President Donald Trump named Federal Housing Finance Agency Director Bill Pulte as Acting Director of National Intelligence on Tuesday. The pick drew immediate celebration from Bitcoin holders tracking his pro-crypto record.

The 38-year-old will keep his FHFA role and chairmanship of Fannie Mae and Freddie Mac. He will dual-hat the positions until a permanent DNI is nominated and confirmed.

Trump Picks Acting DNI

Pulte’s Pro-Crypto Record at FHFA

In June 2025, Pulte ordered Fannie Mae and Freddie Mac to recognize crypto in mortgage assessments. The directive removed any requirement that borrowers liquidate holdings first.

Bill is a great guy who recognizes that the bureaucracy of the intel community must respond to the elected leadership (rather than the other way around). He’ll do great! pic.twitter.com/nlK2tWXZjl

However, only assets held on U.S.-regulated exchanges qualify under the strict custody restrictions attached to the rule.

Federal disclosures list his personal holdings in Bitcoin (BTC), Solana (SOL), and miner MARA Holdings. Spousal crypto exposure reaches up to $2 million.

A Bitcoiner was just picked for DNI role,” cheered David Bailey.

Vice President JD Vance defended the pick in a separate post praising Pulte’s posture toward the intelligence community.

Bill is a great guy who recognizes that the bureaucracy of the intel community must respond to the elected leadership (rather than the other way around),” Vance added.

However, critics highlight Pulte’s lack of intelligence or national security background.

MAJOR BREAKING: Trump just put Bill Pulte, who has NO background in national security, and weaponized government to go after Trump Critics Letitia James, Adam Schiff, and Lisa Cook, in as the Acting Director of National Intelligence.

They note federal statute favors such experience, especially as the crypto market structure debate heats up in Congress. The acting role itself does not require Senate confirmation.

“He appears to have been selected precisely because the White House believes he will provide the narrative it wants, not the intelligence we need,” stated Senator Mark Warner.

Bitcoin is still trading above $60,000, but there are questions as to whether that area has already become the macro bottom for this correction or whether another crash could still drag the price back into that zone. Technical analysis using Bitcoin’s weekly RSI, prior cycle support, and the 21-week and 50-week EMA trend presents the bullish side of that trend, but bears can still argue that confirmation has not arrived until Bitcoin breaks above the weekly EMA structure.

Bitcoin Might Have Bottomed Already

The strongest argument that Bitcoin may have already bottomed is from the weekly RSI indicator. According to the thesis shared by Cryptoposeidon on X, Bitcoin’s weekly RSI has fallen below 30 only four times in history. The first three came around the January 2015, December 2018, and June 2022 lows, all of which later became macro bottom zones.

Back in January 2015, Bitcoin’s RSI fell to about 28 when the price fell to $200. A similar pattern played out in December 2018, when RSI dipped below 30 around $3,500, followed by about three months of sideways accumulation before Bitcoin broke higher. The third instance was June 2022, in the depths of the bear market that followed the Luna collapse.

The fourth reading came in early February 2026, shortly after Bitcoin’s crash into a bottom around $63,000, and this supports the proposal that Bitcoin may have already gone through its major capitulation phase.

The weekly candlestick timeframe chart below also shows the RSI recovering from a low band similar to the previous bear-market bottom zones, with the projected path suggesting that momentum could spend more time rebuilding before a stronger move returns in 2027.

What Confirmation And Return To $100,000 Actually Looks Like

The last two bear markets both took 364 days to move from peak to trough. The current correction is now 236 days old, which leaves a 128-day window for Bitcoin to make another low if it follows the same timing pattern.

However, looking at November 2022, Bitcoin broke below the prior cycle’s $19,900 peak and collapsed to $15,500, spending a brief period under $16,000. That breakdown was forced by the FTX implosion, a black swan event that liquidated billions in assets and obliterated confidence simultaneously. Without a comparable catalytic shock, current crypto market dynamics lack the mechanism to sustain prices below $60,000 within the remaining 128-day window for a bottom.

Bitcoin’s long-term support band is between $58,000 and $66,000, and the February 2026 low is inside that range. Bitcoin can still wick to $55,000 or even $50,000 in a liquidation event, but spending a long period below $60,000 would require a very strong bearish catalyst.

On the other hand, a reclaim and monthly close above the weekly EMA and $80,000 in June 2026 would change the conversation from “Is $60,000 the bottom?” to “How fast can Bitcoin rebuild toward $100,000?” At the time of writing, Bitcoin is trading at $72,860, down by 1.2% in the past 24 hours.

Bitcoin is approaching a pivotal moment, with several key support and resistance levels set to determine its next major move. While bulls are fighting to maintain critical price zones and preserve the broader recovery structure, bears continue to pressure the market from above.

Bitcoin Struggles Below $78,080 As Bears Retain Control

Analyst Kamile Uray notes that Bitcoin’s recent recovery attempt was feeble, with the price remaining trapped below the critical $78,080 threshold. Until the market secures a decisive 4-hour close above this level, the structural outlook remains vulnerable, and the downward trend is likely to persist.

To the downside, attention shifts toward the Fibonacci support zone spanning $71,000 to $68,000. This region historically attracts buyers and could serve as a vital foundation for a structural rebound.

Conversely, should the market turn bullish, traders must watch the $82,885 level as the primary launchpad. A successful close above this resistance opens the door to targets at $98,000, $107,000, and $109,000 that would require significant conviction to overcome.

Examining the longer-term landscape, $126,199 represents a pivotal ceiling where corrective pressure may reemerge. Ultimately, $60,000 stands as the final defense line for the asset’s structural health.

$72,500 Monthly Low Becomes The Key Level To Watch

As the new month kicks off, Lennaert Snyder identifies the $72,500 level as the critical pivot point for Bitcoin. Serving as both the Previous Monthly Low (PML) and the Previous Weekly Low (PWL), this zone dictates the immediate market bias. A decisive breakdown here would establish a strong bearish confluence, making a recovery to the previous monthly high (PMH) of $82,500 highly improbable.

Snyder’s ideal short strategy hinges on the loss of this $72,500 threshold. If the price fails to maintain this support, he anticipates a relief retest of the range, using the $78,000 Previous Weekly High (PWH) as the ceiling. This setup would provide a high-probability entry for shorts to drive the asset down to test new lows.

However, if the market successfully defends the $72,500 PML/PWL and generates a clean bullish reaction, the focus shifts to the long side. In this scenario, Snyder intends to play the continuation of the trend, provided the market maintains its structure. He emphasizes monitoring the identified imbalances, which serve as key Points of Interest (POIs) that will help determine the validity of each move.

While there is room for counter-trend opportunities, they require strict discipline. Snyder notes that while a bounce after a breach of the $72,500 support is technically possible, it remains a high-risk play. Consequently, he views such trades strictly as short-term scalps rather than foundational positions, preferring to align with the dominant trend once the market shows its hand.

Less than four years after the collapse of FTX triggered calls for a sweeping crackdown, the crypto industry has emerged as one of the fastest-growing forces in American politics, spending millions across both parties, reshaping key elections, and transforming itself from a regulatory target into a powerful new political machine.

In 2022, Washington’s dominant question about the crypto industry had little to do with the fine print of securities law. After the collapse of FTX triggered a wave of congressional fury and handed Gary Gensler’s SEC a permission slip to pursue enforcement actions at scale, lawmakers on both sides of the political aisle were openly debating whether the sector deserved regulated status at all.

Cautious congressional allies began distancing themselves, and the media cycle was doing the industry no favors. For a little while, it looked like the whole market was headed for supervised wind-down.

But by the end of the 2024 election cycle, Bitcoin’s political environment had been almost entirely remade. Crypto companies collectively spent around $139 million shaping that year’s elections through a network of super PACs, and they’ve since assembled a war chest exceeding $220 million for the 2026 midterms.

The sector’s transformation from a regulatory punching bag to a lobbying operation capable of rivaling oil companies and banks in raw political spend shows what an industry does when it concludes (correctly) that its long-term survival depends on controlling the conditions under which it gets regulated.

How the crypto industry decided to fight back

Between FTX’s collapse and the 2024 elections, the defining pressure on the industry came from the SEC’s aggressive position on digital assets. The agency issued 46 crypto-related enforcement actions in 2023 alone, pursued landmark cases against Coinbase, Binance, and Ripple, and treated most digital assets as unregistered securities subject to the same oversight as stocks and bonds.

For companies like Coinbase, which found itself simultaneously suing the SEC and being sued in return, the agency’s intent was clear: it planned to define the industry’s regulatory future on its own terms, leaving little room for any input from the industry. The more enforcement pressure accumulated, the more clearly the industry saw that regulatory outcomes are fundamentally political, and that winning them requires political tools.

Andreessen Horowitz’s early decision to build an aggressive lobbying operation designed specifically to exclude crypto from SEC jurisdiction served as a template for how the industry could fight back at the structural level. The realization spread through 2023: the companies that’d survive the next decade would be the ones that saw Washington as a competitive arena, and that winning there required the same disciplined capital deployment as winning in markets.

Fairshake, the super PAC backed by Coinbase, Andreessen Horowitz, Ripple, and a consortium of other crypto companies, came up with concrete solutions. Fairshake itself operated across party lines, while two affiliates (Defend American Jobs for Republicans, Protect Progress for Democrats) routed money to each party’s candidates in parallel.

It was a strategic calculation built on the understanding that an industry capable of influencing either party’s electoral outcomes would reach a far more durable position than one committed to a single political faction.

Results from 2024 showed that kind of approach was successful. Fairshake and its affiliates spent roughly $139 million across 58 House and Senate races. About 85% of the candidates the network supported won their elections, including all six in New York, where the PAC spent $5.3 million exclusively backing Democrats.

One in ten members of the incoming Congress had received meaningful support from crypto industry ad spending, and the majority of those ads never mentioned crypto at all, targeting incumbents on unrelated character grounds instead. What political power actually buys

It took almost no time to see meaningful policy changes. The SEC reversed course on a sweeping scale: it dismissed its civil action against Coinbase in early 2025, dropped its lawsuit against Binance shortly after, and closed its investigation into Robinhood’s crypto business with no charges filed. Ripple, having spent years and tens of millions in legal fees fighting XRP’s securities classification, settled for $50 million and had its remaining $75 million in escrow returned.

In May, Fairshake’s affiliate Protect Progress spent $5 million supporting Democratic challenger Christian Menefee in Texas’ 18th Congressional District runoff, and another $2.8 million opposing incumbent Representative Al Green, who voted against both the GENIUS Act and the Clarity Act.

Green cast the wrong votes, the PAC identified the seat as removable, and moved nearly $8 million into the district to make the point. Across all Texas races today, crypto-backed PACs deployed money into multiple congressional and Senate contests, backing both Republican and Democratic candidates.

Separately, the Tether-backed Fellowship PAC, led by former White House crypto adviser Bo Hines, reported spending $1.75 million backing Texas Attorney General Ken Paxton in his Senate runoff against incumbent John Cornyn. Paxton won in what the Texas Tribune called a watershed moment that ended over three decades of Cornyn’s electoral dominance. The industry backed the winning side, across party lines, in one of the most-watched primary elections in the country.

However, there has been quite a bit of controversy surrounding the newfound success of crypto lobbying groups. Lawmakers, including Representatives Maxine Waters and Brad Sherman, documented at least 12 cryptocurrency cases the SEC dismissed or closed since early 2024, pointing to what they described as a “troubling correlation” between those closures and the industry’s political spending patterns.

Former SEC enforcement attorneys noted publicly that the scale of case dismissals was unusual given the reportedly strong evidence the agency had assembled in several of those actions.

The industry’s counter-argument (that the crackdown was overreaching and politically motivated from the start) carries genuine weight, but the question of who’s now writing the rules and for whose benefit is a legitimate one that the sector’s advocates haven’t fully put to rest.

The most morally and politically honest answer is that crypto’s regulatory environment shifted because crypto’s political leverage shifted first, and Texas elections showed how that leverage is now being applied.

Crypto PAC spending in Texas has already exceeded $2.5 million on congressional candidates alone this year, up from $1 million across the entire 2024 cycle, and that’s before the general election spending begins later this year.

That puts the industry on a path that resembles the early chapters of Big Tech’s lobbying ascent or Wall Street’s post-crisis political infrastructure build, with a slight distinction: it’s moving faster than either of those precedents did.

The industry that once sold itself as an alternative to legacy financial power is now running the same playbook that legacy power has always relied on: grading legislators on specific votes, deploying capital to punish defection, and building the kind of durable congressional relationships that outlast any single administration.

Bitcoin’s (BTC) 200-week moving average has climbed past $61,000. Blockstream CEO Adam Back flagged the threshold on May 30, weeks after noting the same indicator crossed $60,000 in early May.

The indicator has risen roughly $1,000 in under a month, a pace that reflects steady absorption of supply by long-term holders at current price levels.

A Rising Long-Term Floor

The 200-week moving average smooths nearly four years of weekly Bitcoin closes. It has served as a support floor at each of Bitcoin’s prior cycle bottoms, and crossings of major thresholds draw sustained attention from long-term holders watching the structural trend.

At the time of writing, BTC was trading well above this level. It maintained a significant gap between the spot price and the 200-week moving average first, highlighted by Back in early May.

The 2022 bear market remains the only period where BTC closed a weekly candle below the line before quickly reclaiming it. The long-term bullish structure has trended higher in every cycle since.

Munger’s Argument, Applied to Bitcoin

In a follow-up post, Back cited a remark attributed to the late Charlie Munger, a popular American billionaire investor.

Apparently Charlie Munger would agree generally “If all you ever did was buy high-quality stocks at the 200-week moving average, you would beat the S&P 500 by a large margin over time. The problem is, few human beings have that kind of discipline”

Back attributed the comment to Munger, then added a caveat. He noted that Munger and Buffett “never got bitcoin,” drawing a parallel to their early dismissal of the internet. He attributed both misses to their preference for physical businesses.

The implicit argument is that Bitcoin holders willing to apply Munger-style patience at moving-average lows could see outsized returns over full cycles.

Bitcoin 200 Week Moving Average Heatmap. Source: Coinglass

The indicator rises gradually across cycles, meaning entries near it have historically represented a structural discount to Bitcoin’s long-term trend.

Whether the 200-week moving average sustains its current climb depends on whether institutional and retail demand continue to outpace selling. On-chain data has supported the case that structural buying remains intact for now.

The US Treasury market is the foundation of the global financial system. It determines mortgage rates, government borrowing costs, corporate lending, and the price of money across the world. For decades, investors treated it as the safest and most stable market on Earth.

But after years of exploding government debt, repeated liquidity scares, and increasingly aggressive Federal Reserve interventions, Wall Street is starting to confront an uncomfortable possibility: the Treasury market may have become too large, too leveraged, and too systemically important to function without constant support.

Now, with debt issuance accelerating and bond yields elevated, a different fear has taken hold inside financial markets: whether the world’s most important market can still absorb America’s borrowing needs without something breaking.

Foreign central banks have reduced their share of Treasury holdings, and the Federal Reserve, after expanding its balance sheet to $8.5 trillion at the 2022 peak through successive rounds of quantitative easing, has spent the years since trying to shrink it.

That left private markets, including hedge funds, asset managers, individual investors, and increasingly stablecoin issuers, to absorb what sovereign and central bank demand once handled.

When the debt market started needing support

The warning signs had been accumulating for years. The September 2019 repo market freeze was the first real signal that something changed beneath the surface: short-term funding markets seized without warning, and the Fed was forced to inject emergency liquidity within days.

The second and far more alarming episode came in March 2020, when the onset of COVID-19 triggered a mass liquidation of Treasury securities, with institutional investors selling “the world’s safest asset” alongside everything else as they scrambled for cash at any price.

What Brookings Institution researchers later described as the evaporation of bond market liquidity forced the Fed into massive, unprecedented emergency purchases to restore market functioning, interventions that worked but also established a precedent that’s proven difficult to walk back.

Underneath those acute stress events is a structural feature of modern Treasury trading that regulators have grown increasingly worried about. Hedge funds have become central players in what’s known as the cash-futures basis trade, a leveraged arbitrage strategy that exploits tiny price differences between Treasury securities and Treasury futures contracts by holding bond positions funded almost entirely through overnight repo borrowing.

The April 2025 tariff announcement tested that assessment almost immediately: liquidity deteriorated sharply within days, prompting speculation about Fed intervention before conditions eventually stabilized.

The repo facilities, standing liquidity programs, and targeted purchases used to stabilize those episodes were designed as emergency instruments, but they’ve since become recurring features of the system.

What a strained Treasury market means for everyone

Mortgage rates are where this kind of structural pressure becomes tangible for the average person. The 30-year fixed mortgage rate tracks the 10-year Treasury yield closely, which is why the 10-year’s refusal to fall below 4.3% through much of 2025 and into 2026 kept home loan rates pinned well above 6% even after the Fed cut its benchmark rate three consecutive times.

The central bank’s short-term policy rate and the long bond have now essentially decoupled, showing the bond market’s growing preoccupation with debt supply over short-term monetary signals from the Fed.

At the government level, the numbers are self-reinforcing in ways the Congressional Budget Office has put in specific dollar terms: interest payments are projected to climb from $1 trillion annually in 2026 toward $2.1 trillion by 2036, with an alternative scenario where persistently elevated yields push that figure toward $2.2 trillion.

Every dollar spent servicing debt is a dollar unavailable for anything else, and the debt is rolling over at higher rates every year. A run of weak Treasury auctions in early 2026 brought that into sharp focus: in a two-year note sale in late March, primary dealers absorbed roughly twice their normal share, a clear sign that the marginal buyer base has thinned considerably.

The connection to Treasury yields has become one of Bitcoin’s defining macro features of 2026. CryptoSlate has documented how Bitcoin’s near-term price ceiling has repeatedly been set by yield movements.

The 10-year crossing above 4.5% and the 30-year climbing toward 5.1%, its highest level since 2007, pushed Bitcoin back below $80,000 last week even after Congress advanced one of the industry’s most-watched regulatory milestones.

The Fed rate cuts that crypto markets treated as a reliable macro tailwind have been priced out of the near-term picture entirely, with Barclays moving its first expected cut to March 2027 and futures markets now assigning meaningful odds to a hike before the end of the year.

There’s a specifically crypto-native dimension to how the buyer composition has shifted. As foreign central banks and the Fed have pulled back from Treasury markets, Tether has filled part of the gap, with its Treasury exposure reaching $141 billion in 2025 and making it one of the largest non-sovereign holders of US government debt.

That demand supports the short end of the market, and it means that crypto-native capital is now embedded in America’s debt infrastructure in a way that would have seemed implausible a decade ago. It also means that any stress in the stablecoin market is now capable of rippling directly through Treasuries. For years, inflation prints were the primary input that moved markets.

Today, Treasury auction results, refinancing calendars, and the buyers absorbing new supply have taken over the weekly agenda. The concern growing across the financial system is now deeper than the scale of America’s borrowing.

It reaches toward whether the combination of central bank backstops, leveraged private capital, and an increasingly disparate group of marginal buyers is stable enough to keep absorbing it.

A crypto analyst has identified multiple price levels he believes could be dream entry points ahead of Bitcoin’s (BTC) long-term price rally. The analyst has shared several ambitious price targets for BTC, expecting the cryptocurrency to skyrocket to $300,000 and even $500,000 in the coming years.

Analyst Identifies Bitcoin Buy Zones Before $300,000 Target

In a recent X post, market expert Crypto Patel stated that while many investors are panicking after Bitcoin’s recent decline below $74,000, he is using the opportunity to quietly build his position. The analyst said he is preparing to buy more BTC, suggesting that additional dip buying opportunities may still lie ahead as he targets a long-term rally above $300,000.

Crypto Patel has identified three ideal Bitcoin accumulation zones ahead of this projected move. The zones are based on Fibonacci retracement levels highlighted on his accompanying chart. The analyst noted that the first entry point around $60,000 has already been filled, leaving just two ideal points remaining. He noted that this first zone aligns with the 0.382 retracement level and a bullish order block.

Crypto Patel also identified a second accumulation zone near $45,000, which aligns with the 0.5 Fibonacci retracement level. He noted that he is patiently waiting for a move into this area before adding more BTC to his position. Meanwhile, the third and most aggressive zone sits around $35,000, close to the 0.618 retracement. Crypto Patel described this area as a “dream entry” point, suggesting that it would offer the most attractive buying opportunity of the three targets provided if Bitcoin were to decline that far.

Notably, the foundation of Crypto Patel’s bullish analysis and accumulation zone rests on an Inverse Head & Shoulders pattern that formed on the weekly chart between 2022 and early 2024. According to the analyst’s chart, the pattern took shape as Bitcoin suffered a 77.6% decline from its previous peak in 2024, with that market bottom forming the head of the H&S pattern.

When BTC confirmed a breakout from that structure in early 2024, it signaled a major market shift, with buyers gaining most control. After this, the cryptocurrency recorded a major price rally that carried it to its current all-time high above $126,000, set in October 2025.

Once that ATH was hit, Bitcoin eventually met significant resistance between $84,000 and $100,000. A subsequent rejection in that area brought Bitcoin back down into the current retracement territory around $74,000, where Crypto Patel’s accumulation plan is now playing out.

Multi-Year BTC Price Targets Point To $500,000 Peak

Crypto Patel’s accumulation strategy for Bitcoin also feeds into a longer price roadmap based on Fibonacci extension levels stretching into 2027 and 2028. The analyst has set an initial long-term target of $200,000, representing a more than 170% increase from current levels above $73,000.

For his second target, the analyst expects Bitcoin to rally to $300,000. The price curve shown on the analyst’s chart suggests that this move could unfold by late 2027 if market conditions remain favorable. Beyond that, Crypto Patel projects an ultimate peak near $500,000. A rise to this bold target would mark a staggering gain of over 580% from current prices.

Featured image from Unsplash, chart from TradingView

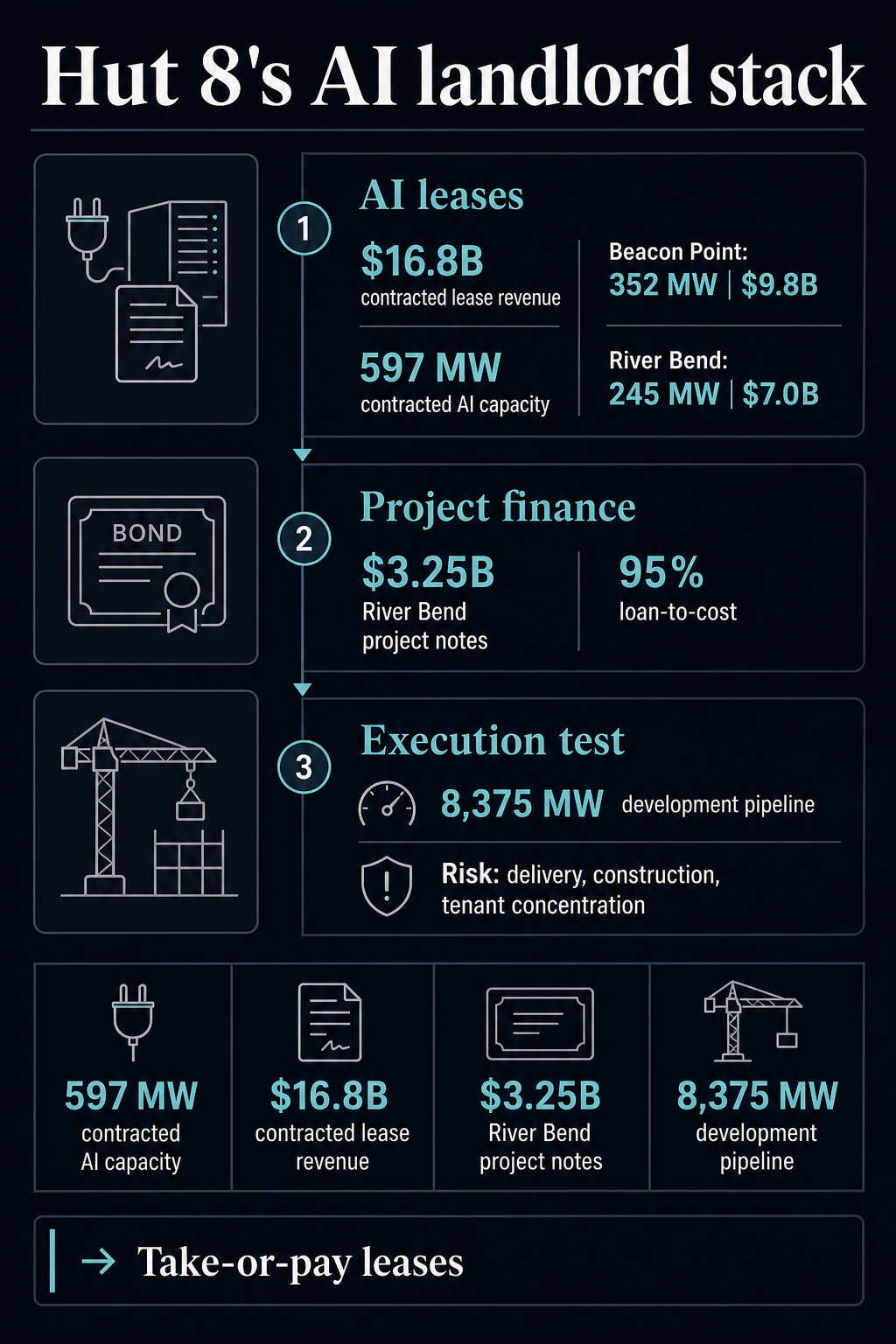

Hut 8 is pushing even further into AI infrastructure than most other Bitcoin miners are. Its latest disclosures show a company using power access, data center leases, project debt, and BTC-backed liquidity to build the financing stack for that move.

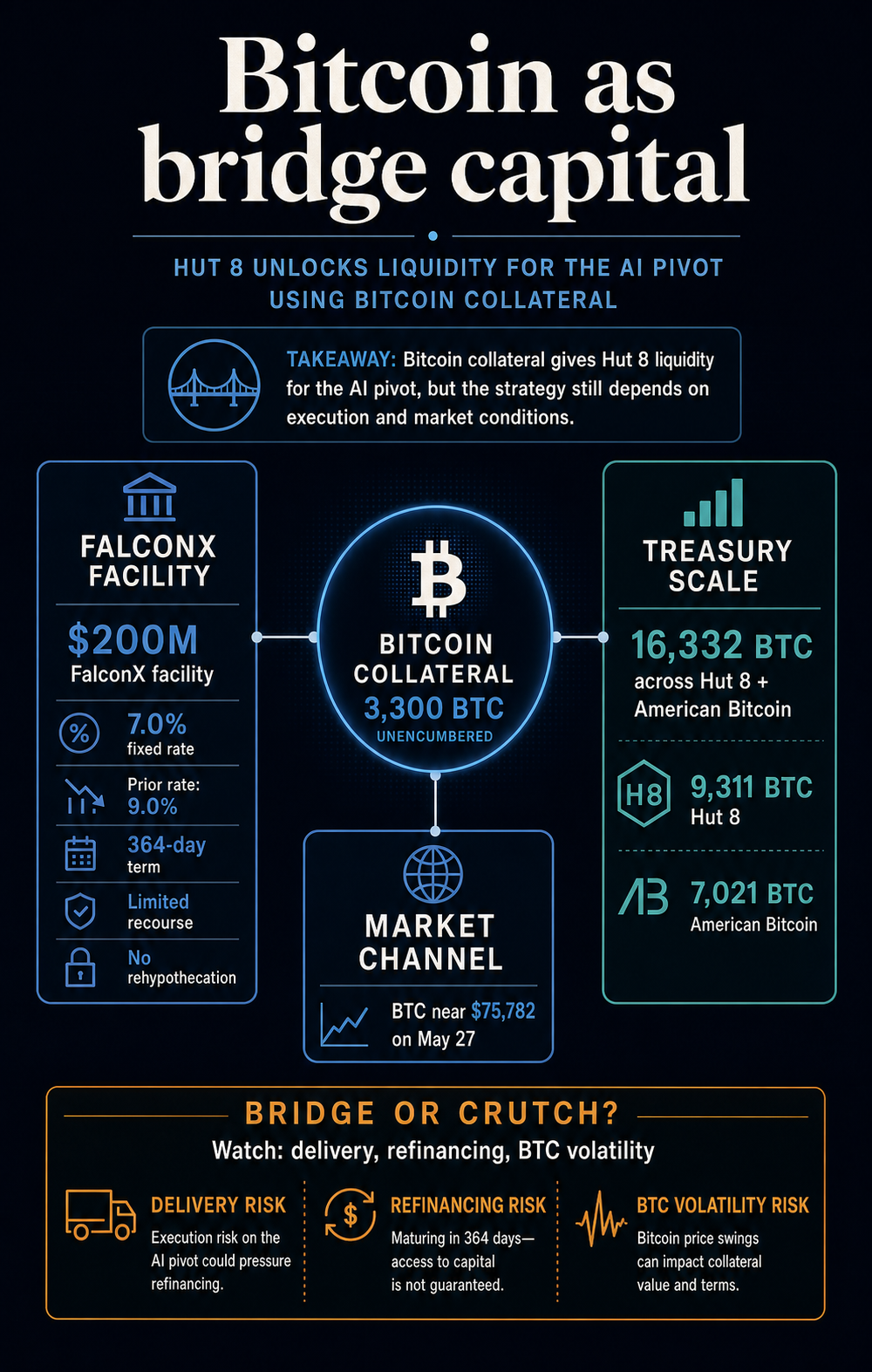

The company’s latest disclosures put numbers around that transition. Hut 8 reported $16.8 billion in triple-net, take-or-pay contracted lease revenue across two hyperscale AI campuses, then separately refinanced a $200 million Bitcoin-backed credit facility with FalconX.

The new facility cut the fixed rate to 7.0% from 9.0% and unencumbered roughly 3,300 BTC from the prior collateral package.

Taken together, the disclosures show a miner identity changing into something closer to an infrastructure landlord. Hut 8 is turning megawatts, lease commitments, project debt, and Bitcoin holdings into the machinery for a business that depends less on mining alone.

The result is a case study with more substance than a generic AI pivot. Hut 8 is showing a funded path into data center infrastructure, though the model still needs operating proof. The test is whether contracted AI cash flows arrive on schedule and become durable enough that Bitcoin collateral becomes a bridge instead of a recurring source of balance-sheet dependence.

The lease base turns power into finance

The strongest number in Hut 8’s first-quarter disclosure sits outside the Q1 income statement: $16.8 billion of contracted lease revenue across River Bend and Beacon Point, covering 597 MW of AI data center capacity.

Hut 8 generated $71 million of revenue in the first quarter, including $66 million from Compute, and posted a $253 million net loss that included $295 million of primarily unrealized digital-asset losses.

The $16.8 billion figure represents long-term contracted lease value that Hut 8 is presenting as the foundation for a different kind of business.

The pieces are specific. Hut 8’s Beacon Point lease added 352 MW of IT capacity and $9.8 billion of base-term value. Its earlier River Bend lease added 245 MW and $7 billion of base-term value, with Google providing a financial backstop for the base lease term.

Hut 8 is commercializing scarce power and data center capacity under long-term lease structures. The appeal comes from contracts and power access rather than a token, a cloud slogan, or a vague compute promise.

Triple-net and take-or-pay terms are designed to make those cash flows more financeable because the tenant obligation is less tied to day-to-day mining economics.

Hut 8’s disclosures line up across four moving parts:

Model component

Hut 8 evidence

Reader impact

Risk still live

Power and sites

597 MW of contracted AI data center capacity across two campuses

Turns miner infrastructure into leaseable digital infrastructure

Delivery, interconnection, construction, and tenant concentration

Contracted demand

$16.8 billion in base-term contracted lease revenue

Creates a financing story beyond hashprice exposure

Lease value depends on execution over long timelines

Project finance

$3.25 billion River Bend notes, non-recourse to Hut 8

Reduces the need to fund all growth from equity or BTC sales

Large projects still carry cost, schedule, and market risks

Bitcoin balance sheet

$200 million FalconX BTC-backed facility and 3,300 BTC unencumbered

Gives liquidity without immediately selling coins

Collateral value still moves with BTC

Hut 8’s AI transition has more to it than most, but each component still carries a different kind of risk.

The leases reduce some revenue uncertainty. The bond financing reduces some parent-level funding pressure. The Bitcoin facility improves liquidity. Still, all three leave Hut 8 with the task of building, delivering, and operating infrastructure for customers whose requirements differ from Bitcoin mining.

Bitcoin becomes bridge capital

The FalconX refinancing is the clearest sign that Bitcoin is becoming part of the financing machinery rather than only the asset being mined.

The full Hut 8 release distributed through Nasdaq described the facility as a 364-day Bitcoin-backed loan with limited recourse to pledged BTC, a no-rehypothecation covenant, fixed loan-to-value thresholds, and no loan-to-value ratchet triggered by declines in Bitcoin’s price.

Those terms blunt part of the obvious criticism. The deal improves the terms of a miner’s coin-backed borrowing instead of worsening them to chase a new market.

Hut 8 lowered its fixed cost of debt by 200 basis points and increased Bitcoin held outside collateral covenants. The release valued the newly unencumbered coins at roughly $260 million as of May 1, 2026, giving Hut 8 more balance-sheet room without selling the asset.

That makes the facility a better tool, but not a risk-free one.

Hut 8’s own balance sheet shows why the distinction is important. Its 10-Q said the company held about 16,332 BTC as of March 31, 2026, including about 9,311 BTC held by Hut 8 and about 7,021 BTC held by American Bitcoin.

The aggregate fair value was about $1.11 billion, based on approximately $68,222 per BTC. The same filing tied the first-quarter digital-asset loss to Bitcoin’s decline during the period.

Today, Bitcoin trades near $75,782 on CryptoSlate’s price page, down 2.1% over 24 hours and roughly 40% below its October 2025 all-time high. The market-price channel is the relevant risk.

Bitcoin can provide liquidity without a sale, but the borrowing value, covenant comfort, and refinancing backdrop still depend on the asset’s market behavior.

That is why the AI landlord strategy cannot be separated from the Bitcoin treasury strategy. If AI leases produce reliable cash flows, BTC collateral can be transitional capital. If delivery slips, financing markets tighten, or Bitcoin weakens at the wrong time, the same collateral can keep the pivot tied to the volatility it was meant to escape.

The miner label is becoming less useful

Earlier coverage of miners’ AI pivot showed the broader identity split facing the sector. Miners are moving toward AI and high-performance computing because power access, cooling infrastructure, land, interconnection work, and industrial operations can be worth more under contracted dollar revenue than under compressed mining margins.

Hut 8 fits that broader sector shift. Public miners built businesses around converting power into BTC, and AI data center demand is now giving some of them a second possible use for the same physical footprint.

The difference is that AI customers do not buy the same thing the Bitcoin network buys. Mining can tolerate interruption when economics or grid conditions change. AI tenants want uptime, delivery certainty, dense power, cooling, network architecture, and creditworthy execution.

A miner with megawatts still has to become a hyperscale landlord. It has to turn a power position into infrastructure that lenders and tenants will treat as dependable.

Hut 8’s disclosures show both sides of that transition. The company describes itself as an energy infrastructure platform integrating power, digital infrastructure, and compute. It also still reports digital-asset losses, BTC holdings, and exposure to mining economics.

Some Compute revenue and BTC holdings are held by American Bitcoin, a consolidated subsidiary, making Hut 8’s strategy less straightforward than a clean exit from mining.

That complexity is part of the shift. The market is watching whether miners can stop being pure BTC proxies without losing the balance-sheet optionality that made their treasuries valuable in the first place.

The strongest argument in Hut 8’s favor is that the AI pivot uses more than Bitcoin-backed debt. The company said it closed $3.25 billion of fully amortizing 16.5-year investment-grade senior secured notes to finance River Bend.

Hut 8 described the financing as non-dilutive and non-recourse to Hut 8, with loan-to-cost increasing to about 95%.

That weakens the crutch argument. If project-level debt funds the campus and long-term leases support the debt, then Bitcoin collateral is one part of the structure rather than the whole. It is a liquidity tool alongside project finance and contracted revenue.

The caution is that the financial structure still has to become operationally sound. River Bend is still advancing toward delivery, Beacon Point still has to be built out, and the company still has to convert an 8,375 MW development pipeline into real contracted capacity.

Hut 8 also warned investors about risks tied to data center construction, financing, power expansion, permitting, supply chains, technical challenges, and market conditions.

Hut 8 is showing that miners can finance a route into AI infrastructure when they have scarce power, credible tenants, project-finance access, and a Bitcoin balance sheet lenders will underwrite. It has yet to show that the route is self-sustaining.

The next test is whether AI infrastructure cash flows become strong enough to push Bitcoin collateral into the background. If they do, Hut 8’s BTC-backed financing will look like bridge capital for a miner that successfully monetized its power footprint.

If they fail to do so, the pivot will remain tethered to the same balance-sheet asset that made the strategy possible in the first place.

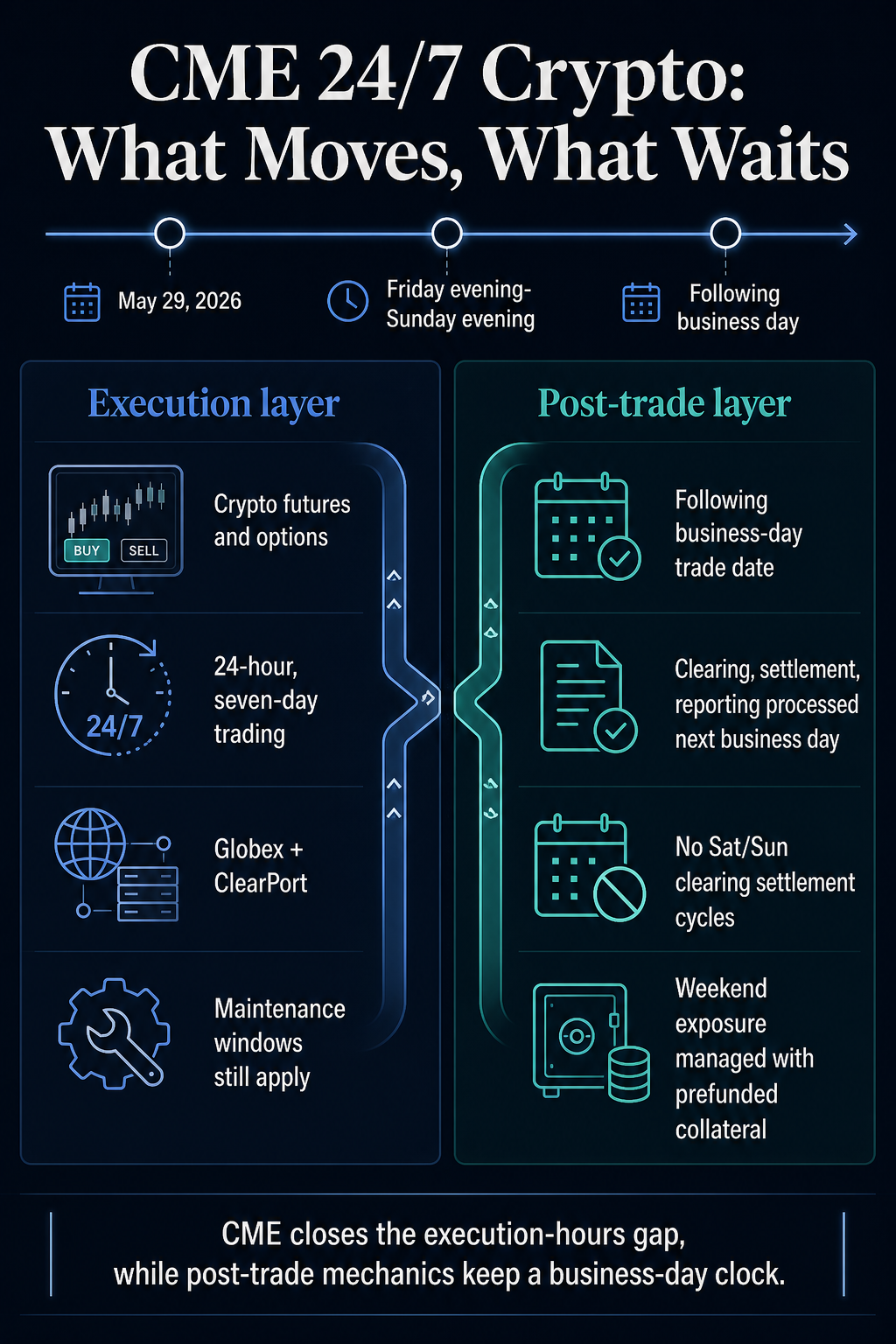

CME Group says its regulated crypto futures and options will move to 24-hour, seven-day trading on May 29, pending regulatory review, cutting into one of Bitcoin‘s familiar institutional market tells.

The weekday venue that helped create weekend CME-gap talk is preparing to keep matching trades while crypto prices keep moving.

CME is extending the moment traders can execute, while other parts of the regulated futures stack still keep a business-day clock.

Weekend and holiday trades from Friday evening through Sunday evening will still carry the following business day’s trade date, and CME says clearing, settlement and regulatory reporting tied to that activity will be processed on that following business day.

For participating institutional users, the execution gap gets smaller. The harder question shifts to liquidity quality, clearing behavior and Monday post-trade processing.

CME announced that its regulated cryptocurrency futures and options will become available for trading 24 hours a day, seven days a week beginning May 29, pending regulatory review.

The move applies to the exchange’s crypto futures and options complex and is being implemented through CME Globex and ClearPort, subject to maintenance windows.

The commercial case is clear. CME said client demand for digital-asset risk management reached a record level, with $3 trillion in notional volume across its crypto futures and options in 2025.

It also reported 407,200 year-to-date average daily contracts in 2026, up 46% from the prior year.

Those figures show why the weekend access problem has moved beyond a meme. Bitcoin traded around $75,782 in CryptoSlate’s May 27 snapshot, with a market capitalization near $1.52 trillion and 24-hour volume near $35.17 billion.

In a market of that size, a regulated derivatives venue that closes through the weekend can leave institutional desks managing price risk with a time-zone mismatch.

For traders using futures to hedge spot exposure, manage basis, or offset ETF-linked flows, the practical question is whether the regulated instruments they are allowed or required to use can respond when prices move outside the old CME week.

CME’s move gives qualified participants a regulated execution channel during periods that previously sat outside that trading window.

That access can change how a weekend shock is absorbed. Instead of compressing every move into a Sunday evening or Monday reopening, participating desks can hedge, roll, quote or adjust exposure while the broader crypto market is already trading.

The improvement is meaningful for basis trades, ETF-linked exposure, liquidation risk and headline-driven volatility, even as the rest of the regulated workflow remains more constrained.

For CME, the scale also shifts the launch from product housekeeping into market-structure work: a large derivatives franchise is adapting its access model to an asset class that keeps pricing risk through weekends.

The Post-Trade Clock Still Runs On Business Days

CME’s clearing and global operations guidelines spell out the limit of the change. The document says there will still be five business days, Monday through Friday, and that Saturday and Sunday clearing settlement cycles are outside the new setup.

The distinction is operationally important: execution becomes continuous, while the official machinery that turns trades into cleared obligations still leans on the next business day.

Layer

Weekend change

Business-day mechanic

Trading access

Crypto futures and options can trade through weekends and holidays, subject to maintenance windows.

Some clients may remain on five-day access instead of enabling seven-day trading.

Trade date

Trades can be executed from Friday evening through Sunday evening.

Those trades carry the following business day’s trade date.

Clearing and settlement

Weekend trades are accepted into the regulated workflow.

Settlement-cycle processing waits for the following business day.

Regulatory reporting

Weekend activity enters the reporting chain.

CME says reporting tied to weekend and holiday activity is processed on the following business day.

That design reflects the unresolved operating problem for regulated crypto markets. Crypto prices can move continuously, while futures markets depend on clearing members, collateral, risk controls, settlement cycles, reporting records and operational staffing built around business-day discipline.

CME’s guidelines show how the exchange is trying to bridge the mismatch. Clearing members that participate in supplemental trading hours must be approved by CME Clearing.

They must have risk policies and procedures that cover the extra hours, including account monitoring, credit controls, position limits, intraday and overnight monitoring, and defined liquidity sources.

During certain weekend hours, CME Clearing will monitor exposure against posted performance bond and available liquidity. Clearing members are required to submit weekly liquidity templates and deposit collateral for anticipated weekend clearing activity by Friday afternoon into separate weekend settlement accounts.

Those mechanics are the back-office version of 24/7 trading: prefunded risk capacity and monitoring until the business-day cycle catches up.

Weekend Liquidity Has To Prove Itself

The old CME gap became shorthand because Bitcoin and other crypto assets kept trading while CME’s institutional venue was closed. If spot prices moved sharply on Saturday, CME futures reopened later at a different level, creating a visible gap on the chart.

That chart pattern was only one part of the issue. The deeper problem was that regulated access stopped during precisely the period when crypto-native venues, offshore platforms, ETFs, market makers and leveraged traders could still be forced to react.

CME’s BTIC materials show how weekend access reaches the basis-trading and ETF workflows around crypto futures, not just directional bets.

In plain terms, a basis trade at index close lets participants trade crypto futures basis against CME CF reference rates, including reference-rate closes in London, New York and APAC. CME also cites ETF creation and redemption NAV risk as a use case.

That places CME’s derivatives complex close to the plumbing of institutional exposure. A desk managing basis against a reference rate, hedging ETF-linked exposure, or carrying futures against spot needs instruments, margin processes and liquidity when prices move.

Access alone still leaves market quality to prove itself. If weekend books are thin, spreads widen, or clearing constraints bite during stress, the market may feel more available without feeling fully continuous.

CME appears aware of that risk. Separate CFTC filings show weekend market-maker programs for cryptocurrency futures and options.

The options program says participants must quote continuous two-sided markets in covered products at maximum bid-ask spreads and minimum quote sizes during a required share of time in market.

Those filings support a launch-liquidity program rather than evidence of deep weekend markets. The first live measure will be practical: which clearing members enable seven-day access, how much volume trades outside old hours, how weekend bid-ask spreads compare with weekdays, whether options quotes remain reliable, and whether exposure alerts or prefunding requirements shape behavior during volatile periods.

There are two plausible paths. In the stronger version, CME’s weekend access becomes a genuine pressure valve.

Institutional traders can hedge, roll, quote and adjust exposure while crypto-native markets are already moving, and Monday becomes more of an administrative processing point than a delayed risk event.

In the weaker version, the venue is technically open while liquidity remains uneven, with many users still treating Monday as the real moment when weekend activity becomes visible in clearing, settlement and reporting.

The launch would still be important; it would show that the weekend gap has migrated from price charts into market depth and operations.

CME’s 24/7 launch gives institutional traders a way to use familiar futures and options products while Bitcoin and the broader crypto market move through weekends and holidays.

It also exposes the limits of the shift. Regulated crypto can trade more like crypto, while it still clears and reports through machinery built for business days.

For the weekend gap, the split is now clearer. CME is likely to kill the most visible version for traders who can access the venue through the weekend.

The tougher part moves into a less visible place: whether liquidity, risk controls and clearing behavior can make regulated crypto feel continuous when the back office still keeps a business-day clock.

Russian authorities are preparing to ban crypto mining in the capital city, the adjacent Moscow Oblast and parts of the Kursk region for the next six years.

The news follows reports that mining may be restricted in the whole of Central Russia and comes alongside the adoption of stiff penalties for illegal miners.

Russian government mulls mining ban in Moscow

A Russian government commission responsible for the electric power industry has recommended banning cryptocurrency mining in more of the country’s regions.

The planned full prohibition is expected to cover the city of Moscow, the Moscow Oblast which surrounds it, as well as some areas in the Kursk region, media reports unveiled.

Speaking to the official TASS news agency, Russia’s Deputy Energy Minister Evgeniy Grabchak highlighted that the proposed ban may remain in place until at least 2032.

The issue has been raised by local officials, his department announced at the end of last month, adding it will be resolved by taking into account their positions on the matter, as reported by RBC.

Moscow Oblast’s Energy Minister Sergey Voropanov had previously stated that crypto mining did not benefit the local economy, while the ban had already had a positive effect in other regions.

The region’s governor, Andrey Vorobyov, and Moscow Mayor Sergey Sobyanin both proposed introducing restrictions on mining, the crypto news outlet Bits.media recalled in a post.

At least 65 data processing centers with a total capacity of 734 MW are connected to the grid in the two territories, according to data from the Russian energy ministry.

Kursk Governor Alexander Khinshtein suggested similar measures in eight districts and the city of Lgov, pointing to the oblast’s power supply problems exacerbated by the war in neighboring Ukraine.

His administration claims the mining ban will increase the region’s reserve capacities and save electricity for other consumers, including in both residential and industrial areas.

Mining may be banned in the rest of Central Russia

According to a recent article by the business daily Kommersant, the Russian government is considering banning crypto mining in a total of 19 regions served by Moscow’s power distribution network.

If that happens, the crypto activity will be curbed throughout the Central Federal District, which is the economic heart of the vast nation.

The country legalized mining in 2024, hoping to monetize its competitive advantages in terms of abundant energy resources and cool climatic conditions.

However, the high concentration of mining enterprises in certain areas with low electricity rates resulted in energy deficits.

To deal with power shortages, last year local and federal Russian authorities banned the minting of digital currency in 13 regions until spring 2031.

Affected territories include the Siberian regions of Irkutsk Oblast, Republic of Buryatia, and Zabaykalsky Krai, most Russian republics in the North Caucasus and four occupied Ukrainian oblasts.

Russia to send illegal crypto miners to prison

Meanwhile, the State Duma moved to criminalize illegal mining in Russia. On Wednesday, the lower house of parliament in Moscow passed the respective bill on first reading.

The legislation introduces tough penalties for those engaged in such activities without registration or using stolen energy, including fines, forced labor and imprisonment.

The punishment will depend on the size of the damage and the severity of the violation in each case, the news agencies RIA Novosti and Prime reported.

The operators of a mining facility working outside the law, which generates significant income or causes large financial losses, would face fines that can reach 2.5 million rubles ($35,000).

Prison sentences of up to five years, forced labor and additional fines await miners doing illegal business as members of an organized crime group.

What’s more, the authorities will be able to confiscate the property of such individuals and entities. At the same time, compensating for damages may exempt a guilty person from criminal prosecution.

Both individual entrepreneurs and companies are allowed to mine cryptocurrency in Russia, which is still one of the world’s top Bitcoin mining destinations, provided they register with the state and pay taxes.

However, less than 1,500 out of an estimated 50,000 crypto mining businesses in Russia have done so until now, according to the explanatory note to the draft law.