Crypto exchange balances saw a notable withdrawal wave heading into July 1, with USDC and Bitcoin leading approximately $850 million in net outflows from centralized platforms. The move adds another layer to a market already watching liquidity, ETF flows, and investor positioning closely.

TL;DR

Centralized exchanges reportedly saw around $850 million in net withdrawals over 24 hours.

USDC led stablecoin outflows with about $503 million leaving exchanges.

Bitcoin recorded around $352.7 million in net withdrawals over the same period.

Exchange outflows are wallet movements, not direct evidence of spot buying or selling.

Exchange flows are useful because they show where traders are moving assets, but they need careful interpretation. A withdrawal does not tell us exactly what the owner plans to do next. It may reflect self-custody, institutional settlement, collateral movement, treasury management, or DeFi deployment.

USDC leads the stablecoin move

The largest reported component of the outflow was USDC, with roughly $503 million leaving centralized exchanges. Stablecoin withdrawals can mean several things. Sometimes traders are moving dollars on-chain to use in DeFi. Sometimes market makers are shifting liquidity between venues. Sometimes funds are simply being pulled into custody after a trading period ends.

Because USDC is widely used as a settlement asset, its movement can offer clues about where liquidity may appear next. If stablecoins leave exchanges and move into wallets or protocols, that may support on-chain activity. If they move into custody and stay idle, the signal is more defensive.

Bitcoin withdrawals add a second signal

Bitcoin also saw significant reported withdrawals, with around $352.7 million in net outflows during the same 24-hour window. BTC leaving exchanges is often interpreted as a sign of holding conviction because coins moved into self-custody are usually less immediately available for sale.

That reading is useful, but it should not be pushed too far. Large holders can move coins between wallets for operational reasons. Institutions can rebalance custody arrangements. Traders can withdraw funds without making a long-term investment statement. The signal is strongest when exchange outflows persist across several days and align with improving price action.

A market looking for cleaner signals

The latest outflow wave comes as Bitcoin and the wider crypto market are searching for direction after a difficult June. Spot ETF flows have weakened, US demand indicators remain mixed, and traders are watching liquidity closely. In that environment, exchange reserve data can help show whether investors are preparing to sell or moving assets away from trading venues.

For now, the takeaway is balanced. USDC and Bitcoin withdrawals suggest capital is moving off centralized exchanges, which can be constructive if it reflects custody confidence or on-chain deployment. But the data does not prove immediate buying pressure. It is one piece of the market puzzle, and it becomes more meaningful if the trend continues through the next several sessions.

For readers, the cleanest takeaway is to separate the raw data from the market interpretation. The figures are useful because they show how capital is moving, but they should still be read alongside price action, liquidity conditions, and the wider risk environment.

This report is based on information from CryptoQuant.

This article was written by the News Desk and edited by Samuel Rae.

Bitcoin’s break below the $60,000 area has pushed digital asset markets into a more defensive phase, ending months of narrow trading and exposing a market structure that traders say could amplify the next major move.

CryptoSlate’s data show the largest cryptocurrency had been moving sideways since February, when it first tested the $60,000 area.

That long consolidation made the level a widely watched marker for traders, even as macro risks, spot exchange-traded fund outflows and concerns around corporate Bitcoin holders weighed on sentiment.

As a result, the latest decline points to a more fragile setup where large amounts of Bitcoin have moved toward major exchanges, open interest is rising while spot prices remain weak, and professional traders are paying more to protect against another leg lower.

Bitcoin’s break turns exchange flows into a supply test

The clearest sign of stress has appeared in exchange-linked flows.

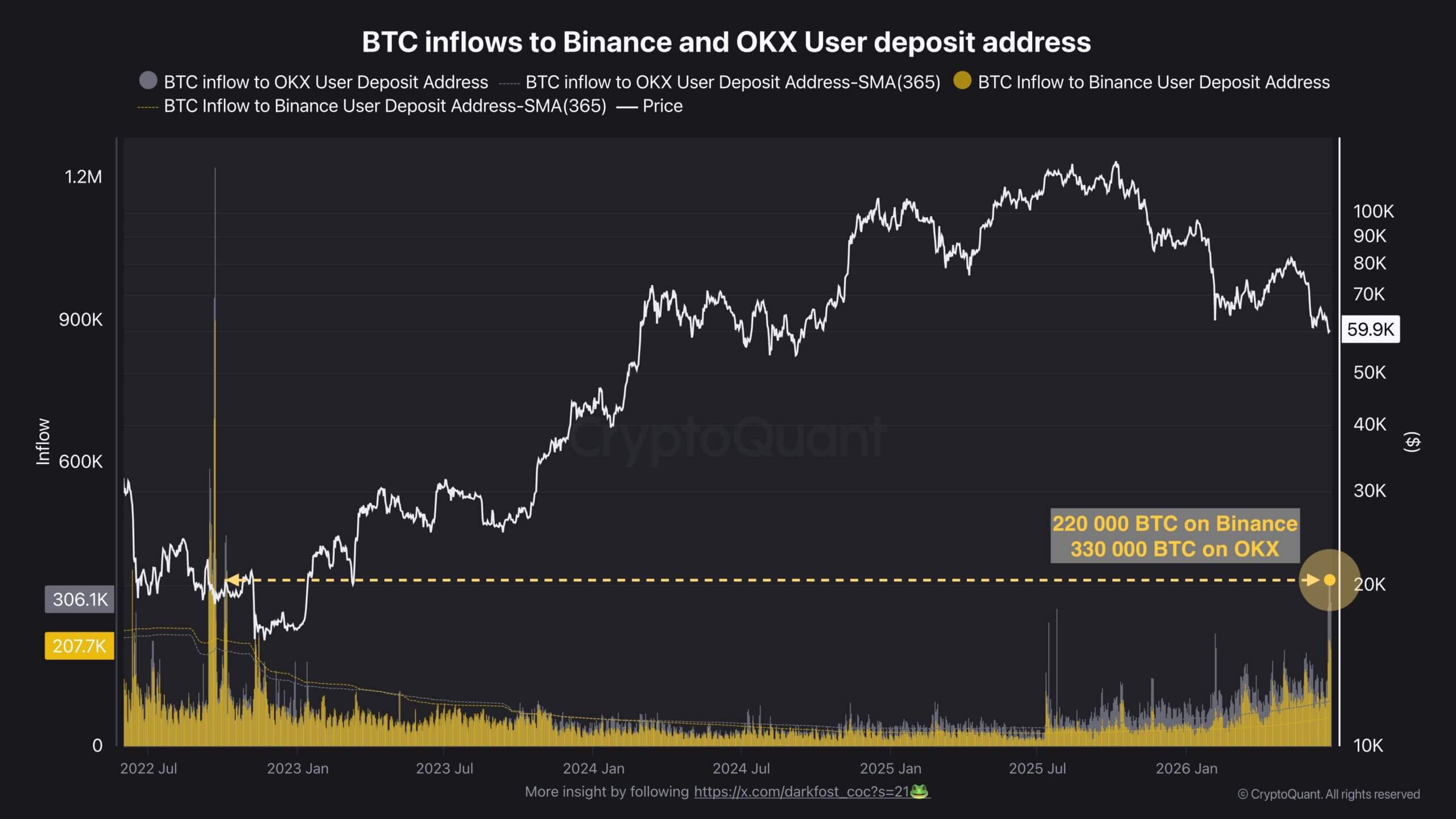

CryptoQuant data show more than 550,000 BTC moved to deposit addresses linked to Binance and OKX after Bitcoin slipped below the $60,000 area. Binance-linked deposit addresses received more than 220,000 BTC, while OKX-linked addresses received more than 330,000 BTC.

Those figures are well above this year’s normal readings. Binance has averaged about 60,000 BTC in comparable inflows, while OKX has averaged about 95,000 BTC, according to CryptoQuant data.

The latest transfers are the largest of the year and resemble levels last seen during the 2023 bear market.

Bitcoin Exchange Transfers (Source: CryptoQuant)

In cryptocurrency market architecture, a sudden transfer of coins to exchange deposit addresses functions as an initial operational indicator of intent. Users typically route assets to these specific points before funds are aggregated into a platform’s central hot wallets for execution, lending, or collateral assignment.

Still, the timing gives the data more weight. Large transfers toward exchanges during a price decline often raise concern that more supply could become available if the market weakens further.

In a market already trading below a level many investors had watched for months, that potential supply overhang can make rebounds harder to sustain.

The flow also reflects how range-bound markets can become unstable once a familiar level breaks. When traders spend months reacting to the same zone, risk controls, hedges and stop-loss decisions can cluster around it. Once the level gives way, many participants reassess exposure at the same time.

That is why the exchange data are central to the current setup. The market is not only dealing with a lower Bitcoin price. It is also dealing with the possibility that more coins have moved closer to venues where holders can act quickly.

Valuation reset reduces excess, but not volatility risk

The exchange flows are arriving as Bitcoin’s on-chain valuation metrics show that much of the earlier cycle’s excess has already been compressed.

CryptoQuant’s MVRV Z-Score shows Bitcoin’s valuation premium has fallen sharply, moving closer to historical low-valuation areas.

The MVRV framework compares Bitcoin’s market value with its realized value. Market value reflects the current price of circulating coins, while realized value estimates the network’s aggregate cost basis by valuing each coin at the price where it last moved on-chain.

Bitcoin MVRV Score (Source: CryptoQuant)

When market value trades far above realized value, unrealized profits are usually elevated and cyclical risk tends to rise. As the gap narrows, profitability declines, and some speculative pressure eases.

The Z-Score adjusts that relationship by measuring the distance between market value and realized value against Bitcoin’s historical market-cap deviation. That helps traders judge whether Bitcoin is trading near unusually stretched or compressed valuation levels compared with its own history.

The current reading suggests the market has moved closer to reset territory.

However, the indicator does not identify a precise bottom. Bitcoin has traded near cheaper valuation zones before while prices continued to weaken, particularly during periods of poor liquidity, forced selling, or macro stress.

That distinction is important now because valuation and positioning are sending different messages. On-chain data suggest the market is less stretched than it was earlier in the cycle. Market structure data suggest traders are still preparing for a disorderly move.

CryptoQuant data show funding rates across major exchanges have moved back into positive territory while Bitcoin remains weak around the $59,000 to $60,000 area. Positive funding generally means traders holding long positions are paying shorts, a sign that demand for bullish exposure has returned after a more negative stretch.

At the same time, open interest is rising while spot prices remain soft. That means new positions are being built into the decline rather than risk leaving the system.

The combination can make price action more sensitive. If Bitcoin falls further, newly opened long positions could come under pressure. If the market rebounds sharply, traders positioned for more downside may be forced to cover.

Either outcome could make the next move larger than the spot market alone would suggest.

Downside hedges build as institutional interest weakens

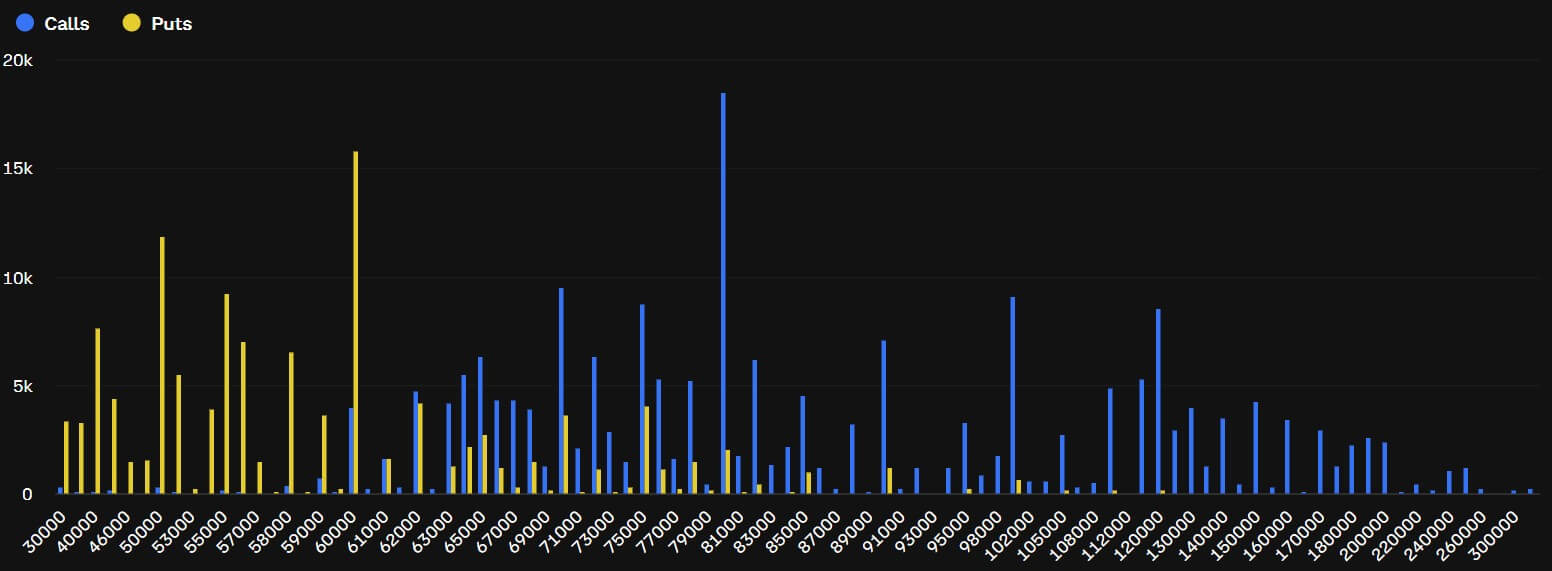

To manage this heightened structural uncertainty, institutional traders are aggressively building a defensive position in the options markets.

Singapore-based digital asset trading firm QCP Capital reports that implied volatility metrics are trending systematically higher as market participants pay a premium for downside protection.

According to the firm, demand has centered on July-expiry Bitcoin put options with strike prices between $55,000 and $58,000.

Data from the digital asset derivatives exchange Deribit reinforces this narrative, showing roughly $1.2 billion in open interest clustered specifically at the $55,000 and $50,000 strike zones.

Bitcoin Options Positioning (Source: Deribit)

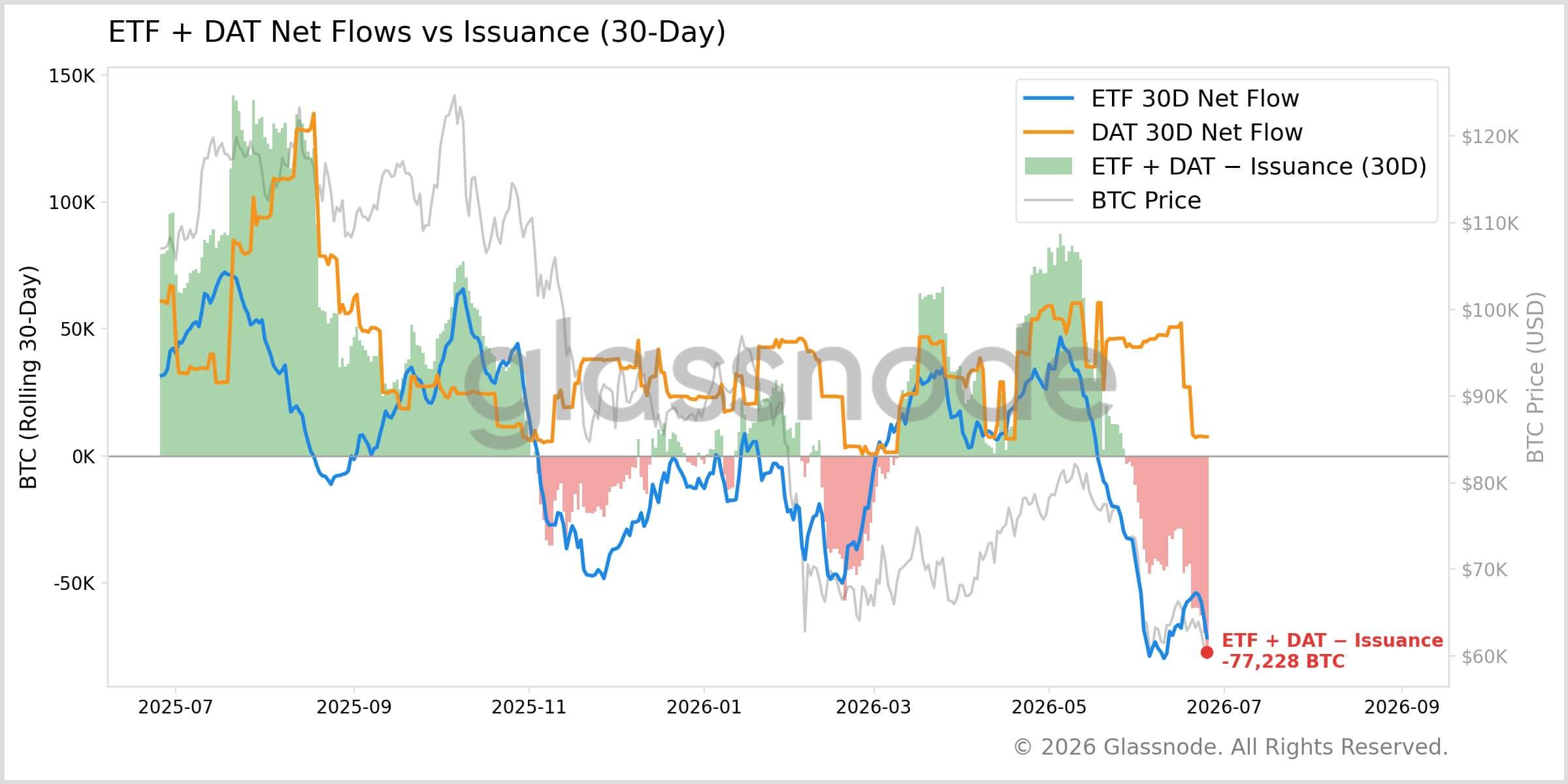

Compounding this defensive positioning is a structural shift in institutional capital flows.

Data from blockchain analytics firm Glassnode reveals that institutional demand is no longer acting as a reliable sponge for circulating supply. Over the past month, spot Bitcoin exchange-traded funds (ETFs) shed approximately 71,600 BTC, while digital asset trusts added only a marginal 7,500 BTC.

When adjusted for network issuance, the combined net institutional capital flow is -77,000 BTC.

Bitcoin ETF and DAT Companies Flow (Source: Glassnode)

According to Glassnode’s analysis, any near-term spot market recovery will face immediate friction from this persistent wrapper supply overhang until net flows reverse.

This institutional deleveraging trend is explicitly quantified by BlockScholes, whose proprietary Bitcoin risk indices have remained fixed below the -1.0 threshold for more than 23 consecutive days.

BlockScholes notes that the longevity of this trend marks a departure from typical cyclical dips, signaling an ongoing, structural risk reduction by institutional allocators that will likely require a fundamental macroeconomic or industry-specific catalyst to alter.

That leaves Bitcoin in a fragile position after its break below the $60,000 area. On-chain valuation metrics suggest the market has already shed much of its earlier excess, but exchange flows, options positioning, and institutional demand all point to a market still preparing for stress.

The immediate test is whether spot demand can absorb the supply now sitting closer to exchanges. If demand improves, defensive positioning could help fuel a rebound.

If it does not, the same structure could turn the $60,000 break into a broader shock to volatility.

Galaxy Digital CEO Mike Novogratz identified excessive leverage as a key factor behind the June crypto drawdown.

The view fits with a market environment where derivatives positioning can amplify spot-market weakness.

Risk note: Do not add dramatic price targets or overstate the quote beyond the original wording.

For more details, visit the official Galaxy platform.

Leverage unwinds can turn ordinary market weakness into sharper crypto corrections

Mike Novogratz Points to Leverage as Driver of June Crypto Market Correction is a timely crypto-market story because it gives readers a clear signal to watch without leaning on hype or unsupported price targets.

The important point is not just the headline number or technical level. It is the way that signal fits into the wider market: liquidity is thinner, Bitcoin direction is fragile, and traders are paying closer attention to flows, wallet activity, derivatives positioning, and official ecosystem updates.

What the verified setup shows

Galaxy Digital CEO Mike Novogratz identified excessive leverage as a key factor behind the June crypto drawdown. The view fits with a market environment where derivatives positioning can amplify spot-market weakness.

The claim should be tied only to the original quote or interview once verified.

That makes this a useful setup for readers who want to understand what is actually changing beneath the surface. It also helps separate measurable market data from the more speculative narratives that often appear during volatile weekends.

Why this matters for the market

For Novogratz leverage crypto, the signal matters because it offers a specific lens for the current market rather than a vague bullish or bearish call. In a weak or uncertain tape, traders tend to focus on the data points that can be checked directly: flows, wallet routes, support zones, funding, moving averages, official technical updates, or security disclosures.

This is especially important in the current environment. Bitcoin has been trading near important support, altcoins remain sensitive to broader risk appetite, and institutional or on-chain activity can quickly become part of the market narrative.

What traders should avoid assuming

Do not add dramatic price targets or overstate the quote beyond the original wording.

That caution matters because many of these signals can be misread. ETF outflows do not automatically mean permanent institutional retreat. Wallet transfers do not automatically mean selling. Technical support does not guarantee a bounce. Developer updates do not immediately translate into price action.

What to verify next

The next validation path is: Mike Novogratz public statements or Galaxy Digital investor updates. This is the key step before treating the setup as anything more than a developing market or ecosystem signal.

The original quote must be verified for timing and context before publication.

This report is based on information from official source materials and publicly available market data.

This article was written by the News Desk and edited by Samuel Rae.

Jeremy Grantham, the GMO co-founder who called both the 2000 dot-com crash and the 2008 housing collapse, branded Bitcoin (BTC) “a useless, speculative mechanism” and predicted it would dwindle over the next few decades.

The veteran strategist built his critique around three failures he sees in crypto. Bitcoin pays no yield, holds no stable value, and fails as a usable currency in daily life, he argued.

Proof of Work, Proof of Nothing

Grantham singled out Bitcoin’s proof-of-work design for particular scorn. The energy burned to validate transactions, he argued, generates no economic benefit for society.

“Proof of unnecessary work shouldn’t be worth a bucket of warm spit, and it will not be.”

He made a name for himself by making brave calls, and seeing around corners. Today Jeremy Grantham made a rare TV appearance on Squawk Box with a warning for investors. https://t.co/QNxCC0nioLpic.twitter.com/i5dpQRgV1Q

Beyond the mining critique, he said Bitcoin does not work as a practical currency. Regular users do not accept it at the supermarket, and serious investors do not settle large transactions with it. Without a functioning transaction layer, the asset cannot claim monetary legitimacy, he added.

He also dismissed Bitcoin as a store of value. Unlike equities, it pays no dividend and generates no cash flow. In his view, that leaves speculators with nothing to anchor a fair price.

A Skeptic With a Record

Grantham’s warnings carry weight because of his track record. He flagged the dot-com bubble before 2000 and warned of the US housing collapse before 2008. His more recent AI bubble stock warning extended that thesis to US equities, where he now sees downside of up to 70%.

However, his timing is not always precise. His 2021 epic-bubble call on US stocks arrived early, as markets climbed before their 2022 correction.

The Bitcoin remarks land as BTC trades near $60,500, down sharply from its late-2025 peak above $126,000. US spot Bitcoin ETF records outflows of $6.35 billion over 30 days through mid-June, reflecting cooling institutional demand.

Earlier, Coinbase CEO’s Bitcoin outlook has also flagged AI infrastructure costs as a variable reshaping crypto capital flows.

Bitcoin Price Chart in June 2026. Source: CoinGecko

Grantham is not alone in his skepticism. Peter Schiff has made similar bearish arguments, contending that Bitcoin holds no intrinsic value.

Whether Bitcoin’s current price holds key support in Q3 2026 will test both camps. Grantham predicted the decline would come gradually, over years or even decades, not all at once.

Ripple CTO Emeritus David Schwartz has clarified a long-running point of confusion in the XRP community: XRP did not exist before Bitcoin. The debate often resurfaces because RipplePay, an early trust-based payment concept created by Ryan Fugger, dates back to 2004. But Schwartz drew a clear line between that earlier idea and the XRP Ledger, which launched years after Bitcoin.

TL;DR

David Schwartz clarified that XRP was not created before Bitcoin.

Bitcoin launched in 2009, while the XRP Ledger and XRP token were developed from 2011 and launched in 2012.

The confusion comes from RipplePay, a 2004 credit-trust network concept that did not use blockchain technology or a native asset.

Schwartz also pushed back on claims linking an old distributed computing patent to XRP or blockchain design.

RipplePay Versus XRP Ledger

The heart of the confusion is the word “Ripple.” Ryan Fugger’s RipplePay was conceived in 2004 as a way to think about payments through trust relationships and credit lines. It was not a blockchain, and it did not include XRP as a native digital asset. That distinction matters because some social media narratives have blurred the early RipplePay idea with the later XRP Ledger.

According to the validated writing pack, Schwartz clarified that development of the XRP Ledger and XRP token began in 2011, with the ledger launching in 2012. Bitcoin, by comparison, launched in 2009. On that timeline, XRP clearly does not predate Bitcoin.

Why The Claim Keeps Returning

The claim is sticky because the XRP ecosystem has a complicated history. RipplePay predates Bitcoin, the company that became Ripple later became associated with XRP, and several early crypto builders explored payment-network ideas before blockchains became mainstream. That creates enough overlap for misleading claims to spread quickly online.

But the technical distinction is straightforward. A credit-trust payment network is not the same as a blockchain ledger with a native token. RipplePay was an early payments concept. The XRP Ledger was a later cryptographic network built in the post-Bitcoin era.

Schwartz Also Addresses Patent Rumors

The validation notes also state that Schwartz pushed back on rumors connecting his 1988 distributed computing patent to blockchain or XRP. That type of claim has circulated in parts of the XRP community for years, often as part of broader theories about XRP’s origins or supposed pre-Bitcoin design.

Schwartz’s clarification narrows the historical record. His earlier work in distributed computing may be part of his broader technical background, but it should not be treated as proof that XRP existed before Bitcoin or that the XRP Ledger was secretly developed before 2009.

A Cleaner Timeline

The clean version is simple: RipplePay was an early 2004 payment-network concept without blockchain technology or a native digital asset. Bitcoin launched in 2009. The XRP Ledger and XRP token were developed beginning in 2011 and launched in 2012. Those dates do not diminish XRP’s role in crypto history, but they do correct the idea that XRP came first.

For traders and long-term XRP holders, the clarification is less about price and more about narrative discipline. Crypto communities often build identity around origin stories, but when those stories become inaccurate, they can create unnecessary confusion. Schwartz’s comments help separate genuine XRP history from social media mythology.

A Hong Kong district court has rejected Xiao Rui’s claim that part of his money came from selling Bitcoin and found him guilty of laundering more than HK$64 million through underground banking channels.

The 37-year-old son of a former anti-corruption official from Wuhan faces sentencing on July 23 after being found guilty on four counts of money laundering and one count of using a false document.

Bogus BTC sale defense gets rejected

Between March 2014 and November 2023, about 38 transactions totaling over HK$64 million flowed into Xiao Rui’s personal bank accounts. The money came from at least 12 companies and 12 individuals. None had any business ties to Xiao’s asset management firm, yet he told the court that some of the money in his Hong Kong bank accounts came from selling Bitcoin.

Acting Judge Bernard Chung said Xiao could not provide any basic records like transaction dates, reference numbers, or wallet addresses to prove his claim. The judge found this explanation weak and rejected it outright.

Xiao also claimed that the money was a gift from his mother. According to him, she had earned the money through her business and gave it to him for investment in Hong Kong. However, under questioning, Xiao said his mother had worked as a nurse before moving to administrative jobs. He claimed she received a cash bonus of HK$20 million from a power company in 2016, but the judge said this story did not fit with her employment history.

The court heard that a contractor named Yao Qian, who had secured a municipal water-pump project in Wuhan, deposited about HK$4.72 million into Xiao’s bank account. Xiao Jun, Xiao Rui’s father, reportedly helped with this contract when he headed a bureau in the Wuhan People’s Procuratorate. Notably, the older Xiao was previously suspended amid a mainland corruption investigation.

The judge found the contractor’s testimony believable and rejected the defense claim that the money was legitimate business income.

How did Xiao get Hong Kong residency with fake documents?

The case also includes fraud related to Xiao Rui’s Hong Kong residency. In 2013, he applied to live in Hong Kong through the Capital Investment Entrant Scheme. This program required applicants to show they had assets over HK$10 million. Xiao submitted fake deposit certificates from a China Construction Bank branch in Wuhan.

Bank staff later confirmed the accounts did not exist. Despite this, Xiao was approved for residency in 2014, and that same year, he used his HSBC account to buy two fund products worth HK$10 million in order to meet the scheme’s investment requirements.

The court found Xiao guilty of using false documents for this application, and he claimed to be unaware of the fact that the documents were fake because his mother handled the application. The judge did not accept this excuse.

Prosecutors said the money laundering happened over nearly a decade. Xiao used accounts at Standard Chartered, DBS, and HSBC to move the money through what the court called underground banking channels.

The Independent Commission Against Corruption (ICAC) has asked for the criminal proceeds to be taken from Xiao, but a date for this hearing has not been set yet.

Xiao will stay in custody until his sentencing, where he faces prison time for the money laundering charges, which carry sentences of up to 14 years in Hong Kong.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Bitcoin (BTC) fell below $60,000 again on Wednesday, this time with a steeper decline than the two previous instances in early June.

However, despite the breach, 21Shares still says the four-year cycle has not broken. The crypto asset manager had forecast that institutional demand would end Bitcoin’s halving-driven pattern in 2026.

Bitcoin recorded an intra-day low of $59,102 as of this writing, down nearly 5% over 24 hours. The token has fallen more than 50% from its $126,080 record set in October 2025. It marks the third time the pioneer crypto falls below $60,000 this month.

Bitcoin has peaked 12 to 18 months after each past halving, then fallen hard. The April 2024 halving fed the run to October’s record, and the current slump tracks the same path.

Bitcoin’s four-year cycle has not yet broken. Source: 21Shares

In its latest State of Crypto report, 21Shares said the decline still mirrors past post-halving corrections. The firm had entered the year expecting Bitcoin’s four-year cycle to finally break.

“Heading into 2026, we believed that Bitcoin’s four-year cycle could be finished. Six months in, we have to be honest: price action still looks familiar,” read an excerpt in the report.

The drawdown still looks mild next to the past two cycles. Glassnode data show Bitcoin fell about 84% after its 2017 peak and 77% after the 2021 peak.

Even while trading below $60,000, Bitcoin holds above the roughly $54,000 cost basis the report flags. That suggests sellers have not fully capitulated.

Institutional Money Cushions the Drop

21Shares built its original call on heavy exchange-traded fund (ETF) inflows and growing institutional adoption. It expected those forces to soften the boom-and-bust rhythm tied to Bitcoin’s halving.

Ownership has indeed grown more institutional, which the firm says makes capital stickier through downturns. Through late May, it counted about $3 billion in net ETF outflows.

The bleed has since deepened into a record outflow streak in June. Even so, net ETF inflows since the 2024 launch still total roughly $53 billion, SoSoValue data shows.

Bitcoin ETF Cumulate Total Net Inflow. Source: SoSoValue

21Shares still expects that institutional base to support a recovery toward $100,000 by year-end, not a breakout to new highs.

Not Every Analyst Sees a Soft Landing

Other voices see more pain ahead. BitMEX co-founder Arthur Hayes expects a $40,000 bottom within six months, well below the cost basis 21Shares watches.

Hayes points to a hawkish Federal Reserve, where traders now put December rate-hike odds near 37% on CME FedWatch. He stays long while hedging with options, a stance that captures the current unease.

Thursday’s inflation reading and the Fed’s next moves may decide which view holds. A softer print could ease pressure, while another hot number may invite a deeper test of support.

Bitcoin’s break below $60,000 on June 24 exposed the market’s timing problem: sellable coins moved closer to exchanges while ETF demand weakened and leveraged traders cut risk.

CryptoSlate market data shows Bitcoin trading near $59,340, down 4.05% over 24 hours and 9.03% over seven days.

That price puts BTC below one of the market’s most visible support areas just as selling pressure was becoming easier to trace.

The clearest signal came from CryptoQuant, which flagged roughly 7,600 BTC moving into Binance as panic selling picked up. At these market levels, that represents about $479 million in potential sell-side pressure.

Potential is the key qualifier. Exchange inflows show sellable supply moving closer to a venue where it can hit the market, while the $60,000 area was already under pressure.

That is the key difference between a simple price move and a market-structure break. Bitcoin fell as new supply became more available and some of the market’s usual absorbers looked weaker.

Sell pressure reached the venue first

Exchange inflows become more important when they arrive near a crowded level. A move of 7,600 BTC into Binance gains force when set alongside other pressures already building around support.

CryptoQuant’s separate market-deterioration context pointed to weakening conditions around the move, reinforcing the view that the break was driven by a stack of pressures rather than a single clean headline catalyst.

When Bitcoin is hovering at a level as visible as $60,000, traders do not need a single event to trigger selling. They need a reason to doubt that buyers will keep absorbing supply.

That doubt was visible in the flows. Lookonchain reported negative net flows in spot Bitcoin ETFs on June 24, with 1D net flow at -2,548 BTC and 7D net flow at -6,728 BTC.

Still, ETF flows represent only one demand channel, but they have become one of the clearest public gauges of whether institutional-facing demand is adding support or removing it.

When those flows turn negative while exchange inflows rise, the market receives two signals at once. More coins may be available to sell, while one of the most-watched demand channels appears weaker.

ETF outflows were one part of the break, rather than the sole reason, but they help explain why the move accelerated once $60,000 gave way.

The price context added to the pressure. CryptoSlate’s broader crypto market and Bitcoin data shows BTC still holding market dominance but trading with a sharp seven-day decline.

In that setting, dip buying had to fight both spot supply and deteriorating confidence. The same combination also made each new flow update more important, because traders were watching whether the market still had enough absorption to turn a break into a reset.

That is the direct answer to why the break accelerated: new sellable supply appeared while the market’s public demand channel was weakening. The move turned a familiar support test into an absorption test, forcing traders to judge whether buyers were stepping in, whether support had stopped doing its job, and whether leverage would add another round of selling below the line.

Leverage turned the break into a faster move

The second layer was leverage. Lookonchain separately reported that a whale closed an 800 BTC long after Bitcoin fell below $61,000.

One large, long closure only shows a single example of discretionary risk being cut, but the timing is still important. It came before the $60,000 line fully stabilized.

That dynamic changes how support fails when leveraged positions are involved. Spot selling can push the price to a level.

Leverage can make the next leg faster because traders who expected a bounce are forced to reduce exposure or exit when the level fails. That is where liquidation dashboards become part of the story rather than a side detail.

CoinGlass data shows Bitcoin liquidation pressure, with repeated BTC long liquidation alerts near $59,650 to $59,670 as the price traded below $60,000, consistent with the move’s shape. As the price pushed through support, long exposure was being cleared near the new lower range.

The breakdown should therefore avoid a bearish prediction frame. The evidence leaves room for a bounce, but it also shows that the market’s ability to absorb selling weakened precisely when more sellable supply and forced risk reduction became visible.

That makes the liquidation sequence a sign of stress in the support zone rather than a standalone forecast for the next leg.

The distinction changes what traders should watch next. If the break was mainly panic selling into stronger hands, the market should begin to show signs of repair quickly: fewer exchange inflows, calmer liquidation alerts, and ETF flows that stop bleeding.

If those signals fail to appear, the same evidence points to a different conclusion: $60,000 was not redistribution, but failed support.

The sequence also keeps the focus on market plumbing rather than sentiment alone.

The next signal is absorption

A quick bounce above $60,000 would be incomplete if it arrives without calmer flows underneath. The more important question is whether the market can absorb supply without leaning on forced buying or a temporary short squeeze.

For the redistribution case to improve, Binance inflows need to slow after the 7,600 BTC move. ETF flows need to stabilize after the reported 1D and 7D outflows.

Long liquidation pressure needs to cool rather than migrate to lower bands. A $60,000 reclaim would carry more weight if it came with signs of calmer positioning.

The failed-support case gains weight if the opposite happens. Continued exchange inflows would suggest sellers are still preparing to use deep liquidity.

More ETF redemptions would imply weaker demand from institutional investors. Further long liquidations below the near $59,650 level would indicate that the market is still clearing leveraged exposure rather than rebuilding spot demand. Bitcoin is currently testing that exact area.

Strategy and MSTR anxiety also play in the background, as confidence among large Bitcoin holders affects market psychology. However, as of press time, there is independent evidence of direct BTC selling.

The market points elsewhere: sellable coins moved toward Binance, ETF flows were negative, a whale long was closed below $61,000, and liquidation pressure appeared as BTC traded under $60,000.

That makes the $60,000 break a test of absorption more than a simple support failure. Bitcoin can still turn panic selling into redistribution if buyers step in while flows calm.

If they fail to do so, the break has already shown where the weakness sits: new selling reached the market before backstop buyers showed enough strength to catch it.

Bitcoin (BTC) has slipped below the lowest band of the Bitcoin rainbow chart, the zone the original model bluntly labeled “Bitcoin is dead.” The asset now trades near $62,500, roughly half its October record.

Statistician George Box once wrote, “All models are wrong, but some are useful.” Stock-to-flow has already crossed from useful to broken. The question now is whether the rainbow chart is heading the same way.

Understanding Bitcoin’s Rainbow Chart

The rainbow chart plots Bitcoin’s price against a logarithmic regression band. Each colored band marks a sentiment zone. Red euphoria sits at the top, and deep value sits at the bottom.

The original version contains 10 bands. At its lowest, a purple strip carries the grim label “Bitcoin is dead.” Sliding into it has always signaled extreme pessimism.

A Reddit user first sketched the chart in 2014. A Bitcointalk contributor later paired it with logarithmic regression, which gave the bands their familiar shape.

For most of Bitcoin’s history, the gauge worked. Tops landed in the warm red bands, and bottoms landed in the cool blue and purple zones.

An updated version of Coinglass trims the model to nine bands. It drops the purple floor entirely, leaving “Fire sale!” as the bottom zone. Our explainer on the rainbow chart band model covers how these bands are built.

Today, Bitcoin sits below even that floor. Its live market price of about $62,500 has dropped through the “Fire sale!” band, outside the model’s defined range.

That has happened only once before, near the 2022 bear-market low. By one reading, the breach frames the current level as a rare deep-value entry point.

A deep-value reading assumes the model still works. Stock-to-flow shows why that assumption carries real risk.

The pseudonymous analyst PlanB introduced the stock-to-flow scarcity model in 2019. It tied Bitcoin’s price to its shrinking supply, with issuance halving after each halving.

For years, the fit looked convincing. Price oscillated around the model line through 2013, 2017, and 2021, which lent the framework real credibility.

Then it broke. After the 2024 halving, the model demanded roughly $500,000. Bitcoin instead peaked near $126,000 in October 2025, missing the target by about 75%.

PlanB pushed the projection further. He has suggested Bitcoin could near $5 million by the 2028 halving, a figure the current price makes hard to defend.

Critics point to a deeper flaw. The model tracks supply alone and ignores demand, the force that actually moves price during real market stress.

The stock-to-flow deflection chart measures price divided by the model’s value. For years, that ratio reverted toward one. Now it is collapsing toward zero.

A ratio grinding to zero means the error no longer corrects itself. The model now predicts a number that reality keeps ignoring, cycle after cycle.

George Box anticipated this outcome. A model can accurately describe the past and still fail to predict the future. Stock-to-flow has moved firmly into the wrong column.

Will the Bitcoin Rainbow Chart Follow?

The rainbow chart shows early symptoms of the same illness. Its weakness appears at both ends of the range, not just the floor. Past peaks in 2013, 2017, and 2021 pushed into the red “sell” bands near the top.

This cycle’s high reached only the green “Accumulate” zone, far below previous levels.

So price keeps undershooting the upper bands while now breaking the lower one. The band structure that once contained Bitcoin no longer holds it on either side.

Both models lean on relentless exponential growth. Yet Bitcoin is now a $1.25 trillion asset, and very large numbers compound more slowly over time.

That maturing growth curve is exactly what an aging exponential model fails to capture. The chart assumes tomorrow will look like the early years, and it may not.

This shift has a name among analysts. Many now favor a power-law view, where Bitcoin keeps rising but at a steadily slowing pace. A genuine recovery would pull the price back inside the bands and quiet the doubts. A long drift below them would suggest the model is breaking in real time.

Trading near $62,500, down about 3% on the day and 50% below its record, Bitcoin is clearly not dead. The model that was named that band might be.

Whether the rainbow chart joins Stock-to-Flow in retirement, or its longer-term price forecast still holds, is the question the next cycle will answer.

Diplomatic efforts between Iran and the United States showed early signs of progress after senior officials from both countries held talks in Switzerland.

Mediators from Qatar and Pakistan said the discussions were constructive, as both sides agreed to a 60-day timeline to secure a final deal. Further technical meetings are scheduled to take place at the Burgenstock resort later this week. The optimism surrounding the talks briefly pushed Bitcoin (BTC) above $64,000, although the asset later gave back some gains and fell below the level.

However, tensions between the two countries still linger as the deal was not signed by June 19 as promised and there are new attacks between Israel and Lebanon. One analyst has outlined a potential downside scenario for Bitcoin if wider market conditions deteriorate.

Worst-Case Scenario

Bitcoin could fall to $23,979 in 2026 if the broader stock market suffers a crash of more than 50%, according to technical analyst Jesse Olson. He shared a two-week Bitcoin chart that depicted BTC potentially declining toward the $23,980 level, based on a long-term volume-weighted support line derived from his proprietary Market Sniper Pro VWAP indicator.

Olson said such a move would likely require a major stock market downturn while adding that he does not expect Bitcoin to fall to zero.

Meanwhile, another prominent market commentator, Doctor Profit, said that Bitcoin is forming a bearish flag on the daily chart, while growing market optimism is creating liquidity below current prices. He said Bitcoin’s recent uptick matched his earlier expectations and explained that prices can revisit the same levels several times during sideways trading. He expects the asset to eventually fall toward the $54,000-$56,000 range before finding a market bottom at lower levels.

Lagging Institutional Demand

Between June 14 and June 18, spot Bitcoin ETFs saw net outflows of $227 million and extended their losing streak to six straight weeks.

CryptoQuant analyst Darkfost also highlighted the weak institutional appetite for Bitcoin and said the Coinbase Premium Index has remained largely negative in recent weeks. The indicator compares BTC prices on Coinbase Advanced and Binance to gauge the behavior of professional and retail investors.

According to Darkfost, negative readings mean that institutions trading on Coinbase are selling more aggressively than retail investors on Binance, which has created downward pressure on prices. He added that a wider price gap between the two exchanges points to a greater divergence in investor behavior. Institutional investors are not trying to catch a market bottom; instead, they prefer to wait for stronger price performance and clearer signs of a recovery before increasing their Bitcoin exposure.