The Bitcoin price could be on track to reach $200,000 within the next one to two years, according to crypto analyst @CryptoTice_. Backed by a long-term cycle chart, the analyst argues that Bitcoin is once again moving through a familiar historical pattern, placing the current phase in what he describes as a key accumulation zone ahead of a potential major rally.

Bitcoin Price Path Points To 2027 Target

The chart maps Bitcoin’s previous market cycles and outlines a potential path toward $200,000. Based on this projection, the target could be reached within 12 to 24 months from June 2026, placing it between mid-2027 and mid-2028, with 2027 appearing as the more probable timeframe.

To support this view, the analyst compares Bitcoin’s current setup with the cycle lows recorded in 2019 and 2022, both marked as “buy zones” that were followed by major rallies. The 2019 bottom preceded a climb to roughly $69,000, while the 2022 low eventually led to a surge toward $126,000.

The analyst believes the latest correction fits the same pattern. After falling from around $126,000, Bitcoin rebounded near the $60,000 region, creating what he identifies as another accumulation zone. From there, the projection points to a recovery that ultimately pushes the Bitcoin price toward $200,000.

The consistency of this structure forms the foundation of the forecast. In each cycle, Bitcoin experiences a sharp correction, spends time consolidating, and then enters a strong expansion phase. Although the percentage gains have become smaller with each cycle, the broader upward trend remains intact.

Why The Crypto Analyst Sees A Rare Opportunity

That historical pattern is also why @CryptoTice_ argues that the current market environment may offer a significant opportunity. According to the analyst, previous cycle bottoms were formed during periods of widespread uncertainty, before sentiment eventually shifted and prices moved higher.

The chart reflects this view by projecting a gain of roughly 230% from the 2026 buy zone to the $200,000 target. While substantial, that increase is far below the explosive returns seen in Bitcoin’s earlier years, reflecting how the asset’s growth has gradually moderated as the market has matured and attracted greater institutional participation.

The forecast comes at a time when investors remain divided over Bitcoin’s next move. Some continue to focus on macroeconomic conditions, interest-rate expectations, and regulatory developments, while others see the recent pullback as another cycle correction that could eventually lead to new highs.

For the crypto analyst, the most important factor is timing. His model suggests that the current phase may represent the final stage of accumulation before the next major advance begins. If Bitcoin continues to follow the structure shown in the chart, the path to $200,000 could unfold over the next 12 to 24 months, making 2027 a year worth watching closely.

Bitcoin’s latest upward move has sparked debate among market participants, and some believe the rally may have little to do with the purchase announcement that received the most attention. While the acquisition is generally viewed as constructive for the broader market, it is not necessarily the type of development that would justify a significant upward move in Bitcoin price.

Why The Latest Purchase May Not Be Driving Bitcoin Rally

The Bitcoin’s recent move higher is being misinterpreted as a direct reaction to purchase news, when in reality the drivers appear to be more technical in nature. Crypto analyst Aylo has explained on X that the BTC bounce is likely the result of an oversold market finding relief after sweeping key February lows.

Another factor supporting the move higher is the easing of concerns surrounding Strategy and its Bitcoin holdings. The company’s recent sale of a relatively small 32 BTC sparked fears that it could become a larger seller in the future.

Aylo suggests that while the current low may hold in the near term, it remains plausible that BTC could form a slightly lower low in June before a rally, particularly if the broader equity markets experience further weakness. Any deeper stock market shakeout could temporarily drag the price lower before a more sustained recovery begins. This level will be temporary before Bitcoin sees a low later in the year.

Furthermore, the fear that Michael Saylor and Strategy may be forced to liquidate a significant portion of their BTC holdings is likely overstated. The company may need to sell limited amounts to meet specific obligations, but the narrative that a major liquidation event from their supply will be driven more by bearish sentiment.

What The Recent Breakdown Could Mean For The Market

Bitcoin’s recent price action appears to be following a market structure that has played out before during previous corrective phases. A crypto trader known as Max Trades pointed out that roughly a month ago, BTC was entering a distribution phase of this pattern, and the outlook has since played out with notable accuracy.

In this bear market, BTC first formed an accumulation range, where price consolidated before breaking higher and sweeping out the liquidity above the previous highs. However, instead of continuing its upward trajectory, the asset price has transitioned into distribution. Since then, BTC has experienced a significant decline, falling more than 20% from its previous highs.

According to Max Trades, what makes the current setup particularly noteworthy is the comparison to a previous distribution phase that ultimately resulted in substantially deeper downside after the initial breakdown. If the current structure continues to mirror that historical pattern, it could imply that the recent decline is not yet complete.

The lead research analyst at Glassnode has highlighted how the Bitcoin supply clustered at the top levels might have to shift down before a sustained recovery can take shape.

Bitcoin Cost Basis Distribution Shows Massive Supply Above $80,000

In a new post on X, Glassnode lead research analyst CryptoVizArt has discussed how the Bitcoin supply is looking from the perspective of the Cost Basis Distribution (CBD). The CBD is an on-chain indicator that tells us about the amount of BTC that was purchased at each of the levels that the cryptocurrency has visited during its history. Below is the chart for the metric shared by CryptoVizArt.

As is visible in the graph, there is a decent amount of Bitcoin supply that was purchased at recent price levels. This supply cluster has built up as the asset has consolidated in the region since February.

While this cluster isn’t small, it’s still less dense than some other zones. From the chart, it’s apparent that there are regions above $80,000 that host the break-even level of an extreme amount of supply approaching the 495,000 BTC mark.

These zones extend up to the top levels from the 2025 bull market. Earlier, the levels near $126,000 used to be even more dense, but as the digital asset sector has gone through this downturn, supply has changed hands at lower levels, weakening these clusters. However, the zones continue to be dominant relative to the clusters below $80,000.

“The Cost Basis Distribution heatmap shows a dense supply cluster in the $80k–$126k range, representing coins still held by buyers near cycle highs,” noted the analyst. Naturally, all of these holders are in a notable amount of unrealized loss right now.

Generally, underwater investors act as an impediment to price surges as they sell near their break-even. This effect could in part be what capped out the recovery rally in May. CryptoVizArt explained:

For a sustained recovery to take shape, this supply needs to gradually migrate into new buyers’ hands at lower cost basis levels. As that wall softens, the overhang pressure eases and demand has room to build conviction.

In the past, the process has often taken some time to occur for Bitcoin. “This transition can be achieved through deeper correction and/or bear market continuation,” said the Glassnode researcher.

It now remains to be seen how the CBD will develop for Bitcoin in the near future, particularly in terms of whether the top buyers finally capitulate to new investors.

BTC Price

Bitcoin plummeted to $59,000 last week, but the asset opened on Monday with some recovery as its price is now floating around $63,200.

Ethereum’s slide to its lowest level in more than a year is testing the Wall Street trade that brought the token deeper into institutional portfolios.

Data from CryptoSlate shows that the second-largest cryptocurrency fell to as low as $1,506 during the last 24 hours, its weakest level since April 2025, extending a broad crypto selloff that has already drained leverage from derivatives markets and pushed traders toward defensive positioning.

Crucially, the downswing is not confined to ETH’s spot market as the digital asset is also experiencing a broader deterioration across regulated ETF flows, centralized exchange deposits, and derivatives positioning.

This situation comes at a time when the broader crypto market sentiment has significantly weakened, with Bitcoin falling toward a four-month low near $60,000, while Ethereum has erased much of its market support.

ETF outflows weaken Ethereum’s institutional bid

The pressure has been most visible in the ETF market, where the products that gave institutions a regulated way to buy Ethereum have turned into a source of persistent outflows.

Data from SoSoValue shows that spot ETH ETFs have recorded four straight weeks of withdrawals totaling more than $870 million.

Ethereum ETFs Weekly Flows (Source: SoSoValue)

During that period, the funds posted a 17-day outflow streak interrupted by only one day of inflows, when investors added $19.3 million.

As a result, sosoValue data show total spot Ethereum ETF assets have declined more than 70% from their $30 billion peak to $8.71 billion, which is equal to about 4.01% of Ethereum’s circulating market capitalization.

The reversal has weakened one of the main arguments behind Ethereum’s institutional expansion. The ETFs were expected to broaden access to the asset, deepen liquidity, and give traditional investors a cleaner way to gain exposure without handling tokens directly.

However, that demand has softened as ETH’s price moved lower and investors have reduced risk across digital assets.

Exchange inflows add another supply risk

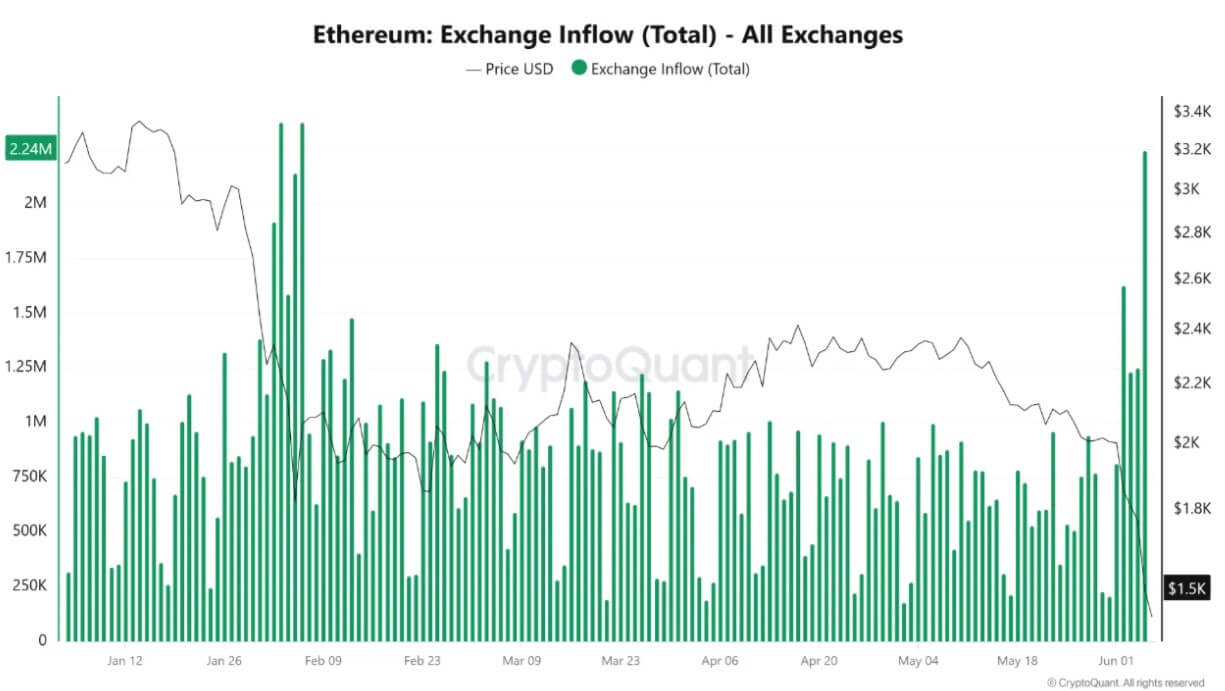

As institutional demand-side forces abated, the physical supply available on liquid trading platforms experienced a sudden and substantial expansion.

CryptoQuant data show Ethereum inflows to trading platforms climbed to about 2.24 million ETH in a single day, the highest level in four months. Binance accounted for more than 1.16 million ETH of those inflows, representing more than half of the total.

Ethereum Exchange Inflows (Source: CryptoQuant)

This surge in active supply can be seen in high-profile on-chain movements that served as glaring evidence of the liquidity migration.

Notably, a wallet linked to Ethereum co-founder Joseph Lubin awoke after more than three years of dormancy, mobilizing 80,001 ETH, valued at roughly $122 million.

The massive transfer epitomized the broader trend where long-inactive capital breaks from cold storage to seek out active trading venues and liquid architectures amid the mounting market stress.

Large inflows to trading platforms do not automatically mean investors are selling. They can reflect market-making activity, collateral movement, internal transfers, or portfolio restructuring during periods of stress.

However, traders watch the metric closely because coins held on exchanges are easier to sell or use in derivatives activity than coins sitting in private wallets.

The timing has made the increase harder to dismiss. Ethereum was already trading near $1,580 when the inflows accelerated, while Bitcoin had fallen toward $59,000. That combination suggested investors were moving assets during a marketwide reset rather than during a routine period of repositioning.

If exchange deposits remain elevated, the market could face additional short-term volatility.

Derivatives deleveraging deprives market of rebound capital

The velocity of the current crypto market decline has been accelerated by an extensive deleveraging cycle across leveraged futures platforms.

As spot valuations rapidly deteriorated, automated liquidation engines on major exchanges systematically closed out underwater long positions to protect clearinghouse integrity, amplifying organic selling pressure.

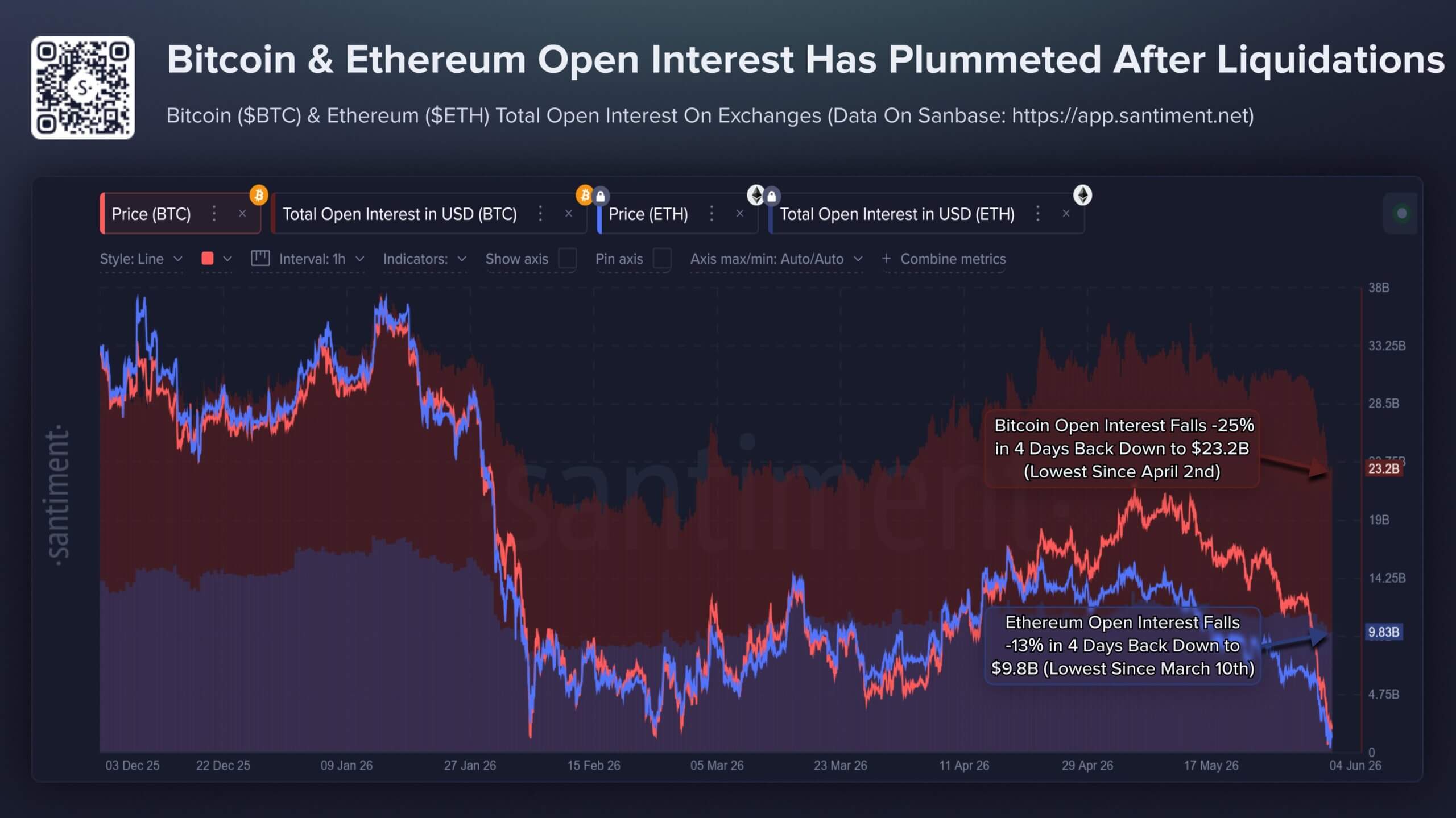

Data analyzed by Santiment illustrates that this liquidation wave effectively flushed out a massive block of speculative capital over a narrow four-day window:

Bitcoin Total Open Interest: Contracted by approximately 25%, dropping to $23.2 billion, which is its lowest operational aggregate since early April.

Ethereum Total Open Interest: Decreased by 13%, settling at $9.8 billion, a structural low point not seen since March.

Bitcoin and Ethereum Open Interest (Source: Santiment)

While this aggressive deleveraging leaves the underlying market structurally healthier by purging speculative excess and over-extended margin, it introduces an immediate liquidity vacuum.

The severe drop in open interest demonstrates that the speculative floor has thinned, leaving the market highly vulnerable to further spot pressure due to the lack of immediate leveraged capital available to front-run a classic V-shaped recovery.

Consequently, retail crowd sentiment has cratered to its most pessimistic footing since mid-February.

The firm noted that social metrics reveal an exponential increase in the phraseology of capitulation, with organic social discussions increasingly pairing terms like “Bitcoin” and “altcoins” alongside terminal descriptors such as “dead,” “finished,” “over,” and “ending.”

Traders hedge for a break below $1,500

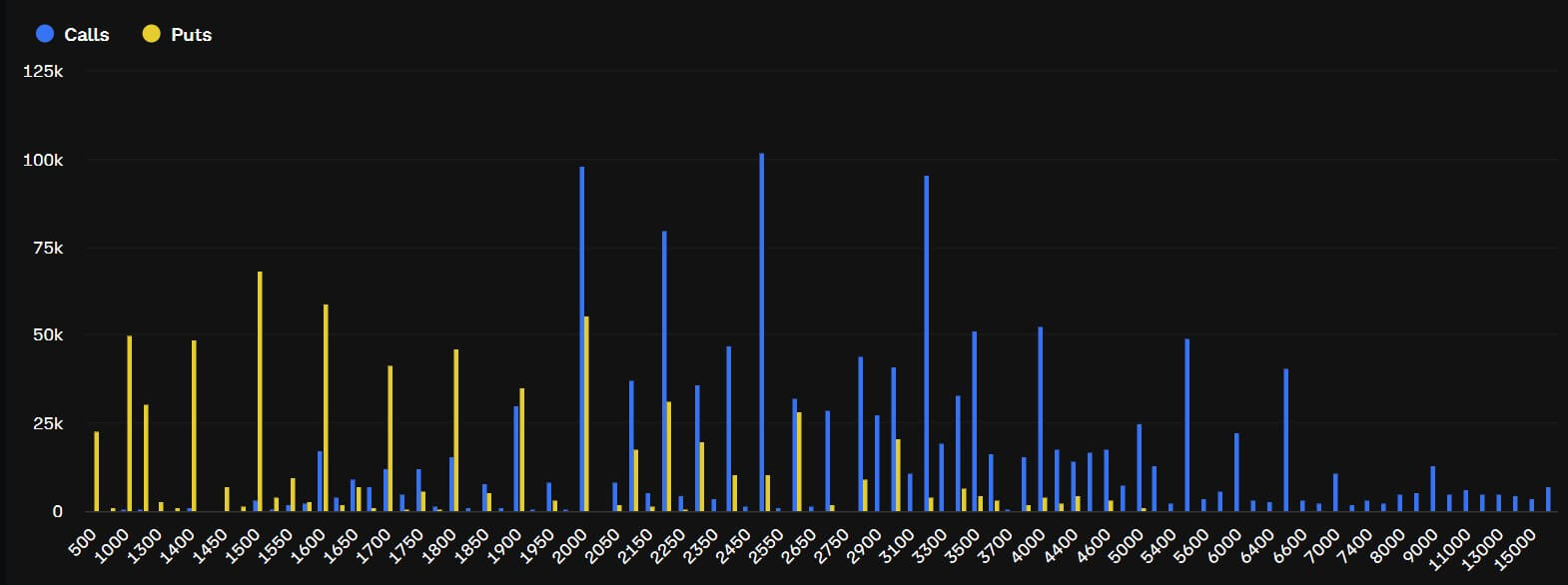

The buildup of stress across ETFs, exchange flows, whale cost bases, and leveraged markets has shifted attention to ETH’s options market, where traders are paying more to protect against another leg lower.

Deribit data show demand for downside protection has increased sharply. The ETH options put-to-call premium rose to 3.7 times on Friday and has shown consistent excess demand for put options since Monday. Put contracts give holders the right to sell at a set price, making them a common hedge when traders expect further losses or want protection against a disorderly move.

ETH’s open interest has clustered around several downside strikes. Traders have built roughly $108 million in open interest around the $1,500 strike, while the $1,400 strike has attracted about $75 million. The $1,000 strike has drawn about $78 million in positioning.

Those levels do not mean the market expects ETH to fall to $1,000 immediately. Instead, they show that traders are paying for protection after several support signals weakened at the same time.

BlockScholes data show the shift has also appeared in volatility pricing. ETH short-dated implied volatility has jumped from a year-to-date low of 36% to 67%, signaling that traders now expect larger near-term price swings.

The move has been accompanied by a sharper skew toward out-of-the-money puts. The seven-day ETH options skew has moved to about -14%, compared with roughly -3% to -4% in late May. Additionally, the demand for puts has also spread across 7-day, 14-day, 30-day, and 90-day maturities.

That broadening shows traders are not just hedging a single event or one short-term move. They are preparing for the possibility that Ethereum’s weakness could extend if ETF outflows continue, exchange inflows stay elevated, and large holders remain below key cost levels.

The next test is whether $1,500 becomes a floor or a trigger. A stabilization in ETF flows and a decline in exchange deposits could help ease pressure.

Without that, the options market’s focus on downside strikes may become the clearest signal of where traders expect the next phase of the selloff to concentrate.

Andrei Grachev, co-founder of DWF Labs, warned on X that Strategy (formerly MicroStrategy) and BitMine could trigger the largest crypto market crash in history, urging investors to imagine Bitcoin falling to $10,000-$20,000.

This warning lands at one of the most fragile moments for both companies.

A crypto treasury crash happens when major corporate holders are forced to liquidate large positions, pushing prices into a self-reinforcing downward spiral. Grachev believes MicroStrategy and BitMine could become exactly that kind of trigger event.

He framed his post as a thought exercise. The DWF Labs co-founder said he hopes the scenario does not unfold, yet he wants investors to genuinely consider their trading strategy if Bitcoin slides toward the $10,000-$20,000 range.

BitMine and Strategy have all the chances to create the largest market crash in the history of crypto Fingers crossed that it won’t happen, but if it did, what’s your strategy for BTC crash to 10-20k$?

Grachev has consistently warned about leverage and structural risk. He previously described the October 2025 cascade as a “nuclear bomb” event and has spoken about ongoing “liquidity wars” that keep wiping out billions across crypto markets repeatedly.

His core argument focuses on concentration. Two corporate giants now hold massive crypto positions, and any forced selling under financial pressure could amplify weakness across already fragile market conditions and trigger panic among retail and institutional holders.

🚨RETAIL HAS VANISHED FROM THE CRYPTO MARKET

CEX spot volume collapsed to $679 billion, the lowest level since October 2023, as per CryptoQuant.

Spot trading is now down 46% YoY, a staggering -67% drawdown from its October 2025 peak.

Why MicroStrategy and BitMine Sit at the Center of the Storm

MicroStrategy recently incurred approximately $13 billion in unrealized Bitcoin losses, its largest paper loss ever recorded. The firm holds more than 843,000 BTC across its corporate balance sheet.

The pressure runs through its capital stack. Strategy’s variable-rate perpetual preferred stock STRC slipped below $95, according to TradingView data. Meanwhile, MSTR shares have pulled back sharply, and the company recently sold 32 BTC for the first time since 2022.

BitMine sits on a similar problem. The Ethereum-focused treasury holds around 5.28 million ETH and carries over $10 billion in unrealized losses, after acquiring its stack at an average price near $3,500 per token.

FTX Imploded In 2022 And Left Customers With Over $8 Billion In Losses.

Today, Tom Lee’s Ethereum Position Is Down More Than $10 Billion. That’s Over $2 Billion Worse Than One Of Crypto’s Biggest Disasters.

Grachev does not predict the crash. He simply asks investors to mentally prepare for a scenario in which two corporate Bitcoin and Ethereum giants tip the market toward levels not seen since the previous deep bear-cycle low.

Bitcoin’s bearish structure over the past few weeks has raised clear concerns about the flagship cryptocurrency’s future. Amid these concerns are speculations concerning its trajectory, some of which point to bottoms as low as $25,000. However, an on-chain analyst recently took to the social media platform X to explain why Bitcoin’s fall to $25,000 is an unlikely scenario in its current cycle.

Electrical Cost Model Points To Potential Bitcoin Bottom

In a June 6 post on X, crypto analyst Ted Pillows implied that the Bitcoin price might see further declines before a definitive bear market bottom is established. This conjecture is based on the Bitcoin Electrical Cost model.

For context, the model estimates Bitcoin’s fundamental production costs by measuring the electricity required to mine new BTC. Because mining operations tend to consume substantial amounts of energy, the metric is often used as a proxy for Bitcoin’s inherent value. This is because it represents the minimum price at which miners can sustainably operate over the long term.

In line with historical data, Pillows explained that Bitcoin bear markets have never fallen below this Electrical Cost, despite the severe drawdowns seen during these periods. On the contrary, bear markets have often found bottoms near this crucial price level.

Pillows pointed out that Bitcoin’s current Electrical Cost sits at approximately $48,694 — a threshold still somewhat far from Bitcoin’s current market price. According to the analyst, this suggests that the BTC price could find support near $50,000 if the current downturn continues.

However, Pillows highlighted a caveat in this analysis, stating that it would take an extraordinary global event for this support zone to be broken. In the event that the world is hit by a recession or a pandemic as severe as COVID, the Bitcoin price could temporarily fall below its estimated production cost due to panic-driven sales.

Silent BTC Accumulation On Binance Underway As Outflows Steadily Climb

In a Quicktake post on CryptoQuant, analyst CryptoOnchain highlighted an interesting contradiction ongoing within the Bitcoin market. According to the on-chain analyst, BTC accumulation events have been underway on Binance.

The analyst noted that technical indicators — notably, the RSI (14) and the EMA50/200 — are telling a clearly bearish story. RSI readings, for example, have fallen to extreme levels near 6.4, and the EMA50/200 currently displays a “Death Cross” pattern.

At the same time, Binance’s Exchange Netflows reads as negative (-0.58σ), indicating that Bitcoin is leaving Binance consistently—an event that further suggests its holders are accumulating BTC rather than simply panic-selling. But then CryptoOnchain explained that the unignorable threat of a long squeeze still looms, given the high Open Interest.

As of this writing, the price of BTC stands at around $602,388, reflecting an almost 3% jump in the past 24 hours.

President Donald Trump endorsed lower interest rates and declared that growth does not cause inflation before walking out of a Meet the Press interview with NBC’s Kristen Welker.

The walkout clip now dominates social feeds. However, the policy signals buried in the exchange matter far more for Bitcoin (BTC), oil, and equities.

The Walkout Buried a Clear Message on Rates

In the interview, Welker pressed Trump on whether the Federal Reserve may need to raise rates under new Chair Kevin Warsh.

The Senate confirmed Warsh on May 13 by 54 votes to 45, the narrowest margin for any Fed chair. He chairs his first policy meeting on June 16 and 17, with rates at 3.50% to 3.75%.

Trump pushed the opposite way.

“There’s no reason to raise interest rates. The country becomes great. We built the country by doing great and having rates low.”

Fresh data gives the President his talking point. May payrolls rose by 172,000, roughly double the 85,000 consensus, while unemployment held at 4.3%.

Trump drew a conclusion that rejects decades of Phillips curve thinking, which links hot labor markets to rising prices.

“Growth is the greatest thing you can have and growth does not cause inflation.”

The stance revives a first-term pattern. Trump publicly hammered then Chair Jerome Powell through 2018 and 2019 to force cuts.

This time the pressure lands on an awkward target. Warsh built his reputation as a hawk and quit the Fed board in 2011 after opposing quantitative easing.

“I think Kevin is fantastic, and I want to do whatever he wants and I don’t want to have a big influence on him…”

Markets are not listening yet. CME FedWatch prices a 96% chance of a hold this month.

The war has rewritten energy math since late February. Brent crude jumped from about $72 per barrel to nearly $120 before easing to about $94 on Friday.

AAA puts the national gas average at $4.17 per gallon, up $1.16 since the Iran war began.

“It depends. It depends where the war goes. It could be after I give them a shot, and it could be if we sign an agreement it will go down now otherwise it will go down after we finish.”

Either path ends the same way, he argued, with gasoline prices set to “drop like a rock.”

Trump also signaled more military spending on top of a record base.

“We have debt and other thing, we have things we want to take care of. I want to go bigger on the military. I really do.”

The FY2027 budget already requests $1.5 trillion for defense, the largest single-year total since World War II, per CSIS.

The OMB projects a $2.06 trillion deficit this fiscal year, rising to $2.17 trillion next. Funding that gap forces the Treasury to issue more than $166 billion in debt every month.

Lower rates plus heavier issuance point to expanding liquidity, the variable Bitcoin traders watch most.

Michael Saylor doubled down on his Bitcoin conviction today, but while he did that, his MicroStrategy CEO, Phong Le, sold roughly $11.1 million in company stock tied to the same exposure.

The timing drew attention across crypto markets. Saylor frames Bitcoin as the premier long-term asset, yet the executive running his company trimmed shares that give investors leveraged exposure to that same bet.

Michael Saylor’s Conviction Meets an Inconvenient Sale

He argued the AI capital boom validates Bitcoin rather than threatening it.

“The AI buildout is absorbing capital at historic scale, creating temporary pressure across global markets. That does not weaken Bitcoin. It strengthens the case for scarce, liquid, digital capital. Bitcoin remains the premier asset for the long term,” Saylor explained.

It comes amid market uncertainty as the pioneer crypto continues to show weakness. Some associate that weakness with the latest MicroStrategy BTC sale, a move seen as a symbolic crack in the “never sell” fortress.

To worsen the matter, a regulatory filing shows that on June 5, Le filed to sell 93,738 MicroStrategy (MSTR) shares at a weighted average near $118.73. The proceeds came to about $11.1 million.

It is imperative to note that the sale may not necessarily be a bearish call.

It covered the tax bill on 190,740 performance stock units that vested on June 3. Le still holds 119,925 Strategy shares. Notwithstanding, the timing raises concerns.

“Not a good time to do this,” analyst Ted Pillows remarked.

Why the Optics Sting

The vesting itself sharpens the irony. Those units paid out at 200% because Strategy’s three-year total return ranked in the top quartile of the Nasdaq Composite. The reward for years of outperformance landed in the worst week of the year.

MicroStrategy trades as a leveraged Bitcoin proxy. Investors buy it for the firm’s huge BTC treasury and Saylor’s refusal to sell.

The sales ran through a Rule 10b5-1 plan set in May 2024, so the timing was automatic rather than chosen.

For the better part of two years, Wall Street has treated AI as the most bullish trade on the board, a growth engine that turbocharges earnings, underwrites stretched valuations, and promises a productivity windfall somewhere down the road.

However, the Fed has access to the same numbers and seems to be more inclined to treat the AI build-out as a fresh source of demand in a market that’s still fighting to drag inflation back toward its 2% target.

Goldman Sachs now expects AI-related capital spending to approach $800 billion in 2026, and it calculates that the surge will lift its full-year business investment forecast to 7.8% while adding roughly 3.3 percentage points to capital-expenditure growth on its own.

TrendForce, tracking the nine largest cloud providers in the world, places their combined 2026 outlay near $830 billion, a jump of about 79% over the previous year. A pretty big slice of that increase reflects rising prices rather than added capacity, with Microsoft attributing some $25 billion of its $190 billion budget to costlier memory and components.

All of it puts quite a bit of weight on the inputs the Fed tends to watch most closely, which could turn this investment boom into a policy headache.

Where does the $800 billion in AI spending actually go?

It helps to imagine this spending in physical terms. All of that money takes the shape of land, steel, transformers, copper wiring, gigawatts of fresh generation capacity, industrial-scale cooling, and the incredibly skilled and incredibly rare trades hired to assemble all of it.

Goldman described this as a wave that reaches across servers, semiconductors, memory, power infrastructure, data centers, software, and research budgets, and the bank’s longer-range model traces annual AI capex climbing from around $765 billion this year toward $1.6 trillion by 2031.

Power has become the binding constraint. In a late-May speech, Fed Governor Lisa Cook noted that electricity and water prices have each climbed about 5% over the past year, that chips, high-tech equipment, and software have all grown more expensive, and that wages in specialty construction trades have picked up notably. Households feel some of that pressure on their monthly bills, which began drawing political pushback as several state legislatures move to slow large data-center development.

The central bank’s leadership has been unusually clear and honest about where this leads. Speaking back in March, Jerome Powell told reporters that the construction frenzy was “putting pressure on all kinds of goods and services that go into building these things,” and he conceded that the effect was “probably pushing inflation up.”

Cook went further in that same May address, warning that “yet another shock to prices could be layered on from the heightened investment demand due to AI” and pointing out that companies have announced more than $1.5 trillion in data-center plans, only a sliver of which has actually been built.

The demand side of AI, in other words, is showing up in the price data well ahead of any productivity payoff the technology eventually delivers.

The consequences travel from Silicon Valley balance sheets straight into crypto. Bitcoin spent most of the year leaning on the expectation that cooling inflation would free the Fed to cut rates, loosen financial conditions, and rekindle the risk appetite that powered the 2024 rally.

CryptoSlate has documented how tightly the asset now tracks liquidity cycles, a sensitivity that has overtaken Bitcoin halving as the dominant price driver. An $800 billion demand makes rate cuts unlikely, since every dollar of AI-related price pressure hands the Fed one more reason to stay put.

Markets have already begun repricing that. Futures and prediction markets now put the odds of a hold at the June 16-17 meeting above 93%, which will be the first one chaired by Kevin Warsh following his May handover from Powell. CryptoSlate has tracked the reversal as it unfolded, from a stretch when bond traders were pricing a year-end hike to the inflation prints that kept the Fed frozen.

The repricing has bled into spot prices, with Bitcoin sliding to around $63,600 by June 4 after briefly breaking below $62,000, roughly half its October 2025 record and down more than 13% over the week. Much of that damage comes from exits, since Bitcoin ETFs saw a record 11-session outflow streak worth about $3.45 billion, the longest run of redemptions since the funds launched in 2024. A large share of that capital rotated straight into the AI and semiconductor equities that were driving the macro problem in the first place.

Over a five-year horizon, AI may well do what its champions promise, lowering costs, automating routine labor, and easing inflation through real gains in output per worker. However, the build-out phase tends to work the other way around first. Pulling years of infrastructure demand into a narrow window bids up hardware, energy, and talent long before we see any real efficiency, so the price shock arrives early and the windfall arrives late.

That gap between immediate consequences and delayed benefits is what’s been troubling the Fed. Warsh has argued that AI will prove “structurally disinflationary” and usher in “the most productivity-enhancing wave of our lifetimes,” a view that confirms his openness to lower rates. But Cook and Governor Michael Barr lean the other way, with Barr saying flatly that he doesn’t believe the AI boom will be a reason for lowering policy rates.

Traders, on the other hand, have been mostly troubled by timing. Bitcoin, alongside equities and the rest of the market, tends to respond to the first decision in front of them. So, a “productivity thesis” that will probably pay off in 2030 does little to positions held this week, month, or even quarter. Inflation running above 3% leaves Warsh little room to act on his convictions in June, regardless of where he’d like to steer.

The same AI boom inflating tech valuations and carrying the indices higher may be the very force keeping the Fed cautious, delaying the liquidity cycle that crypto traders have spent eighteen months waiting for. If policymakers settle on seeing $800 billion in annual spending as one more pillar of sticky demand, Bitcoin’s rate-cut trade rests on a foundation considerably thinner than its holders would care to admit.

Bitcoin just broke below $60,000. The Fear & Greed Index is sitting at 12 — Extreme Fear. One week ago it was near 52. That is a full swing from Greed to Extreme Fear in seven days.

I’ve been watching this market long enough to know what this kind of move feels like from the inside. It doesn’t feel like an opportunity. It feels like the bottom might fall out. That’s exactly why it’s worth paying close attention right now.

Let’s look at what the data actually says. The daily RSI is at 17, among the most oversold readings in years. Bitcoin is trading well below the 20-day, 50-day, and 200-day moving averages. That’s a structural breakdown, not a routine pullback. It doesn’t automatically mean we bounce. But it does mean the selling pressure is historically extreme.

“The fundamentals didn’t break. The sentiment did.”

What hasn’t changed: the GENIUS Act is law. Institutional capital is still moving on-chain. Stablecoin infrastructure is scaling. Neil Steinhardt at Nexo told me just a few weeks ago that the amount of institutions willing to work in this space increased considerably after the GENIUS Act passed — and that was before this dip.

Historically, the moments that feel like this — $60K with a Fear & Greed of 12 — are rarely the right time to panic out. They’re the moments that look obvious in hindsight. That said, no one rings a bell at the bottom. If you’re holding through this: know why you’re holding. If you’re watching from the sidelines: know what level brings you back in.

$60K is the line right now. How Bitcoin behaves around it over the next few sessions will set the tone for the weeks ahead.

Ashton Addison

CEO, Crypto Coin Show

🎤

This Week on CCS

Neil Steinhardt — COO & Principal, Nexo US

Is America Finally Open for Crypto? Nexo’s COO on the US Comeback, Regulation & What’s Next

The US is back open for crypto business, and the companies that survived the chaos are making their move. Neil Steinhardt walks Ashton through what a genuinely compliant re-entry into the US looks like from the inside, why the GENIUS Act changes everything for institutional adoption, and what it means that the Bank of America CEO is now recommending 20% digital assets in a portfolio. If you want to understand where the US crypto industry is headed, this is the conversation.

The internet can’t tell humans from AI agents at scale — How can we identify them?

World (formerly Worldcoin) just launched a “full-stack proof of human” upgrade, and the timing couldn’t be more relevant. DC Builder breaks down how World ID works as the identity layer for an AI-driven internet, the AgentKit launch with Coinbase that puts human verification at the core of AI agent commerce, and why proof-of-personhood is one of the most important infrastructure problems in crypto right now. A must-watch if you’re thinking about identity, AI, or both.

Private Credit is a $1.7 Trillion Market — and It’s Broken. Here’s How to Fix It Onchain

Benjamin built QiDAO from $0 to $400M in TVL and started his career at Citi, and now he’s bringing private credit markets on-chain with principal protection backed by Franklin Templeton. He explains why Celsius and BlockFi collapsed (hint: the team was making credit decisions they had no business making), how Cap’s underwriter model fixes the structural flaw, and why the GENIUS Act is quietly making Cap more attractive to institutions by the week. The token announcement at the end is worth staying for.

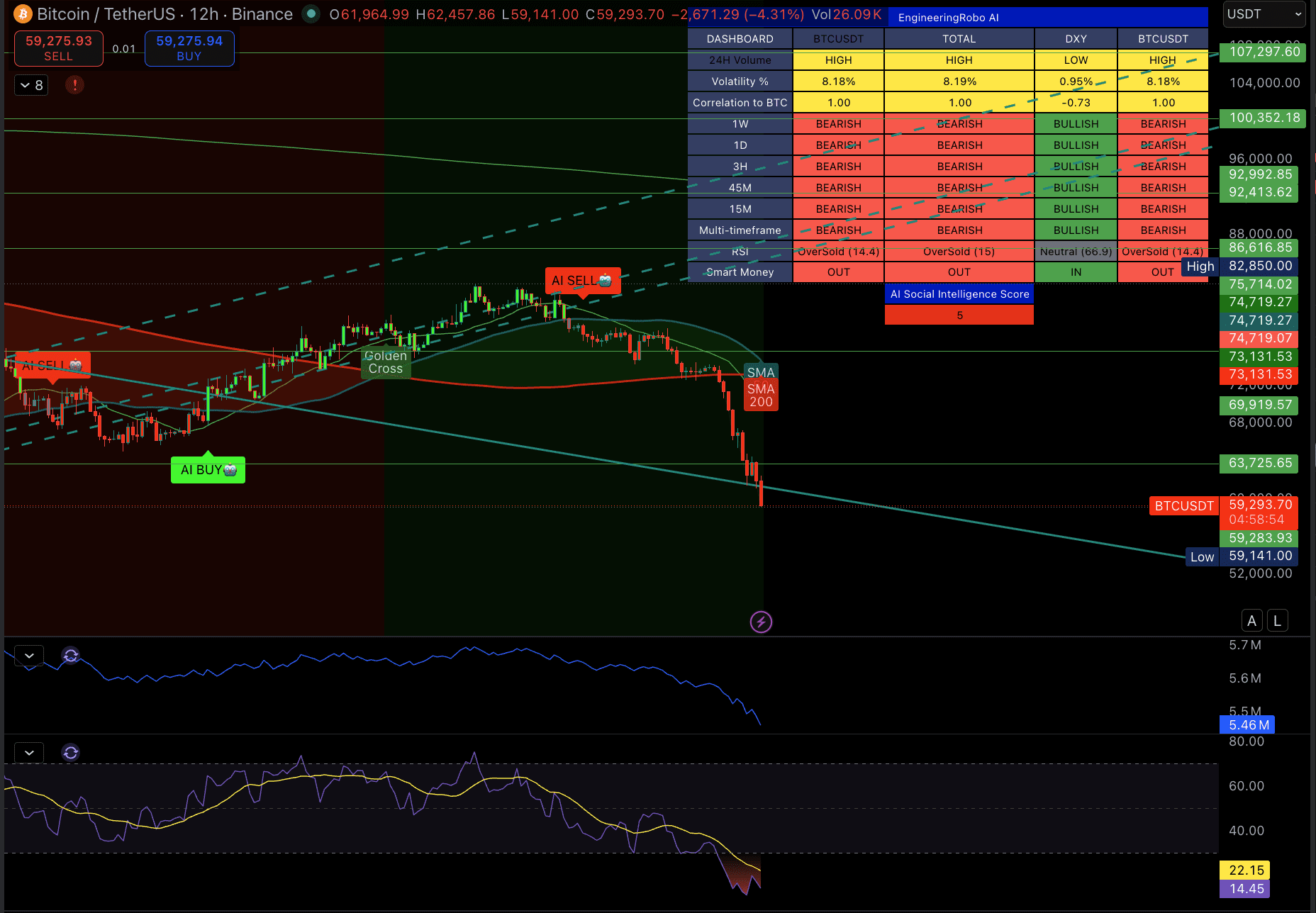

Bitcoin is trading at $59,293 on the 12-hour chart and the picture is about as clean as it gets — cleanly bearish across every timeframe. The 1W, 1D, 3H, 45M, and 15M are all red on EngineeringRobo. Multi-timeframe consensus: BEARISH. Smart Money is OUT. The RSI is sitting at 14.4 — one of the most oversold readings this cycle. Price knifed through both the SMA 50 and SMA 200 in a single move, with volume dropping on the way down, which tells you this is not panic selling finding a floor yet — it is a controlled bleed with sellers still in control.

The Death Cross is confirmed on the chart. The Golden Cross that gave bulls hope earlier in the cycle has been fully reversed. There is no timeframe on this chart showing buyers have any edge right now. The AI Social Intelligence Score is 5 out of 100, meaning sentiment from social channels is as negative as it gets.

My bias: BEARISH — oversold but no confirmation of reversal. The RSI is extreme enough that a mean-reversion bounce is possible at any session, but oversold does not mean bottom. There is no Smart Money flow, no timeframe flipping bullish, and no volume spike to suggest capitulation is complete.

What I’m watching

$59,141 is the session low and the immediate line. A close below it on the 12H with sustained volume opens the door toward $52,000, the next visible support. A reclaim of $63,725 on a close would be the first sign buyers are stepping in at scale. Until that happens, any bounce is a relief rally inside a downtrend.

Do not try to catch this falling knife without a confirmed close above structure. Manage your risk accordingly.

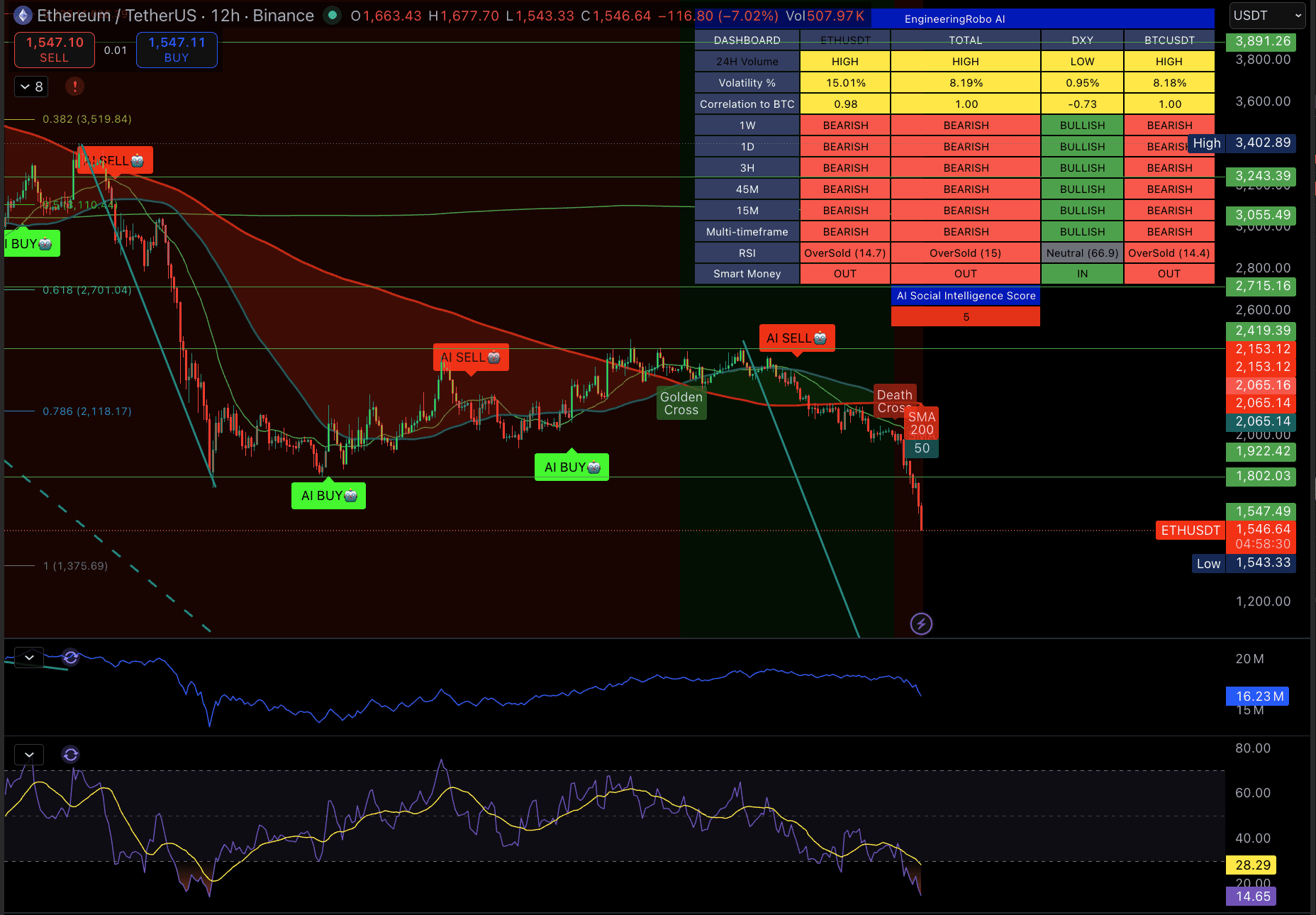

Ethereum is at $1,546 and it is not just following Bitcoin down — it is leading it lower. ETH is showing 15.01% volatility versus BTC’s 8.18%, and with a 0.98 correlation to Bitcoin, it is absorbing almost the full force of this move with added leverage to the downside. ETH is down 45% year to date versus BTC’s 32%. When the market sells off, ETH sells harder. That pattern is holding.

The Death Cross formed and has accelerated. Price is well below both the SMA 50 and SMA 200. All timeframes from 1W down to 15M are BEARISH on EngineeringRobo. RSI is at 14.7 — slightly more oversold than Bitcoin. Smart Money is OUT. The AI Social Intelligence Score is 5 out of 100. There is no timeframe or signal on this chart showing accumulation.

The Fibonacci structure is worth watching. The 0.786 level at $2,118 was the last meaningful support that gave way. Price is now in open air between that level and the 1.0 extension at $1,375. The session low is $1,543, which is sitting almost exactly on that 1.0 level. That is the line.

My bias: BEARISH — high volatility, no floor confirmed. ETH is the weaker asset in this environment. Until BTC stabilizes, ETH will not. The RSI is deep enough for a snapback but there is nothing in the signal data suggesting smart money is positioning for one.

What I’m watching

$1,543 is the session low and the Fibonacci 1.0 extension. A close below it on the 12H targets $1,375 as the next level of any significance. A reclaim of $1,802 would be the minimum needed to suggest the structure is beginning to repair.

The Original DePIN Protocol — Now with Its Own Layer One

10M+ nodes. A decade of proof-of-work. XYO’s Layer One is built for high-volume data, AI infrastructure, and real-world asset tokenization, with dual tokens $XYO and $XL1.

Filtered for signal, not noise. CCS articles linked where we’ve covered it in depth.

⭐⭐⭐

Zcash ($ZEC) crashes 50%+ as hidden privacy flaw wipes $5B from market cap.

A vulnerability in Zcash’s Orchard privacy pool, undetected for 4 years, allowed counterfeit ZEC to be generated. The bug was patched June 2, but whether fake coins were minted before the fix is impossible to verify. Traders are selling the uncertainty.

Crypto Clarity Act added to the Senate Legislative Calendar.

Now eligible for a full Senate vote — the next major piece of crypto legislation after the GENIUS Act, and the one that settles the securities vs. commodities question.

⭐⭐⭐

Visa, Mastercard, and Stripe launching a joint crypto stablecoin platform.

Three of the largest payment networks moving together on stablecoins while the market is in extreme fear. The buildout is not slowing down.

⭐⭐⭐

JPMorgan, Citi, and major US banks launching a tokenized deposit system to compete with crypto.

TradFi is not watching stablecoins take share — both a competitive threat and a validation signal.

Also this week

Bank of America appoints a top trading executive as global head of digital asset transformation.

Senior hire with a real mandate, not a press release title.

Over 50% of all Bitcoin in circulation now held at unrealized loss.

Historically coincides with late-stage capitulation, not the start of sustained declines.

Bitcoin down 32% YTD. Ethereum down 45%.

Neither is unprecedented. Both have recovered from worse.

$200 billion wiped from crypto market cap in 24 hours on June 3.

Not a slow bleed — a sharp flush.

In brief

US sanctions Iran’s largest crypto exchange, Nobitex.

Pattern Day Trader rule eliminated — $25K minimum gone.

US and Japan announce $1B partnership on AI, quantum, fusion, and biotech.

$60,000. That’s the line this week. Fear & Greed at 12, RSI at 17 — the data is flashing oversold. The fundamentals haven’t changed. The price has.

One question before you go.

Bitcoin is at $60K in extreme fear. Are you buying, holding, or waiting?