Robert Kiyosaki warns that the global economy is heading for a 2026 crash. The author of Rich Dad Poor Dad named silver as one of his best current investments.

The veteran investor framed the coming downturn as an opportunity for prepared buyers. He pointed to silver as a real asset that fiat money cannot replicate.

Why Kiyosaki Sees a 2026 Crash

Kiyosaki has repeated this warning across X (Twitter) in recent months, tying it to his 2002 book Rich Dad’s Prophecy. He argues the “Everything Bubble” he flagged decades ago is finally unwinding.

He blames roughly $39 trillion in US debt and a weak dollar dating to 1974. Fragile baby boomer retirement accounts add another layer of vulnerability.

Past crashes in 1987, 2000, 2008, and 2022 made him richer, he says, because he held real assets. He plans to run the same playbook in 2026.

“In 2026 the global economy is about to crash. That’s good news for those that can see the future. Bad news for the blind,” Kiyosaki stated.

However, mainstream forecasters do not share the Great Depression framing. Most institutions still project moderate global growth in 2026, while flagging sovereign debt and geopolitical tension as downside risks.

Kiyosaki said he began stacking silver in 1965 at 18 years old, when prices traded in cents. He now treats it as both a monetary hedge and a critical industrial metal.

The asset feeds solar panels, electric vehicles, batteries, and artificial intelligence (AI) infrastructure. Spot silver trades near $85 an ounce after a sharp run-up over the past year.

The fundamentals support parts of his case. The market is running its sixth straight year of structural deficits. Industrial demand now accounts for roughly half of total consumption.

Other Voices Echo the Silver Trade

Kiyosaki is not alone. Veteran trader Vijay called silver near $75 to $80 too cheap to ignore. He cited the lowest CME inventory since January 2025.

“Next 6 months, likely to surprise on the Positive side. It is a a scarce commodity (Lowest inventory on the CME since January2025 ) & one of the most hated asset class,” the trader wrote.

Research firm World of Finance and Associates set a $88 to $92 ceiling if macro shocks stay limited, while other precious metals analysts see silver miners as leveraged plays.

Silver: Currently given buy since 72$ for 82$ Target which was hit successfully.

If there is no negative news then we can head towards 88$-92$ max .

Beyond that I am not looking for it .

For long term investment Wait for another round of minimum 50% correction in both #Gold… https://t.co/UKO6tgAazI

— World of Finance and Associates 🌎 (@manerhushi123) May 10, 2026

Kiyosaki’s six-asset survival list for 2026 also includes gold, oil, food production, Bitcoin, and Ethereum. Whether his crash call arrives on schedule will determine how the silver bet looks by year-end.

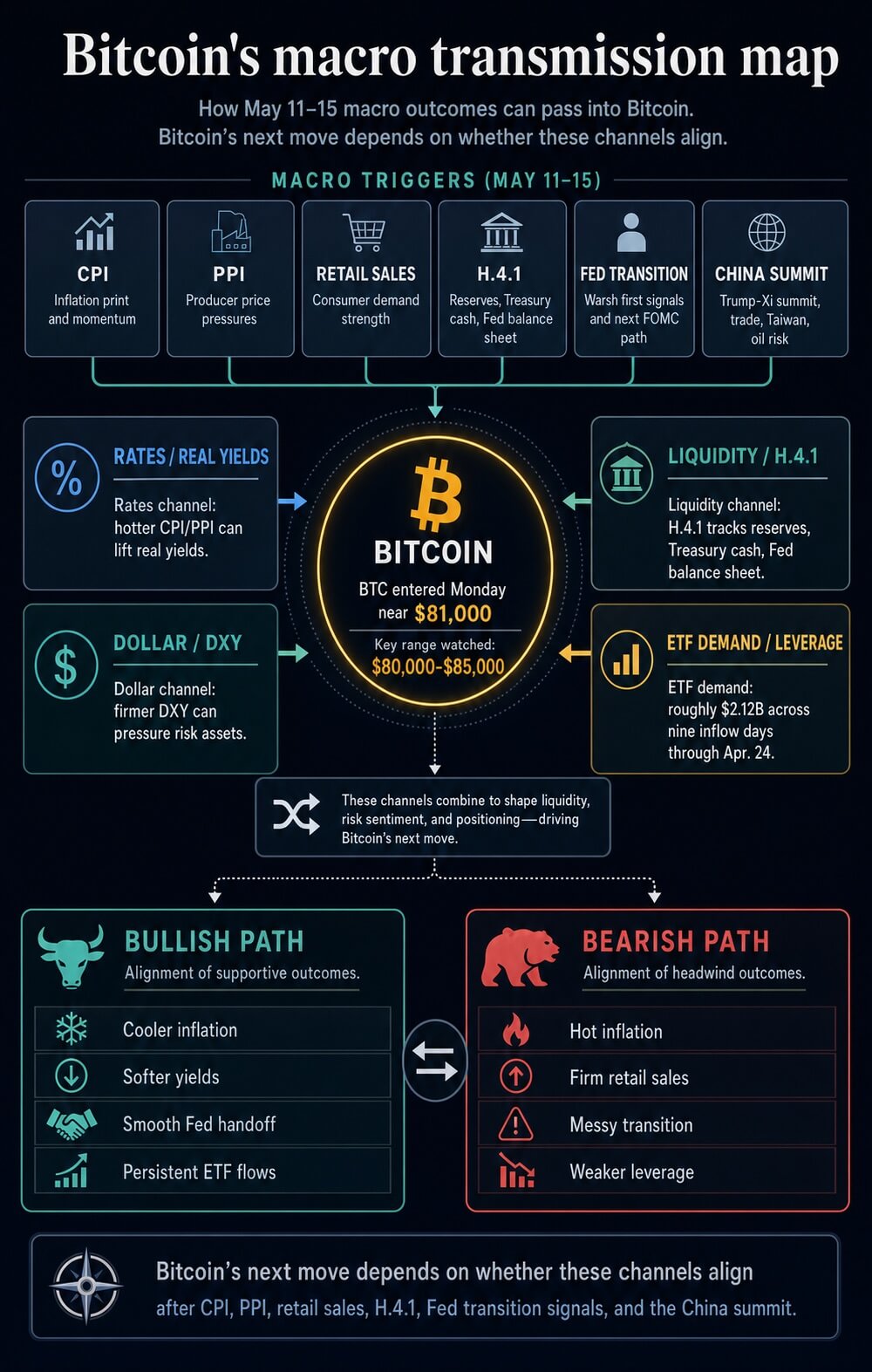

Bitcoin faces 2026’s densest macro test as CPI, Warsh, and Trump-Xi collide

This week (May 11-15) has a credible claim to being the most consequential macro window of 2026 so far, as it compresses every channel currently driving risk assets into a single sequence.

Inflation, producer costs, consumer demand, Fed liquidity, central bank leadership, trade risk, oil risk, and the dollar are all scheduled to move within five trading days.

Bitcoin enters that window as a liquidity-sensitive institutional asset, making the calendar a direct test of whether the recovery above $80,000 has macro sponsorship or only positioning support.

The strongest rival week came earlier in the year, when the Iran conflict and the Strait of Hormuz shock pushed energy markets into the center of the inflation debate.

The St. Louis Fed’s review of market reactions to military action against Iran marked Feb. 28, Mar. 1, and Apr. 13 as key shock points for oil, volatility, and geopolitical repricing.

That episode carried the larger single exogenous impulse. It changed the inflation path through energy, widened the risk premium in crude, and forced investors to reprice the Fed’s tolerance for cutting into a supply shock.

The March inflation data then showed how that shock entered the official series. The March CPI report showed consumer prices rising 0.9% month over month and 3.3% year over year, with energy up 10.9% and gasoline up 21.2%. The March PPI report showed final demand prices rising 0.5% in March and 4.0% over the prior 12 months, the largest annual increase since February 2023.

Those prints gave 2026 a genuine inflation shock rather than a routine data scare.

April 28-29 was the other major comparison point because it combined an FOMC decision, dissents, oil-related inflation anxiety, and the Senate Banking Committee’s movement on Kevin Warsh.

The Fed held rates at 3.5% to 3.75%, but the April FOMC statement carried an unusually fractured vote. One governor dissented in favor of a 25 basis point cut, while three officials supported the hold and opposed language that leaned toward easing.

That meeting exposed a central bank split between inflation caution and growth insurance.

May 11-15 ranks above those weeks in event density.

The Iran shock was larger as a geopolitical impulse. The April FOMC was sharper as a policy signal.

This week combines both transmission paths and adds a leadership handoff. It forces markets to price in inflation persistence, consumer resilience, Treasury and reserve mechanics, Fed credibility, and U.S.-China geopolitical risk simultaneously.

For Bitcoin, that makes it the broadest macro stress test of the year so far.

Calendar of major macro events between May 11 and May 15, including CPI, PPI, retail sales, Fed liquidity data, Powell remarks, and the Trump-Xi summit, outlining the key catalysts shaping Bitcoin and global risk markets.

The official calendar stacks inflation, demand, Fed liquidity, leadership risk, and China into one macro test sequence

The official sequence begins with inflation.

The Bureau of Labor Statistics has the April CPI release scheduled for Tuesday, May 12 at 8:30 a.m. ET.

It then has the April PPI release scheduled for Wednesday, May 13 at 8:30 a.m. ET.

That pairing gives markets a two-day signal on whether the March energy shock and tariff pressure are still moving through consumer and producer prices, or whether the inflation impulse is already losing force.

Thursday broadens the test from prices to demand and liquidity.

The Census Bureau has April retail sales scheduled for Thursday, May 14 at 8:30 a.m. ET.

The Federal Reserve’s May calendar lists H.4.1 balance sheet data for the same day at 4:30 p.m. ET.

That means markets receive a consumer-demand signal in the morning and a liquidity signal after the close.

A strong retail number alongside hot inflation would reinforce the case for policy restraint. A weaker retail print alongside softer inflation would give the next Fed chair more room to argue that the economy can absorb lower rates.

The balance sheet release carries direct information for crypto. The May 7 H.4.1 report showed total Fed assets near $6.71 trillion, reserve balances around $3.03 trillion on average, and the Treasury General Account near $878 billion on average.

For Bitcoin, the direction of reserves and Treasury cash balances often carries more direct market information than the headline size of the Fed’s asset portfolio.

Falling reserves and a large Treasury cash balance can keep liquidity tight even when investors expect easier policy later.

Friday then adds the leadership handoff.

Jerome Powell’s official term as Fed chair ends May 15, while his Board term runs to January 2028.

Powell also said at the Apr. 29 press conference that he expected to continue serving as a governor for a period after the chair term, while keeping a low public profile.

Kevin Warsh’s nomination sits on the same track. The Senate Banking Committee held a nomination hearing on Apr. 21, and the committee later advanced him on a party-line vote.

Warsh could inherit his first inflation test before markets know his reaction function

Wednesday’s official anchor is PPI, while the Fed calendar lists other officials and provides no primary-source basis for making a chair speech the central event.

The larger issue sits at the end of the week: Warsh could inherit his first inflation signal before his reaction function is visible.

If CPI or PPI accelerates, the new chair begins boxed in by data.

If inflation cools, he begins with room to define how quickly the Fed can pivot without inviting a bond-market credibility premium.

President Donald Trump’s China trip then widens the map. He is scheduled to meet Xi Jinping in Beijing during a May 14-15 visit, according to AP.

That summit adds trade, tariffs, Taiwan, oil logistics, and dollar-risk channels to the same window as CPI, PPI, retail sales, H.4.1, and the Fed leadership transition.

A constructive summit could lower the trade-risk premium and ease the dollar bid.

A tense summit could lift the dollar and pressure offshore liquidity, especially if energy security and the Iran war remain tied to the negotiations.

That combination makes the week structurally different from the usual CPI cycle. Inflation data alone can move Bitcoin. A new Fed chair inheriting that data can change how markets price the next several meetings.

Warsh’s nomination has already been framed around institutional change at the central bank, including questions about models, communications, bond holdings, and the Fed’s reaction function.

That creates an immediate test: does the market treat the transition as a path toward a more responsive Fed, or as a source of uncertainty around independence, inflation tolerance, and the long-run policy framework?

A hotter sequence would put Warsh in the hardest possible opening position.

CPI and PPI strength would raise doubts about near-term cuts.

Strong retail sales would reduce the urgency for demand support.

Elevated oil prices would keep the inflation path vulnerable.

A tense Beijing summit would support the dollar through trade and geopolitical risk.

In that environment, a dovish signal from the incoming chair could backfire if bonds interpret it as political pressure or premature easing.

Bitcoin might initially respond to the idea of easier policy, but a rise in real yields and the dollar would likely cap that response.

Bitcoin’s macro test transmission map runs through real yields, the dollar, ETF flows, leverage, and reserves

Bitcoin enters the week near $81,000 after recovering from the high-$75,000s around the Apr. 29 FOMC period.

That rally improved the chart structure, but the next leg depends on whether macro variables confirm the move. The relevant channel is now broader than spot demand on crypto exchanges.

Bitcoin now trades through real yields, the dollar, ETF allocation flows, leverage conditions, and the same liquidity variables that shape equities and credit.

The first channel is rates.

A hot CPI print would likely lift nominal yields and real yields if markets conclude that the Fed has less room to cut. A cooler CPI print would likely ease that pressure, especially if core inflation softens alongside headline inflation.

The distinction is important because an energy-driven headline shock can produce an awkward signal.

Powell said after the Apr. 29 meeting that officials wanted to see progress beyond the energy shock and tariff effects before easing.

If April shows hot headline inflation with cooler core inflation, the market reaction may depend on whether Warsh signals patience, urgency, or a willingness to look through the oil impulse.

The second channel is the dollar.

CryptoSlate’s prior work on Bitcoin, M2, and dollar strength showed how a stronger dollar can interrupt the transmission from expanding global liquidity to BTC.

That remains the central macro risk. Bitcoin can benefit from easier policy expectations, but a rising dollar can offset that impulse by tightening global financial conditions.

This is why the Trump-Xi meeting sits inside the Bitcoin trade. Trade relief can soften the dollar and lower risk premia. Escalation can lift the dollar and pressure offshore liquidity.

The third channel is the Fed balance sheet and Treasury cash.

A Thursday H.4.1 release showing rising reserves and easing pressure from the Treasury General Account would give Bitcoin a stronger liquidity foundation.

A release showing reserve drain alongside a still-large Treasury cash pile would make any rally more dependent on ETF inflows and leverage.

CryptoSlate’s analysis of debt, liquidity, and Bitcoin has already shown that aggregate liquidity can look supportive while the usable liquidity reaching risk assets remains constrained.

Bitcoin’s next macro test runs through inflation data, Fed signals, liquidity, ETF demand, and geopolitical risk.

The next major Bitcoin move depends on whether macro test channels align

The fourth channel is institutional flow.

Since the launch of U.S. spot Bitcoin ETFs, BTC has become easier for traditional portfolios to buy, rebalance, and sell.

CryptoSlate’s coverage of the ETF-driven market-structure shift described how institutions have become a primary force in Bitcoin liquidity and price formation.

A separate analysis of passive money noted that U.S. spot Bitcoin ETFs had accumulated roughly $58.4 billion in cumulative net inflows by late April, with IBIT above $60 billion in net assets, reinforcing how far Bitcoin has moved into traditional allocation workflows through ETF wrappers.

That structure works in both directions.

ETF inflows can amplify a macro relief rally when yields fall, and the dollar weakens. ETF outflows can accelerate downside when real yields rise, the dollar strengthens, and leveraged traders are forced to reduce exposure.

A hot CPI and PPI sequence, strong retail sales, falling reserves, and a tense Trump-Xi outcome would be the most difficult mix for BTC because every transmission channel would point toward tighter financial conditions.

A cooler inflation sequence, resilient but slowing retail sales, improving reserves, and a less hostile China signal would give Bitcoin the strongest macro foundation it has had in 2026.

A cooler sequence would change the setup. Softer CPI and PPI would validate the idea that the March energy spike was passing through rather than embedding.

A slower but stable retail number would support a soft-landing path. A Thursday balance sheet release showing firmer reserves would improve the liquidity backdrop. A constructive Trump-Xi meeting would reduce the trade-risk premium and could weaken the dollar.

In that scenario, Warsh would have more room to define a gradual policy pivot without starting his tenure under immediate inflation pressure.

Bitcoin would then have a clearer path to test higher levels, provided ETF creations expand, and derivatives positioning avoids an unstable long build.

The mixed outcome may be the most realistic one.

Headline inflation can stay firm because of energy while core inflation cools. Retail sales can remain solid in nominal terms while real demand slows. The Fed balance sheet can show a large aggregate asset base while reserves remain under pressure. Trump and Xi can produce limited trade relief while leaving Taiwan, oil logistics, and tariff enforcement unresolved.

That mix would keep Bitcoin in a macro waiting zone. It would reward intraday volatility, but it would withhold the confirmation needed for a durable range expansion.

The next test is specific.

Watch Warsh’s first signals on inflation tolerance, balance-sheet policy, and central-bank independence.

Watch the June FOMC path, especially whether the statement language shifts after the leadership handoff.

Watch real yields and DXY before treating Bitcoin’s move as confirmation.

Watch H.4.1 reserves and the Treasury General Account before assuming liquidity has improved.

Watch spot ETF net flows, funding rates, and liquidation clusters before treating a breakout as structurally supported.

If those variables align, May 11-15 becomes the week Bitcoin regained a macro tailwind after months of rate, dollar, and oil pressure.

If they fail to align, the week becomes a sharper lesson in the post-ETF regime: Bitcoin can trade like a scarce asset, a liquidity asset, and an institutional risk asset at the same time.

The direction of the next major move will come from which identity markets choose after CPI, PPI, retail sales, H.4.1, Warsh, and Trump-Xi all hit the same window.

Deepfakes have shifted from a niche concern to a mass-market threat. May’s incidents show how consumer-grade tools now outpace any institutional response.

The damage extends into crypto. Scammers leverage artificial intelligence (AI) to create impersonation scams.

The Deepfake Economy Is Here, and Detection Is Losing

In early May 2026, AI-generated content showed up across politics, entertainment, and crime, as documented by Resemble AI.

FBI Director Kash Patel posted a video that appeared to use AI to generate shots nearly identical to those in the Beastie Boys’ “Sabotage” music video. Furthermore, an AI video of mayoral candidate Spencer Pratt drew 4.1 million views on X.

With President Trump’s leadership, this @FBI and our interagency partners are conducting massive fraud takedowns coast to coast – and we’re not stopping pic.twitter.com/lLAY4nSsQa

— FBI Director Kash Patel (@FBIDirectorKash) May 4, 2026

These tools aren’t just being used for viral content. They are also fueling real financial harm. A Chicago man lost $69,000 to a scammer who flashed an AI-generated US Marshals badge on a video call.

Meanwhile, the Atlantic’s Lila Shroff found that OpenAI’s ChatGPT Images 2.0 can generate fake IDs, prescriptions, receipts, bank alerts, and news screenshots.

“All of this makes it even harder for banks, hospitals, government agencies, and the like to prevent fraud,” Shroff wrote.

404 Media exposed Haotian AI, a Chinese real-time deepfake software. Reporter Joseph Cox swapped faces on a live Teams call using this, proving the technology is functional, for sale, and already being used against real victims.

“Three of this week’s stories, Haotian AI, the Meloni deepfake, and the Patel FBI video, come from completely different categories and geographies, but they share a structural condition: the tools used to produce the harm are consumer-grade, widely available, and improving faster than any institutional response. Haotian AI costs a few hundred dollars and works on Teams. ChatGPT Images 2.0 is a subscription product,” Resemble AI said.

Crypto Also Bears the Cost

Crypto has become a prime target for AI-driven deception. According to Chainalysis, fraudsters are now pairing deepfakes, face-swap apps, and large language models with classic romance and investment cons, and the math favors them.

The average AI-assisted crypto scam nets roughly $3.2 million, about 4.5 times the haul of a conventional scheme. Several cases underline the threat. In August 2025, attackers stole $2 million by impersonating the founder of Plasma.

BeInCrypto has also reported on North Korean operatives running deepfake video calls on Zoom. Together, these incidents mark AI-powered impersonation as one of the sector’s most pressing security risks.

The Trump administration’s Intel (INTC) stake has grown into a $28 billion paper gain after Intel surged to a fresh all-time high.

Back on August 22, 2025, Cryptopolitan reported that the U.S. government had bought a 10% holding in Intel at $20.47 a share, a position worth about $8.9 billion at the time.

Now, after a huge run in the stock, that U.S. position is sitting on a gain of about 315%.

On Friday, Intel surged by 28% and traded as high as $85.22, setting a new record for the stock. The rally pushed Intel to its strongest one-day performance since October 29, 1987. It also lifted the stock’s gain for the year to about 120%.

Intel also climbed 22.6% in another reading that took it above the peak it reached during the dot-com era in 2000. Truly just… outstanding!

Intel turns strong earnings into a market shock

Yesterday, Cryptopolitan reported that Intel saw $13.58 billion in revenue for the quarter, beating the $12.42 billion that Wall Street expected. Earnings per share came in at $0.29, far above the $0.01 forecast.

Revenue was also up 7.2% from the $12.67 billion that Intel reported a year earlier. For the next quarter, Intel said it expects revenue between $13.8 billion and $14.8 billion in the second quarter. Analysts had been looking for about $13 billion.

And then of course, we’ve got the whole matter of Tesla and SpaceX picking Intel’s 14A process for the Terafab AI chip project. That gives Intel an outside customer for a future manufacturing node that the market is watching closely.

At the same time, Intel’s Data Center and AI business posted year-over-year growth. Those two things landed together. The foundry build-out is still expensive and still one of the biggest financial variables in the Intel story, but the new customer link gave traders another reason to bet on Intel in the near term.

For a long stretch, Intel looked like it was losing ground in the fight for AI hardware demand. Other chip companies got most of the attention, and Nvidia led much of that run. But perhaps that money is now flowing back into Intel in a serious way.

Intel lifts the whole chip sector as AI spending keeps rolling

The rally did not stop with Intel. U.S. chip stocks surged to new highs on Friday after Intel’s stronger-than-expected forecast boosted confidence in the wider AI trade.

The Philadelphia Semiconductor Index rose 3.2% to a record and was on track for its 18th straight day of gains. The index is now up more than 47% this year.

That broader rise has been tied to the spending binge from major tech companies building more AI infrastructure. Chip names have been among the biggest winners from that wave of spending. The earnings outlook shows how wide the gap has become.

The semiconductor group is expected to post 109.2% earnings growth for the first quarter, based on LSEG data. The wider S&P 500 information technology sector is expected to grow earnings by 48.2%. Both numbers are strong, but the chip group is in a different league.

Other stocks joined the Friday jump. AMD climbed 13.7%. Arm gained 12%. Nvidia, now the most valuable company in the world, added 1.6%. Last year, a lot of the rally in chip names came from demand for Nvidia’s graphics chips, which are used to train large AI models on huge piles of data.

Earlier this year, many AI and other Big Tech stocks came under pressure. Investors started asking whether all the spending would really turn into better revenue, fatter margins, and stronger cash flow soon enough.

Even with that concern, valuations have cooled from earlier extremes. The S&P 500 tech index now trades at about 22 times forward 12-month earnings, down from about 31.8 last year. The Philadelphia Semiconductor Index was last around 26.6 times forward earnings, compared with about 20.7 times for the S&P 500.

Business activity picked up in April, but Americans are paying more for almost everything, and most say things are only getting worse.

The U.S. composite PMI is at 52.0 this month, a three-month high that suggests a slight recovery following a sluggish March, according to new data from S&P Global.

However, the average price of goods and services increased at its quickest rate since July 2022, a signal that should concern both consumers and legislators.

However, economists advise being cautious. Much of that growth came not from people actually buying more, but from companies rushing to stock up before prices climb further or supply chains buckle.

Surveys were filled with phrases like “panic buying” and “emergency buying,” language that points to fear, not confidence.

Services told a quieter story. The services PMI edged up to 51.3, but that is still the second-lowest reading of the past year. New orders barely grew.

Businesses and households across tourism, financial services, and other sectors are holding back spending. People are waiting to see what happens next, weighed down by geopolitical tensions and stretched budgets.

Supply chains under pressure

Supply chains are showing real strain. Delays from factory suppliers in April were the worst since August 2022.

Shipping difficulties related to continuing hostilities overseas account for a portion of that.

A portion of it stems from businesses purchasing excess inventory just to be safe, which further restricts supply and drives up costs.

The report’s pricing information is uncomfortable to read. Inflation in manufacturing products reached a ten-month high. The service sector’s price rises hit a 45-month high.

Input costs rose at their fastest rate in 11 months. Taken together, the inflation picture is getting harder to dismiss.

Regular Americans are feeling it. A new Fox poll found that 70% of respondents believe the economy is getting worse, up sharply from 55% a year ago.

Only 26% said conditions have improved. The pessimism cuts across party lines. Even among Republicans, 56% described the state of the economy as bad.

The consumer price index rose 3.3% in March, slightly above the level when he took office.

Roughly one in four Americans approves of how he is handling the cost of living. One major driver of that frustration is energy costs, pushed higher by the ongoing conflict with Iran.

That conflict is also shaping what comes next for the broader economy.

The prospect of gasoline hitting $5 a gallon is now a real concern for both the White House and the Federal Reserve.

For the Fed, the situation is getting harder to navigate.

Chris Williamson, chief business economist at S&P Global, said that if inflation keeps moving in the direction the PMI data suggests, it becomes much harder for the central bank to make a case for cutting interest rates.

The gap between what the numbers show and what people feel is hard to ignore. A manufacturing PMI of 54.0 normally signals solid growth.

However, rather than being motivated by actual customer demand, this reading is being driven by defensive actions taken by businesses to create buffers against uncertainty.

There might not be enough actual demand to sustain the trend when stockpiling eventually decreases.

For the time being, the Fed is torn between an economy that appears to be doing well and inflation that is being driven up more by fear than by growth.

Any discussion of rate cuts will remain firmly on hold until that changes.

Despite a new chip challenge from Google and a billion-dollar contract loss hitting one of its key suppliers, Nvidia remains the dominant force in artificial intelligence hardware, with fresh deals in the UK, China, and the automotive sector reinforcing that position.

Wall Street research firm TD Cowen reaffirmed its buy rating on Nvidia this Thursday, brushing aside concerns raised by Google’s Wednesday announcement of new AI training and inference chips.

The firm said it continues to see Nvidia as “the market leader in terms of performance and breadth of software ecosystem.”

The endorsement came as Nvidia announced a string of new partnerships across multiple industries on the same day.

BT will provide the connectivity needed to handle rising compute demand. The project extends BT’s business platform to offer new AI services to both the private and public sectors.

Use cases include AI-powered analysis of sensitive healthcare data, as well as applications in energy, finance, and security.

On the automotive front, Nvidia and Chinese company Desay SV are set to jointly unveil a new intelligent driving solution at the Beijing Auto Show.

The system is built on Nvidia’s DRIVE AGX Thor computing platform and uses NVLink interconnect technology, which links two AGX Thor chips together.

The combined setup delivers a maximum computing power of 4,000 FP4 TFLOPS and is designed to tackle the technical challenges of building Level 3 and Level 4 autonomous vehicles, cars that can largely or fully drive themselves under specific conditions.

The system runs entirely on edge-side computing, meaning it does not rely on the cloud to function.

According to the companies, this approach improves real-time performance, data security, and overall reliability, making it suitable for both highway and urban driving.

Supply chain troubles mount

While Nvidia’s partnerships continue to grow, trouble is brewing in its supply chain. Shares of Super Micro Computer fell 10% on Thursday after reports surfaced that the company lost a major contract with Oracle for Nvidia’s GB300 NVL72 server racks.

A report from research firm Bluefin said Oracle canceled an order for between 300 and 400 racks, wiping out a contract worth between $1.1 billion and $1.4 billion for Super Micro.

Bluefin, citing industry sources, said the cancellation is believed to be connected to a lawsuit against Super Micro’s co-founder over the alleged smuggling of AI graphics processors to China.

Bluefin also reported that Wistron NeWeb is believed to have taken over the racking business that Super Micro lost.

At the same time, sources within the supply chain flagged concerns about a build-up of unsold B200 GPU inventory, describing the levels as “considerable.”

The accumulation is being linked to a shift in demand.

Buyers have moved away from B200 hardware toward the newer GB200 NVL72 racks, and the contracts for those were awarded to Dell and Hewlett-Packard Enterprise, not Super Micro.

As Nvidia pushes further into sovereign infrastructure, self-driving technology, and financial services, keeping its hardware moving through the right hands is becoming just as important as building it.

So Wall Street is betting on Nvidia’s software strength, but overlooking real cracks in its supply chain.

The buy rating assumes these problems will sort themselves out. That is not guaranteed. Unsold chips and contract shuffles signal growing pains.

The real test is whether Nvidia can get its own operations under control before rivals move in.

Defiance ETFs has filed a preliminary prospectus with the SEC for the Defiance US AI Resilience ETF. The passively managed fund is designed to hold companies least likely to be disrupted by artificial intelligence (AI).

The filing, submitted on Thursday, marks Defiance’s latest thematic bet. Rather than chasing AI upside, this fund takes the opposite approach by targeting old-economy businesses that AI is unlikely to replace.

What the AI Resilience ETF Holds

The ETF will track the VettaFi US AI Resilience Index. The index selects roughly 50 US large-cap companies from VettaFi’s broader equity universe. It focuses on what the industry has labeled “HALO” firms, short for Heavy Asset, Low Obsolescence.

These are businesses with inelastic demand, long-life physical infrastructure, and revenue profiles insulated from labor automation.

Under normal conditions, the fund will invest at least 80% of net assets in companies that meet these AI-resilience criteria. It may use either full replication or representative sampling to track the index.

The HALO Thesis Behind the Fund

The ETF arrives as Wall Street’s appetite for HALO stocks continues to grow. Goldman Sachs introduced the framework in early 2026.

The firm found that capital-intensive companies relying on physical assets have outperformed capital-light, digital-first peers by about 35% since the start of 2025.

The reasoning is straightforward. Transmission grids, pipelines, industrial capacity, and transport infrastructure are costly to replicate and sit outside the reach of generative AI.

Software companies, by contrast, face growing displacement risk as AI systems automate more of their functions.

Defiance, which manages over $8 billion in assets, already operates thematic funds covering quantum computing, AI power infrastructure, and drone automation.

Its Quantum Computing ETF (QTUM) recently passed $4 billion in AUM with a 5-star Morningstar rating. The AI Resilience ETF extends that lineup into contrarian territory.

Congratulations to @Defiance_ETFs on their Quantum Computing #ETF – $QTUM – Surpassing $4 Billion in Assets and Earning a 5-Star @MorningstarInc Rating!@MarketVector is proud to be the administrator of $QTUM‘s benchmark, the #BlueStar Machine Learning and Quantum Computing…

The prospectus is still preliminary. The ticker has not been assigned, and management fees are listed as placeholders. The fund will trade on Nasdaq once the filing becomes effective, which typically takes about 75 days.

Principal risks highlighted in the filing include interest-rate sensitivity for capital-intensive holdings and sector concentration in staples and industrials.

Penserra Capital Management will handle day-to-day portfolio management through a sub-advisory arrangement.

The actual portfolio managers are Dustin Lewellyn, Ernesto Tong, and Christine Johanson, all from Penserra.

The filing is available on SEC EDGAR under ETF Series Solutions. With AI hype dominating markets in 2026, Defiance is betting that investors will also pay for protection against the other side of that trade.

One of the top prediction market platforms in the nation has partnered with a cryptocurrency-focused investment firm to provide a unique research service based on real-time crowd-driven data.

In order to provide a research product focused on prediction market data, ProCap Financial, led by cryptocurrency entrepreneur Anthony Pompliano, revealed on Tuesday that it has partnered with Kalshi, a regulated prediction market exchange.

The service will generate analysis on stock trends, investment ideas, and general economic conditions by combining ProCap’s artificial intelligence tools with Kalshi’s data flow.

Due in large part to the 2024 U.S. presidential election, which caused a dramatic increase in trading volumes and users, prediction markets have evolved from a little-known area of finance to a frequently used instrument.

People purchase and sell contracts linked to the results of upcoming events on these platforms.

Kalshi’s contracts specify an event, potential outcomes, the compensation for each outcome, and the contract’s expiration date.

Proponents contend that compared to conventional opinion polls, prices on these markets more accurately represent public expectations.

That platform uses AI tools to sift through large amounts of data, stress-test findings through automated debate between AI systems, and produce written research reports.

Under the new arrangement, ProCap Insights will publish reports covering individual prediction markets, platform-wide trends, data-based trading strategies, contracts that appear mispriced, and reports built directly from Kalshi’s data.

“Kalshi Research’s prediction market data paired with our AI agents is a powerful combination,” said Anthony Pompliano, Chairman and CEO of ProCap Financial. “Independent investors have never had access to a research engine like this. By combining real-time market signals with AI-driven analysis, we’ll deliver sharper insights to help investors make smarter decisions in the growing industry of prediction markets.”

One of the features that sets prediction markets apart from conventional investing is their precision.

Instead of shifting a portfolio around to prepare for a possible recession, a trader can bet directly on whether a recession happens.

The same logic applies to specific pieces of corporate data.

A trader can take a position on Tesla’s vehicle delivery numbers without buying the whole stock and absorbing the full risk of an earnings report.

“Prediction markets turn uncertainty about real-world events into actionable signals,” said Tarek Mansour, co-founder and CEO of Kalshi. “We’re partnering with ProCap Financial to bring wisdom-of-the-crowds intelligence directly to financial research, so both retail and institutional investors can benefit from this data and analysis.”

Research from Kalshi found that its markets outperformed Wall Street consensus forecasts by 40% across various timeframes and conditions, and matched or beat analyst forecasts on 85% of inflation data releases a full week before the numbers came out.

A shifting regulatory landscape for prediction markets

As a first step toward a comprehensive regulatory framework for prediction markets, the CFTC released a formal notice requesting public input four days later, on March 16.

David Miller, the CFTC’s new enforcement chief, listed insider trading, market manipulation, and retail fraud as the agency’s top priorities.

He also introduced a strategy that encourages businesses to promptly report issues and take corrective action.

Kalshi currently has open markets running on where the S&P 500 will close today, which direction SPY moves on April 21, and a range of short-term economic and political questions, the kind of live data that ProCap’s tools will now turn into research for subscribers.

If you want a calmer entry point into DeFi crypto without the usual hype, start with this free video.

Nvidia’s share price fell to $199.86 on Monday, a drop of less than 1%. On its own, that barely registers. But zoom out, and the picture looks more complicated. Google is coming for Nvidia’s fastest-growing market, billions of dollars are flowing into rivals, and a South Korean startup just raised $400 million with Nvidia squarely in its sights.

Nvidia closed at $199.48, down 0.79% on the day. The stock still sits well above its 20-day, 50-day, and 200-day moving averages, which are clustered around $181-$183, so the longer-term trend remains intact.

The MACD is still flashing a buy signal, and the ADX reading of 15.28 points to a weak but continuing upward trend.

Google takes aim at Nvidia’s fastest-growing market

While Nvidia’s stock treads water, Google is making its most direct push yet into the chip market.

The Alphabet-owned company is preparing to announce a new generation of tensor processing units, known as TPUs, at its Google Cloud Next conference in Las Vegas this week, with a focus on inference: the process of running AI models once they have already been trained.

“It now becomes sensible to specialize chips more for training or more for inference workloads,” Google Chief Scientist Jeff Dean said. The company is “looking at a whole bunch of different things,” he added, including how fast it can deliver AI results to users.

Big names are now in for the TPUs. Anthropic has signed a contract for 1 million TPU’s while Meta is using them through Google’s cloud as part of a multi-billion-dollar agreement. In the upcoming Google conference, Citadel Securities will be talking about how TPU’s are faster at training models than GPUs. This isn’t where it ends. Abu Dhabi’s G42 is also in discussion to access them.

Google is also loosening the rules around TPU access, letting some customers run the chips inside their own data centers and supporting outside tools like PyTorch, rather than locking users into Google’s own software stack.

Not to forget, OpenAI is also growing frustrated by Nvidia’s inference hardware and looking for alternatives, as reported by Cryptopolitan previously.

Billions are flowing into chip startups

Google is not the only one sensing an opening. AI chip startups pulled in $8.3 billion globally in 2026, according to data from Dealroom, putting the sector on track for a record year. In the U.S., Cerebras raised $1 billion in February. MatX, Ayar Labs, and Etched each secured $500 million rounds. In Europe, Axelera and Olix both raised over $200 million.

“It’s no longer a niche bet,” said Carlos Espinal of European VC firm Seedcamp. “It’s becoming a core part of how people think about AI infrastructure.”

Samsung-backed South Korean startup Rebellions raised $400 million at a $2.34 billion valuation, led by Mirae Asset Financial Group and South Korea’s state-backed National Growth Fund. The company has raised $650 million in the past six months alone, more than 75% of its total funding, and is now targeting U.S. customers and preparing for a public listing.

Its Rebel100 chip is built specifically for inference.

One constraint is memory. High-bandwidth memory is tight across the industry, and prices have risen sharply. “Memory is not very easy to get. But our demand is so huge,” Park said. Rebellions has an edge there: both Samsung and SK Hynix are investors, giving it better access than most rivals.

The crypto card with no spending limits. Get 3% cashback and instant mobile payments. Claim your Ether.fi card.

The numbers are in, and they are not pretty for everyday traders who bet on prediction markets.

Despite handling tens of billions of dollars in trades, these platforms appear to be leaving the overwhelming majority of users worse off financially.

Prediction markets have grown fast. By 2025, platforms like Polymarket and Kalshi were processing $28 billion in trading volume.

The idea behind them is simple: people bet on future events, and the odds that form are supposed to reflect what the public genuinely believes will happen.

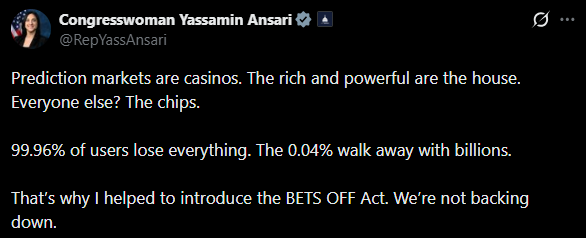

Arizona Democrat Yassamin Ansari recently targeted both Polymarket and Kalshi, calling them “casinos where the rich and powerful are the house and everyone else is the chips.”

She posted on X that 99.96% of users lose everything while the top 0.04% walk away with billions.

Ansari slams the prediction market as a rigged casino Source: @RepYassAnsari

Her claim comes from a December 2025 on-chain analysis by a blockchain researcher known as DeFi Oasis.

That study found that less than 0.04% of Polymarket wallet addresses captured more than 70% of all realized profits, totaling $3.7 billion.

Analysts, however, pointed out that Ansari’s wording mixes up two separate figures. The 0.04% refers to who captured most of the winnings, not simply who won anything at all.

Ansari is co-sponsoring a bill called the BETS OFF Act alongside Sen. Chris Murphy of Connecticut and Reps. Greg Casar and Rashida Tlaib of Texas and Michigan, respectively. The bill would ban betting on events like war, terrorism, assassination, and government decisions.

Whatever the exact interpretation of the 0.04% figure, more recent data puts the problem in sharper focus.

The sharp drop, according to Sergeenkov, is tied to a flood of new and inexperienced users drawn in by the buzz around the November 2024 U.S. presidential election. “Less experienced users tend to trade less successfully,” he noted.

The 84.1% figure is also higher than what a 2025 study from researchers Felix Reichenbach and Martin Walther found.

Their paper put the losing share at around 70%. The difference, Sergeenkov explains, comes down to how the math is done.

His method accounts for wallet splits and merges, which earlier analyses left out. “When splits are left out, an address looks more profitable because one category of expenses is simply invisible,” he said.

The numbers behind the losses

A deeper look at the data shows just how rare meaningful earnings are on these platforms. Of 2.5 million wallets studied, only 2% had ever made more than $1,000 in total. Just 0.32% had cleared $10,000, and only 840 wallets, that is 0.033%, had earned more than $100,000.

The average trade on Polymarket is $89, and 80% of traders never place a bet larger than $500 on average.

The idea of replacing a regular paycheck through trading appears almost out of reach. The average monthly salary in the United States is roughly $5,000. Only 0.98% of traders ever hit that mark in a single month.

The number who managed it for 12 months straight: just 35 out of 2.5 million people.

The findings carry weight at a time when major financial institutions have moved in.

The Intercontinental Exchange, which owns the New York Stock Exchange, completed a $2 billion deal with Polymarket in March. Kalshi recently raised $1 billion, pushing its valuation to $22 billion.

The BETS OFF Act and a separate bill called the Death Bets Act, introduced by Rep. Mike Levin, are not widely expected to pass in the current Congress. Still, observers say the push for stronger protections for everyday users is not going away.