There are two distinct paths that the prediction market sector is taking.

Platforms are rapidly growing in the US to draw big investors and expert traders. Italy is the most recent nation to outlaw a significant prediction market platform, while other nations tighten laws.

Kalshi builds a professional trading cockpit

Kalshi has introduced Kalshi Pro, a desktop trading platform for seasoned traders, in the United States.

The platform is intended for customers who trade simultaneously in several markets, respond rapidly to real-time events, or make limit orders that are only fulfilled when a predetermined price is met. Currently in beta, Kalshi Pro is available for free.

According to the corporation, its business has been expanding quickly. Its yearly trading volume has tripled to $178 billion, with a significant portion of activity coming from quantitative trading firms and seasoned traders referred to as “sharps.”

To obtain a competitive advantage, these traders have historically depended on customized procedures, direct data linkages, and proprietary software.

All of those capabilities and tools are intended to be combined on a single platform with Kalshi Pro.

The new platform uses the same account and balance as Kalshi’s regular app. It also adds advanced trading tools that have long been available to professional stock and bond traders through traditional brokerages and exchanges.

“Kalshi’s active traders are already trading prediction markets and perpetuals like Wall Street trades equities and bonds,” said Andy Chang, the Kalshi Pro product lead. “We built Pro to give them the cockpit they deserve.”

For seasoned traders, Kalshi Pro offers a number of new tools. One tool that allows users to watch and trade numerous marketplaces simultaneously is called Canvas.

Active Markets Screener is another tool that lets traders keep an eye on around 2,000 active markets simultaneously.

Along with integrated risk management features like stop-loss and take-profit orders, it also provides everlasting futures trading with licensed TradingView charts.

Kalshi Pro’s release follows the company’s other significant accomplishment. Under the direct supervision of the Commodity Futures Trading Commission (CFTC), Kalshi just became the first trading platform in the United States to provide cryptocurrency perpetual futures. In just one week, the trading volume of these contracts hit $1 billion.

Italy blocks Polymarket for the second time

Across the Atlantic, the picture looks very different.

Polymarket, one of the biggest prediction platforms in the world, has been cut off in Italy for the second time. The Italian Customs and Monopolies Agency, known by the initials ADM, has added the website to its official list of blocked addresses, saying the platform does not comply with Italy’s gambling laws.

This is not the first time Polymarket has clashed with Italian authorities. The ADM first blocked the platform in October 2025, but that decision was reversed in December of the same year after Polymarket challenged it in the Regional Administrative Court of Lazio.

Following the Italian football team S.S. Lazio’s sponsorship deal with Polymarket, the matter gained even more attention.

The agreement raised awareness of the platform and introduced the discussion to the Italian parliament.

Compared to overseas platforms operating in Italy without authorization, licensed gambling companies contend that they must adhere to far tougher advertising regulations. Additionally, critics claimed that the nation’s current legislation should prohibit a platform that has been identified as an unlawful operator from sponsoring sports teams.

It is now anticipated that AGCOM, Italy’s communications regulator, will finish reviewing the sponsorship agreement.

Polymarket has always insisted that it provides a financial service rather than a gambling product.

According to the firm, users in Italy are only permitted to examine market data and are not permitted to trade on the platform. Even so, the ADM’s decision to blacklist Polymarket again shows a wider trend.

Regulators in several countries are increasing their scrutiny of prediction market platforms that operate without a local license. At the same time, the industry is moving in different directions around the world.

While prediction markets are becoming more popular and accepted in some countries, they are facing stricter rules and tougher regulatory action in others.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

A New York federal court has returned prediction-market access to state hands just weeks before the CFTC closes comments on national event-contract rules.

In a July 7 opinion and order, Judge Analisa Torres of the Southern District of New York denied KalshiEX LLC’s request for a preliminary injunction to block New York gaming officials from enforcing state gambling law against its sports-event contracts while the case proceeds.

The decision is preliminary. It leaves the merits open, but it rejects Kalshi’s bid for immediate relief on the argument that the Commodity Exchange Act preempts New York’s gambling laws as applied to those contracts.

The access risk now has two tracks: whether the Commodity Futures Trading Commission accepts event contracts at the federal level, and whether states can force platforms to block, limit, or redesign access before the federal framework is finished.

The order landed while the CFTC’s proposed prediction-market rules remain open for comment. The agency’s June 12 Federal Register notice gives interested parties until July 27 to comment on proposed public-interest determinations for event contracts, including contracts involving gaming or activity unlawful under federal or state law.

A related CFTC release said the framework would apply to growth in event contracts, including those referencing sporting events.

Torres’s order sharpened the access issue before that process closes. The court rejected Kalshi’s argument that CFTC-designated contract market rules requiring impartial access effectively require nationwide access to sports contracts.

It also treated the cost of geolocating users on a state-by-state basis as an ordinary regulatory compliance burden, undercutting Kalshi’s irreparable harm argument.

That part of the ruling carries the most operational weight for venues. Geofencing may be expensive, disruptive, and inconsistent with a national market, but the order leaves room for states to keep pressing their gambling-law theories while platforms litigate.

The order binds Kalshi’s New York case. The product category is already broader.

Crypto.com describes its sports-event trading as a CFTC-regulated derivatives feature. Coinbase says its prediction markets are available to U.S. residents, but not in Nevada.

CryptoSlate has previously tracked how state-vs-CFTC fights can turn prediction-market compliance into refunds, blocked access, and venue-by-venue risk. New York adds a new pressure point because the court said state gambling law can complement federal commodities law, at least at this stage.

The next signal is whether the CFTC’s final rule reduces that fragmentation or leaves platforms with a national listing process and local access map. Until then, prediction markets can win federal recognition and still face state-by-state limits on who can actually trade.

The FIFA World Cup is always one of the hottest events for betting, but prediction markets are making this scene more explosive this year.

Who wins tonight? Who survives the group? Which favorite looks shaky? Which underdog has a real chance? While these are casual arguments for most football fans, crypto exchanges are turning them into monetizable user behavior.

That is why the 2026 World Cup has become a month-long attention engine, filled with live results, emotional swings, and daily predictions. Zoomex is one of the exchanges trying to plug into that rhythm through match predictions, trading tasks, rewards, and World Cup ticket access.

The campaign is less interesting as a one-off promotion and more useful as a sign of where exchange marketing is heading. Crypto firms are moving closer to live sport because sport already does what platforms want users to do: return daily, take a side, react quickly, and argue about the next outcome.

Prediction markets exceeds 2B in volume just for this World Cup. From people who knew one thing — a team, a trend, a trade — and backed themselves. You know something too. That is all it takes.

The 2026 World Cup gives platforms a bigger stage than usual. It is the largest edition in tournament history, with 48 teams, three host countries, and 104 matches. That means more fixtures, more upsets, and more reasons for fans to check back every day.

Pew Research found that combined monthly trading volume on Kalshi and Polymarket rose from less than $5 billion in September 2025 to about $24 billion in April 2026.

Sports already drive much of that activity. Pew said sports accounted for 80% of Kalshi trading volume and 39% of Polymarket volume since July 2024.

So, football gives exchanges a simpler entry point than politics, macro data, or token prices. A match result is easy to understand. The uncertainty is the product.

Zoomex’s World Cup Prediction Campaign follows that logic. Users can predict match outcomes, group-stage results, knockout progress, finalists, and the eventual champion. The exchange is using football as a familiar doorway into prediction-style products.

Zoomex has also added a trading campaign built around volume-based tasks and rewards. Users can compete for USDT, vouchers, bonuses, and World Cup ticket packages. Some prizes include access to group-stage matches, semi-finals, and the final, depending on eligibility and campaign rules.

The ticket rewards give the campaign its sharper hook. World Cup access has become expensive this year. Reuters reported that face-value tickets for the 2026 final range from $2,030 to $6,370, a sharp jump from the 2022 final in Qatar.

That makes match access more powerful than a routine bonus. For a trader who also follows football, a World Cup ticket carries emotional weight. It turns a platform campaign into a possible real-world memory.

These campaigns usually come with KYC checks, trading-volume targets, reward caps, eligibility rules, risk-control reviews, and “up to” prize pools. Those details decide whether users see the campaign as useful or as another glossy exchange promotion.

Crypto Wants the Group Chat

The social layer is part of the strategy. Zoomex plans X Spaces with former footballers including Djibril Cissé, Didi Hamann, David James, Javier Mascherano, and Fernando Llorente. The goal is to keep the campaign inside football conversation, not just within the trading dashboards.

FIFA said the 2022 tournament generated 93.6 million social posts, with a cumulative reach of 262 billion and 5.95 billion engagements.

Crypto brands want a place inside that stream. They want the reply, the prediction, the share, and the return visit. During a World Cup, each match gives them a new reason to ask for one.

This is part of a longer sports push. Crypto companies spent heavily on sports sponsorships during the last bull cycle, using football, racing, and combat sports to reach people who did not spend their days on crypto Twitter.

The difference now is that campaigns are becoming more interactive. The brand no longer only wants visibility. It wants action.

The Hype Has Rules

The risk is that sports-themed campaigns can blur into aggressive user acquisition if the rules are unclear. Regulators are already watching crypto and trading links in sport more closely. The UK FCA recently warned football clubs about legal, money laundering, and reputational risks tied to unauthorised crypto and trading sponsors.

That does not make every campaign suspicious. It does mean execution is more critical than ever.

Zoomex has a timely idea because football predictions feel natural during the World Cup. The campaign will stand or fall on simpler questions. Are the rules clear? Are rewards distributed fairly? Does the prediction product work well? Does the football content feel real?

Overall, the bigger shift in the integration of crypto and sports events is already visible. The World Cup has become a live testing ground for crypto exchanges that want users to behave less like passive account holders and more like daily participants.

Something big just happened in US crypto trading. The Commodity Futures Trading Commission has cleared the way for a brand new kind of crypto product to be sold inside the country, and one trading platform has already jumped in to offer it.

According to a cryptopolitan report, Kalshi, a platform best known for letting people bet on real-world events, started selling Bitcoin perpetual futures to American customers on June 3.

These are called BTCPERP, and Kalshi is now the first company to sell this kind of product after getting the green light from the CFTC.

Perpetual futures are financial contracts tied to Bitcoin’s price that do not have a set expiration date.

Rather than expiring and settling on a specific day, they use a funding-rate mechanism to keep the contract price closely aligned with the underlying market.

Profits and losses are paid in cash, meaning traders do not take delivery of actual Bitcoin.

These products are widely traded around the world, with offshore platforms recording more than $90 trillion in volume last year.

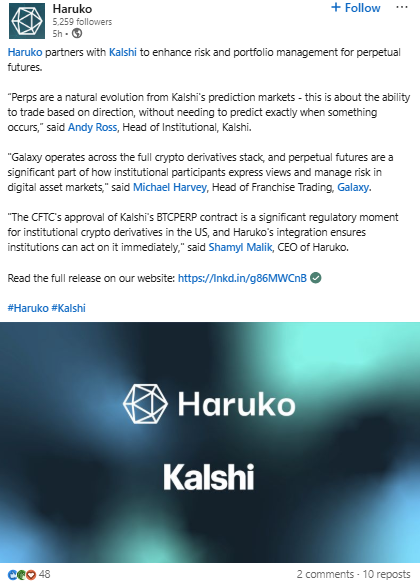

The official launch of Kalshi’s strategic integration with Haruko, a digital markets risk and portfolio management platform, marks a significant milestone in bringing regulated Bitcoin perpetual futures to the U.S. market.

In addition to traditional asset classes, this framework is intended to provide institutions with an instantaneous, compliant solution to handle their new onshore perpetual positions.

How risk software opens the door to Kalshi’s new crypto perps

Getting approval from regulators is only part of the story.

Big investors and institutions follow strict rules about how they manage money and risk, and that’s a much bigger hurdle than just having a legal product to trade. This is where a company called Haruko comes in.

Large institutional investors in a variety of asset classes employ Haruko’s portfolio and risk management software.

By integrating its platform with Kalshi’s recently established perpetual futures market, the business enables customers to trade the new Bitcoin contracts while using the same interface to track their exposure and risk in real time.

Haruko partners with Kalshi to elevate institutional crypto risk management. Source: Haruko

This connection allows companies like Galaxy Digital to monitor Kalshi’s perpetual futures on the same platform as their other holdings, which include traditional assets, spot cryptocurrency positions, and investments in decentralized finance.

Because of this, investors can integrate these regulated contracts into their current processes without having to create new infrastructure or redesign their current systems.

Shamyl Malik, who runs Haruko as CEO, said the CFTC’s approval marks a big moment for institutions trading crypto derivatives in the US.

He pointed out that perpetual futures have been hugely popular in crypto markets around the world for a long time, but until now, there was no way for US based institutions to access them through a regulated channel.

He said that with Haruko, firms adding Kalshi’s perpetuals don’t need new infrastructure and don’t have to give up any of their existing oversight or standards.

What institutions are saying about the new market

Michael Harvey, Galaxy’s head of trading, said the lack of a regulated U.S. market for perpetual futures had been a major challenge.

With Kalshi’s new offering, Galaxy can now manage these positions using the same risk management system it already relies on for the rest of its portfolio, without changing its existing processes.

Andy Ross, who oversees institutional business at Kalshi, described perpetual futures as a natural extension of the company’s prediction market products.

He said the goal is to give traders a way to bet on price movements without having to predict exactly when something will happen.

Ross added that a regulated marketplace serving both institutional and retail traders is the next logical step for the industry, and said Kalshi is pleased to work with Haruko and Galaxy to make the product easily accessible to institutional investors.

Industry participants expect this development to encourage greater trading activity and pave the way for additional products, especially as trading, compliance, and reporting become more integrated and easier to manage.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Investors are speculating about when the official announcement may be made because the company behind ChatGPT appears to be preparing for a stock market debut.

As early as Friday, OpenAI may discreetly submit draft filings for an IPO, as per some sources.

According to reports, the corporation, which is presently valued by private investors at over $850 billion, has engaged Morgan Stanley and Goldman Sachs to help with the IPO preparations.

The file might be made in the upcoming days or weeks, according to the unidentified source.

Legal obstacles cleared, timeline accelerates

The artificial intelligence firm hasn’t publicly confirmed any specific dates.

In a statement, OpenAI said it “regularly evaluates strategic options” while staying focused on current business priorities.

But internal preparations have been underway to potentially launch the offering during the final three months of this year.

The move forward comes just two days after a federal judge threw out Elon Musk’s lawsuit against the company. Musk had sought $150 billion in damages and wanted to stop OpenAI from converting to a for-profit structure.

Getting this legal matter resolved appears to have cleared a significant roadblock and may have encouraged company leadership to move faster.

OpenAI might attract less concentrated attention while communicating with investors by submitting around the same time as SpaceX.

In what may become one of the largest market listings ever, money managers will now have to consider both well-known corporations.

Traders bet heavily on 2026 announcement

Reports of the possible filing quickly fueled activity in prediction markets.

On Kalshi, traders sharply increased the chances of OpenAI going public before its rival Anthropic.

On the prediction market platform, confidence in OpenAI continued to rise sharply, with traders assigning the company an estimated 84% to 85% chance of going public ahead of its rivals.

In contrast, contracts tied to Anthropic on Polymarket remained much lower at roughly 22%, reflecting significantly less optimism about the Amazon- and Google-supported startup moving toward an IPO in the near term.

The widening gap between the two businesses’ odds suggests that investors are becoming more confident in OpenAI’s aggressive efforts to capitalize on the generative AI industry’s explosive growth and the robust demand for high-profile technology stock offerings.

Because many investors now anticipate a significant announcement within the next year, trading activity on prediction platforms has increased significantly.

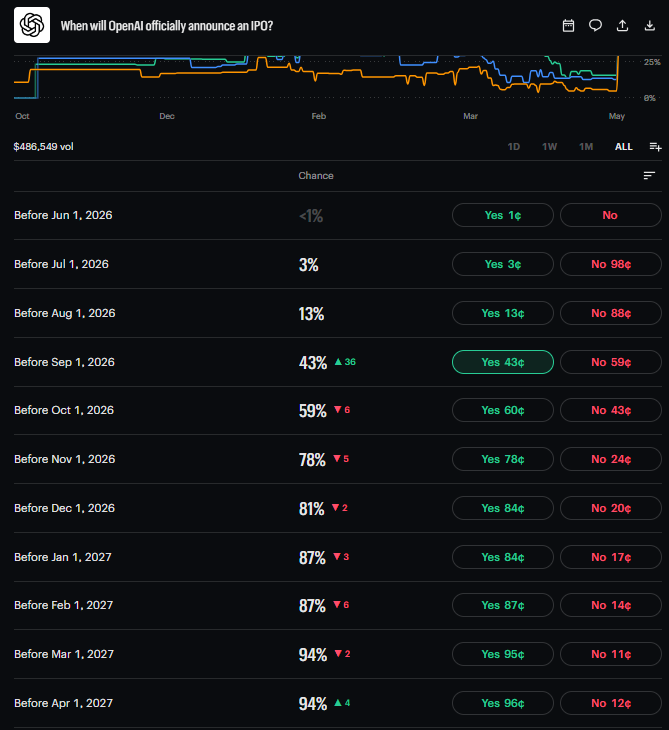

The likelihood of an IPO-related announcement by 2026 has increased to 88%, according to Kalshi.

Data from Kalshi reveals spiking trader confidence for an upcoming OpenAI IPO

According to Polymarket, OpenAI has a 73% chance of formally going public by the end of 2026.

Looking at more specific timeframes, traders think the formal announcement will most likely arrive during late summer or autumn months.

Polymarket shows a 72% probability that OpenAI will launch its IPO by December 31, 2026.

Kalshi markets currently price an announcement before November at 81%, with bets specifically on before November 1 at 78%.

The odds drop to 60% for an announcement before October and 38% for before September, although two sources indicate OpenAI aims to complete the process as early as September.

Furthermore, competitors are under increased pressure as a result of these reports.

Prediction market participants, however, don’t seem to believe Anthropic will go public anytime soon.

According to reports, Anthropic is talking with investors to obtain capital at a valuation of approximately $900 billion, which might exceed OpenAI’s current private valuation.

The corporation reported that its annualized revenue had surpassed $30 billion in April.

Despite those numbers, there has been a noticeable change in market attitude due to recent revelations concerning confidential IPO filings; many traders now anticipate that OpenAI will reach Wall Street before its competitor.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Prediction markets processed more than $44 billion in wagers last year, but regulators say many of the top-performing participants are now automated trading bots rather than humans.

On Polymarket, automated bots now run more than 30% of active accounts. Data from the platform’s top earners shows that 14 of the top 20 accounts are controlled by bots.

More than 37% of these automated accounts consistently.

Lawmakers target insider trading risks

Polymarket trading activity fell 8.9% in April for the first time since August, as competitors gained market share.

According to Dune Analytics, the platform and its US operation registered $10.2 billion in bets in April, a decrease from $11.2 billion the previous month.

Meanwhile, rival platform Kalshi saw volume jump 13% to reach $14.8 billion in April.

The decrease occurred as Polymarket tried to rebuild its US footprint while under increased scrutiny from politicians concerned about insider trading.

Senator Elizabeth Warren wrote to the Commodity Futures Trading Commission in March, along with more than 40 other members of Congress.

They wanted laws that would ban government officials from profiting from secret material on these platforms.

“The CFTC maintains that event contracts are a type of swap subject to its jurisdiction, and, therefore, it should ensure that federal employees understand existing restrictions on prediction market insider trading,” the lawmakers said.

Several Polymarket users have drawn suspicion for placing winning bets on sensitive world events, including military actions in Venezuela and potential conflict with Iran.

CFTC Chairman Michael Selig told reporters that the agency utilizes AI tools to examine trade patterns, detect anomalous conduct, and collaborates with blockchain tracking businesses like Chainalysis to monitor offshore platforms such as Polymarket.

According to an AIMPACT update dated May 15, the CFTC uses AI to scan vast volumes of trading data, assisting staff in identifying suspect accounts and deciding whether to initiate investigations or issue subpoenas.

The business is combining blockchain analytics tools with market anomaly detection technologies to monitor both cryptocurrency and traditional financial markets.

The CFTC has received many allegations of odd trading and is actively looking into “hundreds to thousands” of potential cases. Future enforcement efforts are likely to broaden.

Selig stated that the agency will take action against U.S. users who attempt to mask their location by utilizing VPNs to access prohibited services.

That enforcement applies to worldwide marketplaces.

Even while platforms like Polymarket operate outside of the United States and lack U.S. licenses, the CFTC said it will seek enforcement against cross-border trades involving Americans and may utilize extraterritorial authority if necessary.

Platforms are reacting to the demand.

Polymarket and Kalshi have improved their checks for insider trading and market manipulation, bringing in external blockchain data providers to meet regulatory requirements.

The CFTC offered prediction market platforms some regulatory relief on Wednesday, issuing a no-action letter that exempts them from certain swap reporting requirements.

The exemption applies to exchanges and clearinghouses that handle event contracts.

Agency staff said they would not pursue enforcement against platforms that skip those reporting rules, following requests from companies seeking clarity on how event contracts should be regulated.

Although event contracts are officially classed as swaps since they have yes-or-no outcomes, the CFTC believes they work more like futures and options due to their uniform terms and exchange trading.

According to the new guidance, firms can report these transactions directly to the Commission in a manner similar to futures and options markets.

The relief now applies to 19 firms, including Polymarket US, Kalshi, Gemini Titan, and Bitnomial. Other companies listing event contracts may request coverage on the same terms.

Top prediction market platforms, including Kalshi and Polymarket, are rushing to offer highly leveraged crypto derivatives at the exact moment state and federal authorities are clashing in court over whether the industry’s core products constitute illegal betting or legitimate financial instruments.

Over the past year, these companies have gained national prominence by facilitating wagers on discrete, real-world occurrences, ranging from political races to macroeconomic data releases.

Now, by preparing to list perpetual futures, which are complex contracts that never expire and allow traders to multiply their market exposure using borrowed funds, these platforms are blurring the line between niche forecasting hubs and full-service digital asset exchanges.

Against this backdrop, this shift drastically expands their potential customer base, but it also amplifies the legal risks associated with the platforms.

Historically, platforms like Kalshi operated on a cyclical, event-driven basis, with traffic and trading volume spiking around major catalysts such as a presidential debate or a championship sporting event and then plummeting once the outcome was settled.

In this kind of market, a user purchased a binary “Yes” or “No” share, and the contract expired upon the event’s resolution.

Perpetual futures fundamentally alter that business model. Because these derivatives lack an expiration date, participants can maintain their market positions indefinitely, provided they meet ongoing margin requirements.

The instruments frequently allow users to leverage their bets up to 50 times their initial capital, attracting aggressive speculators seeking rapid returns from minute price fluctuations.

By rolling out these derivatives, Polymarket and Kalshi are abandoning their siloed event-contract operations to compete directly with centralized exchanges and retail brokerages. The underlying strategy for both platforms is to convert occasional political bettors into daily, high-frequency traders.

While Kalshi has explicitly stated its intention to enter the perpetuals arena, Polymarket’s exact roadmap remains guarded, including which specific assets it will cover and whether it will restrict access for US customers.

Why prediction markets are moving into perpetual futures

Why perps, why now?

The motivation to embrace this new feature comes down to basic market structure.

Traditional crypto spot trading, which is the simple buying and holding of digital assets, has decelerated from the frenzied peaks of previous market cycles, logging $18.6 trillion in volume last year.

Meanwhile, perpetual futures generated more than three times that amount. Data from CryptoQuant show that the global trading volume for crypto perpetual futures hit $61.7 trillion last year.

That volume disparity dictates corporate strategy. Platforms recognize that to maintain engagement during periods of low volatility, they must offer instruments that allow users to short the market, hedge portfolios, and employ leverage.

While prediction markets currently command significant capital, with all-time notional volume surpassing $150 billion, the episodic nature of event contracts cannot match the continuous, around-the-clock fee generation of a highly active derivatives order book.

Moreover, the broader financial technology sector is experiencing a rapid collapse of operational boundaries, with centralized platforms like Robinhood, Coinbase, and Gemini all embracing event-based offerings.

Mo Shaikh, co-founder of the Aptos blockchain network, noted that financial applications have historically trended toward consolidation, citing the expansions of legacy platforms like PayPal. However, he warned that forcing disparate user bases into a single application rarely succeeds seamlessly.

“The trader, the bettor, the long-term investor, the payments user, they show up for different reasons,” Shaikh said, adding that true value lies in controlling the underlying infrastructure. “Clearing, liquidity, identity, settlement, data, those layers can unify even if the frontends remain fragmented.”

Meanwhile, the shift among prediction market players is partially defensive.

Offshore decentralized exchange Hyperliquid, a dominant force in perpetual futures, recently encroached on the prediction sector by revealing plans to list its own event contracts.

As a result, the market is split on who holds the strategic advantage in the ensuing turf war.

Jiani Chen, a growth officer with the Solana Foundation, noted the technical disparities, arguing that decentralized derivatives exchanges have a much easier time adding prediction markets to their backend than prediction platforms do spinning up complex futures trading engines.

However, Kyle Samani, chairman of Forward Industries, dismissed the technical hurdles, arguing that customer acquisition is the true bottleneck for digital asset platforms. He said:

“It’s way harder to bootstrap liquidity and acquire normie users for prediction markets. Kalshi perps are going to crush.”

The legal fight is still about who gets to call it gambling

Legal battle over prediction markets

The aggressive product expansion coincides with an existential legal threat as state regulators are launching coordinated efforts to classify the prediction platforms as unlicensed casinos, rejecting the premise that event contracts are sophisticated financial tools.

On April 21, New York Attorney General Letitia James filed sweeping lawsuits against digital asset firms Coinbase and Gemini, demanding $3.4 billion in combined penalties and restitution.

James alleged the companies bypass state taxes and consumer protection laws by offering prediction markets to retail users, including minors.

State officials pointed to research by the National Institutes of Health linking early exposure to mobile betting with heightened risks of anxiety and financial distress, while noting American Psychological Association data showing severe mental health risks associated with gambling disorders.

James said:

“Gambling by another name is still gambling, and it is not exempt from regulation under our state laws and Constitution.”

The industry firmly rejects the gambling label, countering that the contracts are vital instruments for hedging geopolitical and economic risks.

The judiciary is already untangling the overlapping claims. A federal appeals court in Philadelphia ruled against New Jersey gaming regulators earlier this year, determining the CFTC held sole regulatory authority over Kalshi’s election and sports-related contracts.

This sequence of litigation reflects a deeply fractured regulatory perimeter that companies must navigate as they deploy new derivative products.

A bigger market, and a bigger regulatory target

The move into perpetual futures would further position prediction markets as part of mainstream financial infrastructure rather than a niche corner of online speculation.

That shift is already drawing attention from traditional finance. The Intercontinental Exchange, parent of the New York Stock Exchange, recently invested $2 billion in Polymarket, a sign that major market operators see commercial value in platforms built around event-driven pricing.

Supporters of the model argue that prediction markets are proving useful as both forecasting tools and trading venues.

In high-liquidity markets, Brier scores, a standard measure of probabilistic accuracy, have fallen as low as 0.0247 shortly before resolution, suggesting pricing errors narrow sharply as capital and participation deepen. Industry estimates also show that about 10% of proprietary trading firms are already active in event contracts, using them in part to hedge macro and policy risk.

That combination of data value and trading activity helps explain why platforms are racing to broaden their product mix.

Rob Hadick, managing partner at Dragonfly, framed the commercial logic bluntly:

“Owning your customer will be the only way to have longevity in this new world of broad financialization.”

However, not everyone sees perpetual futures as the natural next step.

Alex Momot, chief executive and co-founder of Peanut Trade, told CryptoSlate that the current push looks more like a response to tightening legal pressure than a durable product strategy.

He noted that regulators and some jurisdictions are moving against prediction markets, and as a result, these operators appear to be shifting closer to the crypto-exchange model, where the rules are clearer, and the risk of being classified as gambling is lower.

Momot argued that strategy may offer only limited relief. In his view, the deeper problem is liquidity. Without more depth, many of the sector’s most promising use cases, including hedging and insurance against real-world event risk, remain too small to scale.

He said the stronger long-term path may lie in index-style products, market aggregation, and pooled liquidity across events, structures that could make prediction markets look more like traditional derivatives or synthetic exposures.

That viewpoint points to a broader tension now shaping the industry. One camp sees perpetual futures as the fastest way to capture more trading volume and keep users active between headline-driven events. Another sees them as a tactical detour from the harder task of building deeper, more resilient liquidity.

Either way, the legal risk is rising. Dyma Budorin, founder and chief executive of CORE3, said the merging of prediction and derivatives markets is likely to draw closer scrutiny from regulators already struggling to define the sector.

He said:

“What we’re really seeing is a convergence toward perp-like behavior without the corresponding risk controls. If this trend continues, regulators won’t treat prediction markets as harmless forecasting tools, they’ll treat them as derivatives platforms operating outside the rules. And historically, that doesn’t end quietly.”

The New York litigation has already ensured that the fight over jurisdiction will remain central to the industry’s future. That battle could eventually reach the U.S. Supreme Court or force Congress to step in with a clearer statutory framework.

Until then, prediction-market operators appear willing to keep expanding through the uncertainty, betting that the commercial upside of perpetual futures is worth the legal exposure.

The numbers are in, and they are not pretty for everyday traders who bet on prediction markets.

Despite handling tens of billions of dollars in trades, these platforms appear to be leaving the overwhelming majority of users worse off financially.

Prediction markets have grown fast. By 2025, platforms like Polymarket and Kalshi were processing $28 billion in trading volume.

The idea behind them is simple: people bet on future events, and the odds that form are supposed to reflect what the public genuinely believes will happen.

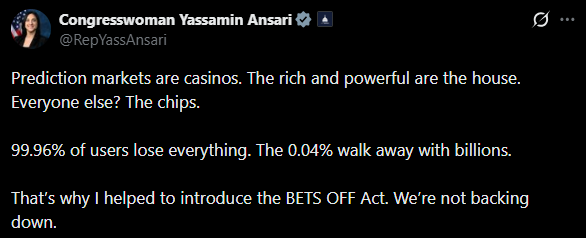

Arizona Democrat Yassamin Ansari recently targeted both Polymarket and Kalshi, calling them “casinos where the rich and powerful are the house and everyone else is the chips.”

She posted on X that 99.96% of users lose everything while the top 0.04% walk away with billions.

Ansari slams the prediction market as a rigged casino Source: @RepYassAnsari

Her claim comes from a December 2025 on-chain analysis by a blockchain researcher known as DeFi Oasis.

That study found that less than 0.04% of Polymarket wallet addresses captured more than 70% of all realized profits, totaling $3.7 billion.

Analysts, however, pointed out that Ansari’s wording mixes up two separate figures. The 0.04% refers to who captured most of the winnings, not simply who won anything at all.

Ansari is co-sponsoring a bill called the BETS OFF Act alongside Sen. Chris Murphy of Connecticut and Reps. Greg Casar and Rashida Tlaib of Texas and Michigan, respectively. The bill would ban betting on events like war, terrorism, assassination, and government decisions.

Whatever the exact interpretation of the 0.04% figure, more recent data puts the problem in sharper focus.

The sharp drop, according to Sergeenkov, is tied to a flood of new and inexperienced users drawn in by the buzz around the November 2024 U.S. presidential election. “Less experienced users tend to trade less successfully,” he noted.

The 84.1% figure is also higher than what a 2025 study from researchers Felix Reichenbach and Martin Walther found.

Their paper put the losing share at around 70%. The difference, Sergeenkov explains, comes down to how the math is done.

His method accounts for wallet splits and merges, which earlier analyses left out. “When splits are left out, an address looks more profitable because one category of expenses is simply invisible,” he said.

The numbers behind the losses

A deeper look at the data shows just how rare meaningful earnings are on these platforms. Of 2.5 million wallets studied, only 2% had ever made more than $1,000 in total. Just 0.32% had cleared $10,000, and only 840 wallets, that is 0.033%, had earned more than $100,000.

The average trade on Polymarket is $89, and 80% of traders never place a bet larger than $500 on average.

The idea of replacing a regular paycheck through trading appears almost out of reach. The average monthly salary in the United States is roughly $5,000. Only 0.98% of traders ever hit that mark in a single month.

The number who managed it for 12 months straight: just 35 out of 2.5 million people.

The findings carry weight at a time when major financial institutions have moved in.

The Intercontinental Exchange, which owns the New York Stock Exchange, completed a $2 billion deal with Polymarket in March. Kalshi recently raised $1 billion, pushing its valuation to $22 billion.

The BETS OFF Act and a separate bill called the Death Bets Act, introduced by Rep. Mike Levin, are not widely expected to pass in the current Congress. Still, observers say the push for stronger protections for everyday users is not going away.

A Las Vegas online casino company has struck a deal with Crypto.com to offer prediction market contracts in the U.S., entering what could become a trillion-dollar industry.

High Roller Technologies (NYSE: ROLR) is the company behind the High Roller and Fruta casino brands. It has signed an agreement with Crypto.com’s derivatives arm, known as CDNA. U.S. customers will be able to trade event-based contracts across finance, sports, and entertainment.

It’s the company’s first move into prediction markets, a space that’s been attracting serious money. Analysts have floated projections of $1 trillion or more in annual U.S. trading volume if the market matures, with global figures potentially higher.

Crypto.com co-founder and CEO Kris Marszalek cited High Roller’s existing platform as the draw. “Together, we believe we can expand access to regulated event contracts in the United States through a differentiated and highly scalable offering,” he said. High Roller CEO Seth Young said the company has spent months preparing for the launch.

Partnership creates new revenue channels

The arrangement designates Crypto.com and its affiliates as prediction contract suppliers across High Roller’s U.S. distribution network. High Roller (NYSE: ROLR) plans to operate through the structure, which is expected to generate additional revenue streams for the company.

CDNA is already registered with the CFTC as both a designated contract market and a derivatives clearing organization. High Roller plans to register as a CFTC Introducing Broker and connect with Crypto.com’s CFTC-registered Futures Commission Merchant.

Rivals attracting billions in investment

The news comes during a frenzy of investment in the prediction market space. Rival platform Kalshi just hit a $22 billion valuation after raising roughly $1 billion, led by Coatue Management, double its December valuation, which drew backing from Andreessen Horowitz, Sequoia, Ark Invest, and Paradigm.

The company’s rise accelerated after winning a court fight with the CFTC in May 2025 that cleared it to offer election contracts, taking it from $2 billion to $22 billion in under a year.

Polymarket closed a $1.6 billion investment from Intercontinental Exchange, the NYSE’s parent company, fulfilling a commitment ICE first made in October 2025 when it valued Polymarket at $9 billion. ICE also plans to buy up to $40 million in Polymarket securities from existing holders.

The initial ICE commitment reached as high as $2 billion, with $1 billion deployed upfront. The additional $600 million brings ICE’s total obligation to completion.

High Roller (NYSE: ROLR) raised about $25 million in January through a direct share offering, selling roughly 1.9 million shares at $13.21 apiece. The placement, handled by ThinkEquity, closed on January 21. Proceeds are going toward marketing, expansion, product development, and operations.

On April 1, the NYSE American confirmed the company had resolved a prior stockholders’ equity deficiency, having demonstrated compliance for two consecutive quarters. The compliance indicator on its ticker was removed that morning. The company remains under standard listing oversight going forward.

High Roller’s platform hosts more than 6,000 games from over 90 providers.

If you want a calmer entry point into DeFi crypto without the usual hype, start with this free video.