (hint: the team was making credit decisions they had no business making), how Cap’s underwriter model fixes the structural flaw, and why the GENIUS Act is quietly making Cap more attractive to institutions by the week. The token announcement at the end is worth staying for.

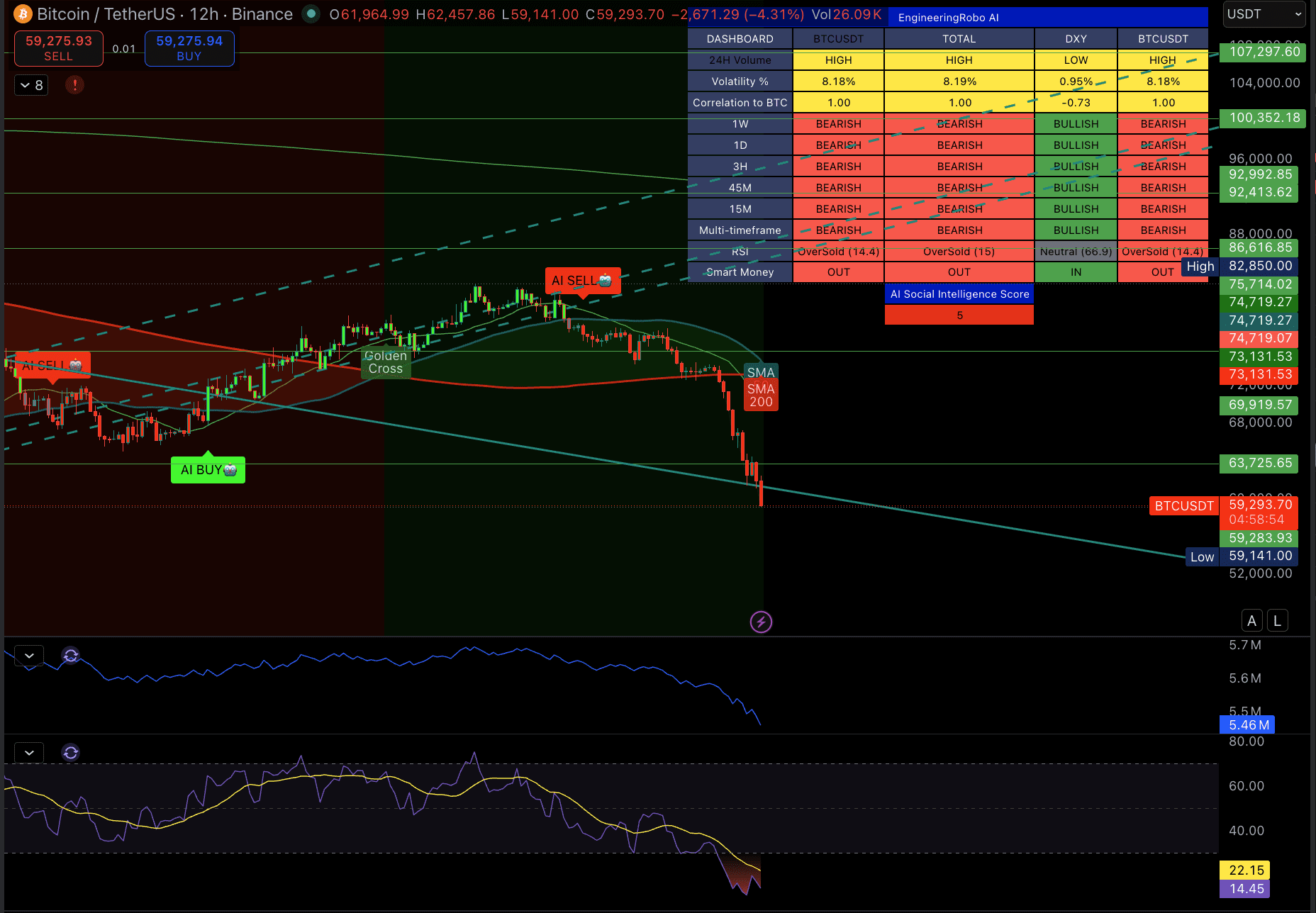

Bitcoin is trading at $59,293 on the 12-hour chart and the picture is about as clean as it gets — cleanly bearish across every timeframe. The 1W, 1D, 3H, 45M, and 15M are all red on EngineeringRobo. Multi-timeframe consensus: BEARISH. Smart Money is OUT. The RSI is sitting at 14.4 — one of the most oversold readings this cycle. Price knifed through both the SMA 50 and SMA 200 in a single move, with volume dropping on the way down, which tells you this is not panic selling finding a floor yet — it is a controlled bleed with sellers still in control.

The Death Cross is confirmed on the chart. The Golden Cross that gave bulls hope earlier in the cycle has been fully reversed. There is no timeframe on this chart showing buyers have any edge right now. The AI Social Intelligence Score is 5 out of 100, meaning sentiment from social channels is as negative as it gets.

My bias: BEARISH — oversold but no confirmation of reversal. The RSI is extreme enough that a mean-reversion bounce is possible at any session, but oversold does not mean bottom. There is no Smart Money flow, no timeframe flipping bullish, and no volume spike to suggest capitulation is complete.

What I’m watching

$59,141 is the session low and the immediate line. A close below it on the 12H with sustained volume opens the door toward $52,000, the next visible support. A reclaim of $63,725 on a close would be the first sign buyers are stepping in at scale. Until that happens, any bounce is a relief rally inside a downtrend.

Do not try to catch this falling knife without a confirmed close above structure. Manage your risk accordingly.

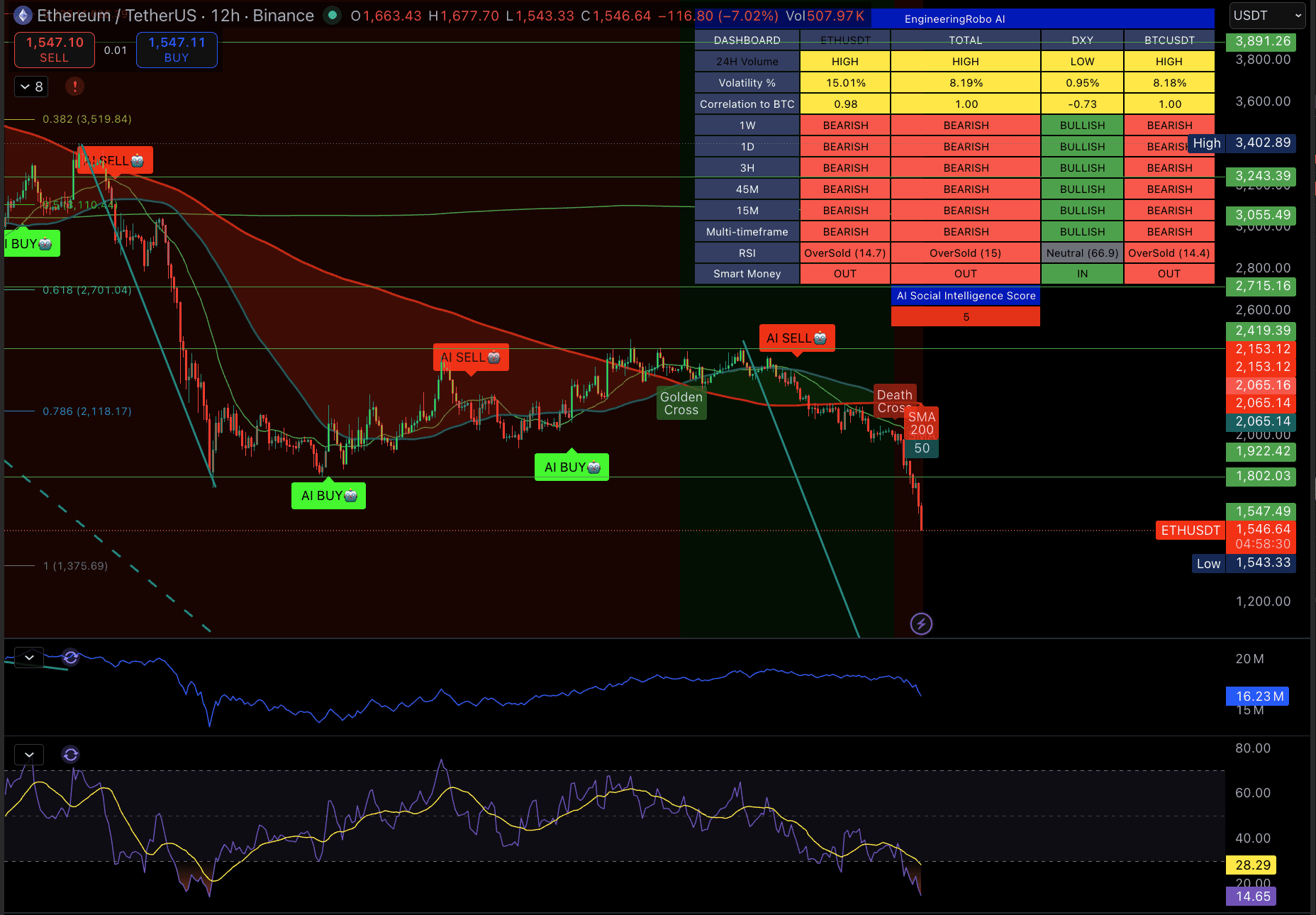

Ethereum is at $1,546 and it is not just following Bitcoin down — it is leading it lower. ETH is showing 15.01% volatility versus BTC’s 8.18%, and with a 0.98 correlation to Bitcoin, it is absorbing almost the full force of this move with added leverage to the downside. ETH is down 45% year to date versus BTC’s 32%. When the market sells off, ETH sells harder. That pattern is holding.

The Death Cross formed and has accelerated. Price is well below both the SMA 50 and SMA 200. All timeframes from 1W down to 15M are BEARISH on EngineeringRobo. RSI is at 14.7 — slightly more oversold than Bitcoin. Smart Money is OUT. The AI Social Intelligence Score is 5 out of 100. There is no timeframe or signal on this chart showing accumulation.

The Fibonacci structure is worth watching. The 0.786 level at $2,118 was the last meaningful support that gave way. Price is now in open air between that level and the 1.0 extension at $1,375. The session low is $1,543, which is sitting almost exactly on that 1.0 level. That is the line.

My bias: BEARISH — high volatility, no floor confirmed. ETH is the weaker asset in this environment. Until BTC stabilizes, ETH will not. The RSI is deep enough for a snapback but there is nothing in the signal data suggesting smart money is positioning for one.

What I’m watching

$1,543 is the session low and the Fibonacci 1.0 extension. A close below it on the 12H targets $1,375 as the next level of any significance. A reclaim of $1,802 would be the minimum needed to suggest the structure is beginning to repair.

The Original DePIN Protocol — Now with Its Own Layer One

10M+ nodes. A decade of proof-of-work. XYO’s Layer One is built for high-volume data, AI infrastructure, and real-world asset tokenization, with dual tokens $XYO and $XL1.

Filtered for signal, not noise. CCS articles linked where we’ve covered it in depth.

⭐⭐⭐

Zcash ($ZEC) crashes 50%+ as hidden privacy flaw wipes $5B from market cap.

A vulnerability in Zcash’s Orchard privacy pool, undetected for 4 years, allowed counterfeit ZEC to be generated. The bug was patched June 2, but whether fake coins were minted before the fix is impossible to verify. Traders are selling the uncertainty.

Crypto Clarity Act added to the Senate Legislative Calendar.

Now eligible for a full Senate vote — the next major piece of crypto legislation after the GENIUS Act, and the one that settles the securities vs. commodities question.

⭐⭐⭐

Visa, Mastercard, and Stripe launching a joint crypto stablecoin platform.

Three of the largest payment networks moving together on stablecoins while the market is in extreme fear. The buildout is not slowing down.

⭐⭐⭐

JPMorgan, Citi, and major US banks launching a tokenized deposit system to compete with crypto.

TradFi is not watching stablecoins take share — both a competitive threat and a validation signal.

Also this week

Bank of America appoints a top trading executive as global head of digital asset transformation.

Senior hire with a real mandate, not a press release title.

Over 50% of all Bitcoin in circulation now held at unrealized loss.

Historically coincides with late-stage capitulation, not the start of sustained declines.

Bitcoin down 32% YTD. Ethereum down 45%.

Neither is unprecedented. Both have recovered from worse.

$200 billion wiped from crypto market cap in 24 hours on June 3.

Not a slow bleed — a sharp flush.

In brief

US sanctions Iran’s largest crypto exchange, Nobitex.

Pattern Day Trader rule eliminated — $25K minimum gone.

US and Japan announce $1B partnership on AI, quantum, fusion, and biotech.

$60,000. That’s the line this week. Fear & Greed at 12, RSI at 17 — the data is flashing oversold. The fundamentals haven’t changed. The price has.

One question before you go.

Bitcoin is at $60K in extreme fear. Are you buying, holding, or waiting?

Washington is turning stablecoins into regulated payment instruments while trying to keep issuer-paid yield away from holders. That combination changesthe economics of digital dollars and puts the value of user balances up for grabs across the intermediary stack.

The GENIUS Act bars permitted payment stablecoin issuers and foreign payment stablecoin issuers from paying holders any form of interest or yield solely for holding, using, or retaining a payment stablecoin.

The FDIC’s April 7 proposal would turn parts of that law into operating standards for FDIC-supervised issuers, including reserves, redemption, capital, risk management, custody, pass-through insurance, and tokenized-deposit treatment.

That leaves a practical question for a market that reached roughly $320 billion in stablecoin supply in mid-April. If holders cannot receive direct issuer-paid yield, the value created by tokenized dollars still has to land somewhere.

The redistribution runs through the operating stack. The fight shifts to issuers, exchanges, wallets, custodians, banks, asset managers, card networks, and tokenized-deposit providers. They are the parties positioned to collect reserve income, distribution payments, custody fees, payment fees, settlement benefits, loyalty economics, or deposit economics.

The rulebook pushes yield into the plumbing

The stablecoin framework begins with reserves. GENIUS requires permitted issuers to maintain identifiable reserves backing outstanding payment stablecoins at least 1:1, with reserve categories that include cash, bank deposits, short-term Treasuries, certain repo arrangements, government money market funds, and limited tokenized reserve forms.

It also requires reserve disclosures and redemption policies, restricts reserve reuse, and calls for capital, liquidity, risk management, AML, and sanctions controls.

That makes compliant payment stablecoins look more like regulated cash-management products than free-form crypto instruments. Issuers can hold large pools of income-producing assets. At the same time, the statute blocks those issuers from paying stablecoin holders direct interest or yield merely for holding or using the token.

The economic trade-off looked uneven in the White House’s April 8 yield-prohibition note, which estimated a baseline $2.1 billion increase in bank lending from eliminating stablecoin yield, equal to a 0.02% lending effect, alongside an $800 million net welfare cost.

The same note said affiliate or third-party arrangements could remain unless CLARITY variants close that channel.

That caveat is where the post-CLARITY money map starts. A direct issuer-yield ban controls the issuer-holder relationship. It leaves open the harder economic question of how platforms, partners, payment apps, and bank structures treat the same value once it moves through distribution or product design.

CryptoSlate has already explored how the CLARITY fight is tied to stablecoin yield, regulatory control, market structure, and banking-sector pressure.

The commercial layer asks whether the law captures only the obvious form of yield, or also the ways a platform can turn stablecoin economics into something that feels like rewards, pricing power, or bundled financial service access.

The split runs through two layers. One side of the stack is statutory and prudential: reserve assets, redemption rights, capital standards, and supervision. The other side is commercial: distribution, wallet placement, exchange balances, merchant pricing, and settlement liquidity.

The policy debate becomes sharper when those layers are separated, because a ban at the issuer level can still leave value moving through the rest of the stack.

Issuers and exchanges already show the money trail

One clear example is USDC. Circle’s public filings describe a business built around reserve income, distribution costs, and partner economics. Its 2025 Form 10-K says Coinbase supports USDC usage across key products and that Circle makes payments to Coinbase tied principally to net reserve income from USDC.

The mechanics are more explicit in Circle’s S-1/A. The payment base is generated from reserves backing the stablecoin after management fees and other expenses.

Circle keeps an issuer portion, Circle and Coinbase receive allocations tied to stablecoins held in their own custodial products or managed wallets, and Coinbase receives 50% of the remaining payment base after approved participant payments.

That structure is the money map in miniature. A holder may see a stable dollar token. In the reserve and distribution structure, the reserve yield can move through issuer retention, platform-balance economics, ecosystem incentives, distribution agreements, and payments to approved participants.

Coinbase’s own filing shows why that channel is economically meaningful. Its 2025 Form 10-K reported stablecoin revenue as a business line and said a hypothetical 150 basis-point move in average rates applied to daily USDC reserve balances held by Circle would have affected stablecoin revenue by $540 million for 2025.

The point is specific: a large platform with distribution, balances, liquidity, and a deep issuer relationship can capture economics that the statute keeps away from holders in direct form.

Asset managers and custodial infrastructure sit on the same map. BlackRock’s Circle Reserve Fund showed a 3.60% seven-day SEC yield as of April 27, while Circle’s filing describes BlackRock as a preferred reserve-management partner and discusses the reserve-management relationship.

Stablecoin economics can accrue to the reserve stack, the manager, the custodian, the issuer, and the distributor before a user ever sees a token in a wallet.

Intermediary

Economic lane

User-facing form

Policy constraint

Issuer

Reserve income and issuance scale

Stable dollar token and redemption promise

Issuer-paid holder yield is barred under GENIUS

Exchange or wallet

Distribution payments, platform balances, loyalty incentives

Rewards, fee offsets, product access, liquidity

Third-party reward treatment remains the live CLARITY fork

Custodian or asset manager

Reserve management, custody, safekeeping

Operational trust and reserve transparency

FDIC and issuer rules shape permitted reserve and custody practices

Payment integration raises intermediation and resiliency questions

Bank or tokenized-deposit provider

Deposit economics and insured-bank balance-sheet activity

Deposit-like digital dollars with bank treatment

FDIC says qualifying tokenized deposits would be treated as deposits

Wallets and payment rails turn yield into product economics

The Fed’s April 8 FEDS Note gives the policy version of that table. It identifies complex intermediation chains, vertical integration, and accelerating retail adoption through wallet partnerships as structural stablecoin vulnerabilities.

It also points to integration with payment networks, banks, retail applications, broker-dealer funding, and card networks.

The Fed is studying a market where the issuer is only one node. Wallet providers, infrastructure firms, payment processors, brokers, banks, and card networks can all sit between the reserve asset and the user experience.

The company described instant crypto-to-stablecoin or fiat conversion, a 0.99% merchant transaction rate through July 31, 2026, support for more than 100 cryptocurrencies and wallets, and PYUSD rewards for funds held on PayPal at the time of the announcement.

That is a different economic shape from direct issuer yield. The holder sees payment access, merchant savings, wallet connectivity, or rewards attached to a platform. The platform can monetize conversion, distribution, customer balances, merchant pricing, and product stickiness.

Visa’s December 2025 USDC settlement launch shows the card-network version of the same intermediary lane. Visa said U.S. issuer and acquirer partners could settle VisaNet obligations in USDC, with Cross River and Lead Bank among initial banking participants.

It described more than $3.5 billion in annualized stablecoin settlement volume as of Nov. 30, 2025, and framed the product around seven-day settlement, liquidity timing, treasury automation, and operational resiliency.

Those benefits accrue through payment networks, issuing banks, acquiring banks, fintech partners, and corporate treasury operations. The user-facing return is payment access, faster settlement, or better pricing rather than issuer-paid yield.

That distinction is central to the policy fight. A yield ban can reduce the visible consumer return on a token while allowing platforms to compete through pricing, access, loyalty, and settlement benefits. The economics remain, but the claim on them becomes mediated by the platform relationship.

Banks gain leverage if the third-party channel closes

The banking lobby understands that channel. The Bank Policy Institute argued in August 2025 that GENIUS’s issuer-yield prohibition could be undermined if exchanges, affiliates, or distribution partners are still able to pay interest indirectly on stablecoins.

BPI framed that as a loophole that could increase deposit-flight risk and weaken credit creation.

Crypto trade groups answered from the other side. Their August 2025 response argued that third-party rewards are competitive consumer benefits rather than evasion of the statute.

The dispute determines whether the post-GENIUS stablecoin market becomes a platform-rewards market or a bank-protected payments market.

The FDIC proposal adds the second bank lane. It says tokenized deposits that satisfy the statutory definition of deposit would be treated no differently from other deposits under the Federal Deposit Insurance Act.

That gives banks a cleaner argument if stablecoin rewards face stricter limits: deposit tokens can keep the economics inside the banking perimeter, where interest, insurance, and lending relationships already have a legal home.

CLARITY’s market-structure section-by-section summary points to another intermediary layer. Digital commodity exchanges, brokers, and dealers would face registration, listing, custody, segregation, disclosure, and customer-election requirements.

Customers could elect into blockchain services such as staking under conditions, while access to the exchange could not be conditioned on that election.

Those provisions reinforce the same intermediary shift by moving economic activity into supervised channels. The contested issue is who owns distribution, customer balances, wallet access, custody, settlement, and optional services.

As of press time, USDT was around $189.71 billion in market capitalization and USDC around $77.63 billion.

CryptoSlate rankings also showed USDe around $3.79 billion, PYUSD around $3.42 billion, and RLUSD around $1.6 billion. That scale means the issuer-yield rule lands first on the largest payment-stablecoin rails.

The next test is the definition of indirect yield. If lawmakers and regulators allow third-party rewards, the advantage sits with platforms that own users, balances, payments, and distribution. If they limit those arrangements, banks and tokenized-deposit providers get a stronger path to keep digital-dollar returns inside deposit products.

The emerging U.S. framework decides whether stablecoin holders can receive yield and how much of the economics of digital dollars becomes visible to users. The rest is absorbed by the intermediaries that move, custody, package, and settle those dollars.

For most of its life, crypto lived outside the financial system. If you wanted to move dollars in or out of an exchange, that money still had to pass through a regular bank somewhere along the way. Most people assumed it would stay that way until Washington finally decided how to regulate it.

But that assumption is now breaking down. In March 2026, a regional Federal Reserve bank approved a limited account for Kraken, the first time a crypto exchange has ever been allowed to plug directly into the US central bank’s payment system. More approvals could follow, and the GENIUS Act, passed last year, has cleared a path for ordinary banks to start issuing their own digital dollars.

None of this needed a sweeping “crypto law”: it was a series of smaller, technical decisions that have added up and changed the picture entirely.

Crypto may not be waiting for permission anymore. It may already be finding a way in.

What a “backdoor into the system” actually means

The US financial system runs on a set of payment networks operated by the Federal Reserve. Banks use them to move money between each other, settle transactions at the end of the day, and tap dollar liquidity when they need it. The most important, called Fedwire, moves trillions of dollars between banks every single day.

To use those networks, an institution needs an account at the Fed, which was historically reserved for licensed banks. Everyone else had to rent access by going through a partner bank that already had one.

That’s what just changed. Kraken’s banking unit now has its own direct line into the Fed’s payment system, without routing dollars through another bank first. The account is limited, which means it won’t have interest on reserves or access to the Fed’s emergency lending, but it lets Kraken settle its own dollar transactions on the same infrastructure banks use.

Think of the difference this way: instead of using a third-party app to talk to your bank, you have your own connection to the bank’s back end. Faster, cheaper, and no longer dependent on a middleman that can say no.

For years, US crypto policy has moved slowly, pulled between agencies that didn’t agree on the basics. At the same time, demand for crypto services from big institutional investors hasn’t gone away. They want cleaner, regulated ways to touch the asset class.

So the system is adapting practically, not politically.

The GENIUS Act gave digital dollars their first real federal rulebook and effectively invited regulated banks into the market. Regulators began handing out special charters that let nonbank firms like Circle operate with bank-like privileges.

The Fed opened a public comment period on a lighter-weight account designed for payment-focused firms. Wyoming’s crypto-friendly bank charter, once treated as an experimental oddity, became the legal vehicle that carried Kraken through the door.

All of this means that your bank’s exposure to digital assets is going up, either through partners, products, or its own tokens. Citi has said it’s targeting a 2026 launch of crypto custody. A group of major global banks, including JPMorgan, Bank of America, and Goldman Sachs, has explored a jointly-backed digital dollar. Even if you never buy crypto, it will now sit on the edges of the account you already have.

This comes with quite a few risks for markets, though. When the pipes between crypto and traditional finance get wider and shorter, money moves faster in both directions, and so do shocks.

For crypto, direct access to payment systems is a stamp of legitimacy that would have been unthinkable a few years ago. But it also means it loses the “outside the system” identity that defined it, and takes on some of the same responsibilities.

The more connected crypto becomes, the less isolated its risks are.

The real tension: stability or contagion for crypto?

One view (call it the normalization case) is that pulling crypto inside the regulated perimeter makes everyone safer. Companies with direct Fed access have to meet stricter standards, and reserves get easier to monitor. This is a net positive for users, as they end up with fewer opaque middlemen between their dollars and the exchange. When seen through this lens, integration reduces risk rather than creating it.

The other view is hard to ignore, as the scares from the 2008 financial crisis are still fresh for many.

The US banking lobby reacted to the Kraken decision by warning that lightly regulated companies like this with direct access to the payment system introduce all kinds of money-laundering and operational risks. However, they would also open a Pandora’s box of new risks: in a panic, money could actually flood into these new accounts, draining deposits from the community banks and credit unions that fund the real economy.

The Bank Policy Institute, representing the country’s largest banks, said the approval happened before the Fed Board had even finished writing its own rulebook for these accounts.

The question underneath this fight is pretty simple: if crypto becomes part of the system, does it make the system stronger or more fragile?

Financial crises are rarely about the risk everyone is watching. They’re a result of the connections no one modeled, and many believe that the new direct connection between crypto markets and the Fed’s payment rails is exactly that kind of linkage.

The subtle part

Part of what makes a huge shift like this hard to see is that nobody is announcing it as one.

There’s no press conference where “crypto joins the banking system,” because there doesn’t need to be. A regional Fed approval here, a stablecoin rulebook there, and a charter granted to a firm most people have never heard of.

Each of these items is boring on its own terms, which is why they clear without the kind of political fight that most comprehensive crypto laws have been stuck in for years.

More crypto firms will almost certainly follow Kraken once the Fed finalizes its lighter-weight account framework, and the approvals will be granted one at a time, in different Federal Reserve districts, with conditions that take pages of legal language to unpack.

Big banks will keep rolling out custody services and their own digital dollars as ordinary product launches, not ideological statements, while the Kraken cybersecurity incident this spring (an extortion attempt built around insider access) hands the banking lobby exactly the kind of material it needs to argue that lightly regulated firms shouldn’t be sitting on the same rails as JPMorgan.

A comprehensive crypto market-structure law may still pass, and probably will eventually, but by the time it does, the thing it’s meant to govern will already have been built around it, and the interesting question will no longer be what the rules say but how much of the system has stopped needing them.

Stablecoin tax treatment in the U.S. is at the center of a new legislative push to exempt qualifying daily transactions involving regulated payment stablecoins from tax.

The latest version of the PARITY Act would stop gain or loss recognition on certain stablecoin sales unless a taxpayer’s basis falls below 99% of the token’s redemption value, marking a direct attempt to treat routine stablecoin spending more like cash payments. The proposal also revises rules on staking rewards and digital asset wash sales, while lawmakers in Washington continue to debate broader crypto legislation.

Stablecoin payments provision removes small transaction tax burden

The bill is grounded on the past discussion drafts issued in December 2025 and on March 26, 2026. The earlier proposal recommended a $200 limit on payments made with regulated payment stablecoins, as in the de minimis section.

That structure was altered in the March 2026 draft. Instead of using a de minimis criterion, the text states that no gain or loss would be recognized on the sale of a regulated payment stablecoin unless the taxpayer’s basis in that stablecoin is less than 99% of its redemption value.

Another standard eliminated by the draft was the previous $200 standard. In addition, it created a deemed basis of $1 for exchanges, which the text treats separately from the stablecoin’s sales. That development solves one of the long-term problems of crypto users. The current tax treatment states that any payment made using USDC or USDT can result in a taxable event, even when the change in value is minimal.

Meanwhile, the bill creates a distinction between passive staking and other activities, such as trading. It would also enable taxpayers to decide when to record staking rewards, upon receipt or after a deferral period of not more than 5 years, as indicated in the material. To qualify under the proposed stablecoin treatment, the asset must be regulated under the GENIUS Act and remain within 1% of its $1 peg.

Stablecoin debate comes alongside ongoing crypto policy pressure

The tax proposal comes following pressure on other digital asset legislation, including the CLARITY Act. Senator Cynthia Lummis recently pointed out that the bill could remain stalled until 2030 if the Senate fails to act before the 2026 election cycle.

At the same time, as reported by Cryptopolitan, the Trump White House has pushed back on concerns over stablecoin yield provisions. A Council of Economic Advisors report dated April 8 said the effect on bank lending would be limited, estimating a 0.02% increase, or about $2.1 billion.

The same report said community banks would face about $500 million in additional obligations, equal to a 0.026% increase over current lending activity. It concluded that banning yield would provide little protection for bank lending while giving up consumer benefits tied to competitive returns on stablecoin holdings.

Your bank is using your money. You’re getting the scraps. Watch our free video on becoming your own bank

The U.S. regulatory landscape for digital assets is undergoing its most significant structural transformation yet, with three major legislative and regulatory developments converging to create what many industry observers describe as a genuine federal framework for stablecoin issuance and institutional custody. Blockchain security firm CertiK has released analysis of this convergence, arguing that recent moves by Congress and the SEC fundamentally alter the conditions under which crypto-focused and traditional financial institutions can operate at scale.

A Federal Framework Takes Shape

For years, the American crypto sector operated within a patchwork of state-level regulations and fragmented federal oversight. That dynamic has shifted markedly with three developments: the GENIUS Act, signed into law in July; the CLARITY Act, which has cleared the House and awaits Senate action; and the SEC’s reversal of Staff Accounting Bulletin 121. Each addresses a specific barrier to institutional participation in digital asset markets.

The GENIUS Act establishes the first comprehensive federal licensing structure for entities issuing dollar-backed stablecoins. Rather than allowing issuers to navigate differing state requirements, the legislation mandates federal approval and imposes uniform standards for reserve assets and redemption mechanisms. This represents a fundamental departure from the previous regulatory environment, where stablecoin operators faced legal uncertainty and varying compliance obligations across jurisdictions.

This report reveals a pivotal shift in how digital assets are regulated and supervised across the United States. By analyzing federal legislation and market structure proposals, as well as state-level obligations, the research highlights the operational demands that digital asset firms must meet in the coming years.

— Kayvon Hosseini, Head of Advisory, CertiK

The CLARITY Act addresses jurisdictional ambiguity between two primary regulators. By clarifying the boundary between SEC and CFTC authority, the legislation expands CFTC oversight of digital commodity markets while defining the SEC’s domain over digital securities. This delineation removes a source of regulatory confusion that has complicated compliance efforts for platforms and service providers.

Key Development

The GENIUS Act introduces the first federal stablecoin licensing regime, requiring approval before issuing dollar-backed tokens and establishing uniform reserve and redemption standards across all U.S. jurisdictions.

Custody and Capital Requirements

One of the most significant barriers to traditional financial institutions entering digital asset custody has been removed through the SEC’s reversal of SAB 121. This accounting bulletin previously required banks to report crypto holdings at fair value on their balance sheets, creating unfavorable capital treatment that discouraged participation.

The reversal eliminates this accounting friction. Traditional custodians can now offer digital asset safekeeping services without the same balance sheet complications that previously made such offerings economically unattractive. This opens pathways for established financial institutions to build custody infrastructure at institutional scale, potentially accelerating the institutional adoption of digital assets.

Together, these three developments address interconnected challenges: regulatory clarity for stablecoin issuers, jurisdictional definition for regulators, and economic feasibility for custodians. The convergence suggests a deliberate policy shift toward establishing conditions conducive to institutional-grade digital asset infrastructure.

Market Implications

What This Means for Market Participants

CertiK’s analysis frames these developments as establishing “operational demands” for digital asset firms seeking to participate in the U.S. market. For established crypto companies, this means adapting internal compliance and operational structures to meet federal standards. For traditional financial institutions, it signals reduced regulatory and capital barriers to entry.

The framework is not without complexity. While the GENIUS Act and CLARITY Act establish federal parameters, state-level regulations remain relevant in certain contexts. Digital asset providers must navigate both federal and state obligations as they build compliant operating models. This dual compliance structure—federal baseline with state-specific requirements—creates what regulators might characterize as comprehensive oversight, though industry observers note it requires sophisticated legal and operational infrastructure.

For Bitcoin, Ethereum, and other digital commodities, the CLARITY Act’s expansion of CFTC authority provides clearer regulatory treatment as derivatives underlying futures and other regulated products. This clarity may reduce legal uncertainty for platforms offering these instruments.

The convergence of these three developments establishes the most coherent federal framework the industry has yet seen for operating payment tokens and managing digital assets at scale.

— CertiK U.S. Digital Asset Policy Report

Industry Context and Historical Perspective

The digital asset industry has experienced rapid growth over the past decade, with total cryptocurrency market capitalization reaching multi-trillion dollar valuations. However, this expansion has consistently outpaced regulatory development, creating friction between innovation and compliance. Stablecoin adoption, in particular, accelerated dramatically following the 2020 financial crisis, with entities like Circle, Paxos, and traditional financial institutions exploring tokenized payment systems. This growth prompted Congressional scrutiny, ultimately leading to the legislative proposals now taking shape.

The current regulatory convergence reflects lessons learned from earlier policy missteps and regulatory fragmentation. Federal agencies—including the Federal Reserve, OCC, FDIC, and SEC—previously issued conflicting guidance on crypto custody and stablecoin treatment. Banks seeking to serve the digital asset sector faced unclear capital requirements, conflicting supervisory expectations, and legal uncertainty. This environment deterred many large financial institutions from meaningful participation, limiting institutional capital flowing into digital asset infrastructure.

CertiK, founded in 2018, has positioned itself as a bridge between the blockchain development community and institutional stakeholders seeking reliable analysis of regulatory and security developments. The firm’s policy research extends beyond security audits into the operational and compliance dimensions affecting institutional participation. This analysis reflects growing demand from traditional institutions for clear frameworks enabling their market participation.

Timeline and Implementation

The GENIUS Act is already law, meaning stablecoin issuers must begin adapting to its requirements. The CLARITY Act remains in the legislative process, pending Senate consideration after House passage. The SEC’s SAB 121 reversal has already taken effect, allowing custodians to immediately adjust their business models.

This staggered timeline means digital asset firms face immediate compliance needs alongside ongoing legislative uncertainty. Those preparing for GENIUS Act compliance should do so now, while monitoring potential Senate amendments to the CLARITY Act that could affect regulatory jurisdiction assignments.

Pending Action

The CLARITY Act has passed the House and awaits Senate review. This legislation could significantly expand CFTC jurisdiction over digital commodity markets, so developments in the Senate warrant close monitoring by industry participants.

Market Structure and Competitive Implications

These regulatory developments carry significant competitive implications. Established financial institutions with substantial compliance and legal infrastructure may find it easier to meet federal stablecoin licensing requirements compared to younger crypto companies operating with leaner organizational structures. Conversely, native blockchain firms with deep technical expertise may adapt more rapidly to operational demands than traditional banks building new digital asset divisions.

The custody framework created by SAB 121’s reversal particularly benefits large custodians and banking institutions. Entities like Fidelity, Coinbase Custody, and legacy financial institutions can now offer services with clearer capital treatment. This may consolidate custody services among larger, well-capitalized institutions rather than distributing it across smaller specialized providers.

For stablecoin issuers, federal licensing creates uniform operating conditions across states. This removes the competitive advantage previously held by issuers operating in favorable state jurisdictions and instead incentivizes competition based on operational efficiency, reserve management, and customer service rather than regulatory arbitrage.

CertiK’s policy report positions itself as a reference tool for institutions navigating this evolving environment. For financial institutions considering custody offerings, digital asset platforms assessing compliance requirements, and policymakers designing supporting infrastructure, the analysis provides a structured examination of how federal and state rules now intersect in the digital asset space.

Whether these legislative and regulatory moves ultimately catalyze institutional participation at the scale some expect remains a forward-looking question. What is clear is that the regulatory environment has become materially more defined than it was twelve months ago. That clarity alone may reduce hesitation among institutions previously deterred by legal and capital barriers.

Looking Ahead: Sustainability and Evolution

The U.S. digital asset regulatory landscape has historically moved in fits and starts, with periods of clarity followed by renewed confusion. The current convergence of legislative and regulatory action suggests a more sustained policy consensus around institutional participation and consumer protection. Whether this represents a durable shift depends on continued Congressional engagement and regulatory agency coordination as market conditions evolve.

Future regulatory development will likely address emerging issues including cross-border stablecoin transactions, decentralized finance supervision, and the intersection of digital assets with traditional securities markets. The framework established through these three developments provides a foundation upon which more specialized rules will likely be built over the coming years.

Get weekly blockchain insights via the CCS Insider newsletter.

Trump Media and Technology Group announced that it had acquired $2 billion worth of Bitcoin and Bitcoin-related securities on July 21, 2025. This was just three days after President Trump signed the GENIUS Act.

The fact that this massive Bitcoin investment was kept hidden until after the law passed appeared to be part of a larger plan rather than a coincidence to critics.

The question on their minds is: Did Trump use his presidential power to change the rules in favor of crypto, only to reveal afterward that he had a massive personal stake in it?

In other words, did he write the playbook and then make the first move once the game was rigged in his favor?

This question runs deep because the line between serving the country and personal interests gets blurred. It becomes especially concerning when a sitting president owns over half of a company that suddenly announces billions in crypto investments right after new laws are passed.

It’s now less about one company or one law and more about how power, money, and policy seem to move together in ways that leave regular people wondering if the system is fair.

The Genius Act aims to make Bitcoin safer for investors

President Donald Trump handed both investors and crypto companies a powerful signal that the federal government now officially supports the growth of digital assets. He did so when he signed the GENIUS Act into law on July 18, 2025.

It requires companies that want to issue payment stablecoins to hold 100% reserves in cash or short-term Treasuries. This means a real, safe, and liquid asset must back every digital dollar they create.

Large Stablecoin issuers must also give regulators and the public insights into whether these companies operate safely and honestly. They must publish monthly public disclosures about their reserves and submit them to independent annual audits.

Furthermore, the new law prioritizes customer protection by banning misleading marketing. This includes claims that stablecoins are backed by the US government, federally insured, or legally recognized as currency. And users will be paid back first, ahead of any other creditors, if a company becomes insolvent.

But most importantly, the law prevents federal government officials, including the president, from issuing or promoting stablecoins while holding public office.

The US government effectively signaled that it is ready to treat crypto as a permanent part of its financial future by officially welcoming one major digital asset into the regulatory fold. The infrastructure built under this act could soon provide legal clarity, financial bridges, and regulatory credibility to support other digital currencies, including Bitcoin.

Trump’s Bitcoin stash appears after laws change

President Donald Trump signed the GENIUS Act into law on July 18, 2025. Just three days later, on July 21, his privately linked company that owns the social media platform Truth Social made a major announcement. Trump Media and Technology Group revealed it had purchased approximately $2 billion worth of Bitcoin and Bitcoin-related financial products.

This tightly packed timeline has drawn intense public scrutiny. It raises questions about Trump’s intentions and the possible use of public power to protect and grow his private wealth.

Observers suspect the events were strategically planned to work together. The company had hinted as early as May that it was exploring a crypto treasury strategy and raising capital for future investments in digital assets.

But until after the legal and political environment had shifted in its favor, it never disclosed the actual purchase of Bitcoin, nor did it reveal the size of its crypto plans.

Critics suspect the president rewrote the game’s rules and then used that new structure to justify and reveal a high-stakes financial move that directly benefits him. They believe this because the company intentionally withheld the news.

This new Bitcoin purchase immediately increased the value of a company that Trump personally controls and profits from because he holds a 53% ownership stake in Trump Media. His move raises serious ethical questions about the role of the presidency in shaping financial markets. This is especially concerning when the person writing the policy stands to benefit financially from the outcome.

New rules help Trump grow his wealth

Trump’s sons, Donald Trump Jr. and Eric Trump, help run World Liberty Financial, another Trump-linked crypto firm. The company has launched its stablecoin, formed global partnerships, and attracted hundreds of millions in foreign investment.

Reports show the firm deals with foreign governments, blockchain billionaires, and companies with past legal troubles. This includes Binance, whose founder CZ pleaded guilty to money laundering in 2023 but remains closely tied to Trump-linked crypto ventures.

In one of the most controversial deals, World Liberty Financial helped facilitate a $2 billion transaction using its USD1 stablecoin. This occurred just weeks before Trump signed the GENIUS Act. Critics say these overlapping business interests, with his family so deeply involved, show a deliberate pattern of using public power to support private wealth.

Traditionally, presidents from both parties understood that public trust depends on drawing a clear line between the Oval Office and the boardroom. As a result, they placed their business holdings into blind trusts. This eliminated the appearance of personal gain from public policy by giving independent managers full control of their assets.

Yet, Trump rejected this tradition during his first term and still maintained direct financial connections with his companies after returning to office in 2025.

Ethics experts, government watchdog groups, and members of Congress say that even if no specific law was violated, Trump’s continued control over companies involved in crypto represents a serious breach of ethical norms. This concern is heightened because he also passed laws that benefit the industry. They point out that the president should not make decisions that boost the value of companies he owns or that his family runs.

Many experts warn that legality isn’t the only issue because Trump and his allies argue there’s nothing illegal about a president owning stock or having business interests as long as he discloses them. They emphasize that disclosure alone doesn’t address all ethical concerns. When the president personally profits from laws he helped create, it raises serious questions about fairness, transparency, and honest governance.

Trump Media says Bitcoin protects its future

Trump Media and Technology Group framed its investment as a bold move for “financial freedom” and a necessary step to protect itself from “ongoing banking discrimination.”

The company’s official statement explained that traditional banks and financial institutions forced it to seek alternative paths that wouldn’t rely on politically biased gatekeepers. They did this by targeting Trump-linked businesses with unfair treatment, freezing accounts, and refusing to process transactions.

The company said it was taking a stand for economic independence, freedom of speech, and secure access to financial systems. It aimed to achieve this by moving a significant portion of its treasury into Bitcoin, beyond the reach of government pressure or Wall Street politics.

Trump Media’s financial records show that the company has faced serious problems since it began. It has struggled to earn steady advertising income and grow its user base. These challenges are especially clear on its main platform, Truth Social, which has failed to attract enough users and advertisers to compete with bigger social media companies.

Because of these ongoing problems, the company’s quarterly reports continue to show heavy losses. Its operating costs are much higher than the money it makes. On top of that, its stock price has dropped sharply since the early excitement, which has made its already weak financial situation even worse.

In the end, the company’s financial problems remain the same. Trump Media still makes very little money, its debt keeps growing, and its future is unclear. Now that so much of its value depends on Bitcoin, one of the most unpredictable assets in the world, the company is even more at risk than before.

KEY Difference Wire helps crypto brands break through and dominate headlines fast

US Congresswoman Marjorie Taylor Greene has warned starkly against the newly introduced GENIUS Act, which she fears will push a forced agenda in the US for a state-backed Central Bank Digital Currency (CBDC).

Greene says that despite being pitched as a stablecoin regulatory framework, the bill includes features and control features you would find in a CBDC.

“This bill regulates stablecoins and provides for the backdoor Centralized Bank Digital Currency.” Greene wrote on X.

The GENIUS Act sought legal clarity around issuing stablecoins and operating them in the US. Yet Greene and others fear that under the hood, it effectively enables sweeping financial surveillance and control like state-run digital currency.

Industry voices alarm over privacy risks

There has been fierce support in the broader cryptonetworks community for Greene’s criticism. Her concerns have not gone unheard, with several other leaders and industry experts voicing similar fears, citing that the proposed GENIUS Act threatens to impact the underlying ethos of decentralization in digital currency negatively.

Economist and Bitcoin maximalist Saifedean Ammous, author of The Bitcoin Standard, said in a recent podcast that the US dollar is already, in many ways, a digital currency. He argued that whether in physical form or through an app, the dollar functions as a digital token of the state, monitored and tracked by the government.

Jean Rausis, co-founder of Smardex, said governments understand that controlling stablecoins means controlling financial transactions. He added that with centralized systems, authorities can freeze assets, reverse payments, and track spending, making stablecoins nearly identical to CBDCs.

This sentiment represents a shared skepticism in crypto about any regulatory framework that would put stablecoins under centralized control. Privacy and financial autonomy are the beginnings of a bridge too far. For many of these people, the concepts of privacy and financial autonomy are simply non-negotiable, and any bill that threatens to interfere with these principles is met with outright defiance.

GENIUS Act spurs concerns over financial surveillance

The GENIUS Act has undergone several revisions since its initial release, with the latest major revision being in March 2025. These developments have introduced more stringent AML obligations, “KYC” requirements, and sanctions compliance requirements. And though they have been justified as necessary shields against criminal abuse, critics say they amount to invasive financial surveillance.

Stablecoin issuers would be required to collect and share customer information and track all transactions; they would sometimes need to suspend payments if regulators tell them to, without passing information on why the transactions are occurring. For many in crypto land, this is not one inch closer to authoritarian repression, but a horrifying mile.

This is all fine and good until 10 years later, issuers are required to keep some of that money in regulated banks and go through draconian AML checks, and the government freezes or confiscates the funds like they would any other bank account.

The problem isn’t limited to the United States. The CBDCs are actively being rolled out in other countries, such as China and the EU.

US crypto proponents fear the GENIUS Act, in pretending to support innovation, could take America down that same road, only low-key.

Your crypto news deserves attention – KEY Difference Wire puts you on 250+ top sites

The US House of Representatives has designated July 14 as “Crypto Week,” marking a day to recognize and honor progress, innovation, and excellence in digital assets.

House Speaker Mike Johnson, Financial Services Committee Chair French Hill, and Agriculture Committee Chair GT Thompson announced the news Thursday, positioning the move as part of a wider Republican plan to further what could be President Donald Trump’s digital finance agenda.

Major bills are expected to be debated and voted on by lawmakers during Crypto Week. Some of those include bills targeting stablecoins, which is a more sweeping bill on the structure of the cryptocurrency markets, among others.

“House Republicans are taking decisive steps to deliver the full scope of President Trump’s digital assets and cryptocurrency agenda,” Johnson said in the statement. He called the upcoming legislative session the first bold step in positioning the United States to lead the world in the digital economy.

House targets August deadline for stablecoin bill

The stablecoin bill will be the top priority for Crypto Week. Although the House had previously pushed its version, known as the STABLE Act, lawmakers are turning their attention to the Senate’s version, titled the GENIUS Act, which has already been approved.

The House had shifted its focus, likely to speed up the process, noting that Trump had publicly stated he wanted a stablecoin bill on his desk by August.

The GENIUS Act also includes tight rules, such as mandating that US dollars or comparable liquid assets must fully back stablecoins.

It requires stablecoin issuers with market values exceeding $50 billion to perform annual audits and sets specific standards for firms or companies domiciled overseas. The House’s previous version had key differences, such as tolerating state-level regulatory structures or treating foreign issuers differently.

Still, Republican leaders seem willing to take the Senate version to meet the tight timetable. The STABLE Act advanced through the House Financial Services Committee in May but has not been brought to a full vote. Choosing the GENIUS Act may expedite negotiations and bypass a protracted legislative ping-pong.

President Trump’s rising interest in crypto regulation has emphasized the urgency. He and his administration want to stabilize the US stablecoin market as part of a campaign to claw back financial innovation from competitors abroad.

Lawmakers clarify crypto oversight in market structure bill

A second key piece of legislation on the Crypto Week docket is the Digital Asset Market Clarity Act, also known as the Clarity Act. This legislation hopes to create regulatory clarity between the agencies by defining the roles of the SEC and the Commodity Futures Trading Commission.

The rules would force firms that issue and manage digital currencies to disclose critical financial information to consumers and keep customer funds separate from corporate assets. Such measures are crucial in light of major blow-ups, such as the FTX scandal, which revealed oversight gaps.

Republicans say an unclear legal framework stifles US innovation and drives entrepreneurs overseas. French Hill, who helped to shepherd the bill, called it a sensible roadmap that strikes the right balance between innovation and investor protection.

But not everybody agrees. District Democrats have expressed skepticism, particularly considering Trump’s close relationship with the digital asset world. Trump and his family have raked in around $620 million from crypto initiatives such as launching memecoins carrying the TRUMP and MELANIA names, and a decentralized finance effort known as World Liberty Financial, according to a recent report by Bloomberg.

The final piece of legislation expected during Crypto Week comes from House Majority Whip Tom Emmer. His bill seeks to ban the Federal Reserve from launching a retail-facing CBDC, arguing that such a currency would seriously threaten financial privacy and civil liberties.

Emmer has positioned the bill as a defense against government overreach. He warned that allowing the Fed to issue a digital dollar directly to consumers would open the door to surveillance and control over personal spending habits.

Cryptopolitan Academy: Want to grow your money in 2025? Learn how to do it with DeFi in our upcoming webclass. Save Your Spot