Cynthia Lummis gave CLARITY Act a July promise, but it still needs a Senate path

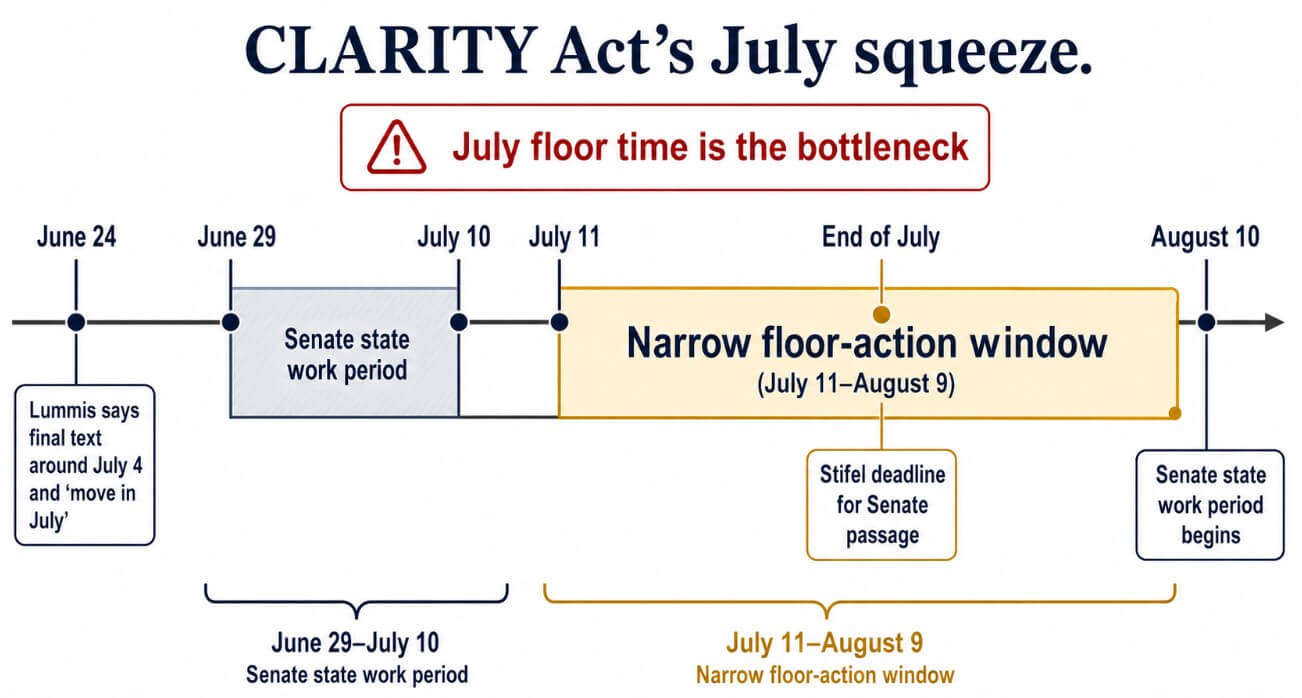

Senator Cynthia Lummis told Fox Business on June 24 that negotiators expect final Senate compromise language around the July 4 recess and then plan to “move in July,” the most public deadline any sponsor has set for a bill that cleared the Senate Banking Committee in May.

The declaration came before Senate Majority Leader John Thune had announced floor time, before a final Senate floor package had been published, and before the ethics dispute that derailed a key negotiating meeting on June 9 had been resolved.

The calendar problem

The Senate enters a state work period from June 29 to July 10, and another one begins Aug. 10 and runs through Sept. 11.

That leaves a mid-to-late July window of roughly four weeks, and Stifel’s chief Washington policy strategist Brian Gardner wrote that CLARITY probably needs to clear the Senate by the end of July, adding that failure before the August recess would materially deteriorate the bill’s prospects.

Galaxy Research put 2026 passage odds at roughly 50-50, treating the August recess as the last realistic legislative gate. Polymarket traders have priced 2026 passage near 48%, down from 74% a month ago.

Lummis has framed the stakes in generational terms, warning that missing this window would delay meaningful market structure legislation until 2030, after midterms reshape the chamber.

That warning now doubles as a recruitment pitch to Thune: allocate July floor time or explain to the crypto industry why the bill that passed the House 294-134 in July 2025 died on the Senate calendar.

What the committee’s vote left open

Democrats Ruben Gallego of Arizona and Angela Alsobrooks of Maryland joined all 13 Republicans to advance the bill, stating that their committee votes reflected conditional support, with floor backing contingent on resolving outstanding issues that have stayed open since May.

The June 9 ethics meeting among senators, including Gallego, Alsobrooks, and Lummis, alongside White House Crypto Council Executive Director Patrick Witt, broke down without agreement after Republicans and the White House withdrew a provision that would have authorized state attorneys general to sue the Justice Department over failures to enforce ethics rules tied to President Donald Trump’s crypto business interests.

Democrats have also raised AML provisions and the question of whether crypto companies should face bank-equivalent capital and consumer protection obligations if they offer deposit-like products.

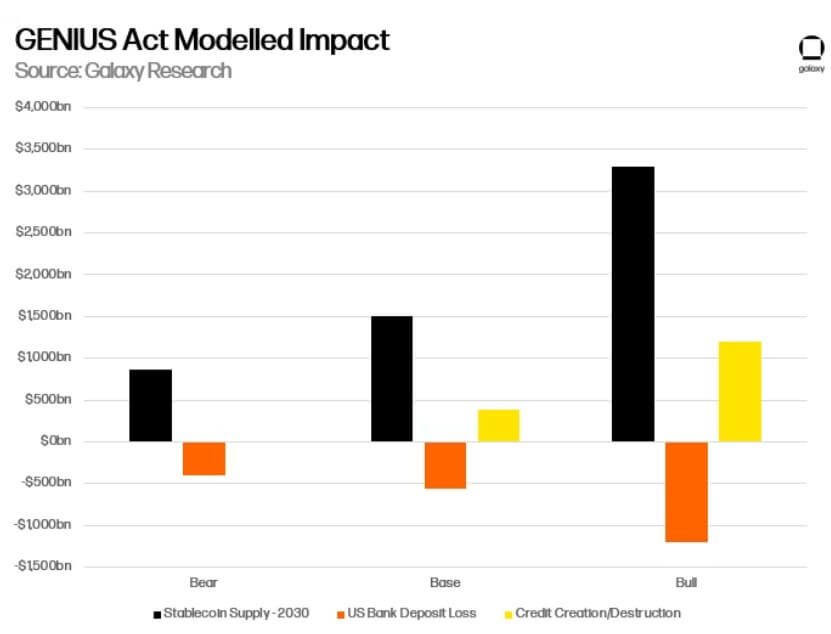

Lummis disclosed that the bill carries $150 million in dedicated funding to combat illicit crypto activity, a provision designed to answer the AML objection directly.

Whether that concession moves conditional Democrats to firm floor commitments is the operative question going into July.

| Requirement | Current status in the article | Why it matters |

|---|---|---|

| Final text | Expected around July 4 recess, but not yet released | Senators cannot fully commit until the compromise language is visible |

| Thune floor time | Lummis says she is working with leadership, but no slot has been announced | A bill can be viable and still die without floor time |

| 60-vote coalition | GOP needs at least seven Democrats | Committee support does not equal cloture support |

| Gallego / Alsobrooks support | Both backed committee passage conditionally | Their final stance is the first test of Democratic durability |

| Ethics language | June 9 talks broke down without agreement | Unresolved ethics disputes can give Democrats a reason to hold back |

| AML / bank-like product concerns | Lummis points to $150M illicit-finance funding and Section 301 revisions | These are the main substantive objections being answered before July |

| House/Senate alignment | Senate changes may require House action | Even Senate passage may not be the final step |

Why Dimon became part of the push

Dimon argued in a Fox Business interview that CLARITY could allow crypto companies to offer rewards resembling interest-bearing deposits without bank-equivalent regulation, and that the bill inadequately addressed AML and Bank Secrecy Act requirements.

Lummis rejected both claims on Fox Business, saying Dimon is “mistaken” and should read the bill over the July 4 recess.

She pointed to revised Section 301, which allows rewards programs but bars benefits tied directly to account balances in a way that replicates traditional bank interest.

Banking sector opposition gives wavering Democrats a respectable reason to hold back, and Lummis is answering JPMorgan’s specific objections before senators go home, making it harder for a Democrat to cite Dimon as grounds for withholding a floor vote.

A letter released by the Blockchain Association and signed by 160 former national security, intelligence, and law enforcement professionals, urging Thune and Senate Democratic Leader Chuck Schumer to advance the bill, adds a national-security frame aimed at the same audience: shrinking the political space for opposition before the recess window closes.

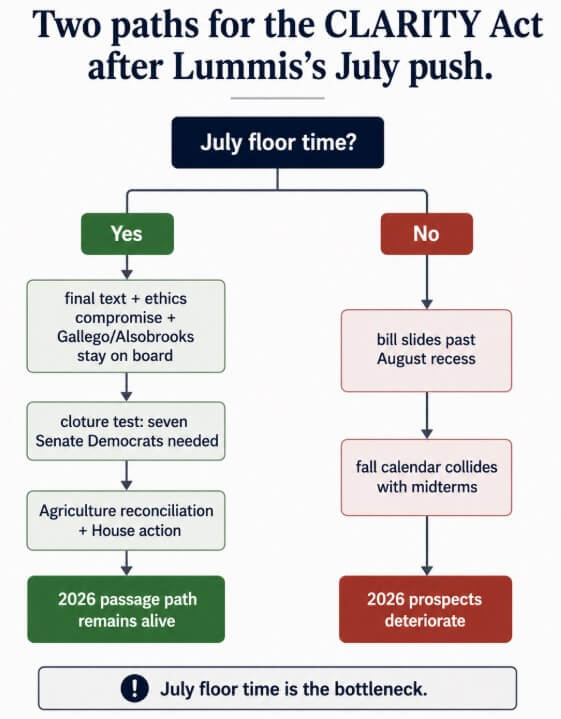

Two outcomes

If Thune schedules July floor time and the ethics language finds a formulation that keeps Gallego and Alsobrooks on board, CLARITY moves to a cloture vote that tests whether five more Democrats are genuinely in range.

A clean floor path through July would require Agriculture Committee reconciliation and House action on any Senate changes before a presidential signature, and clearing those steps would confirm that the 2026 window is real.

Exchanges, token issuers, and asset managers awaiting SEC/CFTC jurisdictional clarity would receive a defined regulatory path by year-end.

If the ethics provision stays unresolved, Thune withholds floor time, or Democratic caveats harden through July, the bill slides into September with a fall calendar running toward November midterms.

Legislation becomes harder to schedule as elections approach, and the coalition that produced a 294-134 House vote and a 15-9 Senate committee vote would face a reconstituted Congress of unknown composition in 2027.

Lummis is saying “moving in July” on national television because that is where the political cost of inaction lands hardest, on Thune, on Democrats, and on the banking lobby simultaneously.

The post Cynthia Lummis gave CLARITY Act a July promise, but it still needs a Senate path appeared first on CryptoSlate.