Ethereum treasury company Bitmine has filed to launch a public offering of 3 million shares of its 9.50% Series A Perpetual Preferred Stock.

The proceeds are expected to support a range of corporate and Ethereum-focused initiatives.

Bitmine’s New Offering

According to the company’s filing with the Securities and Exchange Commission (SEC), the net funds raised may be used for general corporate purposes, including the acquisition of additional ETH and other digital assets, the expansion of its staking and validator infrastructure through its MAVAN platform, working capital requirements, strategic investments tied to the Ethereum ecosystem and broader digital asset adoption, and potential repurchases of its common stock under an existing buyback program.

The preferred shares will carry cumulative dividends at a fixed annual rate of 9.50% based on a stated value of $100 per share. The dividends are payable in cash when declared by the company’s board. If any declared dividend is not paid on schedule, additional compounded dividends will accrue weekly, and the applicable rate will gradually increase up to a maximum of 15% per year until the outstanding amount is fully settled.

Bitmine has applied to list the new preferred shares on the New York Stock Exchange under the ticker symbol “BMNP,” and trading is expected to begin within 30 days of the initial issuance if the listing receives approval.

Interestingly, Bitmine’s application is based on a model similar to Saylor-led Strategy’s STRC perpetual preferred stock, which pays an 11.5% dividend. STRC has attracted investors looking for monthly income while gaining indirect exposure to Bitcoin. After raising around $2.52 billion through its initial public offering in July 2025, the program expanded through follow-on issuances. The total notional amount of STRC is approximately $10.5 billion.

Aggressive ETH Accumulation

With its Ethereum holdings rising to 5.42 million ETH, Bitmine said it has reached roughly 90% of its target to own 5% of all ETH. The company also said 4.72 million ETH are staked, with a portion of those assets secured through its MAVAN staking platform.

As one of the sector’s most active buyers, Bitmine has built the largest ETH treasury and the second-largest overall crypto treasury after Strategy. The sharp drop in Ethereum, which is down more than 45% year to date, has created significant challenges for Ethereum treasury companies. Recent data estimates indicate that Bitmine is carrying unrealized losses of more than $10 billion.

Even so, Chairman and Fundstrat co-founder Tom Lee remains optimistic on Ethereum, as he predicted the end of the bull market and the beginning of crypto spring.

Michael Saylor doubled down on his Bitcoin conviction today, but while he did that, his MicroStrategy CEO, Phong Le, sold roughly $11.1 million in company stock tied to the same exposure.

The timing drew attention across crypto markets. Saylor frames Bitcoin as the premier long-term asset, yet the executive running his company trimmed shares that give investors leveraged exposure to that same bet.

Michael Saylor’s Conviction Meets an Inconvenient Sale

He argued the AI capital boom validates Bitcoin rather than threatening it.

“The AI buildout is absorbing capital at historic scale, creating temporary pressure across global markets. That does not weaken Bitcoin. It strengthens the case for scarce, liquid, digital capital. Bitcoin remains the premier asset for the long term,” Saylor explained.

It comes amid market uncertainty as the pioneer crypto continues to show weakness. Some associate that weakness with the latest MicroStrategy BTC sale, a move seen as a symbolic crack in the “never sell” fortress.

To worsen the matter, a regulatory filing shows that on June 5, Le filed to sell 93,738 MicroStrategy (MSTR) shares at a weighted average near $118.73. The proceeds came to about $11.1 million.

It is imperative to note that the sale may not necessarily be a bearish call.

It covered the tax bill on 190,740 performance stock units that vested on June 3. Le still holds 119,925 Strategy shares. Notwithstanding, the timing raises concerns.

“Not a good time to do this,” analyst Ted Pillows remarked.

Why the Optics Sting

The vesting itself sharpens the irony. Those units paid out at 200% because Strategy’s three-year total return ranked in the top quartile of the Nasdaq Composite. The reward for years of outperformance landed in the worst week of the year.

MicroStrategy trades as a leveraged Bitcoin proxy. Investors buy it for the firm’s huge BTC treasury and Saylor’s refusal to sell.

The sales ran through a Rule 10b5-1 plan set in May 2024, so the timing was automatic rather than chosen.

Nvidia (NVDA) stock is up just 15% in 2026 while the rest of the chip sector races ahead, and one flow signal helps explain why the market’s former leader is being left behind.

The split from the sector is the surface story. Beneath it, options bets, perpetual traders, and institutional flows are pulling in different directions, and only one of them resolves the puzzle.

The Chip Rally Is Leaving Nvidia Stock Behind

Nvidia and the Semiconductor Index have moved in opposite directions on about half of all trading sessions over the past 50 days, near the highest rate since the 2022 bull market began. That frequency has more than quadrupled since the start of April.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

The performance gap is just as wide. The Nvidia stock price is up roughly 15% on the year, while Broadcom (AVGO) has gained about 20% and AMD has climbed far higher.

Nvidia is diverging from the rest of the chip sector:

Nvidia, $NVDA, and the Semiconductor Index, $SOX, have moved in opposite directions on ~50% of all trading sessions over the last 50 trading days, near the highest frequency since the bull market started in 2022.

— The Kobeissi Letter (@KobeissiLetter) June 4, 2026

Through 2024 and 2025, Nvidia drove the sector and outran its peers. The rally has since broadened to include chips other than Nvidia’s, leaving one question open. If the sector is soaring without it, where is the money that used to favor Nvidia going?

Bearish Options Bets on Nvidia Stock Are Building

The first place to look is the options market. The put-call ratio for Nvidia, which weights bearish put contracts against bullish call contracts, has tilted toward puts since the company’s last earnings report.

On earnings day, the volume ratio sat near 0.46 and the open interest ratio near 0.79. Those readings have since moved to about 0.45 and 0.85, with the open interest ratio climbing toward puts.

A higher open interest ratio means traders are adding downside bets or protection. The shift is small, yet it matches the performance lag and hints that conviction in Nvidia shares is fading.

Options point one way, but they are a single venue. Another market is betting the opposite, which deepens the puzzle rather than solving it.

On Hyperliquid, Traders Still Favor Nvidia Stock

On the perpetual futures platform Hyperliquid, the tokenized NVDA contract shows traders leaning long. The smart money and public-figure groups both hold net long positions, while the larger whale group sits net short, but only slightly.

That stance stands out against AMD and Broadcom on the same platform, where positioning skews more heavily short, at least across two cohorts, as opposed to NVDA’s whale-only cohort.

Volatility helps explain the pull. Nvidia carries the highest 30-day annualized volatility among the megacap names at about 33%, second only to Tesla and well above the broad market.

Bigger swings attract traders who want to trade on movement, a common tendency on platforms like Hyperliquid.

Broadcom’s earnings on June 3 also kept the sector’s attention on Nvidia’s rivals. So the venues disagree. Options lean bearish, perpetual traders lean long, and neither settles the question on its own. One last signal breaks the tie.

The One Signal: Institutional Money Is Exiting

That signal is the Chaikin Money Flow (CMF), an indicator that tracks institutional money flow into or out of a stock. Nvidia’s CMF has dropped back below zero.

A reading under zero points to net selling from institutions, the largest and slowest-moving money in the market. This is what the headline numbers hide. Over the past five days, Nvidia’s stock is up about 2%, yet the flow has turned negative beneath that flat price.

The divergence ties the whole picture together. Institutions stepping back explains the lagging year-to-date return and the rising put interest, while the Hyperliquid longs look like shorter-term traders chasing volatility rather than a lasting bid.

The CMF is now testing a rising trendline drawn from early January. A break below it would deepen the outflow and confirm the sector has moved on without its leader.

A recovery back above the line and fresh inflows would show the selling was only a pause. For now, institutional flow is the signal explaining why the chip rally is soaring even as Nvidia stock lags.

Strategy, the largest corporate holder of Bitcoin, recorded the largest unrealized loss on its BTC holdings of over $10 billion in paper value. This reflects a 17% decline in the value of its position after years of steady accumulation.

The loss comes amid a broader market downturn as Bitcoin crashed to around $61,000 today. The apex coin is now down about 28% year-to-date, marking its weakest level since February.

Strategy Logs $10.47B Paper Loss

The company’s latest portfolio snapshot shows total invested capital at about $63.87 billion against a current valuation of $53.4 billion. This leaves a gap of about $10.47 billion in unrealized losses, alongside a smaller realized loss linked to recent portfolio activity. The figures highlight the continued pressure on its Bitcoin-heavy balance sheet after years of accumulation.

That pressure has also coincided with a notable change in its long-standing approach to Bitcoin holdings. The firm sold 32 BTC at an average price of $77,135 per coin, marking its first departure from a previously consistent no-sell stance.

According to a filing with the Securities and Exchange Commission, the sale took place between May 26 and May 31 and generated about $2.5 million. The proceeds are expected to support preferred stock distributions, including cash dividend obligations.

Broader market impact is also visible in the company’s equity performance. Strategy stock (MSTR) has declined about 77% from its peak, reflecting sensitivity to Bitcoin’s price movements and balance sheet exposure.

Over the same six-year period of sustained Bitcoin accumulation, the S&P 500 gained roughly 116%. This contrast underscores a widening performance gap between traditional equity benchmarks and firms with concentrated Bitcoin exposure.

Holding Through the Downturn

Executive Chairman Michael Saylor built the company’s Bitcoin strategy in 2020 by converting corporate reserves into digital assets as an inflation hedge. The firm maintains that it will continue holding BTC despite losses, with its strategy focused on long-term exposure rather than short-term stability.

Market observers say the unrealized loss highlights how Bitcoin price swings directly affect corporate balance sheets tied to digital asset exposure. They remain divided on whether the strategy amplifies volatility compared with diversified portfolios during extended downturns.

Nvidia CEO Jensen Huang called Marvell Technology the next trillion-dollar company at Computex on June 2. Marvell shares jumped about 33% in a single session, their biggest one-day gain on record. The move added roughly $56 billion in market value, pushing Marvell above $250 billion.

The endorsement landed as investor Michael Burry warned that Nvidia itself faces concentrated demand and hidden financing risk across the AI buildout.

Huang made a surprise appearance during Marvell CEO Matt Murphy’s keynote in Taipei, spending about 10 minutes on stage. He praised Marvell’s networking and connectivity chips as essential to data centers, where AI workloads run across thousands of linked processors that must share data quickly.

The remark followed Nvidia’s roughly $2 billion equity investment in Marvell, which tied the firm’s custom accelerators and optical networking to Nvidia’s AI factory architecture.

BREAKING: Marvell Technology, $MRVL, extends gains to over +45% in 2 days after Nvidia CEO Jensen Huang says it could become the “next trillion-dollar company.”

Bulls argue connectivity is the next bottleneck in AI systems after raw compute and memory. Marvell builds the switches, optics, and custom silicon that link those clusters, and data center products now drive most of its revenue.

Skeptics counter that Marvell trades at a steep valuation. It also faces strong competition from Broadcom in networking silicon.

“…the next trillion-dollar company,” CNBC reported, citing Jensen Huang.

A single endorsement rarely changes fundamentals, yet Huang’s words carry weight with traders. Analysts have also stayed broadly bullish on Nvidia, reflecting confidence in the wider AI trade.

Michael Burry’s Warning on Nvidia

Michael Burry, known for his role in The Big Short, has taken the other side of the AI story. His firm, Scion Asset Management, bought put options (short orders) on one million Nvidia shares.

Burry flagged Nvidia’s customer concentration as a core risk. He said the top three customers now account for 64% of Nvidia’s accounts receivable, up from 56% the prior quarter and about 33% in 2020.

🚨Michael Burry says Nvidia has 3 big customers and if they stop buying the whole thing is over.

Those 3 customers now account for 64% of Nvidia’s entire accounts receivable.

In 2020 that number was 33%. It jumped 8 percentage points in a single quarter.

He also described much of today’s spending as a temporary benchmarking phase he calls a tokenmaxxing bubble. In his view, that demand looks permanent now, but could fade.

“The conditions for an aggressive fall are as strong as they have been in the history of the stock,” Burry stated.

His thesis points to leveraging hidden across the system. A Moody’s report in February found that Microsoft, Amazon, Alphabet, Meta, and Oracle have $662 billion in future data center lease commitments that are not yet reflected on their balance sheets.

That figure equals roughly 113% of the five companies’ adjusted debt, according to Moody’s. The obligations become real cash costs once the leases begin.

Other signals have added to the caution. Reports of falling H200 rental prices have raised questions about near-term GPU demand.

Strive (NASDAQ: STRV) purchased 2,500 Bitcoins between May 23 and June 1 for approximately $185.2 million, bringing the company’s treasury to 19,000 BTC

The 2,500 BTC purchase was funded almost entirely through the company’s Variable Rate Series A Perpetual Preferred Stock (SATA), with an average cost of about $74,092 per coin.

Is Strive still buying BTC?

An SEC 8-K filing confirmed that Strive raised most of the money used for its most recent Bitcoin purchase through its SATA stock. The company issued 1,754,188 new shares that generated approximately $175.4 million. The remaining $9.8 million came from selling Class A common stock (ASST).

The average price Strive paid per coin was $74,092, which is lower than its previous purchase when it bought 1,109 BTC at about $76,989 per coin. During the latest purchase window, Bitcoin traded below $71,000 at certain points, meaning the treasury firm bought during a price drop.

Strive’s holdings have risen from 16,500 BTC to 19,000 BTC, representing a 15.2% increase in total holdings over a single reporting period. The CEO, Matt Cole, disclosed the deal on X, adding that the company has a quarter-to-date BTC yield of 23.0%, a year-to-date yield of 36.7%, and an amplification ratio of 57.0%.

The 8-K filing also shows cash and equivalents rising from $93.3 million to $137.3 million, even after Strive spent $185 million on Bitcoin. Strive raised about $229 million total from both equity instruments, and the company stated that the higher cash balance helps it maintain an 18-month dividend reserve for SATA holders.

Strategy’s rare Bitcoin sale

Strategy (NASDAQ: MSTR), the largest corporate Bitcoin holder at 843,706 BTC, disclosed that around the same time as Strive’s purchase, it had sold 32 Bitcoins for $2.5 million to fund dividend payments on its own preferred stock, STRC. This is the second time Strategy has ever sold any of its Bitcoin holdings.

Michael Saylor, Strategy’s executive chairman, responded to Cole’s announcement regarding the Bitcoin purchase with a brief endorsement on X, posting “@Strive for Bitcoin.”

Cole previously announced that Strive expects to increase the size of its at-the-market programs by $2.1 billion each for Class A shares and SATA, which would bring total ATM capacity to approximately $5.15 billion. However, the expansion requires amended SEC filings and a certificate of amendment for SATA.

Strive plans to change SATA‘s current dividend payouts from a monthly to a daily basis beginning June 16, in order to smooth out the concentrated buying pressure that currently builds ahead of each monthly ex-dividend date, and potentially reduce the periodic pauses in Bitcoin accumulation that observers have noticed.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

President Donald Trump named Federal Housing Finance Agency Director Bill Pulte as Acting Director of National Intelligence on Tuesday. The pick drew immediate celebration from Bitcoin holders tracking his pro-crypto record.

The 38-year-old will keep his FHFA role and chairmanship of Fannie Mae and Freddie Mac. He will dual-hat the positions until a permanent DNI is nominated and confirmed.

Trump Picks Acting DNI

Pulte’s Pro-Crypto Record at FHFA

In June 2025, Pulte ordered Fannie Mae and Freddie Mac to recognize crypto in mortgage assessments. The directive removed any requirement that borrowers liquidate holdings first.

Bill is a great guy who recognizes that the bureaucracy of the intel community must respond to the elected leadership (rather than the other way around). He’ll do great! pic.twitter.com/nlK2tWXZjl

However, only assets held on U.S.-regulated exchanges qualify under the strict custody restrictions attached to the rule.

Federal disclosures list his personal holdings in Bitcoin (BTC), Solana (SOL), and miner MARA Holdings. Spousal crypto exposure reaches up to $2 million.

A Bitcoiner was just picked for DNI role,” cheered David Bailey.

Vice President JD Vance defended the pick in a separate post praising Pulte’s posture toward the intelligence community.

Bill is a great guy who recognizes that the bureaucracy of the intel community must respond to the elected leadership (rather than the other way around),” Vance added.

However, critics highlight Pulte’s lack of intelligence or national security background.

MAJOR BREAKING: Trump just put Bill Pulte, who has NO background in national security, and weaponized government to go after Trump Critics Letitia James, Adam Schiff, and Lisa Cook, in as the Acting Director of National Intelligence.

They note federal statute favors such experience, especially as the crypto market structure debate heats up in Congress. The acting role itself does not require Senate confirmation.

“He appears to have been selected precisely because the White House believes he will provide the narrative it wants, not the intelligence we need,” stated Senator Mark Warner.

OpenPayd has announced a merger agreement with Titan Acquisition Corp. that would list the company publicly on Nasdaq at a valuation of roughly $1.1 billion.

If OpenPayd follows through as planned, it would be a rare sighting of a crypto-linked firm advancing its listing plans after a string of digital asset and fintech companies recently paused or abandoned their own ambitions due to weak markets and falling token prices.

Which crypto firm is listing on the Nasdaq?

OpenPayd and Titan, a special purpose acquisition company (SPAC) trading on Nasdaq under the ticker TACHU, have signed a definitive business combination agreement that would list OpenPayd under the symbol “OP.”

If no Titan shareholders redeem their holdings, OpenPayd stands to receive up to $276 million in gross proceeds from Titan’s trust account to expand its business and strengthen its finances.

The company reported annualized recurring revenue above $85 million as of March 2026 and processes more than $240 billion in annualized transaction volume. OpenPayd’s client list includes eToro, Kraken, and OKX, and it operates across more than 180 countries. The deal values OpenPayd at $1.1 billion.

The boards of both companies approved the deal unanimously. The final closing is expected in the fourth quarter of 2026, dependent on shareholder approval and other standard conditions.

OpenPayd’s CEO, Iana Dimitrova, said that the transaction is a major milestone that shows the strength of the company’s platform. Founder Ozan Ozerk added that he believes the next decade of finance will be driven by autonomous systems, and that going public will give his firm the money and mission to lead that market

OpenPayd’s listing comes as crypto listing plans stall across the industry

OpenPayd’s timing stands out as several major crypto firms have delayed or shelved public offerings this year due to a decline in prices and a lack of investor interest.

Cryptopolitan reported that Consensys, the company behind the MetaMask Ethereum wallet, pushed its planned U.S. IPO to at least fall of 2026 after crypto markets dropped sharply earlier in the year. JPMorgan and Goldman Sachs were working on the offering.

Grayscale, one of the largest crypto asset managers and the firm behind the Bitcoin Trust ETF (GBTC), also paused its IPO preparations and is unlikely to restart before the fourth quarter.

Kraken suspended its own multibillion-dollar IPO earlier in 2026, just months after raising $1.3 billion across two funding rounds that valued the exchange at over $20 billion. Cryptopolitan also previously reported that the hardware wallet maker, Ledger, paused a planned $4 billion listing.

BitGo is the only crypto-native firm to complete a U.S. IPO so far this year. The digital asset custodian raised about $213 million in January, but its shares now trade roughly 36% below the offering price.

Titan CEO Frank Mastrangelo called OpenPayd what he believes to be “the first publicly traded, pure-play global payments infrastructure platform at the intersection of traditional finance and digital assets,” per the joint announcement.

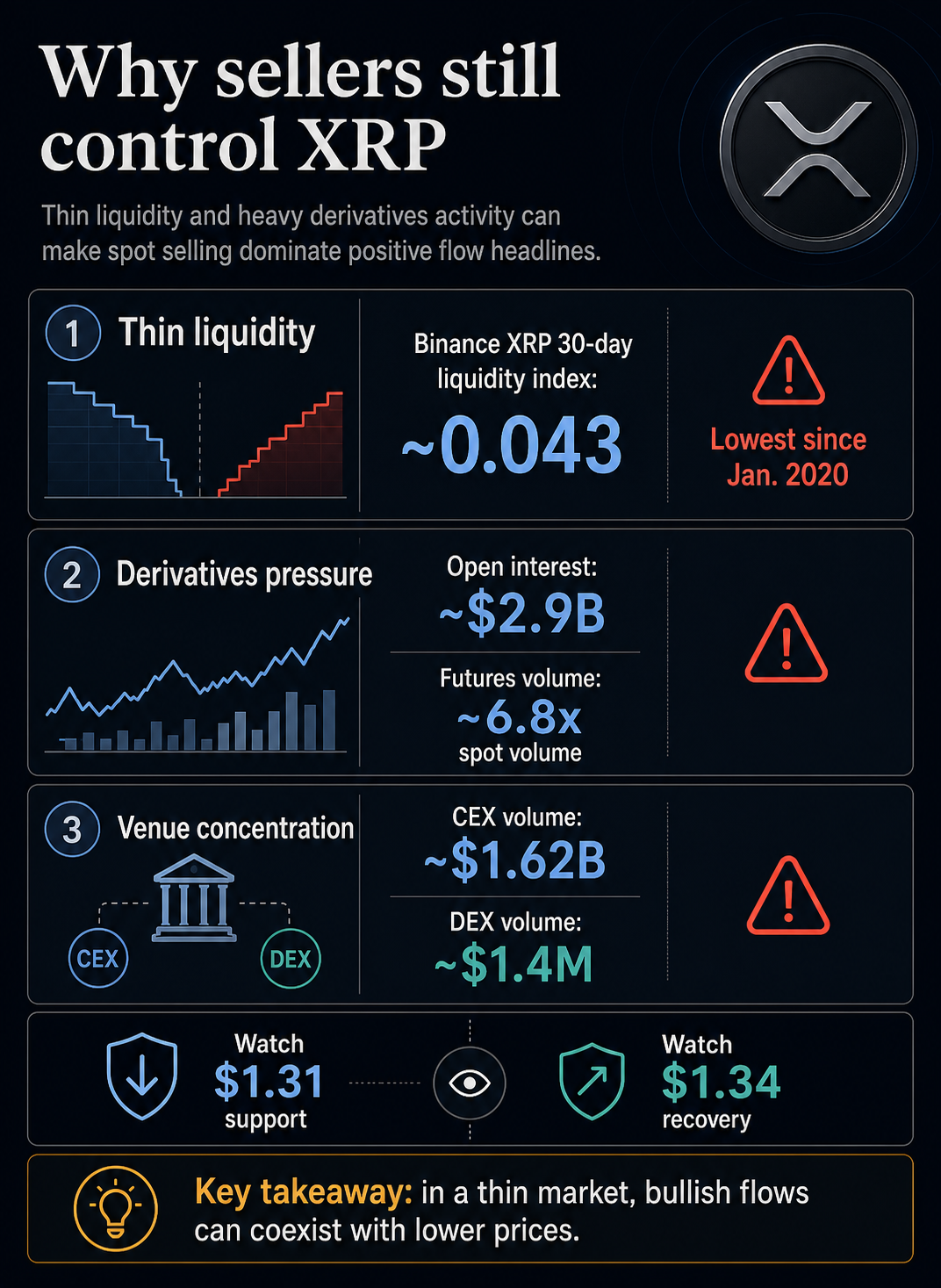

XRP is giving traders a contradiction that separates flow data from actual market control.

The token has been trading around the low-$1.30s after hitting its weakest level in roughly 15 weeks, even as two data points bulls often treat as supportive moved in the other direction.

Spot XRP ETFs have continued to attract money, with cumulative inflows around $1.42 billion, while late-May exchange-flow data showed more than 25 million XRP moving off exchanges after a prior inflow.

That combination would normally invite a simple accumulation case. Less XRP on exchanges can mean less immediately available sell-side supply. ETF inflows can show that regulated wrappers are still drawing capital.

Yet price action points to something colder: neither signal has been enough to stop sellers from setting the marginal price.

CryptoSlate’s XRP market page showed the asset near $1.30 on June 1, with a market cap around $80.87 billion and roughly $1.62 billion in 24-hour volume.

The token remains a top-five crypto asset by market value, but that size has not protected it from a market where rebounds are still being sold.

ETF demand remains indirect

The ETF side of the story has the clearest bullish potential.

SoSoValue data puts late-May spot XRP ETF inflows at roughly $11.8 million on May 29, taking cumulative net inflows to about $1.4 billion. Investor demand for XRP exposure through regulated products has continued during the latest drawdown.

ETF inflows are separate from immediate control of the spot market. They show that capital is entering a wrapper. They do not prove that enough aggressive buying is hitting exchange order books at the moment sellers are pressing sell orders through the market.

XRP has already spent much of May showing the same disconnect.

A recent analysis of XRP’s bullish signals found that ETF inflows, exchange withdrawals, and rising ledger activity had built a constructive setup, while price action still failed to follow.

The June 1 low moves that setup forward from a stalled bullish case to a clearer test of whether those flows can support the token before traders give up on the support zone.

Signal

Bullish case

Offsetting pressure

Spot XRP ETF inflows

Regulated-product demand remains visible

Wrapper demand has yet to overpower spot selling

Late-May exchange outflows

Less XRP may be available for immediate selling

The flow followed a large exchange inflow and covers a short window

XRP still near the top of market rankings

Liquidity and attention remain deep relative to most altcoins

The token is still near a 15-week low

Prior accumulation signals

Bulls can argue that supply is being absorbed

Price keeps treating rebounds as sell zones

The table shows the risk in reading ETF demand in isolation. Each constructive signal has a plausible bullish interpretation, but each also has an offsetting pressure that carries more weight for price right now.

What traders need to ask now is whether those flows are strong enough, direct enough, or immediate enough to change who controls spot trading.

Santiment showed a 22.80 million XRP exchange inflow before the balance reversed, with about 25.24 million XRP moving off exchanges in late May.

The second part of that sequence can look constructive. Coins leaving exchanges often reduce the supply available for fast selling and can point to custody, accumulation, or positioning away from trading venues.

In a stronger market, such a move could help confirm a bounce.

A 22.80 million XRP inflow shows that meaningful supply had also moved toward exchanges before the reversal.

The outflow that followed carries weight, but it leaves the earlier sign of sell-side pressure in the picture. It also cannot prove by itself that buyers are willing to absorb spot supply at higher prices.

The price response shows why the distinction counts. If XRP moves off exchanges and the price still falls to a multi-month low, visible exchange balances are only one part of the pressure.

Spot demand, order-book depth, leverage, and trader confidence can all carry more weight in the immediate window.

CryptoSlate’s XRP data also shows why centralized exchange behavior can be impactful: XRP’s 24-hour CEX volume was around $1.62 billion, compared with DEX volume of about $1.4 million.

For this market, the main price signal is still being formed on centralized venues, so exchange flows and liquidity conditions are where the ETF and accumulation narratives meet live selling.

The sell-zone pattern has been building for months. An earlier analysis found that XRP losses were forcing late buyers out and turning rebounds into fresh selling areas.

The latest low suggests that behavior has not fully cleared. Outflows can reduce potential supply, but they cannot repair sentiment if traders keep using every bounce to exit.

The strongest explanation for the contradiction is market structure.

XRP can keep some bullish signals and still leave sellers in control when liquidity is thin enough, and spot conviction weak enough, for marginal selling to push through supportive flow headlines.

A recent look at XRP liquidity found that Binance’s 30-day XRP liquidity index was near 0.043, its lowest level since January 2020, while all-exchange open interest hovered near $2.9 billion and futures volume ran at about 6.8 times spot volume.

Under those conditions, price can move sharply even when the broader story contains bullish data points.

Thin liquidity changes how flow signals should be understood. In a deep market, ETF inflows and exchange outflows may help absorb selling pressure over time.

In a less liquid market, a smaller burst of spot selling can still move price, especially if derivatives activity is high and traders are leaning on the same levels.

Broader ETF rotation is less important here than it might look at first. XRP inflows have stood out at times while Bitcoin and Ethereum products faced pressure, and CryptoSlate has covered that ETF rotation.

Relative ETF strength is different from outright price strength. XRP can attract capital through one channel and still fall if the spot market is weaker, less liquid, or more leveraged than the inflow headline suggests.

For now, the next test is price, rather than another bullish data point. Buyers need to make the supportive flow signals visible in the chart.

A recovery through the low-$1.30s and a reclaim of the $1.34 area would show that buyers are finally absorbing visible sell pressure.

A loss of the $1.31 area while ETF inflows and exchange outflows remain constructive would strengthen the opposite case: XRP can have institutional wrapper demand and apparent accumulation without giving bulls control of the spot market.

So there is still a contradiction here. The flows say some capital is still moving toward XRP. The price says sellers are still winning.

Bitmine (BMNR) has once again purchased ETH this week, acquiring 26,497 ETH for about $53 million, a massive 75% cut from its last weekly purchase of 120,000 ETH. This comes amid dips in the company’s stock in addition to a drop in Ethereum’s market performance in the past week.

The approximately 75% reduction in buying pace comes as BMNR shares have fallen 38% over the past year, trading near $19.27, with a slip in Ethereum itself by almost 1.8% over the past 24 hours to roughly $1,980.

Bitmine approaches 5% target

Bitmine’s total Ether holdings now sit at about 5.42 million tokens, or 4.49% of the entire network’s circulating supply of about 120.7 million ETH, the company said. That puts the firm at about 90% of the way toward its well publicized goal of controlling 5% of ETH’s total supply.

Chairman Tom Lee, who is also Fundstrat’s co-founder, has mentioned repeatedly that the deceleration in ETH purchases are intentional. At Consensus 2026 in Miami last month, Lee said Bitmine planned to reduce its rate of accumulation as it closed in on the 5% threshold, as previously reported by Cryptopolitan.

“In our view, ETH prices are not reflecting the strengthening of Ethereum fundamentals,” Lee said in Monday’s statement. “But then again, this is not surprising given we are in the early stages of crypto spring.”

The company has purchased more than one million ETH since January, making it the largest publicly traded Ethereum treasury firm by holdings.

Bitmine’s portfolio and staking plans

Bitmine reported total crypto and cash holdings of $11.6 billion as of May 31, holding 203 Bitcoin, $446 million in cash, a $180 million stake in Beast Industries, and a $93 million position in Eightco Holdings (ORBS) beyond its total ETH holdings.

Staking has become a massive revenue stream for Bitmine, as about 4.7 million tokens of Bitmine’s 5.4 million ETH have been staked through its MAVAN platform. This makes the company the largest Ethereum staker globally. The firm estimates an annual staking revenue of $258 million currently, with projections reaching $300 million by the end of 2026.

Markets have been negative

This ETH purchase slowdown has also come during a rough stretch for the general crypto markets. Bitcoin dropped by about 2.5% and briefly fell below $72,000 after Michael Saylor’s Strategy (MSTR) disclosed its first BTC sale since 2022, selling 32 coins for $2.5 million to cover dividend payments.

Retail traders on Stocktwits also expressed frustration regarding BMNR’s stock decline, comparing its poor performance to Hyperliquid Strategies (PURR), whose stock was approaching a record high as Hyperliquid’s native token topped $74 and entered the top 10 cryptocurrencies by market cap.

Bitmine needs to purchase roughly another 61,000 ETH to hit the 5% total ETH supply ownership mark. At last week’s buying pace, that would take the company about two weeks. This means the firm is right on the cusp of its 2026 goal, and it is yet to be seen how this would positively or negatively impact the BMNR stock price.