Bitcoin’s US demand signal is still struggling to recover, with the Coinbase Premium Index reportedly sitting in negative territory for eight straight weeks. The run began on May 6, 2026, and now marks the longest continuous negative stretch for the metric in more than a year.

TL;DR

The Coinbase Premium Index has reportedly been negative since May 6.

That marks an eight-week weak stretch for the US Bitcoin demand signal.

The index compares Bitcoin pricing on Coinbase Pro with Binance.

A negative reading suggests weaker relative buying pressure from Coinbase-linked traders, not a collapse in global volume.

The Coinbase Premium Index is one of those market indicators that can sound more complicated than it really is. In simple terms, it tracks the gap between the Bitcoin price on Coinbase Pro and the price on Binance. Because Coinbase is closely associated with US institutions and retail users, the premium is often used as a rough proxy for US spot demand.

What a negative premium actually means

When Bitcoin trades at a premium on Coinbase, traders often interpret that as a sign that US buyers are paying slightly more than global buyers. When the premium turns negative, it suggests that Coinbase-linked demand is weaker than demand on other major venues.

That does not mean nobody in the US is buying Bitcoin. It also does not mean global trading volume has vanished. The metric is relative. It says more about where demand is stronger or weaker than it does about absolute market size.

Still, an eight-week negative run is difficult to ignore. Short dips can be noise. A two-month stretch points to a more persistent imbalance in the market.

Why this matters after a difficult June

The timing is important because Bitcoin has already been dealing with pressure from other parts of the market. Spot Bitcoin ETFs saw heavy June outflows, price action weakened, and traders became more defensive around risk assets. A negative Coinbase premium adds another signal that the US side of the market has not been leading the recovery.

For bulls, the ideal setup would be a return to positive ETF flows and a Coinbase premium that moves back above zero. That would suggest US buyers are stepping back in rather than leaving the rebound to offshore or global venues. Until that happens, rallies may continue to look vulnerable to fading.

Not bearish on its own, but hard to ignore

No single metric should be treated as a full market thesis. The Coinbase Premium Index can move quickly, and it is best read alongside ETF flows, exchange reserves, derivatives positioning, and spot volume. But it remains useful because it captures a part of the Bitcoin market that traders care about deeply: whether US demand is leading or lagging.

Right now, the signal is lagging. That does not guarantee further downside, but it does tell traders that Bitcoin’s next leg higher likely needs stronger participation from Coinbase-linked buyers. Without that, the market may continue to feel like it is recovering on thinner ground.

This report is based on information from CryptoQuant.

This article was written by the News Desk and edited by Samuel Rae.

Bitcoin’s quantum-risk debate is no longer just a theoretical developer conversation.

TL;DR

A Coinbase-linked quantum-risk discussion has put Bitcoin address reuse and legacy cold wallets back in focus.

The issue is not an immediate break of Bitcoin, but a long-term custody and migration problem.

Large holders, exchanges, and institutions have the strongest reason to care because old exposed public keys could become future risk points.

Why Address Reuse Matters

A Coinbase-linked advisory discussion has reportedly flagged address reuse and legacy Bitcoin wallets as long-term exposure points if quantum computing advances far enough to threaten today’s signature assumptions. That does not mean Bitcoin is suddenly unsafe. It does mean custody practices that look acceptable today may need a migration plan before the risk becomes urgent.

The most important word here is “future.” This is not a panic story. It is a preparation story.

Bitcoin users are generally encouraged not to reuse addresses. The reason is privacy, but there is also a security angle.

When coins are spent from an address, the public key becomes visible on-chain. Under today’s cryptographic assumptions, that does not create an immediate problem. But in a future where powerful quantum computers can attack certain public-key systems, exposed public keys could become more sensitive.

That is why old wallets and reused addresses matter. They may represent a class of coins that would require special attention in a future post-quantum migration.

This is especially important for large custodians and exchanges. A retail wallet with a small balance is one thing. A cold wallet holding large institutional balances is another.

The Institutional Custody Problem

Bitcoin is becoming more institutional every year.

Banks, ETFs, custodians, public companies, and large asset managers are all part of the market now. That makes long-term custody assumptions more important. Institutions do not just need Bitcoin to be secure today. They need confidence that their custody model can adapt over time.

That is where quantum migration becomes complicated.

If the ecosystem eventually needs to move to quantum-resistant signatures, users, exchanges, wallets, developers, and custodians will all need clear paths. The harder question is what happens to dormant coins, old addresses, and funds controlled by entities that no longer exist or cannot respond.

That is not an easy problem to solve quickly.

Not Immediate, But Not Ignorable

The mistake would be to frame quantum risk as either an emergency or nothing at all.

It is not an emergency today. Bitcoin is not being broken by quantum computers in the current market. But it is also not a topic serious custodians can ignore forever.

Good security planning happens before a threat becomes active. That is why these discussions matter now. If the industry waits until quantum risk becomes obvious, migration will be more stressful, more political, and more technically difficult.

What The Market Should Take From This

For traders, this is unlikely to move Bitcoin’s price today. It is not like ETF flows, miner selling, or a macro shock.

But for the long-term investment case, it matters. Bitcoin’s value proposition depends partly on credible long-term security. If large institutions are going to keep building Bitcoin vaults, they need confidence that those vaults can adapt to future cryptographic threats.

The address-reuse warning is useful because it turns a vague quantum debate into a practical custody question: which coins are exposed, which wallets need to migrate, and how early should the process begin?

Bitcoin does not have a quantum crisis today. But it does have a planning challenge, and the larger the asset becomes, the more important that challenge gets.

JPMorgan Chase CEO Jamie Dimon said US banks “will not accept” the current draft of the CLARITY Act. He vowed the industry will fight the bill, escalating a public clash with Coinbase.

At the Reagan National Economic Forum on Friday, Dimon attacked a CLARITY Act provision. The clause lets crypto firms pay interest-like rewards on stablecoin balances without bank-style consumer protections.

Banks ‘Will Fight’ the CLARITY Act

Dimon framed the dispute as a fairness issue. He argued any firm taking deposits should face the same capital, liquidity, and reporting requirements as regulated lenders.

“If he takes deposits like a bank, should have bank rules … If you want to be a bank, be a bank,” Dimon stated in an interview with Fox Business.

The CEO said the American Bankers Association, smaller banks, and credit unions all oppose the current text.

“It will be fought. Don’t bow down to this guy or company.”

“I am not that worried about stablecoin. I would have nothing to do with it. Would blow up on its own.”

The bill is heading for markup in Congress. The dispute now pits Wall Street’s largest bank against the largest US crypto exchange. Dimon said his ask is simple.

The securities regulator was preparing to release its “innovation exemption” for tokenized stocks as soon as this week, and a draft of the plan had been prepared and reviewed by staff.

However, the timing has since been pushed back as the SEC weighs input from stock-exchange officials and other market participants, reported Bloomberg, citing people familiar with the matter on Saturday.

The exemption would have allowed the trading of tokenized stocks on decentralized exchanges that do not have the backing or consent of the public companies whose shares they track.

Experts Weigh Pros And Cons

However, the SEC noted that allowing the trading of third-party tokens has raised concerns. Several former regulators reportedly said it was unclear how companies could fulfill the same rights criteria as tokens traded on third-party blockchains.

Bloomberg also reported that public companies might face uncertainty over normal practices such as issuing dividends and counting shareholder votes. There was also concern about tokens ending up in the hands of bad actors overseas.

SEC Commissioner Hester Peirce said earlier this week that any exemption would be “limited in scope” by only permitting “digital representations of the same underlying equity security that an investor could purchase in the secondary market today.”

“The SEC deserves a lot of credit for preparing diligently for legislation and for moving ahead expeditiously under its existing authority to provide clarity to markets in adopting tokenization in capital markets,” said Coinbase chief legal officer Paul Grewal on Saturday.

Thank you @HesterPeirce. @Coinbase has long supported the thoughtful SEC staff comments already published on tokenization.

The SEC already has the existing authority it needs to permit innovation in securities markets, particularly for real, onchain tokenized NMS equities that… https://t.co/Mwr5VBrSVQ

Meanwhile, Tiger Research director Ryan Yoon cautioned that allowing third-party trading of tokenized stocks could risk liquidity and revenue fragmentation. The move could create “price discrepancies across platforms,” in addition to increasing slippage on large orders, and ultimately “degrading overall market efficiency,” he said.

He added that financial revenues that should accrue to domestic US exchanges could flow offshore instead. Benefits from the move could include faster settlement, fractional ownership, lower transaction costs, the potential for 24/7 trading, and giving non-US citizens access to popular US stocks.

Crypto Markets Bounce on Trump Deal

Crypto markets have recovered from their Saturday slump today following the latest announcement from US President Donald Trump, who said on Truth Social that an agreement has been “largely negotiated, subject to finalization between the United States of America, the Islamic Republic of Iran, and the various other countries.”

The deal would include reopening the Strait of Hormuz, and “final aspects and details of the deal are currently being discussed and will be announced shortly,” he added.

Bitcoin reclaimed $77,000 in early trading on Sunday following its dip to a five-week low of $74,200 on Saturday.

ICP is the worst-performing cryptocurrency today (at least among the top 100), posting a 10% price decline.

However, certain technical indicators suggest this might be only a short-lived pullback, while multiple analysts support the bullish scenario.

ICP Heads South

Just a few hours ago, the asset’s valuation plunged to a one-week low under $3, while its market capitalization sank to approximately $1.6 billion.

ICP Price, Source: CoinGecko

It is important to note that ICP’s negative performance aligns with an overall correction sweeping through the broader crypto market. Bitcoin (BTC) slipped beneath $80,000, while popular altcoins like Worldcoin (WLD), Cronos (CRO), Arbitrum (ARB), and Aptos (APT) tumbled by 7-8% over the past day.

In the meantime, Coinbase could have also played a role in Internet Computer’s downfall. Recently, it removed six non-USD trading pairs, including ICP/USDT and ICP/GBP.

Such actions by one of the biggest cryptocurrency exchanges reduce liquidity for the affected tokens and make it harder for traders to enter or exit positions. Fewer trading options often mean lower volume and weaker investor confidence, especially amid a crypto pullback.

At the same time, one should keep in mind that if Coinbase had removed all ICP-related services, the impact would likely have been far more severe and could have triggered a much sharper price collapse.

The asset remains available on numerous well-known exchanges, including Binance, Bybit, Bitget, OKX, and more. Two months ago, the leading South Korean trading venue Upbit also hopped on the bandwagon, fueling a 16% price increase for ICP following the news.

Resurgence Comes Next?

ICP’s Relative Strength Index (RSI) signals that the price pullback may soon be replaced by a revival. The technical analysis tool runs from 0 to 100, and readings below 30 indicate that the valuation has dropped too much, too quickly, potentially setting the stage for an upside move. Conversely, anything under 70 is considered a warning of impending correction. Currently, the RSI stands at around 28.

ICP RSI, Source: CryptoWaves

Analysts like Kong Trading and JAVON MARKS expressed confidence in the coin’s outlook. The former noted that almost half of ICP’s supply is locked in staking, with people committing for years.

“That’s not weak conviction. Hard to ignore when supply keeps tightening like this,” they added.

For their part, JAVON MARKS recently argued that ICP has displayed a Falling Wedge pattern and shows signs of strength. They believe a potential breakout could spark a 300% move above $10 and “may act as the start of an even larger reversal.”

As the Senate Banking Committee prepares to mark up the long-anticipated CLARITY Act on Thursday, Coinbase CEO Brian Armstrong has argued that the newest version of the bill represents a workable “compromise” and could meaningfully improve the US financial system.

Speaking to FOX Business, Armstrong said the updated draft reflects concessions on both sides—what he described as the crypto industry meeting requests from bank lobbyists and lawmakers, while the banking sector also gave ground during negotiations.

Coinbase CEO’s CLARITY Act Pitch

Armstrong also highlighted one specific element tied to stablecoin rewards. He said the approach in the latest bill would only apply when there is “some sort of material activity on the account,” adding that he believes the overall package would make the system “more efficient.”

The claim is that the legislation would help streamline financial services, reduce friction, and make access easier for consumers and businesses—while still keeping the framework aligned with banking-sector concerns that were raised during talks.

Still, critics point to the banking industry’s pushback as evidence that the dispute is far from settled. As reported throughout the week by Bitcoinist, banking trade groups have opposed the CLARITY Act’s stablecoin-rewards provision, arguing that it could give crypto firms too much flexibility.

Their position is that the policy might also encourage deposits to shift away from traditional, insured banking channels rather than strengthening them.

Beyond the details of stablecoin rules, Coinbase CEO argued that the broader direction of the CLARITY Act reflects growing institutional interest in digital assets.

In his view, banks are increasingly integrating stablecoins and crypto-related services because customer demand is rising—an angle that suggests the bill, if passed in its current form, could provide the clearer structure institutions want before expanding further.

Can The Latest Crypto Bill Draft Survive?

Supporters of the bill are not limited to Coinbase. Ripple CEO Brad Garlinghouse also backed the current push, commenting on social media site X (previously Twitter) that the Senate Banking Committee is “putting in the work” to move the CLARITY Act forward.

Garlinghouse’s message emphasized that Ripple supports the bill because crypto businesses and major participants should have the “same rules and protections as every other asset class,” and because—if the US is serious about leading in crypto—this is the moment to finalize legislation and get it done.

Even with that backing, the legislative road ahead is not smooth. Politico reported that Senator Elizabeth Warren, a well-known crypto skeptic, is vowing to pursue extensive changes to the bill through amendments.

The reporting says Warren and others are preparing more than 100 amendments ahead of the markup, following the release of an updated 309-page draft that expands on an earlier 278-page version introduced in January.

According to the same reporting, Warren submitted more than 40 amendments on her own, with much of the rest attributed to Democratic members of the Banking Committee.

This mirrors earlier moves around the bill: the January markup session drew 137 amendments, and it was eventually cancelled after a period of resistance that included Armstrong and Coinbase withdrawing support for the bill at the time.

For now, the core question going into Thursday’s markup is whether the latest CLARITY Act draft can hold together.

Featured image created with OpenArt, chart from TradingView.com

Circle’s $222 million ARC token presale has given Wall Street a new way to value the USDC issuer, while raising a harder question for one of crypto’s most profitable alliances.

On May 11, Circle said investors led by a16z Crypto backed the presale of ARC, the native token for Arc, its planned public blockchain for institutional finance.

The sale valued the network at $3 billion on a fully diluted basis and came alongside first-quarter results that showed $694 million in total revenue and reserve income, up 20% from a year earlier.

At the same time, USDC in circulation rose 28% to $77 billion, while on-chain transaction volume reached $21.5 trillion, up 263% year over year.

Circle’s Q1 Earnings Report (Source: Circle)

Those figures reinforced Circle’s position as one of the main issuers in the global stablecoin market, where tokenized dollars have become core infrastructure for trading, payments, and settlement.

However, the more important development was Circle’s attempt to move beyond issuance through its new blockchain network, Arc.

Arc gives the company a network-level growth story built around payments, tokenized assets, foreign exchange, capital markets, and AI-driven commerce.

That push places Circle closer to the terrain already occupied by Coinbase, its longtime USDC partner and the operator of Base, the Layer 2 network that the US-based exchange has positioned as a settlement layer for stablecoins, consumer payments, and agentic transactions.

Considering this, Circle’s aggressive expansion could bring a new competition to the crypto landscape: a looming, head-to-head battle with Coinbase.

Circle gives investors a wider story

Circle’s business has long been tied to the economics of stablecoin reserves. The company issues USDC, holds safe assets backing the token, and earns income on those reserves.

That model can be powerful when rates are elevated, but it also raises questions about how durable its earnings will be as interest income declines.

The company is pitching the network as an “economic operating system” for the internet, a shared environment where stablecoins, tokenized assets, and financial applications can operate on common infrastructure.

The chain is expected to be EVM-compatible, with stablecoin-native fees, deterministic sub-second finality, and configurable privacy designed for institutions that need auditability without exposing every transaction detail to the public.

Circle Chief Executive Jeremy Allaire framed the quarter around the convergence of AI platforms and on-chain money, saying:

“Circle’s first quarter reflected strong execution against a much bigger opportunity: the rapid convergence of AI platforms and economic operating systems into a new internet stack. With the ARC token presale, momentum behind the Arc network, and the launch of our Agent Stack, we are building trusted infrastructure for AI-native economic activity and a more programmable internet financial system.”

The investor list shows how far that pitch now reaches. a16z Crypto led the presale with a $75 million investment.

Other participants included BlackRock, Apollo Funds, Intercontinental Exchange, SBI Group, Janus Henderson Investors, Standard Chartered Ventures, General Catalyst,a IDG Capital, Haun Ventures, and Bullish.

The message to investors is clear: Circle wants to be valued less as a stablecoin issuer exposed to rate cycles and more as a full-stack infrastructure company for on-chain finance.

In a note shared with CryptoSlate, Clear Street analysts echoed that view, writing that Circle is “no longer a pure crypto play” and has built the Layer 1 network, application layer, and partner ecosystem required to become a critical infrastructure provider.

The firm raised its price target on the stock from $152 to $157, citing Arc, Agent Stack, Circle Payments Network, and regulatory momentum as potential sources of upside.

USDC already moves across more than 30 blockchains and is integrated throughout exchanges, wallets, fintech platforms, and institutional systems.

That distribution has been one of the stablecoin’s main strengths. Circle could grow as USDC became more widely used, regardless of where the activity settled.

Arc gives Circle a reason to bring more of that activity onto the infrastructure it controls.

The network is designed to support payments, lending, foreign exchange, capital markets, and tokenized assets. Circle has also positioned ARC as a coordination token for validators, builders, liquidity providers, exchanges, institutions, and users.

In that structure, USDC remains the transactional asset, while ARC is intended to help govern economic rules and align network participants.

That creates a broader economic layer around Circle’s core product. If Arc gains traction, investors will not only measure Circle by USDC circulation and reserve income.

They will also track transaction volume, developer adoption, institutional participation, validator activity, and the degree to which Circle can capture revenue from the infrastructure surrounding USDC.

Circle Payments Network adds another part of that strategy. Clear Street said CPN reached $8.3 billion in annualized total payment volume and approached $10 billion by May 7, with 136 financial institutions enrolled.

Managed Payments is intended to reduce friction for banks and payment service providers by handling licensing, liquidity, custody, and compliance burdens.

Taken together, Arc, Agent Stack, CPN, and Managed Payments give Circle a more ambitious public-market story. The company is trying to become the platform where digital dollars move, settle, and interact with software.

That ambition makes the Coinbase relationship more complicated.

Coinbase already controls much of the flow

However, Coinbase has its own claim to the USDC infrastructure story.

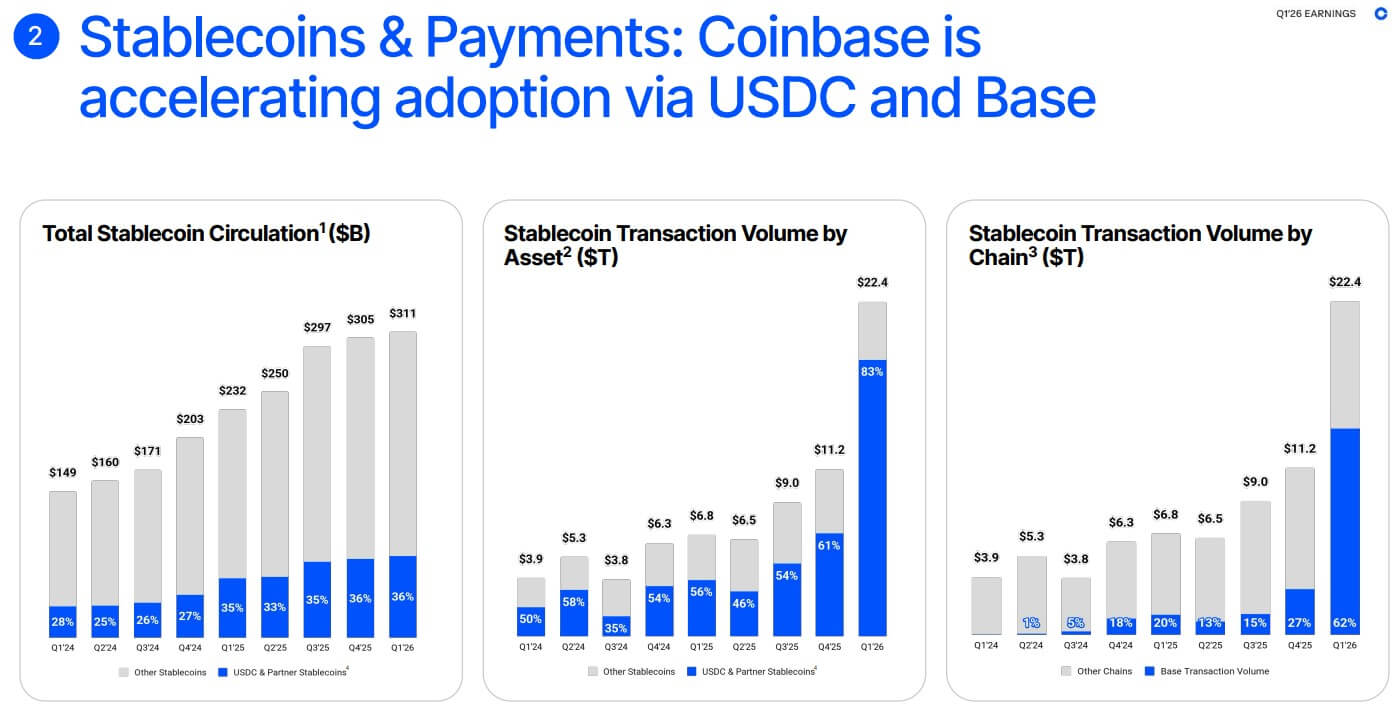

In its first-quarter report, the company described itself as the distribution engine for USDC, with more than 25% of total USDC in circulation, or about $19 billion on average, held across Coinbase products.

Coinbase said Base processed 62% of global on-chain stablecoin transaction volume during the quarter, more than all other chains combined.

At the same time, more than 100 million payments were processed through its x402 protocol, with more than 99% completed using USDC.

How Coinbase is Growing Stablecoin Adoption via USDC and Base (Source: Coinbase)

Those figures show why Arc is sensitive for Coinbase.

Coinbase is no longer merely a distribution channel for Circle’s stablecoin. It is building the rails around the asset.

Its stack includes USDC as the programmable dollar, Base as the low-cost settlement network, and Coinbase Developer Platform, AgentKit, and x402 as infrastructure for developers and AI-enabled payments.

Circle’s emerging stack points in the same direction. USDC provides the dollar asset, Arc provides the network, Agent Stack targets AI-native commerce, and CPN connects financial institutions and payment companies.

The companies remain commercially aligned around USDC growth. But their infrastructure strategies increasingly point toward the same flows.

The alliance gets a new scoreboard

For years, the Circle-Coinbase relationship was one of crypto’s cleanest partnerships. Circle issued USDC. Coinbase distributed it across its exchange, wallet, and institutional products. The stablecoin gained scale, and Coinbase shared in the economics.

That relationship helped make USDC one of the most important dollar assets in crypto. It also gave Coinbase a major stablecoin revenue line and helped turn USDC into a regulated alternative to Tether’s USDT for many US-based institutions.

However, Arc introduces a different incentive structure.

Omar Kanji, an investor at Dragonfly, captured the concern in a post asking how long the “marriage” between Circle and Coinbase can stay clean.

His argument was that the old model worked when Circle was the issuer, and Coinbase was the distributor. But Circle’s public-market demands and Arc’s token-backed network now require the company to show investors that it can own more customers, flows, and infrastructure directly.

That is where Arc overlaps with Base. Circle wants Arc to host USDC balances, tokenized assets, payments, settlement, and eventually foreign-exchange activity. Coinbase wants Base to serve as the main venue for stablecoin payments, on-chain consumer transactions, AI-agent activity, and institutional settlement.

The tension is already visible in adjacent products. Coinbase has cbBTC, a wrapped BTC product used across DeFi. Circle is preparing cirBTC, which is designed to integrate with Arc and Circle Mint.

While this overlap does not signal an immediate rupture, it shows that the companies are no longer staying in separate lanes and are beginning to compete on similar products.

AI payments raise the stakes

The competition becomes more significant when viewed through the lens of agentic commerce.

AI agents are expected to become a larger share of internet activity, handling tasks such as purchasing data, paying for software, settling invoices, managing subscriptions, and executing business processes.

Those transactions require programmable money, low-cost settlement, and infrastructure that can authorize spending without constant human intervention.

Stablecoins are well-suited to that environment because they operate continuously, settle quickly, and can be embedded directly into software. That has made agentic commerce one of the most attractive long-term narratives for stablecoin infrastructure providers.

Coinbase is already claiming early leadership. Its first-quarter materials pointed to Base’s share of on-chain agentic stablecoin transaction volume and the rapid growth of x402 payments. The company is presenting Base, USDC, AgentKit, and x402 as a ready-made stack for machine-driven economic activity.

Circle is moving to meet that opportunity with Agent Stack and Arc. Allaire has framed AI platforms and on-chain money as part of a new internet stack, and Circle’s product roadmap suggests the company wants USDC to become a settlement layer not only for humans and institutions, but also for software agents.

Considering this, Tom Wan, the head of data at Entropy Research, concluded:

“[Circle and Coinbase] business lines are converging across blockchain, tokenization, payments and stablecoins. A formal split is unlikely given the mutual benefits still on the table, but the trajectory is clear. Both sides are building toward a less dependent relationship, and the overlap will only create more friction over time.”

Binance will list MegaETH’s MEGA token on April 30, 2026, with spot trading set to open at 11:00 UTC. The exchange received no allocation or listing fee, drawing wide praise from analysts and founders.

Binance applied its Seed Tag to MEGA. Every major centralized exchange has now added MEGA without taking project tokens, a rare outcome for a Layer 2 (L2) launch.

Binance Joins MEGA Exchange Spread Without Tokens

Spot pairs including MEGA/USDC and MEGA/USDT went live shortly after the Binance announcement. Deposits and trading remain restricted in the United States, Canada, the Netherlands, and other jurisdictions for regulatory reasons.

MegaETH publicly committed earlier in 2026 to a no-pay listing policy. The team refused to send tokens for fees, liquidity rewards, or promotional airdrops.

The team argued that listings should follow merit and demand, not supply transfers.

“MegaETH has not, and will not, give away MEGA tokens as “fees or airdrops” to any centralized or decentralized exchange for a listing. If an exchange chooses to list the MEGA token, it is because they believe it is a strong project,” the team articulated.

By launch day, Coinbase, Bybit, Upbit, Bithumb, and Binance had each added MEGA without taking project tokens.

Smaller venues including OKX, Bitget, and MEXC also enabled trading. Community members called the spread a “royal flush” and a first for an organic Layer 2 listing run.

2x+ for ICO buyers 2.2x paper gains for those who locked for 12 months

Looks like @megaeth was able to pull the rabbit out of the hat with the royal flush of listing spreads: Coinbase, Bybit, Upbit, Bitthumb, and now even Binance.

Industry Figures Frame Listing as a Shift in Exchange Practice

Simon Dedic, chief executive at Blockhead Capital, said Binance “bent the knee” by listing without compensation. He framed the outcome as a positive signal for token founders weighing exchange demands during launches.

“Honestly, I wouldn’t have expected them to bend the knee and list it for free, so kudos to Binance here. Imagine being such a sought-after project that every major CEX lists you without receiving a single token,” wrote Dedic.

Analyst DeFi Ignas pointed out that Binance had previously committed to supporting builders with large communities. He argued that skipping MEGA would have contradicted that stance.

The general sentiment is that the launch is “substantive and principled,” given MegaETH’s avoidance of KOL payments, point-farming campaigns, and supply allocations to exchanges.

The project’s mUSD stablecoin and proximity market design are potential routes for the token to capture network value.

“It’s a rare sight in a space that rewards crime. Good to see good teams win. Hopefully an inspiration playbook for other quality projects to follow,” stated Grail.eth, a popular user on X.

MEGA Trades Near $2 Billion Fully Diluted Valuation

MEGA traded around $0.16 in the hours after the Binance listing announcement. The price placed circulating market cap near $190 million and fully diluted valuation around $1.7 billion. Total supply is 10 billion tokens.

— IAm⭕️hJay | Σ:(CTNG HOUSE) (@OhJay_001) April 30, 2026

Community responses pointed to compromised approvals or phishing rather than a protocol fault. Users urged claimants to revoke unused permissions before interacting with new contracts.

The MEGA listing run sets a precedent for other Layer 2 teams to point to. Whether future launches replicate the playbook may depend on whether their tokens see comparable demand.

Supply concessions have long shaped exchange decisions, and few projects have refused them.

Stablecoin Yield: Why Washington’s Battle Could Reshape Crypto Banking Forever

Regulation·28 March 2026·5 min read

Stablecoin Yield: Why Washington’s Battle Could Reshape Crypto Banking Forever

A single clause in the US CLARITY Act has sent Circle’s stock to its worst-ever single-day drop, alarmed Coinbase, and put stablecoin yield at the centre of a fight that will determine whether crypto platforms or traditional banks control the future of digital money.

AA

Ashton Addison

Founder & CEO · Crypto Coin Show · Since 2014

Syndicated via Refinitiv TV London Stock Exchange Group

A leaked draft of the Digital Asset Market Clarity (CLARITY) Act sent shockwaves through crypto markets on 24 March 2026, when provisions proposing to ban stablecoin platforms from offering yield on customer balances were reported by The Wall Street Journal. Circle Internet Group recorded its largest-ever single-day share price decline, while Coinbase also fell sharply — before both partially recovered the following day. By 25 March, Senate negotiators announced they had reached an agreement in principle with the White House on the disputed yield provisions, but the broader regulatory uncertainty remains unresolved.

Key Concept

Stablecoin Yield

Interest or rewards paid by a crypto platform to users who hold stablecoin balances — functioning similarly to a savings account interest rate, but often at significantly higher rates than traditional banks offer.

Key Concept

The CLARITY Act

US legislation currently before the Senate aimed at establishing a comprehensive regulatory framework for digital assets, covering market structure, stablecoin issuance, and the treatment of crypto platforms under existing financial law.

Context

The Fight Behind the Bill

The stablecoin yield dispute has been the single largest obstacle blocking the CLARITY Act’s advancement through the Senate. On one side, traditional banks — led by the American Bankers Association — have argued that allowing crypto platforms to pay yield on stablecoin balances risks triggering significant deposit flight away from savings accounts, ultimately threatening bank lending capacity. On the other, the crypto industry has maintained that restricting yield would leave US platforms uncompetitive against offshore alternatives and damage innovation domestically.

SEC Chairman Paul Atkins, speaking at the Blockworks Digital Asset Summit in New York on 24 March, described the prior week as “a historic week for America’s digital asset markets” and characterised recent regulatory actions as “the end of the beginning” — while cautioning that congressional legislation remains the only route to a durable framework. Atkins also criticised the prior administration’s enforcement-first approach, acknowledging that it had pushed crypto activity toward offshore jurisdictions.

Analysis

Who Wins, Who Loses if Yield Is Banned

The stakes of the yield debate extend well beyond compliance costs. If enacted in their strictest form, the CLARITY Act’s yield restrictions would align stablecoins more closely with traditional deposit products — effectively handing incumbent banks a structural advantage they have lobbied hard to preserve. For crypto-native stablecoin issuers, the consequences vary significantly by business model.

“

“The impact may be less about restriction and more about redistribution — determining who captures value and under what conditions.”

CCS Analysis · 28 March 2026

Circle, issuer of USDC and the most US-regulated of the major stablecoin operators, faces the most direct exposure given its business model’s reliance on yield-generating activities. Tether, by contrast, operates largely outside US jurisdiction and would face fewer direct constraints. This competitive asymmetry is one reason analysts suggest that a strict yield ban could paradoxically strengthen offshore operators while pressuring the more compliant, domestically-oriented platforms the legislation ostensibly aims to support.

Compounding the picture, the New York Stock Exchange announced on 24 March a collaboration with digital asset infrastructure firm Securitize to develop a blockchain-based trading platform capable of 24/7 settlement using stablecoin funding. If stablecoin yield is curtailed, the economic incentive underpinning much of that institutional infrastructure weakens alongside it.

What It Means

A More Proactive Regulatory Philosophy

What may distinguish the current regulatory moment from prior crypto policy cycles is not merely the content of the rules, but the approach underpinning them. Earlier frameworks largely focused on enforcement after misconduct, or on clarifying asset classifications as disputes arose. The CLARITY Act represents a more proactive posture — attempting to define market structure before it fully matures rather than reacting to crises once they develop.

Whether the Senate’s reported agreement in principle on stablecoin yield translates into final legislative language — and how that language is ultimately worded — will determine how value flows through digital asset markets for years to come. For crypto-native firms, the challenge is to demonstrate that innovation can operate within regulatory constraints. For traditional institutions, it is to move quickly enough to remain relevant in a market they did not build.

The CLARITY Act’s March deadline passed without a final signing. Institutional money has remained hesitant, and altcoin sentiment has stayed subdued as traders wait for Washington to deliver a definitive answer. The bill’s trajectory in the coming weeks will be one of the most consequential regulatory developments in digital assets since the FTX collapse in 2022.

Coinbase Powers First Crypto-Backed Conforming Mortgages | Crypto Coin Show

BTC$87,420▼ 2.78%

ETH$2,041▼ 1.45%

USDC$1.00▲ 0.00%

COIN$214.60▲ 1.12%

BETR$3.88▲ 4.30%

FNMA$1.94▼ 9.29%

BTC$87,420▼ 2.78%

ETH$2,041▼ 1.45%

USDC$1.00▲ 0.00%

COIN$214.60▲ 1.12%

BETR$3.88▲ 4.30%

FNMA$1.94▼ 9.29%

BreakingReal EstateAnalysis·March 26, 2026·6 min read

Coinbase Powers the First Crypto-Backed Conforming Mortgages — Bitcoin Now Buys Your Home

In a watershed moment for digital assets and mainstream finance, Coinbase and Better Home & Finance have launched the first Fannie Mae–backed mortgages that accept Bitcoin and USDC as down payment collateral — unlocking homeownership for 52 million American crypto holders without forcing a single sale.

AA

Ashton Addison

Editor-in-Chief · Crypto Coin Show · Syndicated on Refinitiv TV

For years, crypto holders faced an uncomfortable paradox: sit on life-changing digital wealth while struggling to scrape together a traditional down payment for a home — or sell assets, trigger capital gains taxes, and permanently exit positions they’d spent years building. On March 26, 2026, that paradox officially ended.

Coinbase (NASDAQ: COIN) and Better Home & Finance Holding Company (NASDAQ: BETR) announced a landmark partnership today: the first token-backed, conforming mortgages in U.S. history. Qualified borrowers can now pledge Bitcoin (BTC) or USDC held in their Coinbase accounts as collateral to fund their cash down payment — securing a standard Fannie Mae–backed conforming mortgage without liquidating a single satoshi.

“People who are sitting on Bitcoin or USDC can put a roof over their head without needing to sell it, without needing to incur capital gains.”

— Mark Troianovski, Head of Consumer & Platform Business Development, Coinbase

52MAmerican adult crypto holders eligible

41%of families blocked from homeownership by cash barriers

$4TFannie Mae mortgage market now open to crypto collateral

What Exactly Is a Token-Backed Conforming Mortgage?

The structure is elegantly simple, yet historically significant. A borrower who qualifies under Better’s standard mortgage underwriting criteria can pledge Bitcoin or USDC instead of bringing a traditional cash down payment to closing. That crypto pledge backs a separate, privately financed loan used to fund the down payment. The first-lien mortgage itself remains a fully conforming Fannie Mae loan — carrying identical protections, standards, and regulatory treatment as any conventional mortgage.

Critically, both the down payment loan and the primary mortgage share the same interest rate and amortization term, meaning borrowers manage a single unified monthly payment rather than juggling two separate obligations. This unified payment structure is described by the companies as a true market first in the conforming mortgage segment.

1

Qualify with Better

Borrowers apply through Better’s AI-native Tinman® platform and qualify under standard Fannie Mae conforming mortgage criteria.

2

Pledge Bitcoin or USDC from Coinbase

Borrowers transfer BTC or USDC from their Coinbase account into a custody wallet with Better (held in a Coinbase Prime account), retaining ownership rights throughout.

3

Crypto backs a separate down payment loan

The pledged digital assets collateralize a privately financed loan that funds the cash down payment — no sale, no taxable event.

4

Close on a standard conforming mortgage

The first-lien mortgage is a fully Fannie Mae–eligible conforming loan with a single unified monthly payment covering both loans.

5

Crypto returned upon repayment

The pledged crypto remains in custody for the life of the down payment loan and is returned to the borrower once that loan is fully repaid.

Fannie Mae’s Historic Green Light

The involvement of Fannie Mae — the $4 trillion government-sponsored enterprise that sets standards for the majority of the U.S. mortgage market — is the headline here. For the first time in its history, Fannie Mae is accepting mortgages collateralized by cryptocurrency. By aligning Bitcoin and USDC with conforming loan structures, this partnership positions digital assets as part of mainstream financial infrastructure rather than an experimental parallel system.

Token-backed mortgages originated by Better are designed in accordance with Fannie Mae guidelines and remain structurally identical to other conforming mortgages. This Fannie Mae alignment also enables interest rates far lower than those historically associated with standalone crypto-backed loans — which typically carried steep premiums reflecting their niche, uninsured nature.

“Better was founded to make homeownership more accessible for all Americans, and this partnership with Coinbase introduces a new pathway to realizing the American Dream for the 52 million Americans who own digital assets.”

— Vishal Garg, CEO & Founder, Better Home & Finance

Key Borrower Protections

Perhaps the most significant departure from previous crypto-backed lending products is the elimination of margin calls. In typical crypto-backed loan structures, a sharp decline in collateral value triggers margin calls — forcing borrowers to post additional collateral or face immediate liquidation. This product does none of that.

🚫

No Margin Calls

If BTC drops in value, mortgage terms remain entirely unchanged. Market movements alone never trigger liquidation.

🏦

No Taxable Event

Borrowers pledge — not sell — their assets. No capital gains taxes, no early withdrawal penalties triggered at closing.

💰

USDC Earns Rewards

Borrowers pledging USDC continue earning yield on holdings, potentially offsetting mortgage payments and reducing the net effective rate.

🔐

Ownership Retained

Crypto is custodied in a Better/Coinbase Prime wallet but ownership rights remain with the borrower throughout.

📋

Fannie Mae Protections

As a conforming loan, borrowers benefit from the same legal protections and standards as any conventional mortgage.

💳

Coinbase One Rebate

Coinbase One members who close through Better are eligible for a rebate of 1% of the mortgage value, capped at $10,000 toward closing costs.

Collateral is only at risk of liquidation in the event of a 60-day mortgage payment delinquency — precisely mirroring the treatment of defaulted conventional mortgages. The product is designed, in Coinbase’s own words, to “work within the safeguards of the existing mortgage system, including how risk like asset volatility is managed.”

A Worked Example

📊 Scenario: $500,000 Home Purchase

Home Purchase Price$500,000

Required Down Payment (20%)$100,000

Bitcoin Pledged as Collateral~$250,000 in BTC

Down Payment Loan Funded$100,000 cash

Fannie Mae First-Lien Mortgage$400,000 conforming loan

Coinbase One Rebate (if eligible)Up to $4,000 toward closing

BTC Liquidation RiskOnly on 60-day delinquency

Margin Call RiskNone

The Rate Premium: What Borrowers Should Know

The product is not free. Coinbase has confirmed that crypto-backed mortgages will carry rates 0.5 to 1.5 percentage points higher than a standard 30-year conforming loan, depending on borrower profile. That said, this premium is substantially lower than rates historically associated with crypto-backed loans, which often carried 3–5% premiums or more, and the product is designed to function at near-conforming pricing rather than niche wealth management pricing.

For borrowers who believe in the long-term appreciation of Bitcoin — or who hold USDC and can offset mortgage costs with yield rewards — the calculus may clearly favor pledging over selling. The break-even point depends heavily on individual tax situations, expected BTC appreciation, and current conforming rates.

The Generational Wealth Angle

The companies frame this as a generational solution. Coinbase data shows that 45% of younger investors own crypto, compared with 18% of older cohorts — suggesting digital assets are becoming a primary store of value for a new generation that has simultaneously struggled the most with housing affordability. The median age of first-time homebuyers has risen to 40, versus 32 in 2000, per the National Association of Realtors.

“Token-backed mortgages are a major first step to unlocking homeownership for the younger generations that have struggled with barriers to saving for a traditional down payment.”

— Max Branzburg, Head of Consumer & Business Products, Coinbase

According to Better, roughly 41% of American families fail to purchase homes due to insufficient liquid cash — even when they hold other forms of wealth. With 52 million American adults now owning digital assets, this product directly targets that gap. Redfin data cited in the launch shows 12.7% of Gen Z and Millennial homebuyers have already sold crypto to fund a down payment, compared to 3.5% of Gen X and just 0.5% of Baby Boomers — underscoring both the latent demand and the tax friction this product resolves.

Regulatory Tailwinds and What Comes Next

The launch coincides with a notably crypto-friendly regulatory environment under the Trump administration, which has taken active steps to ease regulatory hurdles constraining the expansion of digital assets into traditional financial products. The Coinbase-Better partnership is an early beneficiary of this shift.

Both companies have also signaled aggressive expansion of eligible collateral types over time, potentially including tokenized equities, fixed income instruments, and tokenized real estate assets — pending market and regulatory conditions. This positions the product as a foundation for a much broader bridge between onchain capital and the traditional mortgage market.

Interested borrowers can register for early access today at better.com/crypto-backed-mortgages.

CCS Take: This Is a Watershed Moment

We’ve covered blockchain’s intersection with real estate since 2014 — from early NFT deed experiments to DeFi lending. But this is categorically different. When Fannie Mae — the entity that backstops roughly half of all U.S. mortgage origination — formally accepts Bitcoin as mortgage collateral, digital assets have crossed an institutional Rubicon.

The absence of margin calls is the product detail that deserves the most attention. Previous crypto-backed lending models essentially invited volatility-driven liquidations that wiped out borrowers during crypto winters. This structure deliberately immunizes borrowers from that risk while keeping them in their homes under the same protections as any conventional mortgage holder.

For the 52 million Americans who hold crypto and the millions more who will enter the asset class in the years ahead, this is the answer to the question they’ve been asking: can my digital wealth build a real one? As of today, the answer is yes.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Crypto-backed mortgage products involve risk. Tax treatment of crypto pledges may vary; consult an independent tax advisor. Crypto Coin Show and its affiliates may hold positions in assets mentioned. This content is syndicated on Refinitiv TV and distributed across CCS media channels.

Tumbles 10% Daily: Is Coinbase Responsible for the Plunge?")

")