Bitcoin pushes toward $65,000 on US inflation relief that may already be fading

Bitcoin approached $65,000 on July 14 as a sharper-than-expected slowdown in US inflation weakened the case for another near-term Federal Reserve interest rate increase.

Data from CryptoSlate showed that BTC rose as high as $64,832 once the report landed, gaining about 4% from its intraday low and coming within $200 of a threshold it has struggled to hold over the past month.

This price performance followed the consumer price index falling 0.4% in June, its largest monthly decline since April 2020, the Labor Department said. Prices were 3.5% higher than a year earlier, down from 4.2% in May and below economists’ forecast for a 3.8% increase.

Core CPI, which excludes food and energy, was unchanged for the month and increased 2.6% from a year earlier. That was also below expectations and marked a slowdown from the 2.9% annual rate recorded in May.

Jake Kennis, senior research analyst at Nansen, told CryptoSlate that the reading represented a clear improvement but stopped short of establishing that inflation was on a sustained downward path.

Kennis said:

“The softness was led largely by energy, which eases near-term pressure on the Fed heading into the July FOMC and helped risk assets bid. That said, this is a cooler print rather than confirmation of durable disinflation.”

The energy decline behind CPI has already reversed

The inflation catalyst could lose force quickly because Bitcoin is responding to an inflation report that accurately describes June, a month whose conditions offer only a rough guide to the price conditions building in July.

This is because the improvement that pushed Bitcoin higher came from an oil market that had changed substantially before the inflation report reached investors.

BLS data show that energy prices fell 5.7% in June, while gasoline prices declined 9.7%, making the largest contribution to the monthly drop in the headline CPI. Those decreases followed a retreat in crude prices as a temporary agreement between Washington and Tehran raised hopes that traffic through the Strait of Hormuz would recover.

That reprieve now has unraveled as the US has reinstated a naval blockade on Iran after Tehran said it had closed the strait, following a third consecutive night of attacks on Iranian targets by US forces, which Iran met by launching missiles at US allies and striking commercial vessels moving through the waterway.

Brent crude rose above $87 per barrel on July 14, then pared its gains, trading near $85. West Texas Intermediate (WTI) found an intraday high at $80.53 after both benchmarks reached their highest levels in about a month.

Patrick De Haan, head of petroleum analysis at GasBuddy, described the June CPI as a “rearview mirror,” saying the decline reflected prices from several weeks earlier, and the latest escalation pushed crude and retail fuel costs higher.

The timing raises the possibility that headline inflation could rebound as July gasoline, diesel, and transportation expenses are incorporated into the data. Higher crude prices could also spread through freight, aviation, agriculture, and manufacturing supply chains.

A renewed energy shock would complicate Bitcoin’s attempt to move through $65,000, as it could revive expectations that the Fed will keep interest rates elevated or raise them again before the end of the year.

Warsh limits the policy relief

Fed Chair Kevin Warsh told lawmakers on July 14 that monthly price fluctuations were inevitable, particularly in an unsettled global environment.

He said the central bank had no tolerance for persistently elevated inflation and stayed committed to restoring price stability.

According to Warsh:

“The Fed’s number one objective is to get monetary policy right—or as near to it as we possibly can. That is our clear and constant aim, the star we steer by. And if we get policy right—and we will—the inflation surge of the last five years will be a thing of the past.”

The Fed held its benchmark rate at 3.5%-3.75% in June after several officials raised concerns that energy costs could keep inflation elevated. The July 14 report weakened the case for a July increase, leaving the outlook for September and later meetings still unresolved.

Warsh described the CPI report as one data point and rejected the suggestion that it represented “mission accomplished.”

The restraint also limited how far traders could extend the post-CPI rally on expectations of easier monetary policy, and Bitcoin stayed below the resistance area that has capped several recovery attempts since June.

Bitcoin’s $65,000 attempt faces an oil test

Bitcoin must now convert its post-CPI advance into a sustained move through the $65,000-$66,000 resistance area, building on the momentum it is forming.

BTC held near $62,000 through repeated US attacks on Iran and avoided the broad liquidation cascade that followed earlier geopolitical shocks.

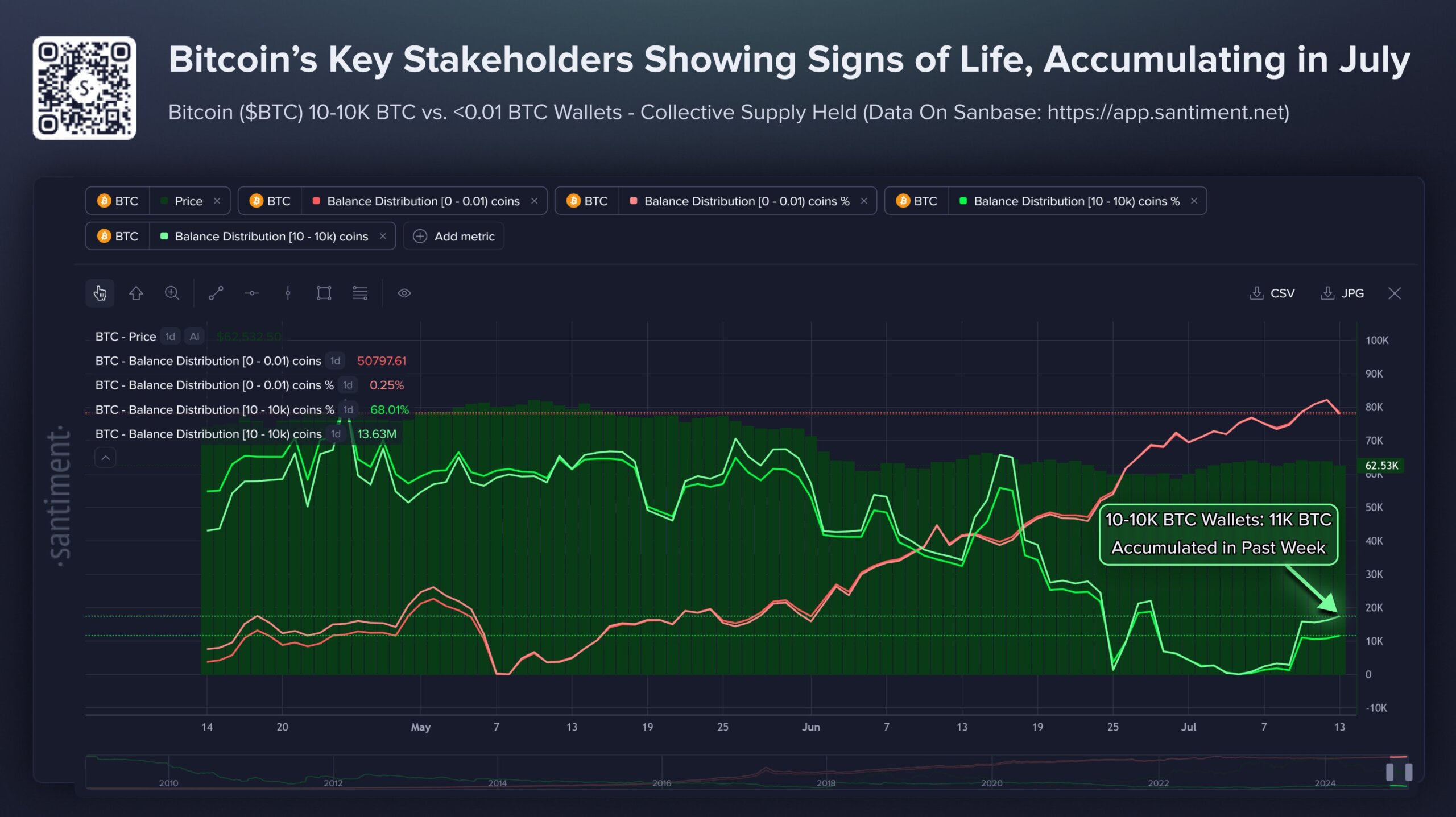

Data from Santiment also showed that key Bitcoin stakeholders were exhibiting bullish behavior and accumulating the top crypto.

According to the firm:

“Wallets holding 10–10,000 BTC have added roughly 11,000 BTC over the past week, a meaningful shift because this tier of whales and sharks has historically tracked closely with price direction. Small retail wallets are still mainly accumulating too, which shows dip-buying interest remains alive even after weeks of volatility.”

That accumulation helped Bitcoin respond quickly when CPI weakened the dollar and Treasury yields, and it could also provide support if higher oil prices begin challenging the inflation outlook again.

Lacie Zhang, a research analyst at Bitget Wallet, told CryptoSlate that the CPI report provided the liquidity-driven catalyst Bitcoin needed to break higher, noting that renewed disruption around the Strait of Hormuz made the advance more vulnerable to reversal.

She placed near-term support at $62,000 to $63,000 and resistance at $65,000 to $66,000, and a sustained break above that zone would take Bitcoin beyond the range that has contained it through much of June and July.

Such a move may require an easing of oil tensions, further ETF inflows, or a softer policy signal from the Fed, which could give buyers the confidence needed to absorb profit-taking near $65,000.

Renewed attacks around the Strait of Hormuz would keep the oil-risk premium elevated. Higher fuel costs could lift inflation expectations, restore bets on another rate increase, and weigh on Bitcoin before it establishes support above the resistance zone.

The post Bitcoin pushes toward $65,000 on US inflation relief that may already be fading appeared first on CryptoSlate.