The last trading day of the previous business week finally brought some more net inflows rather than consistent outflows for the spot Bitcoin ETFs in the United States.

The products tracking the world’s largest altcoin had even more to celebrate at the end of the week, but still closed in the red.

The Good and the Bad: BTC ETF Edition

There’s no need to sugarcoat the end result – the week was still dominated by the bears. Investors pulling out funds from the spot Bitcoin ETFs withdrew $526.64 million throughout the four-day trading week. This means that the overall negative streak continues as the products have not seen a single green week in almost two months.

Within this timeframe, the total cumulative flows have dumped from $59.34 billion to $51.08 billion. July 1 saw the most daily withdrawals, with $294.62 million leaving the funds, according to SoSoValue data. Another $222.64 million went out on June 30 and $231.10 million on June 29. That’s all on the negative side.

The bright side was July 2. After 10 consecutive days of only net inflows, the streak was broken as investors poured in $221.72 million. Moreover, this was the highest single-day inflow recorded since May 5. Friday was a non-trading day due to the July 4 holiday, meaning that the week ended on a more positive note.

Spot Bitcoin ETFs Net Flows. Source: SoSoValue

Ethereum ETF Edition

The daily performance of the financial vehicles tracking ETH was even more promising. The Ethereum ETFs saw more modest $30.04 million withdrawals on June 29 and $27.60 million on June 30. However, the tides turned during the next two business days.

Investors poured in $14.89 million on Wednesday and $29.08 million on Thursday, marking a near-monthly high. Nevertheless, the week still ended in the red, with total net outflows of $13.67 million. As such, the negative streak of the Ethereum ETFs continues, with eight straight weeks in the red. The total cumulative flows are down from $12.09 billion in early May to $10.89 billion on Thursday.

On the more positive side, though, it was a lot less harmful than the $273.34 million taken out during the previous business week.

Ethereum’s slide to its lowest level in more than a year is testing the Wall Street trade that brought the token deeper into institutional portfolios.

Data from CryptoSlate shows that the second-largest cryptocurrency fell to as low as $1,506 during the last 24 hours, its weakest level since April 2025, extending a broad crypto selloff that has already drained leverage from derivatives markets and pushed traders toward defensive positioning.

Crucially, the downswing is not confined to ETH’s spot market as the digital asset is also experiencing a broader deterioration across regulated ETF flows, centralized exchange deposits, and derivatives positioning.

This situation comes at a time when the broader crypto market sentiment has significantly weakened, with Bitcoin falling toward a four-month low near $60,000, while Ethereum has erased much of its market support.

ETF outflows weaken Ethereum’s institutional bid

The pressure has been most visible in the ETF market, where the products that gave institutions a regulated way to buy Ethereum have turned into a source of persistent outflows.

Data from SoSoValue shows that spot ETH ETFs have recorded four straight weeks of withdrawals totaling more than $870 million.

Ethereum ETFs Weekly Flows (Source: SoSoValue)

During that period, the funds posted a 17-day outflow streak interrupted by only one day of inflows, when investors added $19.3 million.

As a result, sosoValue data show total spot Ethereum ETF assets have declined more than 70% from their $30 billion peak to $8.71 billion, which is equal to about 4.01% of Ethereum’s circulating market capitalization.

The reversal has weakened one of the main arguments behind Ethereum’s institutional expansion. The ETFs were expected to broaden access to the asset, deepen liquidity, and give traditional investors a cleaner way to gain exposure without handling tokens directly.

However, that demand has softened as ETH’s price moved lower and investors have reduced risk across digital assets.

Exchange inflows add another supply risk

As institutional demand-side forces abated, the physical supply available on liquid trading platforms experienced a sudden and substantial expansion.

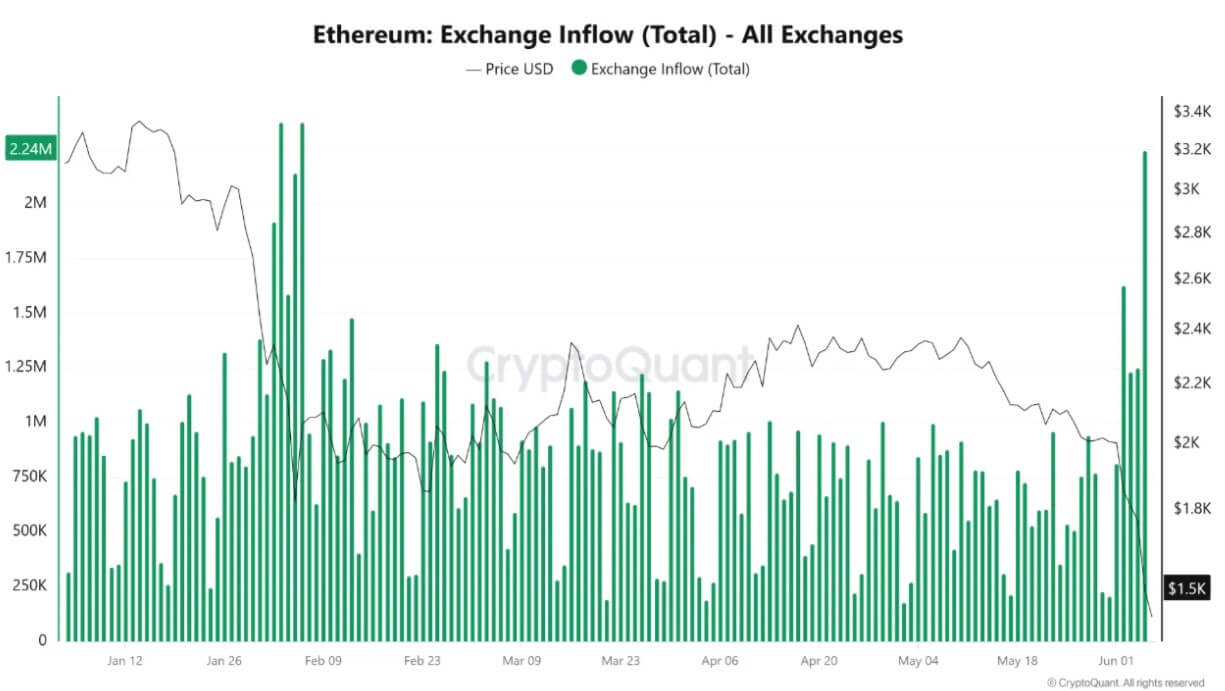

CryptoQuant data show Ethereum inflows to trading platforms climbed to about 2.24 million ETH in a single day, the highest level in four months. Binance accounted for more than 1.16 million ETH of those inflows, representing more than half of the total.

Ethereum Exchange Inflows (Source: CryptoQuant)

This surge in active supply can be seen in high-profile on-chain movements that served as glaring evidence of the liquidity migration.

Notably, a wallet linked to Ethereum co-founder Joseph Lubin awoke after more than three years of dormancy, mobilizing 80,001 ETH, valued at roughly $122 million.

The massive transfer epitomized the broader trend where long-inactive capital breaks from cold storage to seek out active trading venues and liquid architectures amid the mounting market stress.

Large inflows to trading platforms do not automatically mean investors are selling. They can reflect market-making activity, collateral movement, internal transfers, or portfolio restructuring during periods of stress.

However, traders watch the metric closely because coins held on exchanges are easier to sell or use in derivatives activity than coins sitting in private wallets.

The timing has made the increase harder to dismiss. Ethereum was already trading near $1,580 when the inflows accelerated, while Bitcoin had fallen toward $59,000. That combination suggested investors were moving assets during a marketwide reset rather than during a routine period of repositioning.

If exchange deposits remain elevated, the market could face additional short-term volatility.

Derivatives deleveraging deprives market of rebound capital

The velocity of the current crypto market decline has been accelerated by an extensive deleveraging cycle across leveraged futures platforms.

As spot valuations rapidly deteriorated, automated liquidation engines on major exchanges systematically closed out underwater long positions to protect clearinghouse integrity, amplifying organic selling pressure.

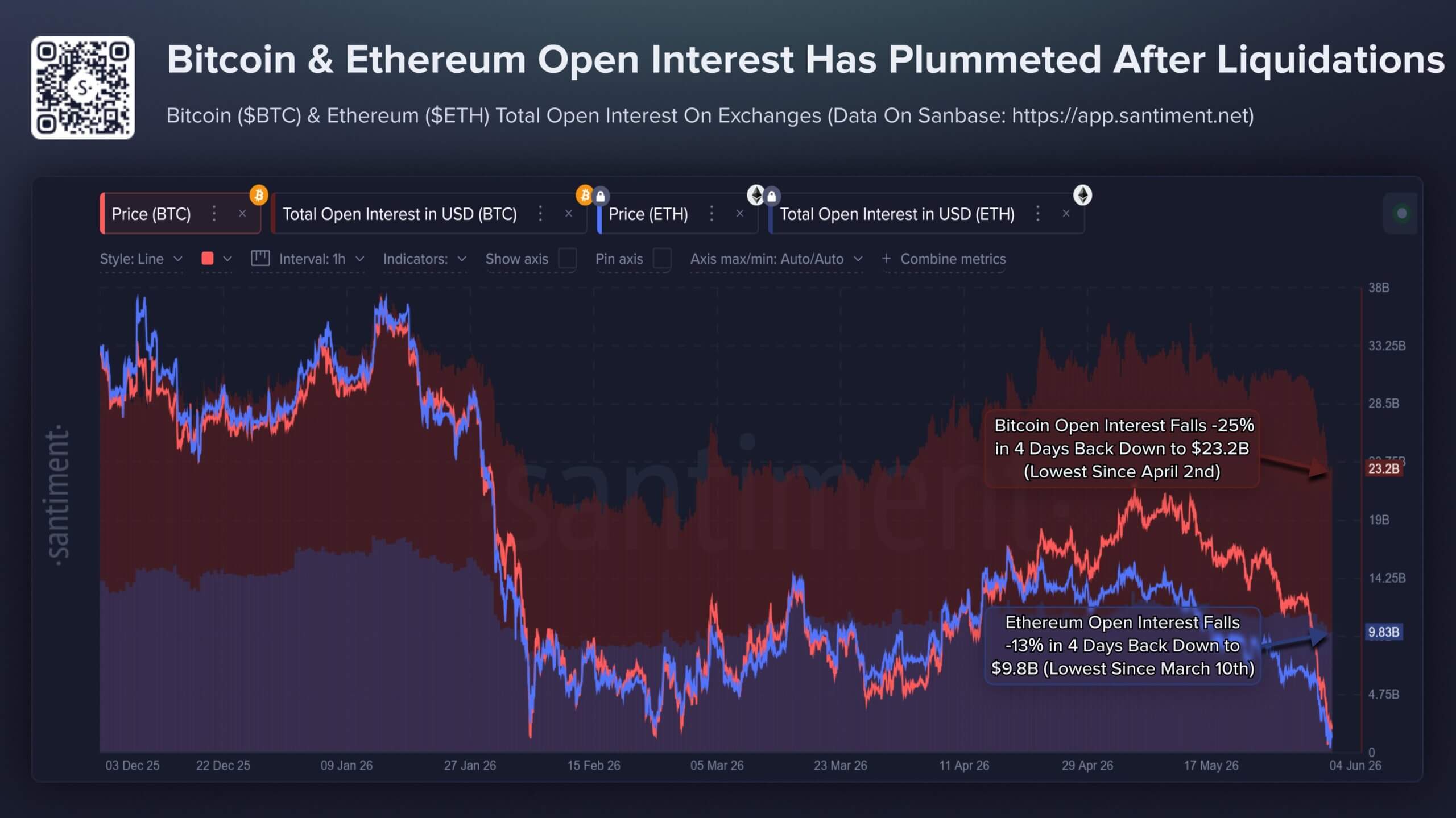

Data analyzed by Santiment illustrates that this liquidation wave effectively flushed out a massive block of speculative capital over a narrow four-day window:

Bitcoin Total Open Interest: Contracted by approximately 25%, dropping to $23.2 billion, which is its lowest operational aggregate since early April.

Ethereum Total Open Interest: Decreased by 13%, settling at $9.8 billion, a structural low point not seen since March.

Bitcoin and Ethereum Open Interest (Source: Santiment)

While this aggressive deleveraging leaves the underlying market structurally healthier by purging speculative excess and over-extended margin, it introduces an immediate liquidity vacuum.

The severe drop in open interest demonstrates that the speculative floor has thinned, leaving the market highly vulnerable to further spot pressure due to the lack of immediate leveraged capital available to front-run a classic V-shaped recovery.

Consequently, retail crowd sentiment has cratered to its most pessimistic footing since mid-February.

The firm noted that social metrics reveal an exponential increase in the phraseology of capitulation, with organic social discussions increasingly pairing terms like “Bitcoin” and “altcoins” alongside terminal descriptors such as “dead,” “finished,” “over,” and “ending.”

Traders hedge for a break below $1,500

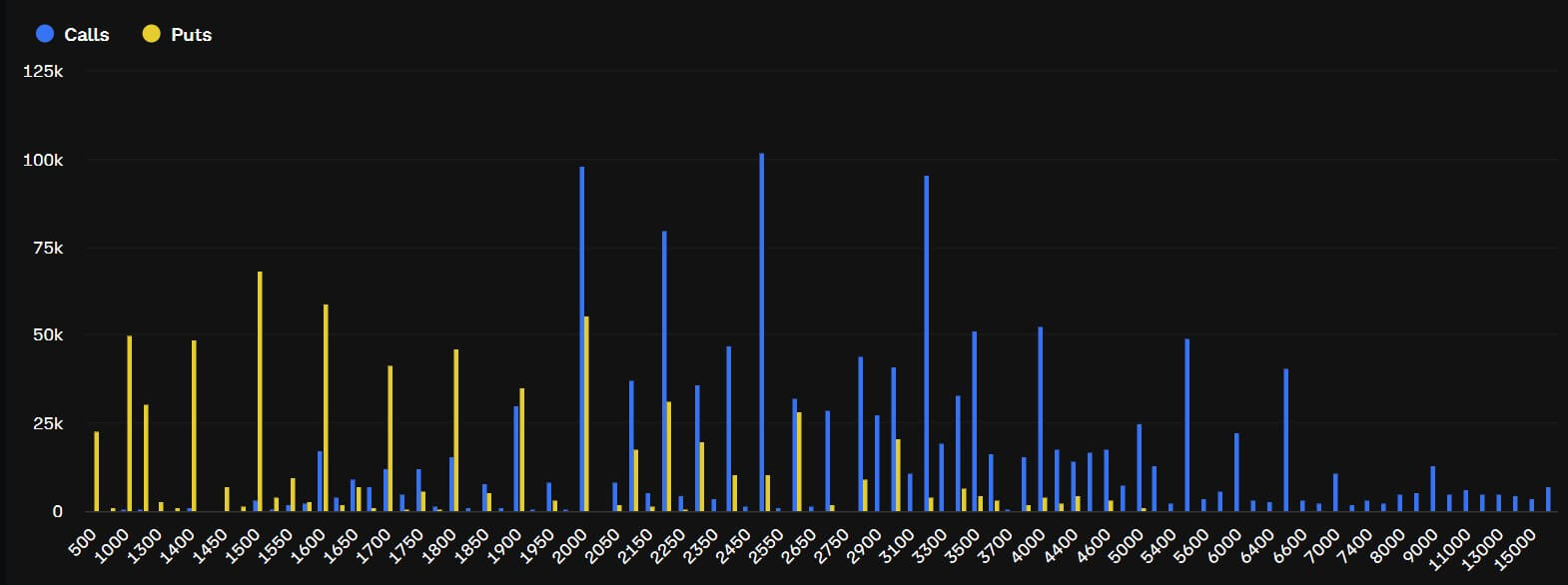

The buildup of stress across ETFs, exchange flows, whale cost bases, and leveraged markets has shifted attention to ETH’s options market, where traders are paying more to protect against another leg lower.

Deribit data show demand for downside protection has increased sharply. The ETH options put-to-call premium rose to 3.7 times on Friday and has shown consistent excess demand for put options since Monday. Put contracts give holders the right to sell at a set price, making them a common hedge when traders expect further losses or want protection against a disorderly move.

ETH’s open interest has clustered around several downside strikes. Traders have built roughly $108 million in open interest around the $1,500 strike, while the $1,400 strike has attracted about $75 million. The $1,000 strike has drawn about $78 million in positioning.

Those levels do not mean the market expects ETH to fall to $1,000 immediately. Instead, they show that traders are paying for protection after several support signals weakened at the same time.

BlockScholes data show the shift has also appeared in volatility pricing. ETH short-dated implied volatility has jumped from a year-to-date low of 36% to 67%, signaling that traders now expect larger near-term price swings.

The move has been accompanied by a sharper skew toward out-of-the-money puts. The seven-day ETH options skew has moved to about -14%, compared with roughly -3% to -4% in late May. Additionally, the demand for puts has also spread across 7-day, 14-day, 30-day, and 90-day maturities.

That broadening shows traders are not just hedging a single event or one short-term move. They are preparing for the possibility that Ethereum’s weakness could extend if ETF outflows continue, exchange inflows stay elevated, and large holders remain below key cost levels.

The next test is whether $1,500 becomes a floor or a trigger. A stabilization in ETF flows and a decline in exchange deposits could help ease pressure.

Without that, the options market’s focus on downside strikes may become the clearest signal of where traders expect the next phase of the selloff to concentrate.

Bitcoin’s latest retreat below $80,000 shows how quickly the bond market has reclaimed control of crypto trading, even after lawmakers advanced one of the industry’s most closely watched regulatory bills.

Data from CryptoSlate showed that the top asset was trading at $79,083 as of press time, down more than 3% after another failed attempt to hold above $82,000.

Blockchain analytical firm Santiment attributed the reversal to a “buy the rumor, sell the news” market reaction to the Senate Banking Committee’s approval of the CLARITY Act. This was a policy milestone that would typically improve sentiment across digital assets by moving market-structure legislation closer to a full Senate vote.

However, the rally attempt faded as traders shifted their focus back to Treasurys.

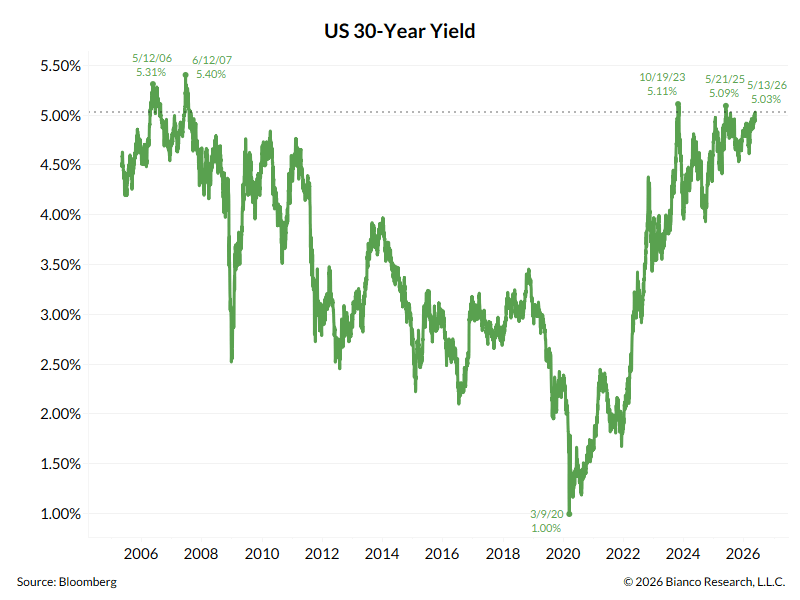

The 10-year Treasury yield moved above 4.5% for the first time since June 2025, while the 30-year yield climbed toward 5.1%. Jim Bianco of Bianco Research said the long bond was only 8 basis points away from a fresh 19-year high.

US 30-Year Yield (Source: Bianco Research)

That move has raised the return threshold for Bitcoin exposure. Higher yields make cash, bills, and longer-dated government debt more competitive, while BTC is trying to recover a key technical level.

Nicolai Sondergaard, a research analyst at Nansen, told CryptoSlate that rising yields are narrowing the compensation investors receive for holding assets such as Bitcoin.

According to him:

“The 10-year Treasury yield pressing toward multi-month highs is compressing the risk premium available to assets like BTC, which remain structurally sensitive to the real rate environment. At current levels, the cost of holding zero-yield assets rises meaningfully when alternatives offer 4.5% risk-free.”

The result is a market where crypto-specific progress is no longer enough to carry price action on its own. Washington has improved the industry’s policy outlook, but the rates market is setting the near-term allocation decision.

ETF outflows show where the rate pressure is landing

SoSoValue data show the funds were on pace for more than $700 million in weekly outflows, the largest weekly retreat since late January. The pullback removes a key source of spot demand as Bitcoin tries to reclaim the $82,000 area and move back above its 200-day moving average.

The ETF channel has become central to Bitcoin’s market structure since the funds began trading, providing institutions with a regulated, liquid way to add exposure. When those flows weaken, the spot market loses one of the clearest sources of marginal demand.

Lacie Zhang, a research analyst at Bitget Wallet, told CryptoSlate that higher yields have made institutional buyers more selective because government debt now offers a stronger return profile.

She said:

“Rising US Treasury yields are acting as a clear macro headwind for Bitcoin. As yields move higher, the relative appeal of government debt improves, raising the opportunity cost of holding a volatile, non-yielding asset like BTC.”

Moreover, the weaker ETF picture is being reinforced by on-chain spot-flow data.

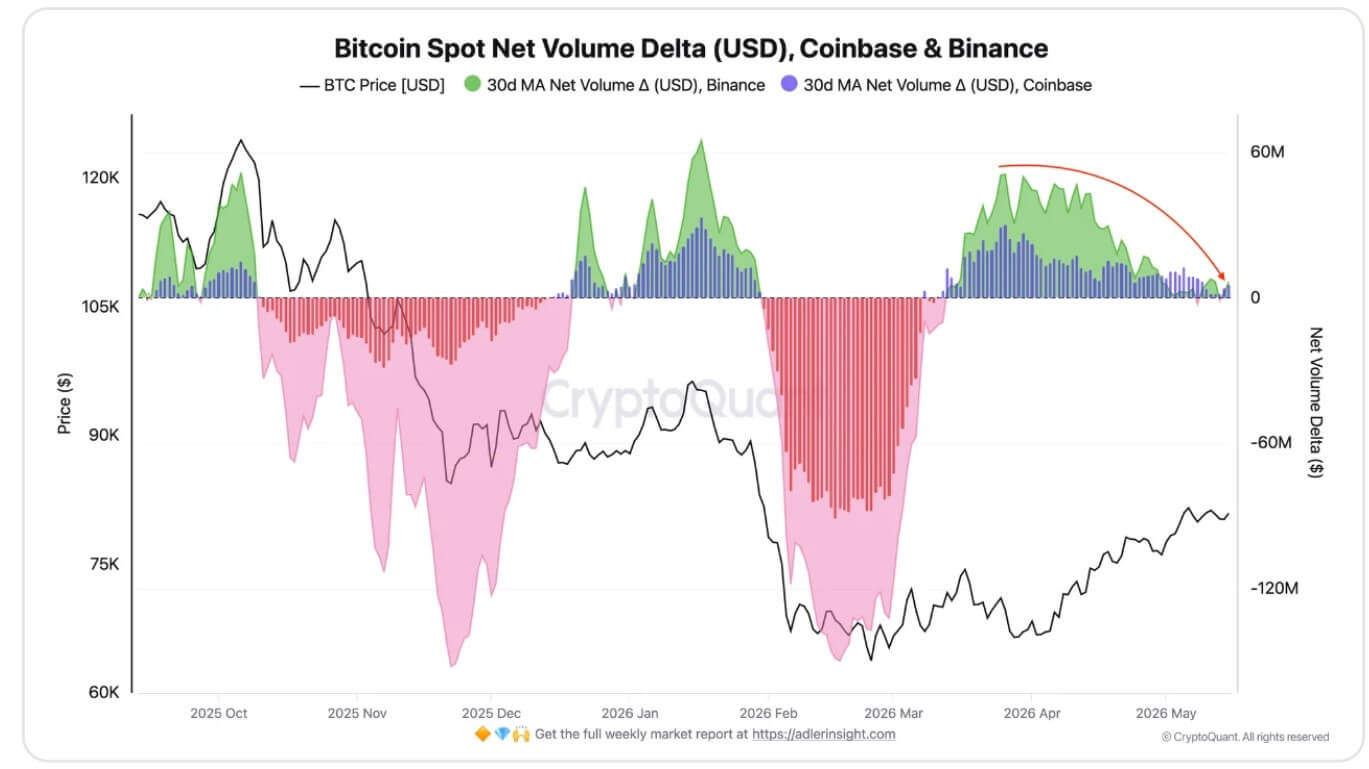

CryptoQuant data show that Cumulative Volume Delta has deteriorated across major venues after stronger readings in March. According to the firm, monthly averages of $50 million on Binance and $30 million on Coinbase have slipped to about $6.5 million and $5.7 million, respectively.

Bitcoin Spot Net Volume Delta on Binance and Coinbase (Source: CryptoQuant)

The indicator also briefly turned negative on May 8, pointing to a weaker balance between buyers and sellers. That leaves Bitcoin trading around a major pivot zone, with thinner spot support than during the earlier phase of the rally.

Moreover, the macro backdrop has also become less supportive for risk assets. The unresolved conflict between Iran and the US has added uncertainty around growth and inflation, even after President Donald Trump initially suggested the conflict would last only a few weeks.

Bitcoin’s hedge case remains longer term

Despite this current market situation, the broader investment argument for Bitcoin has not disappeared.

Analysts at Bitunix told CryptoSlate that while the higher treasury yields can pressure BTC in the short term by draining liquidity and reducing speculative appetite, the same forces could strengthen the case for scarce, non-sovereign assets.

According to the firm, if investors are demanding greater compensation for US deficits, debt issuance, and inflation risk, Bitcoin’s fixed supply could continue to attract buyers looking for an asset outside the sovereign credit system.

However, that argument is more likely to influence long-term strategic allocation than short-term positioning.

For now, Bitcoin appears dependent on two catalysts: a retreat in Treasury yields or a recovery in ETF inflows strong enough to absorb the rate shock.

Without either, price action could remain boxed between support in the upper $70,000s and resistance near $82,000.

Stablecoins and tokenized Treasurys draw cautious capital

In light of the current rate environment, crypto traders are repositioning their capital in the market.

Nansen’s Sondergaard said smart-money wallets have moved incrementally toward stablecoins over the past two weeks, showing a preference for flexibility over directional exposure.

This shift points to caution rather than a full exit from the market as the traders seek fresh market catalysts for their trades.

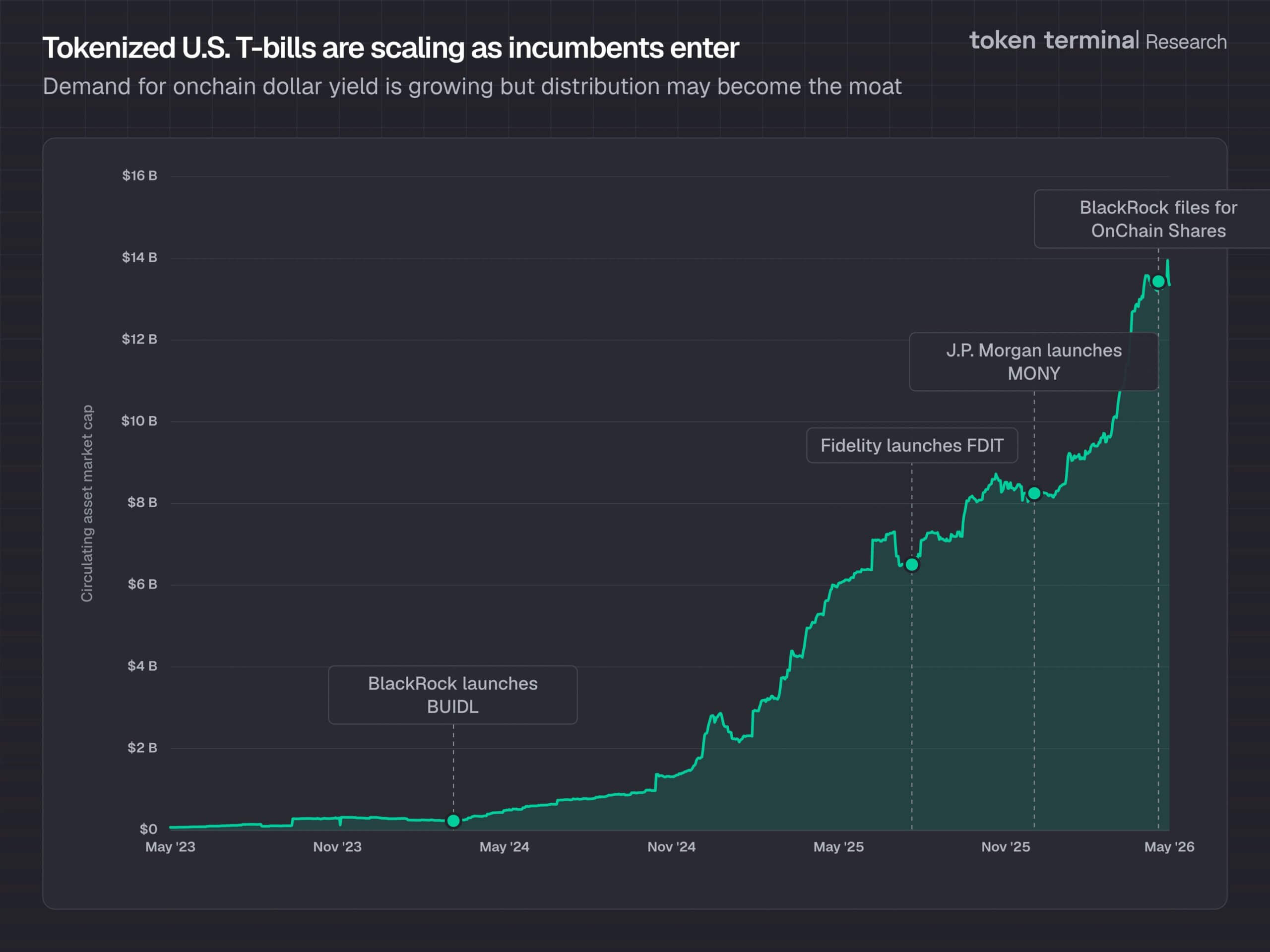

Marcin Kazmierczak, co-founder of RedStone, told CryptoSlate that the risk-free yields above 4% have become a direct competitor to non-yielding assets while strengthening demand for tokenized real-world assets.

Data from Token Terminal shows that tokenized US Treasurys have reached a record high of $15.35 billion in value, up from about $8.9 billion at the start of the year. This represents a 70% growth in under five months.

US Tokenized Treasury (Source: Token Terminal)

According to Kazmierczak, that growth shows capital is still moving through blockchain rails, but with a stronger preference for products tied to short-duration government debt. He added:

“BlackRock BUIDL, VanEck VBILL, Apollo ACRED, Hamilton Lane SCOPE, Franklin Templeton BENJI are all live in production today. Institutions get 4%+ yield with 24/7 settlement, programmable collateral, and composability with DeFi.”

This shift gives the current market cycle a different shape from earlier rate shocks.

Now, Bitcoin is absorbing pressure from a stronger bond market, while another corner of the crypto industry is expanding because that same bond market now offers yield worth tokenizing.

The spot exchange-traded funds tracking the performance of Ripple’s cross-border token continue to dig new lows, as they just ended their first month in the red in March.

The landscape is even more worrying when we examine the details, while XRP is currently losing the battle for the fourth spot against BNB.

XRP ETFs Fall Short

After years of building anticipation, the first spot XRP ETF (Canary Capital’s XRPC) had a highly successful debut day, breaking the launch-day trading volume for 2025. Four more such products followed suit, and they attracted over $1 billion in about a month. Moreover, they didn’t have a single red day in terms of net flows for almost two months before that streak broke on January 7 – something that even the BTC and ETH ETFs couldn’t do.

In November and December, they gained $666.61 million and $500 million, respectively. The before-launch hype seemed justified. However, the following two months were more modest, perhaps driven by quickly escalating global tension. January recorded just $15.59 million in net inflows, while February saw $58.09 million.

The landscape worsened in March as the war-induced tension skyrocketed, oil prices soared, and uncertainty and doubt crept into all financial markets. Investors pulled out $31.16 million from the spot XRP ETFs, making it the first red month since their launch in November last year.

What’s even more concerning is the fact that there were multiple days with no reportable inflows at all. 8 out of the 22 trading days have $0.00 against them on SoSoValue, clearly showing disappearing demand.

Ripple (XRP) ETF Flows. Source: SoSoValue

XRP in Danger

Amid this ongoing investor exodus from the ETFs, the underlying asset has expectedly underperformed, slipping by over 3% weekly. Moreover, XRP now stands inches below the coveted $1.30 support, which, if lost decisively, could lead to more profound corrections.

Popular analyst CW recently warned that a potential drop to $1.26 could trigger mass high-leverage long liquidations.

Fellow analyst CRYPTOWZRD noted that XRP had closed the previous daily candle indecisively and is “teasing the $1.32 intraday resistance.” If it remains below it, the analyst predicted more “weakness and short opportunities.”

ETFs Went From Bad to Worse: First Red Month and No Inflow Days")