Ethereum (ETH) whales keep adding to their holdings while the price trades near $1,963, up 4.3% in the last 24 hours. Three separate datasets now point to an accumulation two weeks after ETH broke its long-term descending trendline.

Glassnode data shows growing whale addresses, and US spot ETF flows have turned positive. However, one metric still refuses to confirm the recovery.

Ethereum Whales Grow Their Ranks at Yearly Lows

Glassnode’s whale address count tracks wallets holding between 1,000 and 10,000 ETH. The metric bottomed near 4,750 addresses in early June and has since climbed toward 4,850.

Meanwhile, the 30-day change has stayed positive through most of July. This suggests sustained accumulation rather than a short-lived spike.

The timing separates this move from October 2025. Back then, Ethereum whales spiked while ETH traded near its record high, and the rally reversed soon after. This time, large holders are buying close to yearly lows.

Fresh wallets also bought 50,000 ETH in mid-July as the ETH/BTC ratio jumped 6%. A flip of the 30-day change back below zero would weaken the signal.

ETF Inflows Return After 8 Weeks of Outflows

Institutional flows tell a similar story. US spot Ethereum ETF net flows flipped positive in July after roughly eight weeks dominated by outflows.

The funds have now recorded a third straight week of inflows, adding $103.9 million in the week ending July 24. Green bars have dominated the Glassnode flow chart throughout the month.

Still, the scale remains modest. Daily inflows sit in the tens of millions, far below the $600 million to $1 billion days of August 2025. Institutional demand is returning, not surging.

A return of sustained daily outflows would flip this signal back to bearish.

Active Addresses Remain the Missing Piece

Network activity complicates the bullish setup. The 14-day moving average of Ethereum active addresses sits near 400,000, according to Glassnode.

That reading stands far below the February 2026 spike near 800,000. It also trails the June local peak of roughly 460,000. In other words, accumulation is not yet backed by growing usage.

Crowd sentiment has also turned deeply bearish, although Santiment treats such readings as contrarian signals. The previous two pessimism extremes preceded ETH rebounds.

ETH Price Prediction as $2,000 Caps the Breakout

The daily chart shows why these signals matter now. A descending trendline from the August 2025 record high rejected the ETH price five times before the mid-July breakout, which came with futures open interest near $19.8 billion.

The price has held above the broken trendline for two weeks. It now presses into the resistance zone just below $2,000, a level with clear psychological weight.

A confirmed daily close above $2,000 could open the way toward the 0.618 Fibonacci retracement at $2,438. That target sits about 24% above the current price and overlaps the supply zone from May.

However, rejection remains possible. In that scenario, ETH could retest the 0.786 Fibonacci level at $1,754 and the broken trendline near $1,600. The green demand zone in that area has supported the price before.

Volume keeps declining during the recovery, which fits an accumulation phase but leaves the breakout unconfirmed. Either the whales, the ETFs, and the chart pull the price through $2,000, or ETH revisits the zone that launched this move.

Our Bitcoin price prediction expects BTC’s price to reach $150K by the end of 2026 due to the bullish sentiment following the halving event.

By 2032, BTC might touch $350,548 following increased institutional adoption.

Bitcoin’s outlook for 2026 has become highly debated. The approval of spot Bitcoin ETFs and the rally after the halving were expected to bring more clarity, but instead they’ve brought mixed volatility in Bitcoin price forecast.

However, top analysts are bullish on BTC price prediction this year. Charles Hoskinson, the founder of Cardano, has predicted that Bitcoin could reach about $250,000 by 2026. He bases this view on Bitcoin’s limited supply and the possibility that institutions and major companies will continue to adopt it. Investor and author Robert Kiyosaki has made a similar prediction, arguing that Bitcoin’s scarcity makes it a strong store of value in a world where traditional currencies are becoming less stable.

As Bitcoin’s on-chain activities surge, questions arise, such as: “Does Bitcoin have the potential to hold above the $100K mark?” or “Will Bitcoin go up?” or “Where will Bitcoin be in 5 years?” Let’s answer them using our Bitcoin price prediction 2026 model.

Overview

Cryptocurrency

Bitcoin

Ticker

BTC

Price

$64,962 (+0.5%)

Market capitalization

$1.42 Trillion

Trading volume (24-hour)

$52.53 Billion (+7%)

Circulating supply

20 Million BTC

All-time high

$124,457; August 14, 2025

All-time low

$0.04865; Jul 15, 2010

24-hour high

$65,621

24-hour low

$64,744

Bitcoin price prediction: Technical analysis

Metric

Value

Current Price

$64,962

Price Prediction

$ 67,003 (+1.61%)

Fear & Greed Index

19 (Extreme Fear)

Sentiment

Bearish

Volatility

3.25% (Medium)

Green Days

12/30 (40%)

50-Day SMA

$ 67,794

200-Day SMA

$ 75,112

14-Day RSI

43.82 (Neutral)

Bitcoin price analysis

TL;DR Breakdown:

BTC price analysis shows that buyers are pushing the price toward $65K

Resistance for BTC is at $65,569

Support for BTC/USD is at $64,405

The BTC price analysis for 27 July confirms that BTC faces buying pressure as BTC surges toward $65K. Currently, the Bitcoin price is aiming to hold above $65K.

Analyzing the daily Bitcoin price chart, we see that Bitcoin faces bullish pressure as it surges toward $65K. Currently, the BTC price is facing short-liquidation around immediate resistance channels. The 24-hour volume has surged to $943 million, showing a surge in trading interest today. BTC is trading at $64,962, surging by over 0.5% in the last 24 hours.

The RSI-14 trend line hovers around 53, hinting that a strong bullish pressure is on the way. The SMA-14 level suggests volatility in the next few hours.

BTC/USD 4-hour price chart: Selling domination rises around EMA trend lines

The 4-hour Bitcoin price chart suggests that sellers are strengthening their position to hold the price below the EMA trend lines. Currently, sellers are strongly defending a recovery.

The BoP indicator trades in a positive region at 0.74, showing that short-term buyers are taking a chance to accelerate an upward trend.

Additionally, the MACD indicator has formed green candles above the signal line and the indicator aims for positive momentum, strengthening long-position holders’ confidence.

Bitcoin technical indicators: Levels and action

Daily simple moving average (SMA)

Period

Value

Action

SMA 3

$ 60,096

BUY

SMA 5

$ 60,036

BUY

SMA 10

$ 60,393

BUY

SMA 21

$ 62,482

SELL

SMA 50

$ 67,794

SELL

SMA 100

$ 71,181

SELL

SMA 200

$ 75,112

SELL

Daily exponential moving average (EMA)

Period

Value

Action

EMA 3

$ 60,652

BUY

EMA 5

$ 60,448

BUY

EMA 10

$ 60,800

BUY

EMA 21

$ 62,305

SELL

EMA 50

$ 66,195

SELL

EMA 100

$ 69,980

SELL

EMA 200

$ 76,481

SELL

What to expect from BTC price analysis next?

The hourly price chart confirms that Bitcoin is attempting to drop below the immediate support line; however, bulls are eyeing a recovery rally in the coming hours. If BTC’s price holds momentum above $65,569, it will fuel a bullish rally to $66,997.

If bulls fail to initiate a surge, the BTC price may drop below the immediate support line at $64,405, beginning a bearish trend to $63,241.

Is Bitcoin a good investment?

The rising institutional demand for Bitcoin etfs makes it a good investment option in the crypto market. However, Bitcoin has a short investment history filled with very volatile market value. Whether it is a good investment depends on your financial profile, investment portfolio, risk tolerance, and investment goals. It is suggested to conduct investment advice of the financial markets and understand the financial system risks.

Why is Bitcoin up today?

Bitcoin faced a surge in buying pressure as buyers pushed the price above immediate fib levels around $66K.

Will the BTC price reach $100K?

Bitcoin price broke its much-anticipated mark of $100K, aiming for a new ATH. The price currently prepares to maintain its buying demand above $100K.

Will BTC reach $1 million?

$1 million is a significant milestone for the BTC price. However, it is achievable if Bitcoin continues to attract institutional interest in the coming years.

Is Bitcoin a good long-term investment?

As several institutions continue to accumulate BTC and Bitcoin faces a rise in global recognition, Bitcoin has a solid long-term future.

Recent news/opinions on BTC

As reported by Cryptopolitan, JPMorgan Chase & Co. is concerned that Strategy’s new policy of selectively selling its Bitcoin holdings will introduce new risk to the crypto market.

Bitcoin price prediction July 2026

Bitcoin’s price dropped toward $60K in June. However, it is now facing minor accumulation, which could mean we’ll see a recovery around July 2026.

Bitcoin’s price might attempt to maintain an average price of $75,000 and be pushed further, at least $80,000 if strong downward pressures are not seen. However, we might see a rejection on the bearish side, leading to a consolidation at around $60,000.

Bitcoin Price Prediction

Potential Low

Potential Average

Potential High

Bitcoin Price Prediction July 2026

$60,000

$75,000

$80,000

Bitcoin price prediction 2026

Historically, Bitcoin has been a significant crypto coin in the years following a halving, and it is expected to push up its price after a downturn in 2025. Bitcoin miners might play a crucial role in holding bullish sentiment for future price movements.

Spot Bitcoin ETFs are projected to be a key driver of Bitcoin prices and the broader cryptocurrency market in 2026. As a result, Bitcoin’s trajectory might follow a bullish trend ahead with rising treasury term premium.

Furthermore, there is an increasing bullish sentiment that the base interest rates could be cut in the US, and thus, help to further the upward movement of Bitcoin. An outcome of which the 2026 year could be positive for Bitcoin, with its crypto-price perhaps touching $150,000 at the highest and the low could be around $48,000.

Bitcoin Price Prediction

Potential Low

Potential Average

Potential High

Bitcoin Price Prediction 2026

$48,000

$100,000

$150,000

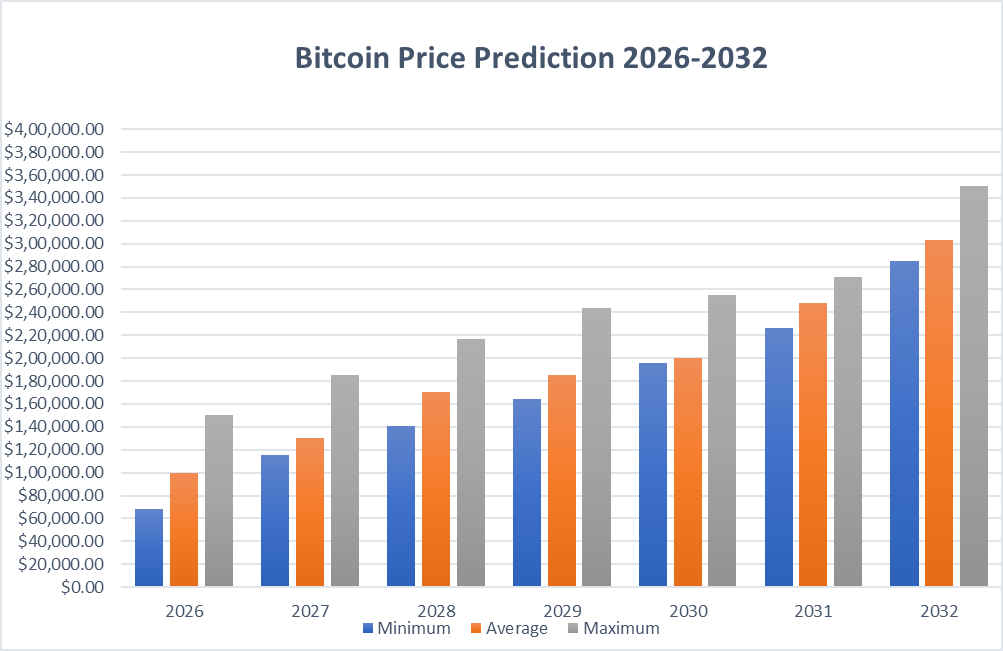

Bitcoin Price Predictions 2027-2032

Year

Minimum Price

Average Price

Maximum Price

2027

$115,000

$130,000

$185,000

2028

$140,491

$170,100

$216,738

2029

$164,063

$185,068

$244,142

2030

$195,629

$200,312

$255,321

2031

$225,903

$248,568

$270,593

2032

$285,058

$303,555

$350,548

Bitcoin price prediction 2027

Bitcoin might witness slow growth after 2025’s Bitcoin halving surge, resulting in a surge in selling pressure. However, more financial products including a surge in ETF flows might hold BTC prices within a bullish region. The digital assets market sentiment shows bullish signals for Bitcoin hit new highs. As the overall sentiment gives a bullish outlook, one should research more about Bitcoin before investing.

We might see a maximum price of $185,000, with a minimum price of $115,000 and average price of $130,000.

Bitcoin forecast 2028

Based on a detailed technical analysis of past Bitcoin price movements, it is projected that in 2028, Bitcoin could see a minimum price of $140,491. The potential maximum price is estimated to be $216,738, with an average closing price of $170,100.

Bitcoin price prediction 2029

By 2029, Bitcoin’s price is expected to reach a low of $164,063. Maximum price projections are as high as $244,142, averaging about $185,068 for the year.

Bitcoin price forecast 2030

Projections for 2030 suggest that Bitcoin could be valued at a minimum of $195,629. The price may peak at as much as $255,321, with an average throughout the year expected to be around $200,312.

Bitcoin (BTC) price prediction 2031

The forecast for 2031 suggests that Bitcoin’s price could start at a minimum of $225,903 and potentially rise to a maximum of $270,593. The average price is anticipated to stabilize at about $248,568 throughout the year.

Bitcoin price prediction 2032

The forecast for 2032 suggests that Bitcoin’s price could start at a minimum of $285,058 and potentially rise to a maximum of $350,548. The average price is anticipated to stabilize at about $303,555 throughout the year.

A surge in bitcoin adoption and the expansion of the Bitcoin ecosystem might end the controversy of “Bitcoin bubble” in future. This might boost the Bitcoin cost and strengthen the Bitcoin network. At Cryptopolitan, we are bullish on Bitcoin’s future price as the historical market sentiment is extremely impressive. By the end of 2026, Bitcoin might record a maximum of $150,000, with a minimum price of $48,000 and an average price of $100,000.

However, Bitcoin’s future market potential entirely depends on its buying demand, regulation, and investor sentiment regarding long-term holdings. Crypto analysts provide a positive sentiment as macroeconomic trends turn promising.

We expect Bitcoin price to surpass a high of $216,738 by the end of 2028.

Bitcoin historic price sentiment

BTC price history: Coinmarketcap

Satoshi Nakamoto created Bitcoin in 2009, marking the first use of blockchain technology.

Bitcoin was initially of little value, gaining significant traction and hitting over $15,000 during the 2017 boom, with further highs reached in 2019 and 2021.

In 2021, Bitcoin peaked at $68,789.63 but dropped to $15,760 by December 2022 amid economic pressures, including inflation and geopolitical conflicts.

By April 10, 2023, Bitcoin’s price surged 83%, breaking the $30,000 resistance level.

Throughout mid-2023, Bitcoin’s value hovered around $30,000, nearly reaching $32,000 due to positive market sentiments and potential ETF approvals.

Bitcoin experienced a significant price drop in mid-August 2023, falling to $25,000. However, its prices remained volatile, fluctuating between $26,000 and $29,500 in October.

Bitcoin closed 2023 above $42,000, a 155% increase from the year’s start.

In early 2024, Bitcoin rose above $45,000 on ETF anticipation but briefly dipped below $40,000 after approvals. It broke its 2021 all-time high in March, reaching $73,750.07 on March 14, before dropping below $60,000 in April. May saw another surge above $70,000, while June and July brought heavy fluctuations between $70K and $55K.

Bitcoin rallied to $66K in September after a Fed rate cut, climbed to $70K in October’s Uptober rally, and surged toward $108K following Donald Trump’s victory in the November US elections. BTC ended 2024 consolidating below $95K.

At the start of January 2025, BTC was trading between $92,788.13 and $95,824.39. However, it formed an ATH at $109,114 on January 20.

In the weeks of February, the price of BTC dropped heavily as it dropped toward the $78K low.

In March, the price of Bitcoin declined heavily and dropped toward a low of $76.6K. In April, the price of Bitcoin started recovering. By the end of April, it neared the critical $95K zone.

In May, Bitcoin price skyrocketed and it formed a new ATH at $111,970. However, the price declined later, toward $104K.

By the end of June, BTC price reclaimed the $108K level.

In July, BTC price triggered a surge toward $123K; however, it faced strong selling pressure later.

In mid-August, the price of Bitcoin surged above $124K. However, the price failed to maintain its momentum as it dropped below $110K in early-September.

By the end of September, the price of Bitcoin dropped further and touched a low around $108K.

In October, the price of Bitcoin crashed heavily below $110K. The price crashed further toward $84K in November.

Bitcoin ended December 2025 on a bearish note by trading below $90K.

Bitcoin price further dropped in January 2026 as it crashed toward $77K. In February, the price of BTC hit a low at $60K.

BTC price continued to face bearish pressure in March. However, it surged above $70K in early April. By the end of April, BTC price surged toward $80K.

By the end of May, the price of BTC dropped toward $73K. In June, BTC dropped toward $60K.

The XYO ecosystem just took another major step onto the institutional stage.

Both $XL1 and $XYO are now listed by Crypto.com — bringing institutional-grade

custody and deep liquidity to the two tokens at the heart of everything XYO builds.

Powers the network’s operations, incentivizing nodes to securely gather and validate real-world location and geospatial data.

$XL1

The utility token of the XYO Layer One blockchain — powering transactions, gas fees, and core network infrastructure.

Custody & Liquidity

Crypto.com will provide institutional-grade custody and liquidity solutions for both tokens through

Crypto.com Custody — a regulated infrastructure that includes cold storage with enhanced security,

transparent audit trails, and streamlined compliance processes. Institutional clients gain immediate

access to Crypto.com’s deep liquidity pool for fast, reliable, and cost-efficient conversions.

Trusted by millions of users worldwide, Crypto.com is an industry leader in regulatory compliance,

security, and privacy — giving builders and enterprises confidence in the foundation they’re building on.

$20B

Crypto.com valuation after recent institutional round

$400M

Funding raised with Citadel Securities participation

2018

Year XYO began building its proof infrastructure

Traditional Finance Meets DePIN

The timing is significant. Crypto.com recently achieved a $20 billion valuation during

an institutional funding round of $400 million with Citadel Securities. The move has been widely

seen as evidence of the growing interest in digital assets from traditional finance institutions —

and XYO is now positioned squarely alongside those players.

A Relationship Built Over Years

For XYO, this partnership builds on a relationship that goes back years.

“We’ve had a great relationship with Crypto.com since listing XYO on their exchange, and expanding

into custody for XL1 and XYO together is a natural next step. As we build out infrastructure for AI,

robotics, and decentralized machine intelligence, having our digital assets XYO and XL1 backed by

enterprise-grade security is essential. Working with one of the most trusted names in the industry

positions XYO alongside the institutional players shaping what comes next, and gives builders and

enterprises confidence in the foundation they’re building on.”

— Markus Levin, Co-Founder, XYO

The Foundation Ahead

XYO has been building since 2018, delivering the proof infrastructure that powers geospatial,

robotics, AI, and decentralized compute applications — operating one of the largest consumer

DePIN networks in production. Institutional-grade custody for XYO and XL1 strengthens that

foundation and signals where the network is headed next.

With Crypto.com Custody now safeguarding both tokens, institutions have a secure and compliant

way to hold and manage the assets behind verifiable real-world data at scale.

Get Involved

Eligible institutions and high-net-worth clients can submit a custody inquiry, or learn more about the XYO and XL1 tokens.

The Transparent Prop Firm | CryptoCoinShow Exclusive

PROPR ◆ ONCHAIN PROP TRADING$1M REVENUE IN 60 DAYS5,000+ ACTIVE TRADERS300+ AI AGENTS LIVE80% PROFIT SPLITHYPERLIQUID INFRASTRUCTUREPOLYMARKET INTEGRATION IMMINENTMMT.GG PARTNERSHIP LIVEALGO PASS RATE: 15% VS HUMAN 13.5%PROPR ◆ ONCHAIN PROP TRADING$1M REVENUE IN 60 DAYS5,000+ ACTIVE TRADERS300+ AI AGENTS LIVE80% PROFIT SPLITHYPERLIQUID INFRASTRUCTUREPOLYMARKET INTEGRATION IMMINENTMMT.GG PARTNERSHIP LIVEALGO PASS RATE: 15% VS HUMAN 13.5%

CryptoCoinShow

Exclusive Feature

July 2026 · Blockchain Interviews

Deep Dive · Prop Trading · DeFi Infrastructure

The Prop Firm That Shows Its Work

While every other prop trading firm hides its books, changes the rules when you start winning, and denies payouts it can’t afford — Propr built the whole thing onchain, in public, for anyone to audit in real time. Louis Régis, former Credit Suisse quant and Rothschild crypto desk head, explains why that’s the only model that survives.

By Ashton Addison · CryptoCoinShow Blockchain Interviews · Exclusive

▶ WATCH THE FULL INTERVIEW

$1M+Revenue · 60 Days

5,000+Active Traders

300+AI Agents Live

80%Profit Split

Onchain Verified · Transparency Dashboard Live

Prop trading is a quiet $10 billion industry in traditional finance. Hundreds of thousands of retail traders pay entry fees for the chance to trade a firm’s capital — keeping a cut of the profits if they succeed, absorbing nothing if they fail. The firms collect the fees, manage the risk, and pocket the spread. It’s a clean business model. It’s also almost entirely absent from crypto.

Louis Régis wants to know why — and he thinks he’s found the answer. “The breakthrough is liquidity,” he says. “For retail traders, it’s now very close to on par with traditional venues. You can trade the Nasdaq and S&P on Hyperliquid, and the spread and execution quality will be similar to TradFi. That’s the building block Propr is built upon. The constraint that killed earlier attempts — dYdX, GMX — was simply that the liquidity wasn’t there.”

Régis is not a crypto-native. He spent years as a quantitative analyst at Credit Suisse, then ran the crypto desk at Rothschild & Co before leaving to build Propr. He now codes the platform live on Twitch every day. Two and a half months after launch: $1 million in revenue, over 5,000 active traders, and more than 300 AI agents already trading with real funded capital.

Propr — Platform Snapshot · July 2026

Revenue (since launch)$1,000,000+

Active Traders5,000+

AI Agents Live300+

Max Funded Capital$300,000

Profit Split (trader)80%

Human Pass Rate13.5%

Algo Pass Rate15.0%

Execution VenuesHyperliquid + Lighter

InfrastructureOnchain · Fully Auditable

Upcoming IntegrationsPolymarket · MMT.gg

01 — The ProblemThe Black Box Business Model

To understand why Propr exists, you have to understand what the rest of the prop trading industry is doing wrong. The mechanics are straightforward: a firm charges a trader a fee — typically between $500 and $1,000 — for the right to attempt a funded challenge. Pass the challenge, get access to real capital. Make profits, keep a share. Sounds fair. The problem, Régis explains, is what happens when you actually start winning.

“If a firm is denying payouts, it’s about the economics of the firm. If they have rules that are too loose and don’t practice good risk management, it’s not good for them. This will still occur onchain — we already see it in quite a lot of onchain counterparts.”

Louis Régis, Founder — Propr

When a trader becomes consistently profitable, a traditional prop firm faces a problem: they now owe that person real money. If the firm has been internalizing trades — acting as the counterparty rather than hedging — a winning trader is a direct loss. The response, documented across the industry, is quiet rule-tightening: consistency requirements that materialize mid-campaign, payout delays, account flags. The rules weren’t changed officially. They were just applied differently.

Régis’s solution is deceptively simple: put the economics onchain so anyone can see them. “A very simple metric is the payout-to-revenue ratio,” he says. “If you have more payouts than revenue, it’s not sustainable in the medium term. That’s something you can now verify on onchain platforms. On Propr, you can audit that the firm is profitable and see the margin we have deployed to all traders — in real time. No other firm has this level of transparency.”

02 — The InfrastructureWhy Hyperliquid — and Why Lighter Is Coming

The choice of Hyperliquid as Propr’s primary infrastructure wasn’t sentimental. “It’s all a function of liquidity,” Régis says. “Hyperliquid is actually very expensive as a trader. But the spread and depth is so much greater than other venues that it makes sense.” When you’re running a book with large open interest, execution quality matters more than fee minimization. A firm that needs to enter or exit a position quickly can’t afford slippage. Fees are secondary.

But Propr already hedges across both Hyperliquid and Lighter — and Régis is candid about where each wins. On a $1 million position, Lighter’s spread-only model (no fees) costs roughly $400 in execution versus $700 on Hyperliquid. For retail traders doing high-frequency intraday work, that gap matters. For larger wallets trading with more capital, Hyperliquid’s depth is worth the premium.

“We don’t really care about the end venue. We go wherever the execution is best. The only thing that matters to us is: on a 1 million to 10 million order, what’s my slippage on any given asset?”

Louis Régis, Founder — Propr

The longer view is aggregation. Régis sees the perpetuals DEX landscape evolving the same way spot DEX aggregators like LlamaSwap did — routing volume to wherever execution is most efficient rather than locking into a single venue. “We’ll value perp DEXes based solely on execution quality, just like we view AMMs today,” he says. “I think that’s coming very soon.”

03 — The ExpansionPolymarket and the Prediction Market Thesis

Propr’s tagline is “get funded, trade anything.” Anything tradable onchain, Régis wants to offer prop trading infrastructure for. The next frontier: Polymarket. At the time of filming, Propr was days away from launching on the prediction market platform — a move that required building entirely new risk management frameworks from scratch.

“Risk management for Polymarket is actually a lot harder than for Hyperliquid,” Régis says. “It’s a fundamentally different structure.” Prediction markets resolve on events, not prices. The question of how and when to resolve a market — and who has the authority to challenge that resolution — is one Polymarket itself is still working through. Propr’s position: mirror Polymarket’s resolutions exactly, without taking a position. “If the market doesn’t resolve a trade, we don’t have the authority to say the market is wrong.”

04 — The SignalAI Agents Are Beating Human Traders

The most unexpected development at Propr isn’t the revenue or the trader numbers. It’s the bots. Over 300 AI agents are currently trading with funded capital on the platform — and they’re outperforming humans on the metric that matters most: the challenge pass rate.

Human Traders

Emotional decision-making under pressure

Stop-losses moved on impulse

Inconsistent rule adherence

Struggle with risk-first discipline

Reactive to market noise

AI Agents / Algos

Zero emotional interference

Strict stop-loss enforcement

Consistent rule execution

Risk-reward filtering built-in

Only takes trades that meet criteria

13.5%Human Pass Rate

15.0%Algo Pass Rate

“The number one trader on our platform is a bot — not a human,” Régis says. The economics make sense for algo builders: for $500, you can get exposure to $100,000 in capital. No developer wants to deploy an algorithm on $100,000 of their own money to test it. Prop funding provides implied leverage that makes the math work at every scale.

The agent builders coming to Propr aren’t all quants. Claude and Gemini have democratized programming to the point where retail traders with a back-tested edge can now automate it without a software background. Propr sees three distinct customer types: amateur traders bootstrapping their first algos with LLMs; sophisticated quantitative players; and small market makers using the firm’s infrastructure to deploy strategies. Platform integrations — like Nick.ai, where anyone can build a bot — are adding a fourth channel that Régis expects to dominate within a year.

“We have pretty strong conviction that AI agent traders will be the far majority of our users in the next six months to a year.”

Louis Régis, Founder — Propr

05 — The Platform PlayMMT.gg and the Funding Layer Thesis

Propr’s most significant announcement at time of publication: a full integration with MMT.gg, one of the largest order-flow tools in crypto. The implication is architectural. For the first time, traders using an existing platform they already know can access prop-funded capital without visiting Propr’s interface at all.

Régis draws the analogy to Hyperliquid’s own distribution expansion — embedded now inside Phantom, MetaMask, and dozens of other interfaces. “Think of the same happening for prop funding,” he says. “Propr will be the main supplier of this equity. You embed the capital layer the same way you embed the execution layer.”

If the thesis holds, Propr isn’t just a prop trading firm. It’s infrastructure — a funded capital primitive that any trading terminal, agent platform, or prediction market can plug into. The transparency dashboard at propr.xyz/transparency is already the clearest demonstration of what that looks like in practice: real-time hedging activity, daily P&L, affiliate payout ratios, and organic versus referral traffic breakdowns — all public, all verifiable, all the time.

“See how much money we make — and if we lose on a given day, you see how much we lose,” Régis says. “No one else is doing this to the extent we are.”

Galaxy Digital’s $3.507 billion financing for its CoreWeave data-center build in Texas comes with a steep price: about $346.3 million in annual interest.

A Galaxy project subsidiary priced the 9.875% senior secured notes on July 23. The deal is slated to close July 28, and the notes mature on Aug. 1, 2031.

The financing is intended to cover part of two buildings with eight data halls at the Helios campus. The facilities are planned for 400 megawatts of utility capacity and 260 MW of critical IT capacity, with some proceeds also funding debt-service reserves.

The 9.875% coupon works out to $346.3 million in annual interest, paid in cash every Feb. 1 and Aug. 1 starting in 2027. The first payment covers only part of a year, but Galaxy has not disclosed the exact amount.

Repayment starts when construction ends

Principal repayment runs on a different schedule. The notes are due to amortize at 4% of original principal each year, subject to adjustment. That equals $140.28 million annually before adjustments, paid in semiannual installments, with the first payment date at least 10 months after project completion.

Interest starts on a fixed schedule, while principal repayments wait until construction is complete and can be adjusted. Creditors will hold first-priority claims on nearly all project assets and the parent company’s stake in the issuer.

The disclosed liens cover Galaxy Helios Data Centers II LLC, its project guarantor and the parent-held equity in the issuer. They do not extend to Galaxy Digital’s assets generally.

The construction schedule now carries a clear financial price. Interest starts in 2027, but principal repayments wait until the project is finished, putting Galaxy’s delivery timeline at the heart of its CoreWeave deal and debt obligations through 2031.

Coinbase (NASDAQ: COIN), Bybit, Circle (NYSE: CRCL), and Gemini lead the names on CNBC and Statista’s 2026 ranking of 500 global Fintechs. Coinbase, listed as decentralized, returned after appearing in an earlier edition.

Bybit is based in Dubai, while Circle and Gemini are in New York. Statista’s ranking covers eight market groups and includes companies of different sizes.

According to McKinsey, the fintech industry generated $650 billion in sales in 2025, up 21% from 2024. The $15 trillion financial services industry as a whole grew by 6%. Public listings also began to rebound, with 31 major fintech initial public offerings (IPOs) in 2025. To McKinsey, those agreements have “returned to prominence.”

Fintech companies represented about 12% of the total value of the world’s 100 biggest IPOs. Listed Fintechs reached a record combined value of $850 billion, helped by Adyen (AMS: ADYEN), Nu Holdings (NYSE: NU), and Robinhood (NASDAQ: HOOD).

At the same time, software suppliers spread throughout banking systems, challenger banks obtained financial licenses, and big institutions began to employ blockchain more frequently.

Digital asset companies turn blockchain tools into services for banks and businesses

The digital asset category in the Fintech 500 covers companies that make crypto services usable, but leaves out individual coins and blockchain protocols.

Crypto demand has risen and fallen, but companies building the working parts of the market have kept attracting customers. Companies that create and manage tokens for other businesses also earned several places.

The Singapore group includes Amber Group, ChainUp, Crypto.com, Triple-A, and previous winner StraitsX. US entries include Bakkt (NYSE: BKKT) in Atlanta; previous winners BitGo in Sioux Falls and Blockdaemon in Los Angeles; Digital Ascension Group in Dallas; Everstake and Securitize in Miami; Payward in Cheyenne; and Zero Hash in Chicago.

San Francisco contributes previous winners CoinTracker and VGS, plus Phantom. New York adds previous winners Fireblocks and Turnkey, alongside Gauntlet, Lukka, NYDIG, Paxos, and Zebec. Galaxy Digital (NASDAQ: GLXY), another earlier winner, is also based there. Fort Worth is home to previous winner Consensys.

Canada has Blockstream in Montreal and previous winner, Figment, in Toronto. London has BVNK, Copper, and TIMVERO. Previous winner Finery Markets is in Limassol, Cyprus. Hong Kong includes HashKey Group and previous winner OSL Group (HKEX: 0863). The remaining names are Kem in Abu Dhabi, previous winner Ledger in Paris, and Wavebridge in Seoul. Blockchain services from these companies now support payments, recordkeeping, asset storage, issuance, and other commercial uses as crypto becomes part of formal finance.

AI and stablecoins force Fintechs to rebuild products and controls

McKinsey expects four trends to shape the next fintech era, though its report detailed two major ones here. Artificial intelligence comes first. “Fintechs are deploying AI to build products in weeks that once took years, to serve customer segments that were previously not economically viable, and to compress cost structures so that legacy operating models cannot compete on price. Early-adopter incumbents are seeing real returns,” said McKinsey.

McKinsey said, “With instant, near-free settlement, the promise of stablecoins for cross-border payments and remittances is clear. However, of the $35 trillion reported annual stablecoin transaction volume, only about 1 percent, or $390 billion, represents true end user payments, such as paying suppliers or sending remittances.”

Trading, arbitrage, and crypto-only transfers make up the rest. Industry forecasts place the stablecoin market between $2 trillion and $4 trillion by 2030. Reaching that range would require an average annual growth of about 40%.

Other tokenized assets on blockchains could grow faster as banks and companies use them for settlement, custody, payments, ownership records, and issuance.

McKinsey predicts that, “A range of industry estimates suggests that by 2030, the market value of stablecoins will be between $2 trillion and $4 trillion, implying a compounded annual growth rate of about 40 percent, with a broader range of on-chain tokenized assets potentially even higher.”

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Then cheap AI tax tools arrived. Goldman Sachs analyst Gabriela Borges cut her price target in June to $276, down from $519.

Intuit moved fast. It cut 17% of staff, roughly 3,000 jobs. It also lowered its TurboTax forecast.

The company is now worth about $88 billion, Forbes reported. A year earlier it was worth more than $219 billion.

Accenture (ACN) tells a similar story, down 45.21%. Clients are spending on AI instead of consultants.

New client orders slipped to $19.3 billion from $19.7 billion. Accenture cut its sales growth forecast to between 3% and 4%. The stock fell almost 18% in one day.

Cognizant (CTSH), Gartner (IT) and The Trade Desk (TTD) each lost 44% to 55%. All three sell work that AI can copy.

But the Two Biggest Losers Had Nothing to do with AI

Here is the twist. The two worst stocks fell for old-fashioned reasons.

AI Fear Wiped 40% Off 10 S&P 500 Stocks While the Index Rose 8%

CoStar Group (CSGP) is down 58.86%, the weakest in the index. Its problem is spending, not AI.

CoStar owns Homes.com, a property listings site. In January it said the site will not cover its own costs until 2029. Profit is not expected until 2030.

The core business is fine. Revenue jumped 23% to $897 million last quarter. Profit was just $3 million.

Investors lost patience. In February, hedge fund D.E. Shaw told CoStar to quit or shrink Homes.com. It said the move could unlock more than $10 billion. CoStar called the campaign “activism malpractice.”

Shareholders backed the board in June. Nasdaq had already dropped the stock from its Nasdaq-100 index in May.

Boston Scientific (BSX) is down 53.59%. It simply grew slower than promised.

In February it expected sales to grow 10% to 11%. By April it cut that to between 6.5% and 8%.

A rival explains why. Medtronic said its heart device sales rose 124% in the United States. It took “an additional 8 points of U.S. share.”

Then bad news piled up. Boston Scientific recalled its Accolade pacemakers. Regulators tied the fault to four deaths and 2,557 serious injuries. It also agreed to buy Penumbra for $14.5 billion.

Where the Money Went Instead

Chip and memory makers took it. Sandisk (SNDK) is up 505.17% this year. Dell Technologies (DELL) rose 247.55%. Micron Technology (MU) gained 222.68%.

Small investors piled in too, feeding the AI capex boom through chip funds. A narrow group of winners now drives the whole index, as data on AI stocks driving gains shows.

Everything else got punished for any slip. Expensive stocks fell hardest when forecasts came down, a danger flagged in recent earnings bubble warnings.

CoStar and Boston Scientific both report results this week. Those numbers will show whether investors were right or just impatient.

KB Kookmin Bank will launch a blockchain payment service for import and export companies in August.

The bank will initially process US dollar payments for those clients over JPMorgan’s Kinexys network. It announced the plan on July 26.

South Korean Bank Moves Dollar Trade Payments Onto JPMorgan Blockchain

Kinexys is JPMorgan’s blockchain unit, formerly known as Onyx. It runs institutional payments, tokenization, and digital asset settlement.

The platform has processed more than $4 trillion since its launch. Average daily transactions exceed $7 billion.

The service will initially support dollar remittances to 10 countries, including South Korea, according to local media reports. The list covers the US, Singapore, Saudi Arabia, India, Thailand, Qatar, the United Arab Emirates, Bahrain, and South Africa. Korean branches and KB Kookmin’s Singapore office will offer the service.

This comes just days after KB Kookmin was selected for a government-backed deposit token payment project. The Ministry of Science and ICT and the Korea Internet & Security Agency run the program.

Whether other Korean lenders adopt Kinexys will test how far tokenized deposits reach beyond JPMorgan’s clients.

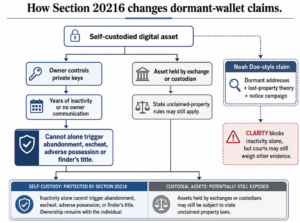

Section 20216 of the latest CLARITY draft states that a self-custodied digital asset cannot become abandoned, unclaimed, or forfeited. It also cannot become subject to adverse possession or finder’s title solely because its owner has not moved it or otherwise shown continued interest.

The language overrides state and local laws that treat years of wallet inactivity alone as grounds for transferring ownership to someone else.

The May 8 and May 20 Senate drafts protected only the ability to hold a self-hosted wallet, and the July 22 version adds scope beyond that, extending into property law and covering whether a person still owns the coins inside that wallet once years of silence go by.

The section defines a self-custodied digital asset as one where the owner keeps exclusive control of the private keys without relying on a custodian, exchange or intermediary.

That definition draws the line the rest of the provision depends on.

Draft / provision

What it protects

What it does not fully settle

May 8 / May 20 Senate drafts

The ability to use a self-hosted wallet and hold private keys

Whether dormant self-custodied coins can be treated as abandoned property

July 22 Section 20216

Continued ownership of lawfully self-custodied digital assets

Claims based on more than inactivity, such as fraud, theft, competing ownership evidence, or court-specific facts

Custodial assets carveout

Preserves state unclaimed-property rules for exchanges, brokers, and custodians

Dormant assets held by intermediaries may still face state reporting and escheat rules

From wallet access to property title

Courts would have to draw a line between two categories of digital assets: coins a person controls directly through private keys and coins sitting with an exchange, broker, or custodian. The federal shield from the new CLARITY Act draft goes to the first group.

State unclaimed-property rules keep governing the second, since the draft expressly preserves them for custodial holdings. Recent state amendments already treat exchanges, custodians, and hosted-wallet providers as a distinct category for assets that could belong to missing owners.

A wallet holding its own keys and an exchange account holding the same dollar value in Bitcoin would sit on opposite sides of that line.

In the exchange case, the custodian controls the keys, so state dormancy, reporting, and delivery rules for that custodian keep applying the way they always have.

The case that made this provision urgent

New York’s own lost-property law shows why the provision has real teeth right now. Article 7-B of the state’s Personal Property Law covers property that someone loses and later turns over to police.

Section 257 lets title vest in the finder under specific conditions, including for property under $10 once a year of failed efforts to find the owner has gone by.

Noah Doe and two companies are using that framework to claim title to 39,069 dormant Bitcoin addresses holding roughly 3.799 million BTC, nearly 18% of Bitcoin’s total supply. Their filing points to an OP_RETURN notice campaign, a press release, and a claim window as evidence that the coins count as lost property nobody came forward to reclaim.

The theory leans hard on the wallets’ silence, years of coins sitting untouched with no owner surfacing to contest the claim, and Section 20216 targets that mechanism. A claimant could no longer point to years of inactivity or a lack of communication as the basis for taking title under state abandoned-property law.

Noah Doe’s plaintiffs also cite police reports, the OP_RETURN notices, and their attempts to contact possible owners. That evidence goes beyond pure dormancy, and it could let them argue their claim rests on more than silence alone even if CLARITY becomes law.

The provision closes the legal opening their case is testing without settling the lawsuit itself, since a court still has to weigh whether that additional evidence moves the analysis.

Section 20216 protects self-custodied assets from inactivity-based abandonment claims while leaving custodial holdings potentially subject to state unclaimed-property laws.

Where the provision goes from here

In the bull case, Section 20216 survives Senate negotiation with its preemption language intact, and courts read the phrase “solely due to inactivity” narrowly enough to give self-custody real protection.

Dormancy-based theories like the one behind Noah Doe become far harder to build, since a claimant would need proof beyond years of silence to get anywhere. Holding your own keys gains a legal backing that self-custody advocates have never quite had before.

In the bear case, Senate negotiators strip or soften Section 20216 before a final vote, and whatever language survives leaves room for courts to weigh inactivity alongside other factors when deciding a claim.

State-law experiments around dormant wallets stay possible, and a future claimant could still build a theory similar to Noah Doe’s around long stretches of silence plus a notice campaign.

Scenario

What happens to Section 20216

Effect on dormant-wallet claims

What it means for self-custody

Strong version survives

Federal preemption remains intact, and courts read “solely due to inactivity” narrowly.

Dormancy-only claims become very hard to bring

Self-custody gains a property-law shield, not just a technical right

Softened version passes

Language is narrowed, or exceptions expand

Claimants can still combine inactivity with notices or other evidence

Courts decide case by case whether silence supports abandonment

Provision removed

CLARITY keeps wallet-use protections but drops title protection

State-law experiments continue

Self-custody remains legal, but dormant-title risk stays unresolved

Court rules before law passes

Noah Doe or a similar case creates precedent first

Congress may need to clarify retroactivity and state-law preemption

Dormant Bitcoin becomes a national property-law issue

Self-custody keeps its protection as an activity; holding your own keys stays legal, and title during years of inactivity stays a live issue courts have to settle case by case.

Section 20216 removes the single easiest argument a claimant could make against a silent Bitcoin address: the idea that years of nothing happening amounts to abandonment on its own. Whether that turns out to be enough depends on what survives Senate negotiation and what a judge eventually decides silence alone can prove.

After a collapse wiped out more than 60% of its value in one day, BMX, the ecosystem token of BitMart exchange, has made a slight recovery.

However, traders across Chinese and Vietnamese crypto channels are saying that withdrawals from the exchange are running slowly.

How far did BMX crash, and how much has it recovered?

BMX currently changes hands near $0.163, according to CoinMarketCap, which is a rise of over 44% in less than 24 hours after it traded as low as $0.107.

BMX token staged a small recovery after its July 24 crash. Source: CoinMarketCap

That recovery follows the July 24 sell-off, which was flagged by various observers, including X user Lu Ge with the account @lugeweb3 (撸哥整顿币圈), who pegged the single-day loss at 63% and told followers with money on the platform to pay attention.

Per Cryptopolitan’s calculations, the token dropped by over 65% within hours.

Lu Ge gave two possibilities that may be responsible for the crash, stating that it could be either that the platform was hacked or someone connected to it dumped supply.

Despite its partial recovery, BMX is still below its June 2024 record of $0.6203 by nearly 74% per CoinMarketCap data and carries a market capitalization of $52.8 million as of the time of publication.

What are users reporting about withdrawals on BitMart?

The price story is now tangled with a second thread, which is withdrawals from the exchange.

X user The KOL 加密无畏 (@cryptobraveHQ) wrote on the platform on July 25 that after BMX cratered, community members began reporting that withdrawal reviews were taking far longer than usual, including one case where a several-hundred-dollar USDT withdrawal requested in the morning still had not landed.

Other reports confirmed the same thing, with some suspecting that it is a suspected anomaly in the platform’s withdrawal process rather than a confirmed outage.

X account, @BTCs_, stated that a 5 USDT withdrawal took more than three hours to clear, calling it something he had never seen. Another user, @solotop999, posted that an untouched Bitmart account he tried to empty returned an on-chain withdrawal freeze message.

Lu Ge followed up, asking users to test their own withdrawals and report back, and noted a wave of near-identical promotional posts from marketing accounts, which he read as a bad sign rather than a reassuring one.

What has BitMart said about the development?

BitMart has not released any official statement about the token crash or the withdrawal challenges some of its users claim to be experiencing.

For now, Bitmart still shows meaningful scale. CoinMarketCap lists about $1.29 billion in 24-hour spot volume for the exchange and reported reserves near $158 million. On July 17, the company published an H1 2026 report describing asset-management growth of roughly 256% and expansion into payments, prediction markets, and US operations.

That report predates this week’s events and does not address the token drop or the withdrawal complaints.