Strategy, the largest corporate holder of Bitcoin, recorded the largest unrealized loss on its BTC holdings of over $10 billion in paper value. This reflects a 17% decline in the value of its position after years of steady accumulation.

The loss comes amid a broader market downturn as Bitcoin crashed to around $61,000 today. The apex coin is now down about 28% year-to-date, marking its weakest level since February.

Strategy Logs $10.47B Paper Loss

The company’s latest portfolio snapshot shows total invested capital at about $63.87 billion against a current valuation of $53.4 billion. This leaves a gap of about $10.47 billion in unrealized losses, alongside a smaller realized loss linked to recent portfolio activity. The figures highlight the continued pressure on its Bitcoin-heavy balance sheet after years of accumulation.

That pressure has also coincided with a notable change in its long-standing approach to Bitcoin holdings. The firm sold 32 BTC at an average price of $77,135 per coin, marking its first departure from a previously consistent no-sell stance.

According to a filing with the Securities and Exchange Commission, the sale took place between May 26 and May 31 and generated about $2.5 million. The proceeds are expected to support preferred stock distributions, including cash dividend obligations.

Broader market impact is also visible in the company’s equity performance. Strategy stock (MSTR) has declined about 77% from its peak, reflecting sensitivity to Bitcoin’s price movements and balance sheet exposure.

Over the same six-year period of sustained Bitcoin accumulation, the S&P 500 gained roughly 116%. This contrast underscores a widening performance gap between traditional equity benchmarks and firms with concentrated Bitcoin exposure.

Holding Through the Downturn

Executive Chairman Michael Saylor built the company’s Bitcoin strategy in 2020 by converting corporate reserves into digital assets as an inflation hedge. The firm maintains that it will continue holding BTC despite losses, with its strategy focused on long-term exposure rather than short-term stability.

Market observers say the unrealized loss highlights how Bitcoin price swings directly affect corporate balance sheets tied to digital asset exposure. They remain divided on whether the strategy amplifies volatility compared with diversified portfolios during extended downturns.

Michael Saylor conceded that the recent Bitcoin selloff reflects a rotation of capital toward AI rather than weakness in the pioneer crypto itself.

He pointed to roughly $4 billion in Bitcoin ETF outflows since May 14, with the king of crypto trading near $64,000 at the time, down about 4% on the day and nearly 49% below its October 2025 record.

Analysts peg 2026 capital budgets at the largest US tech firms above $600 billion. That scale gives his rotation argument some footing.

He cast the ETF redemptions as temporary repositioning, not a structural problem. MicroStrategy holds 843,706 Bitcoin at an average cost near $75,702, per Strategy’s record Bitcoin holdings.

That average now sits well above the market price. With Bitcoin near $64,000, the 843,706 coins are worth about $54 billion against a cost basis near $63.9 billion.

That leaves MicroStrategy about $10 billion underwater on the largest corporate Bitcoin treasury. The loss is unrealized, yet it pressures a stock that trades as a leveraged proxy for the token.

The strain is already visible. A June 1 filing shows Strategy sold 32 BTC to fund preferred-stock dividends, its first sale since 2022. The move was small, yet it showed those obligations now drawing on the same balance sheet.

“Capital markets are funding the AI buildout at historic scale: ~$400B over 6 months. Bitcoin ETFs have seen ~$4B of outflows since May 14, pressuring $BTC. This is a capital rotation, not a Bitcoin impairment. Volatility creates opportunity,” Michael Saylor indicated.

The framing carries an irony, give Michael Saylor rode the same dot-com wave that once broke his company.

MicroStrategy peaked at $333 on March 10, 2000, the day the Nasdaq Composite also topped out. The stock then fell from $260 to $86 on March 20, a one-day drop above 60%.

MicroStrategy (MSTR) Stock Performance in 2000. Source: TradingView

That restatement erased about $66 million in revenue and turned reported profits into losses. Saylor and two executives later paid roughly $11 million to settle fraud charges, without admitting wrongdoing.

Analysts at PFR Capital now explore a possibility where Saylor could rattle markets again.

“In March 2000, MicroStrategy…changed its revenue recognition method…investors started doubting the revenue, profits, accounting quality, and so on of other companies. What happened after that, everyone knows. So you could say MicroStrategy single-handedly crashed the entire market. 26 years have passed. Will MicroStrategy be able to replay its market-crashing magic? Let’s wait and see,” PFR Capital’s Jayson Hu posed.

The parallel is imperfect, however, since the 2000 collapse stemmed from accounting. The current bet rests on transparent, on-chain purchases.

— The Kobeissi Letter (@KobeissiLetter) June 4, 2026

Competing Reads on the Outflows

However, not everyone shares Saylor’s calm. CNBC’s Mad Money host Jim Cramer weighed in as the selling spread. He had touted doomed “new economy” stocks days before the 2000 top.

“Saylor suboptimal move roiling Crypto. Some wags pondering it was only up in the 90s because of Saylor… Seems extreme but it is all i hear,” he noted.

Bloomberg analyst Eric Balchunas described the stretch bluntly, while noting lifetime ETF inflows still top $55 billion. May marked the heaviest Bitcoin ETF outflows of 2026.

BAD TIMES: Bitcoin ETFs in a big step back mode.. $4.4b out over past month which sent the YTD number negative again (it had worked hard to get positive too). That said, some silver lining: $IBIT & a few others STILL positive YTD (unreal) and total net lifetime is still +$55b… pic.twitter.com/VzaijnWhx8

Strive (NASDAQ: STRV) purchased 2,500 Bitcoins between May 23 and June 1 for approximately $185.2 million, bringing the company’s treasury to 19,000 BTC

The 2,500 BTC purchase was funded almost entirely through the company’s Variable Rate Series A Perpetual Preferred Stock (SATA), with an average cost of about $74,092 per coin.

Is Strive still buying BTC?

An SEC 8-K filing confirmed that Strive raised most of the money used for its most recent Bitcoin purchase through its SATA stock. The company issued 1,754,188 new shares that generated approximately $175.4 million. The remaining $9.8 million came from selling Class A common stock (ASST).

The average price Strive paid per coin was $74,092, which is lower than its previous purchase when it bought 1,109 BTC at about $76,989 per coin. During the latest purchase window, Bitcoin traded below $71,000 at certain points, meaning the treasury firm bought during a price drop.

Strive’s holdings have risen from 16,500 BTC to 19,000 BTC, representing a 15.2% increase in total holdings over a single reporting period. The CEO, Matt Cole, disclosed the deal on X, adding that the company has a quarter-to-date BTC yield of 23.0%, a year-to-date yield of 36.7%, and an amplification ratio of 57.0%.

The 8-K filing also shows cash and equivalents rising from $93.3 million to $137.3 million, even after Strive spent $185 million on Bitcoin. Strive raised about $229 million total from both equity instruments, and the company stated that the higher cash balance helps it maintain an 18-month dividend reserve for SATA holders.

Strategy’s rare Bitcoin sale

Strategy (NASDAQ: MSTR), the largest corporate Bitcoin holder at 843,706 BTC, disclosed that around the same time as Strive’s purchase, it had sold 32 Bitcoins for $2.5 million to fund dividend payments on its own preferred stock, STRC. This is the second time Strategy has ever sold any of its Bitcoin holdings.

Michael Saylor, Strategy’s executive chairman, responded to Cole’s announcement regarding the Bitcoin purchase with a brief endorsement on X, posting “@Strive for Bitcoin.”

Cole previously announced that Strive expects to increase the size of its at-the-market programs by $2.1 billion each for Class A shares and SATA, which would bring total ATM capacity to approximately $5.15 billion. However, the expansion requires amended SEC filings and a certificate of amendment for SATA.

Strive plans to change SATA‘s current dividend payouts from a monthly to a daily basis beginning June 16, in order to smooth out the concentrated buying pressure that currently builds ahead of each monthly ex-dividend date, and potentially reduce the periodic pauses in Bitcoin accumulation that observers have noticed.

Don’t just read crypto news. Understand it. Subscribe to our newsletter. It’s free.

Michael Saylor’s Bitcoin 2026 Keynote — CCS Exclusive

CCS Exclusive · Keynote Coverage

Michael Saylor Keynote:

The Birth of Digital Credit

Michael Saylor took the Bitcoin 2026 stage to declare that a new era in capital markets has begun — and that Strategy’s STRC has already become the most liquid preferred stock on Earth.

By CCS Editorial Desk · Bitcoin Conference 2026

Exclusive Analysis

STRC

“Digital credit is a killer application of Bitcoin. We expect to sell tens of billions — then hundreds of billions — then trillions of dollars of digital credit.”

— Michael Saylor, Bitcoin 2026

Full Keynote · Courtesy of Bitcoin Magazine

STRC by the numbers — as presented at Bitcoin 2026

$8.5BAUM

Reached in under 9 months, making STRC the world’s largest preferred stock

11.5%Yield

Tax-deferred dividend — equivalent to ~24% in a high-tax city like New York

2.7×Sharpe Ratio

5× better than the best competing credit instrument; beats Nvidia’s 1.89

$38BRun Rate

April demand annualized — from zero in under twelve months

Chapter I · The Big Idea

Engineering Credit the Way Satoshi Engineered Money

Michael Saylor opened his keynote at Bitcoin 2026 not with a price prediction but with an architectural argument. Just as Satoshi Nakamoto assembled proof-of-work, public-key cryptography, and peer-to-peer networking into ideal capital — a non-sovereign, bearer store of value without counterparty risk — Saylor claims to have done the same for credit.

The vehicle is STRC, the perpetual preferred equity issued by Strategy. Its building blocks are, individually, unremarkable: listed public companies, preferred equity structures, monthly variable dividends, return-of-capital tax treatment, shelf registrations, and ATM programs. Each has existed for decades or longer. The breakthrough, Saylor argues, was the combination — marrying them to a Bitcoin balance sheet to produce what he calls digital credit: liquid, transparent, homogeneous, accessible to any retail account, and carrying no fee.

“Bitcoin represents ideal capital,” he told the crowd. “Digital credit is ideal credit. We engineered it the same way.”

“The world’s built on capital. The world runs on credit. Our company strategy converts capital into credit.”

Chapter II · Stripping Risk from a Volatile Asset

How You Extract an 11% Yield from a 40-Volatility Asset

The mathematics Saylor presented are deliberately simple. Bitcoin has compounded at roughly 38% per year over the past five years — far above gold at 16%, real estate at 6%, or money markets at 3%. Since you cannot pay a credit dividend higher than the expected return of the underlying capital, those asset classes impose a ceiling on what any asset-backed credit product can yield. Bitcoin’s ceiling is the highest of any mainstream asset.

Strategy’s approach is to over-collateralize: at 4-to-1 or 5-to-1 collateral ratios, Bitcoin would need to fall 80% before a credit investor loses a dollar of principal. The capital investor absorbs all of that downside; the credit investor sits safely behind them. Volatility — Bitcoin’s notorious 40-point swings — is mathematically stripped away when you target a par value and pay out only the first slice of return.

In Saylor’s framing, the instrument performs “signal processing on a financial signal.” The first 11% of expected return goes to STRC holders. Everything above that — the excess volatility, the excess return — flows to the common equity. Three distinct products emerge from one underlying asset: digital capital (Bitcoin), digital credit (STRC), and digital equity (Strategy common stock).

Chapter III · A Product That Didn’t Exist

The Largest Preferred in the World — Before Its First Birthday

Saylor displayed a chart of the ten largest preferred stocks globally. STRC sits atop a list that includes preferred issues from Wells Fargo, Bank of America, JPMorgan, and Fannie Mae. Many of those instruments, he noted, are effectively impossible for retail investors to find, let alone trade — some are legally restricted to institutional buyers, and their tickers are nearly ungoogle-able.

STRC is not merely the largest. By Saylor’s presentation, it is 25× more liquid than the next-best preferred stock, turning over roughly 4.5% of its AUM in daily trading volume. Liquidity has grown by a factor of eight in five months. At the time of the conference, daily liquidity was approaching $400 million.

Instrument

Sharpe Ratio

Est. Yield

Liquidity

Tax Treatment

STRC(Strategy)

2.7

11.5%

~$400M / day

Return of capital (deferred)

Nvidia (NVDA)

1.89

—

Very high

Capital gains / ordinary

Top bank preferreds

~0.5

5–7%

Low–moderate

Qualified dividend

Private credit funds

<0.5

8.5%

Illiquid

Fully taxable

Money markets

Negative

3–4%

Daily

Fully taxable

S&P 500 Index

<1

1–2% div

Very high

Qualified dividend

Chapter IV · The Comeback of Preferred Capital

A 100-Year Gap, Closed

One of the more historically grounded passages in Saylor’s keynote was his argument that STRC represents less of an innovation and more of a revival. In the 19th century, preferred stocks financed the railroads and much of the early industrial revolution, comprising as much as 20–40% of corporate capital structures. Over the course of the 20th century, preferred equity fell out of use. Regulatory changes, tax policy, and the rise of bond markets pushed them to the institutional margins.

“Now in the 21st century,” Saylor said, “we’ve reintroduced the idea of preferred credit back into the capital markets.” The difference, he argues, is that this time the underlying collateral is not railroad track or factory equipment — it is Bitcoin, the highest-performing asset class of the last decade.

The shelf registration innovation amplifies this point. Before Strategy began issuing digital credit instruments, the largest shelf registration ever executed on a credit instrument globally was $500 million. Strategy has now filed a $21 billion shelf registration for STRC alone — a figure roughly 40 times the previous world record, according to Saylor.

Chapter V · Adoption and the Three-Million-Household Mark

From Institutional Indexes to Robin Hood Retail

Saylor’s growth numbers border on the incredible. Monthly demand for STRC fell to roughly $80 million in February during a sharp Bitcoin drawdown, then surged to $1.5 billion in March and $3.5 billion in April — a monthly demand run rate that annualizes to $38 billion. “How many products in the world,” he asked, “went from zero to $20 billion a year in their first year? There aren’t many.”

Adoption is broad. By Saylor’s count, roughly 80% of STRC is held in retail accounts — more than 120,000 distinct accounts, across E*Trade, Robinhood, Fidelity, and Charles Schwab. He estimates that approximately three million households are currently benefiting from the instrument.

Institutional adoption is accelerating in parallel. BlackRock and Van Eck, two of the largest credit fund managers in the world, both hold STRC as the third-largest position in their respective credit indexes, representing 2–6% of fund assets. As money flows into those indexes, it flows into STRC — and from there, into Bitcoin. Additionally, 21Shares has already launched an STRC-embedded ETF in Europe, while Strive is preparing a U.S.-listed digital yield fund.

Chapter VI · The Layer 3 Vision

Stable Coins, Streaming Dividends, and the $200 Trillion Endgame

The second half of Saylor’s keynote zoomed out to what he calls the “Layer 3” opportunity. If Bitcoin is Layer 1 (the capital asset) and STRC is Layer 2 (digital credit), then Layer 3 is the ecosystem of products built on top: tokenized STRC, ETFs, bank accounts, stable coins, and private funds that use STRC as their yield engine.

He described companies already building in this space — Apex, Saturn, and Hermetica — all constructing Bitcoin-backed yield products or stablecoin-backed yield products on top of Strategy’s infrastructure. Tokenized STRC grew from nothing to over $200 million in just four weeks, and Saylor said he expected it to cross $1 billion in AUM within weeks.

As a concrete near-term move, Saylor announced that Strategy would seek shareholder approval to shift STRC from monthly to semi-monthly dividend payments. The physics analogy he employed was apt: doubling the frequency of a signal takes it an octave higher — higher fidelity, tighter oscillation, lower volatility. If approved, the first semi-monthly dividend payment would arrive July 15th, making STRC the only stock in the world paying a semi-monthly dividend out of roughly 24,000 publicly listed companies.

The long arc of Saylor’s vision: drive Bitcoin to $10 million per coin, build a $200 trillion network, and give every person on Earth access to a high-yield digital savings account yielding 8–10% annually. “Fix the money, fix the world,” he concluded. “Digital credit is the next killer application to fix the money.”

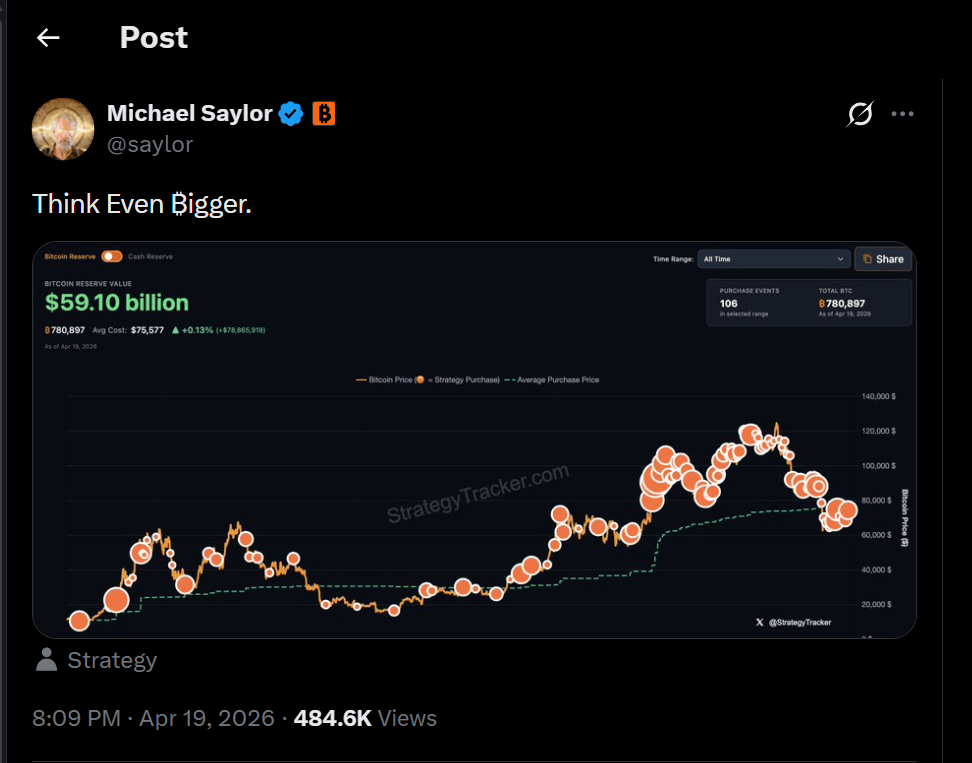

Michael Saylor’s company has already lined up the money. Now the question is how much Bitcoin it plans to buy with it.

Saylor’s Signal Fires Up The Market

Strategy’s executive chairman posted his well-known “Orange Dots” chart on X over the weekend, adding just three words: “Think even Bigger.”

The chart maps every Bitcoin purchase the company has ever made. In crypto circles, its appearance has become a reliable preview of an imminent acquisition announcement — and Monday is the day Strategy most commonly makes those announcements public.

The post landed after a string of major purchases. On April 13, Strategy spent $1 billion on Bitcoin. The week before that, it dropped $330 million.

Both buying rounds were preceded by the same chart. This time, Saylor’s caption suggests the next move could top them both.

A War Chest Already Sitting Ready

The fuel for that purchase appears to already be in place. Strategy’s STRC instrument has raised enough capital to fund up to $1.76 billion in Bitcoin acquisitions, based on reports tracking the company’s fundraising activity.

The company routinely uses proceeds from STRC to bankroll its Bitcoin buying program, so the timing of that capital raise lines up with the weekend post.

At the time of writing, Strategy holds 780,897 Bitcoin across its corporate treasury. The company’s average purchase price sits at $75,577 per coin.

At current market prices, the entire stash is valued at roughly $58 billion — a figure that would shift significantly with any large new purchase.

Bitcoin Price Holds Flat Despite The News

The market has not moved much on Saylor’s hint. Bitcoin was trading around $75,500, down less than 1% in the 24 hours following the post.

Geopolitical pressure has been a drag on price action, with US President Donald Trump accusing Iran of violating ceasefire terms — a development that has kept risk appetite subdued across financial markets.

One signal watched closely by analysts did break out over the weekend, though. Bitcoin Dominance — the share of total crypto market value held by Bitcoin — pushed above a key resistance level on the three-day chart, clearing a descending trendline it had been stuck under for some time.

Reports from crypto analysts indicate that if the breakout holds, more capital could rotate into Bitcoin at the expense of smaller coins.

For Strategy’s playbook, that kind of market shift would not be unwelcome.

Featured image from MetaAI, chart from TradingView

The corporate Bitcoin treasury boom is losing oxygen: a $100 billion public-company bet has shrunk, buying has collapsed outside Strategy (formerly MicroStrategy), and the financing model that drove the trade is starting to fail.

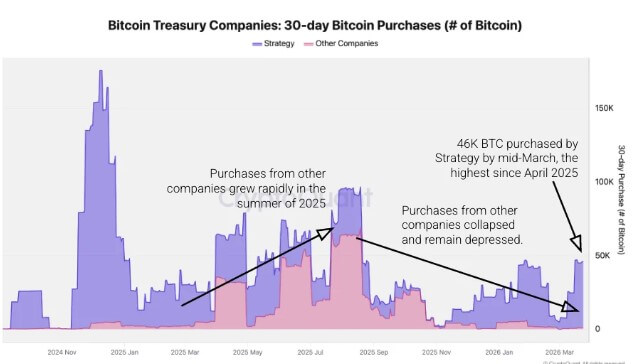

Data from CryptoQuant show that the Michael Saylor-led company bought about 45,000 Bitcoin over the last 30 days, the largest 30-day haul since April 2025.

Over the same period, all other Bitcoin treasury companies combined purchased about 1,000 Bitcoin, down about 99% from the 69,000 BTC they bought at the peak of the trade in August 2025.

CryptoQuant noted that the gap has widened to the point that Strategy now accounts for about 98% of all Bitcoin bought by treasury firms over the past month.

Last October, the balance looked very different, with companies outside Strategy responsible for about 95% of net purchases during a period when corporate buying was spreading across a wider list of names.

That shift has left Strategy as the dominant source of incremental treasury demand in a sector that, only months ago, was being promoted as a broader corporate movement tied to Bitcoin’s rally and to publicly listed companies’ ability to use their stocks as financing tools.

Participation shrinks beyond Strategy

The slowdown outside Strategy is showing up not only in the size of purchases but also in the number of companies still participating.

Treasury companies other than Strategy made 13 Bitcoin purchases in the last 30 days, down 76% from the 54 recorded in August 2025, when corporate activity was at its peak. Strategy, by contrast, has maintained a steadier pace, posting about 4 to 5 purchases each 30-day period.

The numbers point to a market where both the depth and breadth of demand have weakened. Fewer companies are buying, and those that remain active are deploying less capital than they did during the peak of the trade.

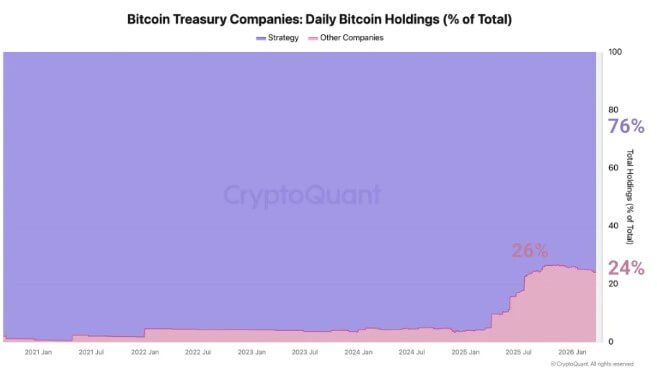

That change has altered the makeup of the sector. While Strategy’s total Bitcoin holdings have grown by about 90,000 Bitcoin so far this year, other treasury companies together have added a net 4,000 Bitcoin over the same period.

As a result, their share of total corporate treasury holdings has slipped from 26% in November 2025 to 24% now, while Strategy’s share has continued to climb.

Strategy now holds about 76% of all Bitcoin owned by treasury companies. The next two largest holders, XXI and Metaplanet, account for 4.3% and 3.5%, respectively.

For a sector that expanded quickly as rising Bitcoin prices pulled in new entrants, the concentration is becoming harder to ignore.

The corporate treasury model gained momentum last year as Bitcoin rose and public-market investors rewarded listed companies that offered leveraged exposure to the asset.

As Bitcoin climbed, many companies were able to issue shares at premiums to the value of the BTC already on their balance sheets.

That gave them a way to raise capital, buy more Bitcoin, and, in some cases, widen the gap between their market value and the underlying value of their holdings. Notably, some also used debt financing to add exposure.

As prices fell, the net asset value tied to corporate holdings also fell. At the same time, equity valuations for many digital asset treasury companies moved lower, reducing their ability to issue stock on favorable terms.

Consequently, the result has been a tighter feedback loop across the sector, in which a lower Bitcoin price reduces Bitcoin’s net asset value per share. This leads to lower equity premiums, making stock issuance less accretive.

Once those conditions are set in, the same financing mechanism that helped companies expand their Bitcoin positions begins to lose effectiveness.

That pressure has hit treasury-company equities hard. Shares that had traded as high-beta expressions of Bitcoin’s upside have declined sharply from their 2025 highs, and many have underperformed BTC itself.

For companies that bought heavily near the top of the market, such as Metaplanet, unrealized losses are beginning to mount.

Metaplanet Bitcoin Holdings Net Value (Source: Metaplanet)

Stress emerges across the sector

Meanwhile, signs of strain are beginning to appear in individual cases across the sector.

One recent example came from GD Culture, the publicly traded artificial intelligence and livestreaming firm, which approved the sale of its 7,500 Bitcoin, worth about $503 million, to fund share buybacks and support its stock price.

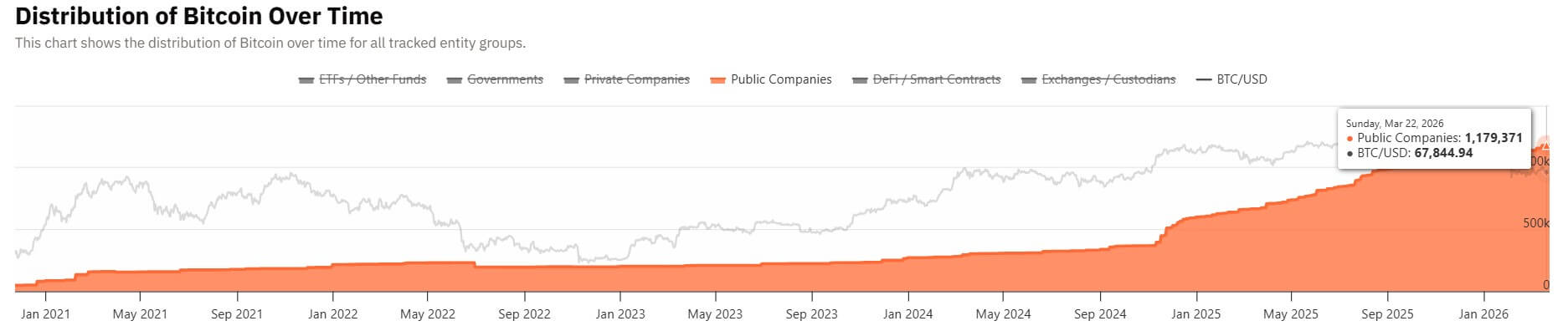

The sector’s aggregate numbers also reflect the change in conditions. More than 100 public companies piled roughly $100 billion into Bitcoin last year as the trade gathered pace.

Those holdings are now worth about $83.7 billion, according to Bitcoin Treasuries data, a sharp reduction from their peak value.

Public Companies Total Bitcoin Holdings (Source: Bitcoin Treasuries)

At the same time, only two of the public companies that hold Bitcoin on their balance sheets bought more of the asset in the past week, according to data compiled by Hodl15Capital.

The slowdown suggests that, outside a small number of committed players, the appetite to keep adding exposure has faded with the market.

Metaplanet, one of the highest-profile Bitcoin treasury companies in Japan, raised 40.8 billion yen, or about $255 million, as part of a financing that could deliver up to $531 million in total capital for Bitcoin purchases.

Yet it has not made a Bitcoin purchase this year, even as it maintains a long-term target of holding 210,000 Bitcoin. The company currently holds 35,102 Bitcoin.

Against that background, research across the sector is increasingly pointing to a more difficult environment for firms that built their strategy around equity issuance and rising Bitcoin prices.

Analysts at Galaxy Digital have said the same financial engineering that amplified upside when valuations were strong is now magnifying downside as equity premiums compress.

For treasury companies whose shares had functioned as leveraged crypto trades, softer markets and weaker risk appetite across public equities have changed the economics of the model.

Crypto research firm 10x Research also argued that the first stage of the treasury-company trade has already run its course, with the easy gains from rich premiums to net asset value no longer available to most firms.

In that environment, companies are likely to face stronger scrutiny over how much stock they issued at peak valuations, how much Bitcoin they bought near cycle highs, and how much debt they took on to fund those positions.

Now, a more selective phase is beginning to take shape.

Galaxy Digital stated that companies with stronger balance sheets and more durable access to capital are better positioned to endure a long period of flat or negative premiums to net asset value.

Already, several Bitcoin treasury firms, including Strategy and Strive, are using preferred stock options to fund new BTC acquisitions, aiming to outperform the top crypto over the long term.

On the other hand, others may need to scale back purchases, rethink capital strategy, or defend shareholder support if equity markets remain unreceptive.

Strategy’s Bitcoin holdings have crossed the 760,000 BTC threshold, marking a significant milestone in what has become one of the most aggressive corporate accumulation strategies in digital assets. Artificial intelligence models now project the company could reach 1 million BTC as early as September 2026, though realistic timelines extend into late 2026 or early 2027, depending on capital availability and market conditions. For institutional investors, this trajectory signals both the viability of Bitcoin as a corporate treasury asset and the emerging role of AI in forecasting long-term acquisition patterns in volatile markets.

Strategy, formerly known as MicroStrategy, has announced its holdings have surpassed 761,068 BTC as of March 16, 2026, following a record weekly purchase of 22,337 BTC valued at approximately $1.57 billion. The company’s relentless pursuit of Bitcoin accumulation, spearheaded by CEO Michael Saylor, continues despite macroeconomic headwinds and cryptocurrency market volatility. This latest acquisition represents the acceleration of a multi-year strategy that has transformed the enterprise software company into one of the world’s largest corporate holders of Bitcoin, rivaling sovereign wealth allocations. As Strategy approaches the symbolic 1 million BTC milestone—representing roughly 4.76% of all Bitcoin ever to be mined—the financial and strategic implications have captured the attention of institutional investors, asset managers, and cryptocurrency market analysts worldwide.

AI Models Project Divergent Timelines for Million-Bitcoin Target

Two leading artificial intelligence platforms have published competing forecasts regarding Strategy’s path to 1 million BTC, each arriving at different conclusions based on distinct methodological approaches. Grok AI, developed by xAI and SpaceX founder Elon Musk, suggests the most optimistic scenario, projecting that Strategy could mathematically reach the 1 million BTC milestone as early as September 2026 if current acquisition velocity persists. This forecast is grounded in Strategy’s recent purchasing patterns, which have demonstrated significant acceleration over the preceding three weeks, during which the company acquired between 3,015 and 22,337 BTC weekly, averaging approximately 14,450 BTC per week. At such a pace, maintaining consistent capital deployment would theoretically close the remaining 238,932 BTC gap within roughly five to six months.

However, Grok AI’s analysis acknowledges a critical constraint: sustaining weekly acquisitions of this magnitude would require continuous capital raises exceeding $1 billion per week—a requirement the platform notes is unrealistic under current market and financing conditions. Consequently, Grok’s more sustainable projection, accounting for historical averages of approximately 2,500 BTC per week through Strategy’s STRC preferred stock funding program, suggests a more credible target date of September 2026. This revised timeline incorporates material factors including market liquidity constraints, capital raising limitations, equity dilution concerns, price volatility, and execution risk. The distinction between theoretical and practical timelines highlights the complexity of translating aggressive corporate strategies into achievable milestones within real-world constraints.

ChatGPT’s analysis presents a more conservative framework, suggesting that Strategy would need to acquire approximately 5,550 BTC weekly to reach 1 million BTC by December 2026—a rate roughly 50 to 100 percent above recent weekly averages. While the AI model acknowledges this goal is ambitious, it suggests late December 2026 could represent an achievable target if Strategy substantially escalates purchases through coordinated equity issuance and accelerated STRC funding. Yet ChatGPT’s base case forecast points toward early January 2027 as a more probable arrival date, recognizing that market liquidity constraints, price volatility, and uneven acquisition patterns across weeks create practical headwinds. Both AI models converge on a timeframe spanning late 2026 through early 2027, suggesting institutional consensus that the 1 million BTC target remains achievable within an 12-to-18 month window from the March 2026 baseline.

Capital Deployment Strategy and Funding Mechanisms

Strategy’s ability to reach 1 million BTC depends critically on its capacity to raise and deploy capital at scale without triggering unacceptable equity dilution or market disruption. The company currently employs two primary funding mechanisms: direct equity issuance and its proprietary STRC (Strategy Tracker Convertible) preferred stock program, which allows the company to raise capital while offering investors conversion rights tied to Bitcoin holdings. The STRC program has proven particularly valuable, as it enables capital raising while preserving voting control and avoiding the traditional equity dilution associated with common stock offerings. Recent weekly acquisitions averaging 14,450 BTC represent deployment rates of $900 million to $1.57 billion, indicating access to substantial capital flows despite macroeconomic volatility.

The sustainability of these acquisition rates hinges on multiple factors beyond capital availability. Bitcoin market liquidity, measured across major exchanges and over-the-counter desks, must accommodate Strategy’s block purchases without triggering significant price slippage or market disruption. As Strategy’s position approaches 5 percent of circulating Bitcoin supply, each successive acquisition becomes operationally more complex and potentially moves markets more noticeably. Additionally, the company must navigate regulatory scrutiny in jurisdictions where large Bitcoin concentrations may trigger disclosure requirements or compliance obligations. Strategy’s historical pattern of acquiring Bitcoin in tranches—rather than attempting to accumulate continuously—suggests management recognizes these practical constraints and tailors acquisition timing to optimize execution.

The financing model also requires sustained access to capital markets during periods of cryptocurrency volatility and regulatory uncertainty. Strategy’s ability to issue STRC securities or conduct equity offerings depends partly on investor appetite for Bitcoin-exposed equity instruments and confidence in the company’s strategic direction. Should broader macroeconomic conditions deteriorate significantly or should Bitcoin experience sustained price weakness, Strategy’s cost of capital could rise substantially, making the aggressive accumulation strategy less economically rational. Conversely, Bitcoin price appreciation would reduce the quantity of capital required to reach 1 million BTC, potentially accelerating timelines. This dynamic creates a feedback loop where Bitcoin’s price discovery mechanism directly influences the feasibility of Strategy’s milestone projections.

Institutional Implications and Market Significance

Strategy’s pursuit of 1 million BTC carries profound implications for institutional asset allocation, corporate treasury management, and Bitcoin’s acceptance as a legitimate institutional store of value. The company’s publicly stated strategy—to accumulate Bitcoin as its primary treasury asset and hold indefinitely—has inspired peer scrutiny and competitive positioning among other corporations and institutional investors. Should Strategy successfully achieve and maintain 1 million BTC holdings, representing approximately 4.76% of all Bitcoin that will ever exist, the company would effectively establish itself as one of the world’s largest non-sovereign holders of a major digital asset. This concentration raises intriguing questions about corporate governance, fiduciary responsibility, and the concentration risk embedded in Bitcoin’s distributed ledger system.

For institutional investors evaluating cryptocurrency exposure, Strategy’s execution demonstrates that large-scale, sustained Bitcoin accumulation is operationally feasible despite real-world constraints and market volatility. The company has successfully acquired over 760,000 BTC through multiple market cycles, price rallies, and corrections, suggesting that disciplined, long-horizon investment strategies can accumulate meaningful positions without requiring perfectly timed entry points. This reality may reduce perceived barriers to institutional Bitcoin adoption and encourage other corporations to evaluate similar treasury strategies. Furthermore, Strategy’s continued success in raising capital for Bitcoin purchases—even during periods of cryptocurrency market skepticism—suggests investor confidence in both the company’s strategic vision and Bitcoin’s long-term value proposition.

The September 2026 to January 2027 timeline projected by AI models also carries symbolic significance. Achievement of 1 million BTC would represent a corporate commitment to digital assets of unprecedented scale and permanence, occurring roughly 17-18 years after Bitcoin’s 2009 genesis block. This timing aligns with Bitcoin’s maturation as an asset class and the growing normalization of cryptocurrency within institutional portfolios. Should Strategy reach this milestone, the financial services industry will likely experience accelerated institutional adoption, potentially triggering cascading demand from pension funds, endowments, and other large asset holders seeking comparable exposure. Conversely, any failure or significant delay in reaching 1 million BTC could signal limitations in corporate Bitcoin accumulation strategies and dampen emerging institutional enthusiasm for large-scale digital asset concentration.

Whether Bitcoin can sustain institutional momentum through current market weakness depends largely on whether the structural advantages cited by major market participants prove durable. MicroStrategy chairman Michael Saylor recently articulated a bullish case for Bitcoin’s near-term recovery, arguing that today’s pullback differs meaningfully from historical bear cycles—a position bolstered by his firm’s substantial on-chain Bitcoin holdings but viewed with skepticism by other market analysts.

Saylor’s Recovery Thesis

Saylor framed the current Bitcoin correction as relatively mild compared to previous downturns, positioning a rapid rebound as the probable outcome. His optimism rests on a fundamental claim: institutional participation in cryptocurrency markets has matured substantially since earlier cycles.

Banks and large financial institutions now operate within purpose-built infrastructure designed to facilitate digital asset custody, lending, and trading. This institutional scaffolding—largely absent during prior bear markets—represents genuine structural change in how capital flows into Bitcoin and related assets.

The deepening of institutional engagement with digital assets occurs within a framework of regulated banking infrastructure and credit facilities specifically engineered for the cryptocurrency sector.

— Crypto Coin Show Analysis

Saylor’s thesis hinges on the idea that institutional capital, once committed, exhibits greater staying power than retail-driven speculative flows. Whether that assumption holds during sustained downside pressure remains an open empirical question.

MicroStrategy’s Bitcoin Position

MicroStrategy maintains approximately 714,644 Bitcoin acquired at an average cost of roughly $76,056 per coin. At current spot prices near $67,900, this portfolio represents approximately $49 billion in value—a figure that exceeds MicroStrategy’s own market capitalization of roughly $42.8 billion.

Key Metric

MicroStrategy’s Bitcoin holdings now exceed the company’s total market capitalization, creating an inverted balance sheet structure where a single asset class drives enterprise valuation.

This concentration presents both opportunity and risk. The company has stressed that even a hypothetical decline to $8,000 per Bitcoin would maintain sufficient collateral backing for debt service obligations. That reassurance, however, carries limited weight if sustained volatility compounds operational pressures.

MicroStrategy has outlined plans to convert outstanding convertible debt instruments into equity over a three- to six-year horizon while maintaining a quarterly Bitcoin acquisition schedule. These capital decisions remain contingent on market conditions, available financing terms, and execution timing. The debt conversion strategy potentially reduces near-term pressure on share price dynamics but locks in exposure to continued Bitcoin volatility.

Institutional Participation and Market Structure

The claim that current conditions differ materially from historical cycles warrants careful scrutiny. Saylor’s argument rests on measurable institutional adoption, yet evidence of sustained, broad-based inflows remains mixed across on-chain transaction data and lending market indicators.

Comparative analysis requires examination of several concrete data points: transaction flow patterns on major exchanges, central bank liquidity conditions affecting traditional finance, banking sector credit extension to digital asset firms, and regulatory posture toward cryptocurrency market infrastructure.

Some market observers note that institutional participation has indeed expanded. Regulated spot Bitcoin Bitcoin exposure vehicles, custody infrastructure, and derivative markets now accommodate substantial capital deployment. Yet the persistence of institutional capital during periods of steep price declines—when leverage unwinds and volatility spikes—remains untested in the current cycle.

Market Context

Institutional adoption metrics improved materially over the past 18 months, but whether this capital proves “sticky” during sustained corrections differs from whether it drives consistent price appreciation.

On-chain analysis provides partial clarity. Wallet concentration, exchange inflows and outflows, and long-term holder behavior offer signals about institutional versus retail positioning. Current data shows elevated volatility across these metrics, consistent with periods of uncertainty about medium-term direction.

The Evolving Cryptocurrency Market Landscape

Understanding Saylor’s positioning requires context about the broader cryptocurrency industry transformation over the past five years. The emergence of spot Bitcoin exchange-traded funds in the United States, Canadian regulatory approval of similar instruments, and growing recognition from traditional asset managers represents a fundamental shift in how institutional capital accesses digital assets.

Major financial institutions including BlackRock, Fidelity, and Charles Schwab have expanded cryptocurrency services offerings substantially. This institutional embrace reflects both market demand and recognition that digital assets represent a legitimate alternative asset class requiring infrastructure equivalent to equities or fixed income markets.

However, institutional adoption does not necessarily stabilize Bitcoin during cyclical downturns. Historical precedent from other alternative asset classes suggests that institutional participation can amplify volatility during periods of systematic deleveraging, particularly if institutions face redemption pressures or margin calls across multiple asset categories simultaneously.

The cryptocurrency lending sector—which expanded dramatically from 2020 through 2022—experienced severe disruption following the collapse of FTX and related market stress. Major institutional lending platforms either ceased operations or substantially curtailed service offerings. This contraction potentially constrains leverage availability during the next institutional capital inflow cycle, an outcome that could either reduce volatility or prevent capital deployment entirely depending on market conditions.

MicroStrategy’s Corporate Strategy and Market Implications

Beyond Bitcoin holdings, MicroStrategy operates a legacy business analytics software division generating approximately $500 million in annual recurring revenue. The company’s strategic pivot toward Bitcoin accumulation, funded through debt issuance and equity offerings, represents an unconventional corporate capital allocation strategy that concentrates shareholder returns entirely on Bitcoin price appreciation.

This approach creates a leveraged play on institutional cryptocurrency adoption. If Saylor’s thesis proves correct—that institutional participation drives sustainable Bitcoin demand—MicroStrategy shares could outperform the underlying Bitcoin asset substantially. Conversely, if institutional participation proves cyclical rather than structural, the company faces pressure to justify its balance sheet composition to debt holders and equity investors.

MicroStrategy’s strategy has attracted both significant investment from Bitcoin enthusiasts and criticism from traditional corporate governance advocates who view the concentrated Bitcoin exposure as excessive and speculative. The company’s quarterly earnings calls have emphasized management’s conviction in the Bitcoin thesis, but execution risk remains substantial if capital markets restrict the company’s access to financing or if debt covenant negotiations become more restrictive.

Catalysts and Uncertainty Ahead

Multiple potential catalysts could reshape market narrative over coming quarters. Central bank monetary policy decisions—particularly regarding interest rate trajectories and quantitative easing programs—directly influence capital allocation decisions across risk assets including Bitcoin and other digital assets.

Regulatory announcements from U.S. and international authorities regarding cryptocurrency market oversight, custody standards, and financial institution exposure limits could either validate institutional participation or impose constraints. Banking sector stress, should it materialize, might paradoxically strengthen Bitcoin’s appeal as a non-correlated asset or trigger forced liquidations across leveraged positions.

The cryptocurrency sector’s regulatory trajectory remains heavily contested. Proposed legislation addressing stablecoin issuance, exchanges, and custody requirements could accelerate institutional adoption by clarifying operational frameworks, or it could impose compliance costs that disadvantage smaller participants and consolidate market power among large incumbents.

Macroeconomic conditions—inflation trajectories, employment data, geopolitical tensions affecting energy markets—indirectly influence institutional appetite for alternative assets. Saylor’s confidence in rapid recovery depends partly on the assumption that macroeconomic conditions stabilize rather than deteriorate further.

The technical picture remains contested. Recent price action has oscillated within defined ranges, neither confirming a decisive break downward nor establishing clear upside momentum. Investors should monitor these levels carefully as they may signal the directional bias for institutional positioning over coming weeks.

Evaluating the Thesis Critically

Saylor’s public positioning—bullish on Bitcoin, confident in institutional participation, and aggressive in capital deployment—naturally reflects his firm’s material financial interests. That alignment of message with incentive structures does not invalidate the underlying analysis, but it does warrant independent verification of the empirical claims about institutional adoption and cycle dynamics.

Market participants evaluating Saylor’s thesis should examine whether institutional capital genuinely exhibits different risk tolerance profiles than retail capital, whether current regulatory clarity truly reduces systemic vulnerabilities, and whether banking sector engagement with cryptocurrency creates durable infrastructure or merely cyclical participation tied to asset price momentum.

The distinction between structural adoption and cyclical participation remains the central question animating current market debate. If institutional participants view Bitcoin as comparable to traditional alternative assets like commodities or real estate, sustained demand could emerge independent of speculative cycles. If instead institutions view cryptocurrency as tactical positioning tied to macroeconomic themes or relative value opportunities, capital flows could reverse sharply if underlying conditions shift.

Evidence will accumulate gradually through transaction data, regulatory developments, and institutional capital commitments. Bitcoin’s price discovery mechanism will reflect market participants’ evolving assessment of these fundamental questions over coming months and years.

Get weekly blockchain insights via the CCS Insider newsletter.

Historic First: U.S. SEC Chair to Address Bitcoin Conference as Industry Scales New Heights

LAS VEGAS, NV — The Bitcoin 2026 Conference, the world’s premier annual gathering dedicated exclusively to Bitcoin, has announced its first wave of headline speakers and a fully redesigned programming structure for its 2026 edition. With over 30,000 registered attendees and projections to exceed 40,000 participants, the conference is expanding significantly with new stages, specialized tracks, and cultural experiences designed to serve the entire Bitcoin ecosystem.

Conference Details at a Glance

Dates: April 27–29, 2026

Location: The Venetian Convention and Expo Center, Las Vegas, NV

Expected Attendance: 40,000+ participants

Current Registrations: 30,000+

Stages: 6 dynamically curated stages

Programming Hours: 100+ hours across three days

Confirmed Speakers: 100+ industry leaders and experts

Historic First Wave of Speakers

Bitcoin 2026 has confirmed a landmark roster of speakers that marks unprecedented engagement from U.S. regulatory bodies and industry leadership:

Michael Saylor

Founder & Executive Chairman, MicroStrategy

One of Bitcoin’s most prominent institutional evangelists, Saylor has been instrumental in shaping narratives around Bitcoin adoption across the enterprise and corporate sectors globally.

Paul S. Atkins

Chairman, U.S. Securities and Exchange Commission

Historic Milestone: First sitting SEC Chair to address the Bitcoin Conference. This appearance represents a significant moment at the intersection of regulatory authority and digital asset innovation.

Mike Selig

Chairman, Commodity Futures Trading Commission

A longtime contributor to digital asset regulatory frameworks, Selig brings deep expertise in futures markets, digital commodity policy, and the evolving regulatory landscape shaping Bitcoin’s institutional integration.

Additional speaker announcements will roll out over the coming months leading up to the April event.

Six-Stage Programming Structure

Bitcoin 2026 features a fully redesigned conference architecture with specialized programming tracks across six distinct stages:

🔗 Nakamoto Stage

Core technical and protocol-level discourse

⚙️ Genesis Stage

Foundational education and ecosystem building

⚡ Energy Stage

Bitcoin mining, energy innovation, and infrastructure

🛠️ Open Source Stage

Development, code, and builder-focused sessions

🏢 Enterprise Stage

Corporate adoption, finance, and institutional integration

🌊 Deep Stage

Advanced topics and specialized knowledge tracks

Beyond the Main Conference: Cultural & Community Experiences

Bitcoin 2026 is positioning itself as more than a conference—it’s a cultural gathering. Alongside main stage programming, attendees will experience:

Compute Village (NEW)

A dedicated hub connecting builders, miners, developers, and infrastructure leaders around power-dense compute and energy innovation.

Women of Bitcoin Bash

An evening celebration highlighting women driving innovation and adoption across the Bitcoin ecosystem.

Bitcoin for Corporations Symposium

A focused forum for enterprise, finance, and institutional stakeholders to explore Bitcoin integration strategies.

Bitcoin Art Gallery

Curated by Bitcoin Magazine (BMAG), this showcase features artistic expression inspired by Bitcoin as part of the magazine’s broader museum initiative.

Side Events & Meetups

Community networking events and specialized meetups throughout the conference weekend.

About Bitcoin 2026

Bitcoin 2026 is organized by BTC Media (parent company of Bitcoin Magazine) and serves as the flagship event in a global conference series. BTC Media hosts Bitcoin-focused events on every continent, including international editions:

Bitcoin Hong Kong — August 27–28, 2026

Bitcoin Amsterdam — November 5–6, 2026

Bitcoin MENA — Abu Dhabi, December 2026

Registration & More Information

Attendees can learn more about programming, register, and explore the full conference experience at:

“Bitcoin 2026 reflects how far this conference — and the Bitcoin ecosystem itself — has evolved. With tens of thousands of attendees already registered, expanded stages, and a redesigned experience, we’re building an event that meets people wherever they are in their Bitcoin journey while continuing to push the conversation forward globally.”

Bitcoin recovered modestly on Sunday as geopolitical tensions eased between Washington and Beijing, while Michael Saylor’s company continued signaling steady accumulation through what has become his trademark purchasing indicator. The subtle market recovery underscores how macroeconomic headlines now compete with company-specific buying activity in driving short-term price movements across digital assets.

The Orange Dot Signal

On October 26, Saylor posted a chart adorned with orange dots—his established visual shorthand for new Bitcoin purchases. The message was unmistakable: his firm had resumed buying despite ongoing market volatility. This simple graphic has evolved into a recognizable market signal that traders and investors monitor closely.

Between mid-October and late October, the company acquired 387 BTC, bringing its disclosed total holdings to 640,418 Bitcoin. While this represents meaningful accumulation, the pace has moderated considerably from September’s aggressive buying spree. The deliberate, measured approach reveals a strategy focused on consistent dollar-cost averaging rather than attempting to time market bottoms.

Strategy’s disclosed average cost for its Bitcoin stands at $74,010, demonstrating how discipline and patience compound over time.

— Public Filings and Market Reports

The company’s current buying cadence—smaller, more frequent tranches—suggests a philosophical shift toward steady accumulation. This contrasts sharply with September, when the firm executed several transactions totaling over 7,000 BTC in concentrated moves. The recent repositioning may reflect both valuation concerns at current price levels and confidence in a longer-term accumulation framework.

Key Metric

At Bitcoin prices near $115,000, the company’s holdings carry an estimated valuation of approximately $72 billion, representing an unrealized gain exceeding $25 billion since the buying program commenced in 2020.

Market Valuation and Investor Confidence

The company’s stock has consistently traded above its net asset value, a premium that reflects investor appetite for Bitcoin exposure through traditional equity markets. This valuation spread suggests the market views the corporate wrapper as valuable—offering convenience and regulatory clarity compared to direct cryptocurrency ownership.

Since 2020, the firm has executed 83 separate purchase events, creating a transparent buying pattern that institutional investors can analyze and predict. The consistency of this approach—purchasing, then disclosing—has become a market rhythm that analysts track closely. Learn more about Bitcoin investment strategies and market dynamics.

The premium valuation also implies confidence that Bitcoin itself will appreciate further, validating the accumulation thesis embedded in the company’s strategy. Investors betting on the firm are effectively making a dual wager: on Bitcoin’s future price and on the company’s ability to manage its balance sheet responsibly.

Corporate Bitcoin Holdings in Institutional Context

The rise of corporate Bitcoin treasuries represents a fundamental shift in how institutional capital allocates to digital assets. What began as fringe activity has evolved into standard practice among publicly traded companies seeking to diversify reserves and hedge against currency debasement. The company’s program now operates within an ecosystem where major corporations from technology, finance, and industrial sectors maintain significant cryptocurrency positions.

This institutional pivot has created cascading effects throughout the Bitcoin market. When large, regulated entities commit balance sheet capital to cryptocurrency, it triggers several market mechanisms: reduced selling pressure from retail investors fearful of legitimacy questions, increased institutional custody demand from banks and custodians, and enhanced regulatory clarity from governments monitoring corporate activities.

The visibility and transparency of these corporate programs—particularly their published acquisition strategies and holdings disclosures—have also established new market benchmarks. Investors can now compare corporate Bitcoin allocation as a percentage of assets under management, creating competitive dynamics that incentivize further accumulation among institutional peers.

Broader Market Drivers

Bitcoin’s 1.6% Sunday gain occurred alongside a 2.8% rise in Ethereum, suggesting that risk-on sentiment was broadly lifting the crypto complex. However, attributing these moves solely to corporate buying would be misleading. Macroeconomic narratives and geopolitical developments wielded outsized influence.

US Treasury Secretary Scott Bessent indicated that trade tensions between America and China had begun to ease, telling CBS News that the threat of sweeping 100% tariffs appeared to have receded. This shift in rhetoric provided relief across risk assets. Earlier in October, Donald Trump had threatened these tariffs alongside export controls targeting Chinese semiconductor-related technologies, with implementation scheduled for November 1.

Context

China had responded to trade pressure by announcing stricter export limits on rare earth minerals critical to chip manufacturing, escalating tit-for-tat measures that rattled global markets and triggered significant cryptocurrency liquidations.

The timing of Saylor’s “Orange Dot Day” announcement coincided with improving headlines on trade, yet the two developments likely reflect separate market forces. Broader sentiment improved independent of any single company’s purchasing activity. Explore current crypto price movements and technical analysis for deeper market context.

Strategic Accumulation Amid Volatility

What distinguishes this corporate buying program is its mechanical consistency. The firm does not attempt to predict tops or bottoms. Instead, it purchases routinely, reports transparently, and lets market participants draw their own conclusions about valuation.

The shift from large September purchases to smaller October transactions may signal either a strategic recalibration or simply the mathematical reality that larger acquisitions become harder to execute at higher price levels. The Bitcoin market has grown substantially since 2020, making five-figure coin purchases more logistically complex.

This approach—disciplined, repetitive, and thoroughly transparent—has established a new template for how corporate entities can participate in the Bitcoin ecosystem without stoking regulatory concerns or market manipulation suspicions.

— Market Observers and Institutional Analysts

Institutional investors now view such accumulation programs as validation signals. When a large, regulated corporation commits capital repeatedly to Bitcoin, it tacitly affirms the asset’s legitimacy within broader investment frameworks. This dynamic has helped Bitcoin transition from speculative bet to strategic reserve asset in institutional portfolios.

Industry Implications and Market Structure

The corporate Bitcoin accumulation trend has accelerated the professionalization of cryptocurrency markets. Where retail speculation once dominated price discovery, institutional capital now provides substantial liquidity depth and reduces volatility during panic events. This structural evolution benefits the entire ecosystem by attracting conservative investors previously deterred by market immaturity.

Bitcoin’s role as a corporate treasury asset also strengthens its position during economic uncertainty. Unlike technology stocks or bonds that correlate with broader market cycles, Bitcoin increasingly functions as an uncorrelated hedge. Companies accumulating Bitcoin are effectively creating financial optionality—preserving capital value against currency depreciation while maintaining exposure to potential cryptocurrency appreciation.

The precedent established by successful corporate accumulation strategies creates competitive pressure on other firms to develop similar programs. As more corporations announce Bitcoin treasury positions, the narrative shifts from “should we own crypto?” to “how much crypto should we own?” This subtle reframing has profound implications for long-term Bitcoin demand and price sustainability.

The coming weeks will test whether trade tensions truly have eased or whether geopolitical uncertainty will resurface. Bitcoin’s price action will likely remain sensitive to headlines regarding US-China relations, Federal Reserve policy, and broader macroeconomic conditions.

Meanwhile, the orange dots will continue to appear on Saylor’s charts whenever purchases occur. Each visual marker reinforces a narrative of patience, discipline, and confidence in Bitcoin’s long-term value proposition. Whether such signals influence broader market sentiment or simply provide confirmation of existing bullish conviction remains an open question for market participants to weigh.

As the Bitcoin market matures and corporate participation deepens, these accumulation signals will likely carry increasing weight in institutional decision-making processes. The transparency of such programs creates accountability mechanisms that enhance market integrity while simultaneously demonstrating corporate commitment to long-term Bitcoin holdings over short-term speculation.

Get weekly blockchain insights via the CCS Insider newsletter.