Chainlink continues to strengthen its dominance within the oracle economy as adoption of its Smart Value Recapture (SVR) solution accelerates across the DeFi ecosystem. With decentralized finance increasingly reliant on accurate, secure, and tamper-resistant data feeds, Chainlink remains at the center of this infrastructure layer, powering a growing share of on-chain applications.

Why SVR Could Become A Major Revenue Layer For Chainlink

Since Chainlink launched, Smart Value Recapture (SVR) has rapidly become the dominant solution for capturing oracle-related Maximal Extractable Value (MEV), now commanding an estimated 99% market share. Crypto analyst Zach Rynes highlighted on X that the system has been widely adopted by the largest DeFi lending platforms such as Aave, Compound, Venus, and various Morpho markets.

At its core, the SVR exclusively recaptures the non-toxic liquidation MEV of value that would have leaked to Layer 1 validators and searchers during DeFi loan liquidations. The scale of adoption is already producing significant results. SVR has reportedly generated approximately $18.7 million in revenue, distributing approximately $12 million back to integrated DeFi protocols while contributing $6.7 million to Chainlink, including support for LINK buybacks.

Meanwhile, the system efficiency is reflected in its consistent recapture rate of about 85%, meaning SVR recaptures the $85 from every $100 liquidation bonus made available. It has already processed over $700 million in liquidation volume on Aave alone, without generating bad debt, even during periods of heightened volatility such as October 10. Additionally, it also features the largest and most decentralized ecosystem of independent searchers, with over 115 independent liquidators. Competition ensures solvency and drives up recapture rates.

SVR marks a major shift in the Chainlink business model, enabling it to directly monetize the total value it secures across DeFi applications, in addition to monetizing the integration, usage, and maintenance of oracle services by blockchains via the Scale program. In this context, SVR is a powerful new economic engine that reinforces the Chainlink position at the center of decentralized finance.

Chainlink’s Staking Model Awaits A Clear Regulatory Framework

The Chainlink staking ecosystem could be approaching a pivotal moment as the crypto industry moves closer to greater regulatory clarity. According to analyst LinkBoi, the current Clarity Art is limiting Chainlink’s ability to expand staking pool rewards distribution within the network.

Currently, stakers are receiving incentives primarily through allocated token emissions rather than a share of protocol-generated revenue. The staking pool expansion requires permission to pay stakers a portion of the protocol’s revenue.

However, if the Clarity Act provides the necessary legal clarity, it would unlock a major opportunity for the LINK token to be considered as a security. The staking pool could expand significantly, bringing the full LINK tokenomics ecosystem into effect.

The rsETH crisis resulted in $200 million in bad debt on Aave’s books, despite not a single line of its contracts misbehaving.

On Apr. 18, attackers that Chainalysis preliminarily linked to Lazarus compromised RPC infrastructure, forced a failover to poisoned nodes via DDoS, and injected false data into a 1-of-1 DVN configuration on KelpDAO’s rsETH bridge.

The forged message released approximately 116,500 rsETH, and Aave’s incident report confirmed that Ethereum accepted nonce 308 while the Unichain source endpoint never advanced past 307.

The attacker supplied the compromised rsETH to Aave and borrowed against it, resulting in bad debt and serving as a frame for the current state of DeFi’s security.

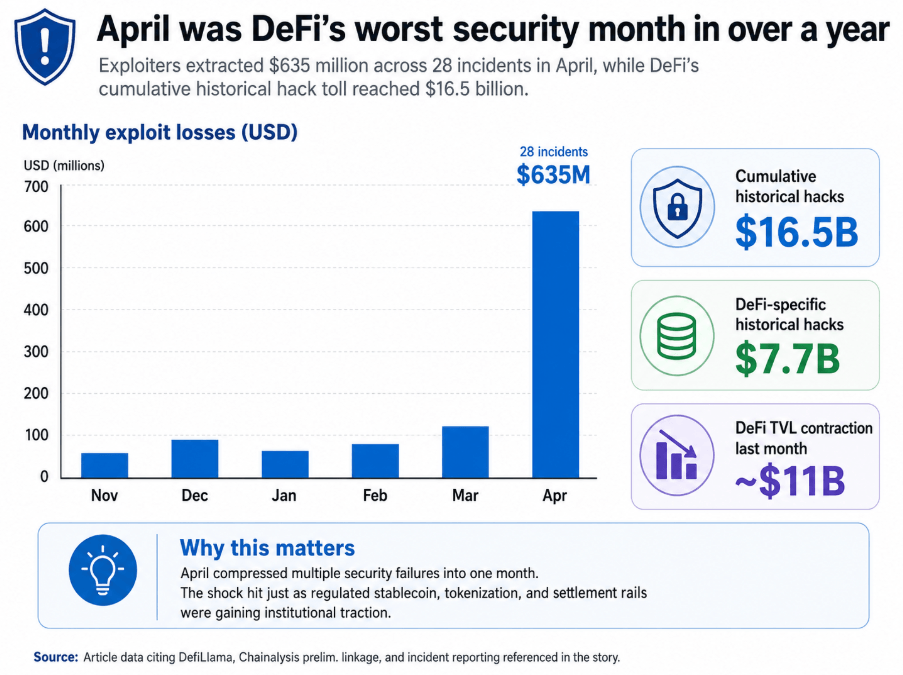

Exploiters extracted over $635 million across 28 incidents in April, the worst monthly total in over a year. DefiLlama puts the cumulative historical cost of hacks at $16.5 billion, with $7.7 billion specifically targeting DeFi.

The high-profile exploits on Drift and the KelpDAO bridge resulted in DeFi losing nearly $11 bilion in total value locked last month.

That contraction occurred as stablecoin rails, tokenized treasuries, and regulated settlement layers gained institutional traction in the same capital markets.

DeFi exploiters extracted $635 million across 28 incidents in April, the sector’s worst monthly loss in over a year, while cumulative historical hacks reached $16.5 billion.

How did DeFi end up here?

Mitchell Amador, CEO of Immunefi, told CryptoSlate that DeFi has historically rewarded growth, integrations, liquidity, and speed over security maturity.

A protocol that adds a new asset, bridge, oracle, adapter, or external dependency gains immediate utility. The risk that integration carries produces no visible price signal until an exploit materializes, because the absence of an incident is invisible while it holds.

That asymmetry kept audit cycles and isolation practices secondary to shipping velocity for years, until April concentrated the consequences into a single month.

Amador said the most overlooked practices were multisig hygiene and management, supply chain hardening, real-time monitoring, and emergency response procedures.

Too many teams treated multisig as a security solution in itself, when its actual strength depends on signer count, the independence of those signers, their operational setup, and the processes around transaction review.

A low-threshold multisig, weak signer security, or a poorly monitored bridge or oracle can become a systemic exposure because DeFi protocols are composable by default. In this landscape, risk travels through integrations as efficiently as liquidity does.

While that culture was forming inside DeFi, a different model was being built in parallel.

“The gap in output per person tells you what happens when you strip away everything that isn’t the core financial function. The teams that win this round will be the ones built on compliance and security from day one, ready to ship faster than a bank can call a meeting about it.”

DeFi built composable rails for over half a decade before Wall Street recognized them as the actual infrastructure layer of the next financial system.

The cost of that early market position was a security culture calibrated for speed over operational discipline.

Kasper Pawlowski, CTO of Euler Finance, names the governance dimension of the same failure in his post-incident analysis.

He said:

“DeFi treats risk assessment as a one-time onboarding decision, when in reality risk is dynamic.”

The 1-of-1 DVN configuration that enabled the KelpDAO exploit existed in production for years. Kelp says it was the default LayerZero shipped and reviewed across multiple integration meetings, while LayerZero says Kelp downgraded to it.

Whichever account is accurate, the configuration persisted unflagged through every integration with every downstream protocol. LayerZero has since banned the configuration on a protocol-wide basis, acknowledging that allowing its DVN to act as the sole verifier for high-value transactions was a mistake.

Stage

What happened

Why it mattered

RPC infrastructure compromised

Attackers compromised RPC infrastructure tied to the rsETH bridge setup

The attack began outside the core smart contracts, showing how off-chain infrastructure can become the entry point

DDoS forced failover

Traffic was pushed onto poisoned nodes through a forced failover

That let attackers control the data environment seen by the bridge verifier

False data injected into 1-of-1 DVN

Poisoned nodes fed false data into a single-verifier DVN configuration

A 1-of-1 verifier setup meant there was no independent check to stop the forged message

Forged bridge message accepted

The forged message released about 116,500 rsETH

Fake collateral was effectively minted into circulation

Fake rsETH supplied to Aave

The attacker deposited compromised rsETH into Aave as collateral

Aave treated the asset as valid and allowed borrowing against it

Borrowing created bad debt

The attacker borrowed other assets and left Aave with roughly $200 million in bad debt

Losses from a bridge failure migrated into a lending market and were socialized across the pool

The more consequential point is that a critical bridge-security parameter was normalized across the entire dependency chain until a $292 million exploit surfaced it.

Pawlowski argued:

“The operational machinery DeFi has built — DAO governance, external risk service providers, and monthly review cycles — doesn’t move at the speed the underlying risk surface does. In many cases, the people doing the reviewing aren’t structurally independent of the assets they’re reviewing.”

That structural conflict produced the specific governance failure Pawlowski dissected. Aave’s 25,000 ETH treasury recovery proposal was authored by TokenLogic, a paid Aave service provider that publicly lists Kelp as a client and operates an Aave delegate platform.

For reference, TokenLogic is the same firm voting on its own proposals. On the same day Aave expanded rsETH to a 93% loan-to-value ratio in eMode, SparkLend deprecated the asset entirely, bundling the move with routine cleanup of underused positions.

Three months later, that routine pruning was the only separation between Spark’s depositors and the bad debt Aave now carries.

One protocol’s independent risk judgment outperformed another’s full-stack risk advisory apparatus. DeFi’s review machinery generated worse outcomes than a single asset manager doing portfolio hygiene.

What “here” means

Before the exploit, Aave was the largest DeFi protocol by total value locked, with over $26 billion in deposits.

Pawlowski noted:

“Aave was the gold standard. If Aave can carry $200 million-plus in bad debt from a bridge exploit on a different protocol, the market has to recalibrate what ‘safe’ actually means in DeFi lending.”

The pooled lending model is only as strong as its weakest accepted collateral, and when that collateral breaks, the entire shared pool absorbs the damage. The exposure reaches every depositor in the broader market, extending well past the vault that held the position.

Protocol

Decision on rsETH

Risk posture

Outcome

Aave

Expanded rsETH to a 93% loan-to-value ratio in eMode

More aggressive onboarding and collateral treatment

Ended up exposed to the compromised asset and now carries bad debt

SparkLend

Deprecated rsETH as part of routine cleanup of underused positions

More conservative portfolio and listing hygiene

Avoided the exposure that later hit Aave

Pawlowski pointed out that the structural reality had been “muted by years of ‘battle-tested’ and ‘blue-chip’ marketing.”

Amador broadened the exposure map beyond the mechanics of KelpDAO. The attack surface in DeFi now covers governance, signers, privileged roles, integrations, bridges, oracles, custody arrangements, and every external system a protocol depends on.

The most dangerous operational assumption a team can hold is that audited smart contracts equal a safe protocol. Immunefi’s own research shows that DeFi losses declined by as much as 80% over the last several years, because the sector hardened its code and attackers adapted.

Amador added that they now study the entire risk chain for the weakest points, and those points are now off-chain, governance-adjacent, or buried in dependency stacks that no single audit covers.

For institutions, April forced a specific reset. Amador described the checklist now: how admin keys are managed, who can pause markets, what dependencies exist, what the incident response process looks like, and how quickly a threat can be contained.

Pawlowski made the same point from the capital side, saying institutions will continue to enter on-chain credit because the demand for tokenized markets, transparent settlement, and programmable financial infrastructure is real.

However, the institutional investors will move toward isolated markets, permissioned or curated vaults, stricter asset onboarding, better insurance, continuous monitoring, and formalized emergency controls.

DeFi exploiters extracted $635 million across 28 incidents in April, the sector’s worst monthly loss in over a year, while cumulative historical hacks reached $16.5 billion.

Aave Horizon, a permissioned market for tokenized securities and RWAs launched in August 2025, has grown to more than $440 million in deposits.

Morpho’s vault ecosystem added ARCHITECT, the first FINMA-licensed investment manager to curate vaults at scale, and Flowdesk launched an institutional AUSD vault in March 2026, using tokenized equities as collateral.

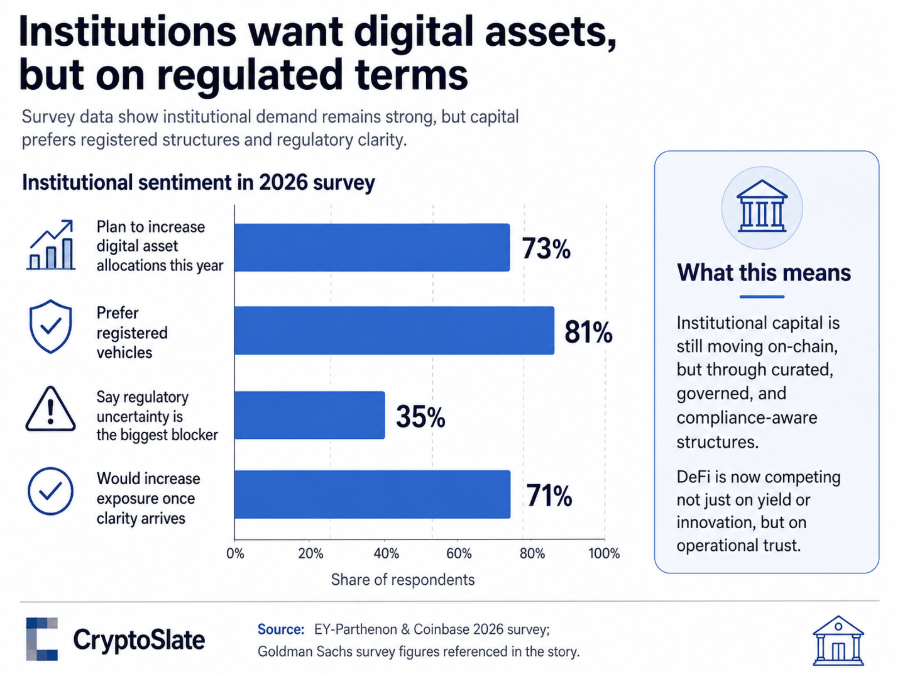

EY-Parthenon and Coinbase’s 2026 survey found 73% of institutional respondents plan to increase digital asset allocations this year, but 81% prefer registered vehicles. Capital is moving on-chain through curated, governed, and compliance-aware structures.

The regulated alternative is accelerating on the other side of that same preference.

The GENIUS Act created the first federal framework for US stablecoins, with mandatory 100% reserve backing, no rehypothecation, and custody standards that Nadareski said “read like something a compliance desk could approve.”

A Goldman Sachs survey found 35% of institutional investors named regulatory uncertainty their biggest blocker, and 71% said they would increase exposure once clarity arrived.

Nadareski said, “The floor is in place, the capital is waiting.” The CLARITY Act, which would define jurisdictional and custodian standards for digital assets, including tokenized securities, awaits consideration by the Senate Banking Committee as of May 14.

When that passes, Nadareski argued that “the last item on most institutional checklists gets checked off. The waiting ends.” DeFi is competing for institutional capital against a nearly complete regulatory framework.

How DeFi resurges

Pawlowski named the full list of DeFi recovery tools: governance combined with proper market isolation, automated and AI-assisted risk monitoring, selective timelocks on parameters that warrant them, circuit breakers, KYC when required by regulation, application-specific sequencing, and policy-aware block builders.

He added:

“What’s been missing is the willingness to use them, because every one [of the tools] involves a tradeoff against the maximalist version of decentralization the industry has marketed itself on.”

Abandoning that marketing position is the starting point, but it’s not easy.

Pawlowski noted that “the crypto industry has spent years pretending it can have everything”, such as full decentralization, censorship resistance, institutional-grade safety, and retail accessibility, without tradeoffs.

It was “that fantasy that produced the conditions for these exploits.” A regulated institutional credit facility on-chain is a different product from a permissionless retail lending market, and governing both under the same orthodoxy created the conditions that let aggressive rsETH listings clear governance while structural bridge-security parameters sat unflagged for years.

Pawlowski believes the structural fix requires ending “the conflicts that let aggressive listings get waved through low-turnout governance votes by service providers with commercial relationships on both sides of the trade.”

SparkLend’s independent pruning, versus Aave’s eMode expansion on the same day, is proof that different risk philosophies yield different outcomes.

DeFi needs to institutionalize that distinction, build governance structures around it, and make the tradeoffs explicit to every user and institution evaluating the protocol.

Amador’s operational prescription attacks the same problem from the execution layer.

DeFi must professionalize security in the same way it professionalized liquidity incentives via continuous audits, live bug bounty programs, formal verification where appropriate, independent security councils, stronger multisig thresholds, hardware-backed key management, real-time monitoring, public incident response playbooks, and mandatory risk reviews for every major integration.

Circuit breakers and isolation mechanisms should be built so that losses from a compromised asset, adapter, or dependency stay bounded within the affected market.

The benchmark for evaluating protocols should expand to cover security posture alongside yield and total value locked: who audited it, what the active bounty size is, how admin keys are managed, what dependencies exist, what the emergency procedure covers, and how quickly a threat can be contained.

Users and institutions should be able to compare protocols on those dimensions the way they compare APR.

Capability

Why it matters

What it looks like in practice

Market isolation

Prevents one compromised asset or dependency from contaminating a shared pool

Keeps risk assessment dynamic rather than one-time

Mandatory reviews for major integrations, recurring audits, formal verification where appropriate

Incident response readiness

Improves containment and recovery when something breaks

Public response playbooks, recovery guardians, predefined recovery procedures

Security transparency

Lets users and institutions compare protocols beyond yield

Clear disclosure of audits, bounty size, dependencies, admin controls, and response plans

A reform is already underway, as KelpDAO has begun migrating rsETH to Chainlink CCIP, LayerZero has banned 1-of-1 verifier configurations protocol-wide, and Aave Proposal 477 authorized liquidation of attacker positions, with recovered assets routed to a Recovery Guardian multisig.

Phase II of that proposal covers burning excess rsETH on Arbitrum, restoring bridge backing, reopening withdrawals, and compensating affected users.

Arbitrum’s Security Council separately froze 30,766 ETH tied to the attacker’s downstream funds.

That recovery required emergency councils, DAO votes, multisigs, and court proceedings, comprising a crisis-management stack drawn from the institutional finance playbook, deployed within a system that describes itself as permissionless.

DeFi reaches for those tools when losses get large enough, and protocols can embed them in advance or reconstruct them while a crisis unfolds.

DeFi’s case for composability

Nadareski identified the specific prize at stake for institutions choosing between DeFi and regulated alternatives.

Compliance officers want circuit breakers, time-locks, and custody standards that match their existing playbooks, and Wall Street has been building that wrapper for years.

Nadareski said:

“The banks that move fastest will be the ones that stop trying to build everything in-house. Spinning up on-chain settlement with legacy teams puts you at 2028 if everything goes right. The play that ships this year is pairing established distribution and customer relationships with teams who already have the rails built.”

Composability is DeFi’s strongest argument for keeping the rails it built. A single protocol that executes a trade, manages collateral, routes liquidity, and automatically settles a transaction within seconds represents a capability that traditional finance can only replicate by rebuilding from the ground up.

Composability works as an institutional argument only if failures stay local. Once a bridge verifier, a governance vote, or a compromised oracle can transmit losses across shared liquidity pools at scale, composability operates as contagion infrastructure.

Amador noted:

“Trust the code is not enough when protocols depend on bridges, multisigs, governance processes, or external assets. The new standard has to be: assume every layer can fail, and design systems so one failure does not cascade into the entire market.”

Pawlowski framed the necessary changes as “growing up,” describing a sector that must accept and publish explicit tradeoffs, build genuinely independent governance structures, and make security a product feature that users and institutions can evaluate and compare.

DeFi built the composable infrastructure that tokenized markets are now adopting. Stablecoin rails, lending primitives, and liquidity mechanisms that originated inside permissionless DeFi are being packaged into products that Wall Street is shipping under regulatory cover.

If DeFi builds the operational maturity to match its technical architecture, composability remains the one capability beyond the reach of regulated wrappers. If DeFi fails to build that maturity, Wall Street captures the stablecoin and tokenization layer and, with it, the argument that open composable finance lacked the operational discipline serious capital requires.

Aave entered April 2026 as DeFi’s largest lending protocol. By mid-month, it was managing the fallout from one of the most damaging exploits in its history — and the on-chain data is now revealing just how deeply the event disrupted the protocol’s core activity.

The incident began at Kelp DAO, where attackers exploited a $293 million vulnerability and used the stolen tokens as collateral on Aave V3. Aave’s smart contracts were never breached — the protocol functioned exactly as designed. However, it could not defend the integrity of the assets it accepted. Fraudulent collateral entered the system. Borrowers used it to take out real assets, and the resulting bad debt triggered a confidence crisis that drove billions in deposits toward the exit within days.

A CryptoQuant report tracking Aave V3 activity in the aftermath has now quantified the impact of that crisis on the protocol’s borrowing market. The data tells a two-chapter story. Borrowing rates across USDT, USDC, and WETH spiked sharply. A reflexive response to sudden liquidity tightening as participants scrambled to adjust positions. Then, almost as quickly, borrowing activity collapsed toward near-zero levels.

That second chapter is the more significant one. Rate spikes during a crisis are expected. The near-complete cessation of borrowing that followed is the signal that requires examination. Because it reflects not just liquidity stress, but a fundamental shift in participant behavior.

The Rate Spike Was the Alarm. The Silence That Followed Is the Story

The CryptoQuant report places the borrowing collapse in a framework that distinguishes shock response from structural breakdown. Rate spikes during liquidity crises are mechanical — when available capital tightens abruptly, the price of borrowing rises immediately as participants compete for shrinking supply. That is what happened in the immediate aftermath of the Kelp DAO exploit. It is expected, it is temporary, and it does not by itself indicate lasting damage.

What followed is less routine. Rather than recovering as rates normalized, borrow event activity across Aave V3 collapsed toward near-zero — a response that reflects participants choosing to step back entirely rather than re-engage once the initial stress passed. Capital that was previously active in Aave’s lending markets has moved into defensive positioning. The protocol’s mechanics are intact. The participants who used them have temporarily left.

The cross-market nature of the contraction makes the signal particularly difficult to dismiss. Stablecoin borrowing weakness reflects reduced appetite for leveraged directional exposure — traders unwilling to borrow against positions. WETH activity falling simultaneously points to the unwinding of more sophisticated strategies: collateral recycling, basis trades, and the layered DeFi positions that require sustained confidence in the underlying protocol to maintain. When both retreat at once, the signal is systemic rather than isolated.

The CryptoQuant assessment is precise about what recovery looks like from here. Borrow event activity returning alongside normalized rates would signal the end of capital preservation mode and the beginning of genuine redeployment. Until that combination appears, the data describes a protocol that has survived the shock structurally but has yet to regain the participant confidence that makes it functionally whole.

AAVE Tests Key Support After Prolonged Downtrend

AAVE is trading near $98 on the weekly chart, attempting to stabilize after a sustained decline from the $350–$380 highs set earlier in the cycle. The structure is clearly bearish on higher timeframes: a sequence of lower highs and lower lows has defined price action for months, with each rally failing beneath declining moving averages.

The recent drop into the $85–$95 zone marks a critical support test. This area aligns with prior consolidation from late 2023 and early 2024, making it a historically relevant demand region. The current bounce is technically constructive, but it remains corrective in nature until proven otherwise.

All major moving averages — 50-week, 100-week, and 200-week — are positioned above price and sloping downward. This creates a stacked resistance structure between roughly $130 and $200, where previous breakdowns occurred. Any recovery attempt will need to reclaim that range to shift the broader trend.

Volume behavior reinforces caution. The sharp selloff phases were accompanied by elevated volume, indicating strong distribution, while the recent rebound has developed on lighter participation.

For now, AAVE is attempting to build a base. Holding above $85 keeps the structure intact. Losing it would likely open the path toward deeper downside.

Featured image from ChatGPT, chart from TradingView.com

This week the crypto market got hit from every direction at once and held.

The Strait of Hormuz, through which roughly 20% of the world’s oil flows, flickered open and closed like a light switch over the weekend. Iran opened it Friday, Trump said the blockade stays, Iran closed it Saturday and ships came under fire. Every headline moved Bitcoin. It opened Monday down 2.5%, bounced back toward $75,000 by mid-morning as institutional buyers stepped in, and that has been the pattern all month: macro shock, dip, institutional buy. BlackRock’s IBIT alone pulled $284M in a single day on April 17. The floor is real. But BTC has failed six times to hold above $76K and the Iran ceasefire clock is still ticking. That weekly close above $76K is the signal I’m watching.

On the DeFi side, KelpDAO got exploited on Tuesday. Attackers found a flaw in the way it verified prices before processing large withdrawals and drained $293 million in 46 minutes. The ripple effect hit Aave, essentially a DeFi lending bank, which was left with $196 million in loans it may not fully recover. If you hold, lend, or earn yield on any cross-chain protocol, the full breakdown is worth reading.

Vercel confirmed a breach on April 19. It’s the platform that hosts the frontend of a huge slice of the Web3 ecosystem, the actual websites you interact with when you use a dApp. Compromised via a supply-chain attack through a third-party AI tool. If you connected a wallet to any Web3 dApp this past week, revoke any approvals you don’t recognize. Full CCS breakdown here.

For all the noise, the market didn’t break. Strategy bought 34,164 BTC for $2.55 billion this week. BitMine bought 101,627 ETH for $235 million. Institutions aren’t waiting for the all-clear signal. They’re buying the chaos.

XYO just went 2-5x faster and most people haven’t noticed yet.

Throughput jump. Dual DataLake SDK. Validator stability. All shipped at once.

Arie Trouw, Co-Founder, CEO, and CTO of XYO, breaks down exactly what changed, what was causing the bottleneck before, and why verifiable data provenance is quietly becoming one of the most important infrastructure layers as AI moves into the physical world.

BTC is still trading below its 100-day and 200-day moving averages and has failed six times to hold above $76K. Total spot ETF inflows now exceed $56 billion — that’s what keeps putting a floor under every dip.

Cautiously Bullish

The structure holds as long as $75K holds. A weekly close above $76K opens the path to $85K–$90K. A breakdown here puts $70K–$72K back in play. The macro overhang from Iran is the single biggest variable on the board right now.

What I’m watching: A confirmed daily close above $76,500 with above-average volume. Without it, every rally is a wick until proven otherwise.

ETH opened down 3.7% on the week and is in recovery mode. Bitcoin is leading and ETH is following, which is the healthy version of this setup. The Vercel breach and KelpDAO hack are headwinds for sentiment, not for the price structure itself.

Bullish — Patient

The next level to watch is $2,701, which is the major resistance before $3,519 comes back into view. ETH outperforming BTC on a percentage basis is the signal I want to see before getting more aggressive.

Vercel confirmed a breach via supply-chain attack through a third-party AI tool, exposing API keys and tokens across Web3 frontends. Solana DEX Orca rotated all credentials immediately. If you connected a wallet to any dApp this week, revoke approvals you don’t recognize. Full CCS breakdown

X’s cashtag trading pilot for stocks and crypto generated an estimated $1 billion in volume in its first week

$400 million in crypto shorts were liquidated in a single 4-hour window during the Hormuz chaos

Michael Saylor says it is “impossible to blockade Bitcoin”

$RAVE collapsed 98% in two days, erasing $6.7 billion in market cap following alleged insider manipulation

India is settling Iranian oil payments in Chinese yuan, a notable de-dollarization signal

Qastle Wallet Premium subscribers can claim a free Bitcoin 2026 Pro Pass worth $1,299. Bitcoin 2026 is April 27–29 at The Venetian, Las Vegas. Claim here

Final Word

The ceasefire between the US and Iran expires this week. That single variable has more power over Bitcoin’s price right now than any on-chain metric. If talks break down, expect another dip and another institutional buy. If a deal gets done, $76K becomes the story fast.

Watch the daily close. That’s where this week gets decided.

Ashton Addison

CEO, Crypto Coin Show

What’s moving your thinking more right now — the Iran ceasefire or the DeFi security story?

KelpDAO’s $293M Bridge Hack Left Aave Holding the Bag

How attackers forged a LayerZero message to drain KelpDAO’s rsETH bridge in 46 minutes, deposited unbacked tokens into Aave as collateral, borrowed $293M in real WETH — and left Aave with $196M in bad debt, a $13B TVL wipeout, and a governance crisis it is still fighting through today.

By Ashton Addison, Editor in Chief · Crypto Coin ShowApril 18–19, 2026Ethereum · Arbitrum · 20+ Chains10 min read

$293MTotal drained

46Minutes to drain

116,500rsETH stolen

$196MAave bad debt

$6.6BAave TVL drop

#1Largest hack of 2026

On the afternoon of Saturday, April 18, 2026, a single wallet — funded through Tornado Cash to obscure its origins — quietly positioned itself at the threshold of Kelp DAO’s cross-chain bridge. What followed in the next 46 minutes rewrote the record books for DeFi exploits, drained nearly a fifth of an entire liquid restaking token’s circulating supply, and left the largest lending protocol in decentralized finance grappling with close to $200 million in irrecoverable bad debt.

The attack on Kelp DAO is not simply the year’s biggest hack by dollar value. It is a masterclass in how interconnected DeFi infrastructure transforms a single vulnerability into a multi-protocol catastrophe — and a sobering reminder that the composability that makes DeFi powerful is also what makes it catastrophically fragile.

“The assumption underlying all of that was that the token would remain fully backed. When that assumption collapsed on Saturday afternoon, there was no circuit breaker, no committee vote, and no grace period.”

Understanding the Target: Kelp DAO and rsETH

To understand what happened, it helps to understand what Kelp DAO actually is. Kelp is a liquid restaking protocol operating under the KernelDAO umbrella. Users deposit established, already-staked Ether derivatives — tokens like stETH or cbETH — into Kelp’s adapter contracts. In return, they receive rsETH, a “receipt” token that earns staking and restaking yield through EigenLayer while remaining liquid and tradeable.

That liquidity is the key. Because rsETH represents real, yield-bearing ETH, it was accepted as collateral by nearly every major DeFi lending protocol, including Aave, SparkLend, Compound, and Euler. Billions of dollars in DeFi value rested on the implicit assumption that rsETH was, and would remain, fully backed by real assets.

To operate across Ethereum’s ever-expanding ecosystem of Layer 2 networks, Kelp relied on a LayerZero-powered Omnichain Fungible Token bridge — a cross-chain messaging system designed to confirm and relay valid transfer instructions between networks. This bridge held reserves backing rsETH across more than 20 separate blockchain networks. It was the protocol’s connective tissue. It was also its most exposed attack surface.

The Attack: A Forged Message, a Minted Fortune

Phase I — Spoofing the Bridge

Blockchain investigators, including the on-chain sleuth ZachXBT who first publicly flagged the outflow at approximately 14:52 New York time, quickly established the mechanics. The attacker did not steal private keys. They did not drain a smart contract through a reentrancy flaw. Instead, they exploited a critical vulnerability in rsETH’s bridge minting logic — specifically in the LayerZero Omnichain Fungible Token contract — by feeding the bridge a forged cross-chain instruction.

The message appeared to the bridge as a valid, legitimate transfer request arriving from another chain. The bridge’s validation layer — the system designed to confirm that a matching inbound transfer existed to anchor any mint — was fooled. It released 116,500 rsETH, worth approximately $292–$294 million at prevailing prices, to an address controlled by the attacker. No corresponding collateral existed. The tokens were, in effect, printed from nothing.

Stolen rsETH deposited into Aave V3 and V4 as collateral. Attacker begins borrowing Wrapped ETH (WETH) against the unbacked tokens, building debt positions across Aave, Compound V3, and Euler.

~18:05 UTC — Consolidation

Attacker consolidates approximately 74,000 ETH post-exploit, having extracted around 106,467 WETH (~$250M) by selling rsETH and using it as collateral to borrow.

18:21 UTC — Emergency Pause

Kelp DAO activates “pauseAll” function. rsETH deposits, withdrawals, and token movements frozen across mainnet and several L2 networks. The bulk of funds had already been extracted.

~18:30 UTC — Protocol Freezes Begin

Aave freezes rsETH markets on V3 and V4. SparkLend and Fluid follow. Lido Finance pauses earnETH deposits. Ethena temporarily pauses its LayerZero OFT bridges as a precaution.

20:10 UTC — Kelp Acknowledges

Kelp DAO posts its first public statement on X — nearly three hours after the drain — confirming “suspicious cross-chain activity” and coordination with LayerZero, Unichain, auditors, and security experts.

Phase II — Weaponizing DeFi’s Composability

The second phase of the attack was arguably more damaging than the first. The stolen rsETH did not simply sit idle in the attacker’s wallet. Having minted 116,500 tokens backed by nothing, the attacker turned immediately to DeFi’s lending markets — the very infrastructure that had accepted rsETH as a trusted collateral asset.

The attacker deposited the drained rsETH into Aave V3 as collateral and borrowed substantial volumes of Wrapped Ether against it. The same playbook was executed across Compound V3 and Euler. By the time Kelp’s emergency pause function fired — 46 minutes after the first successful drain — the attacker had already built more than $236 million in debt positions. On-chain data shows the attacker consolidated around 74,000 ETH post-exploit, extracting over $280 million in actual borrowed value.

Because the rsETH collateral backing those loans was no longer worth anything — the tokens were unbacked fabrications — the resulting debt positions are effectively unliquidatable. No liquidation bot can clear a position where the collateral has no real value. The bad debt simply sits on the protocol’s books, a permanent liability.

Technical Context — Why the Debt Is Unliquidatable

In DeFi lending, liquidations work by allowing third-party bots to repay an undercollateralized loan in exchange for seizing the collateral at a discount. This mechanism only functions if the collateral has genuine market value. Because the rsETH deposited as collateral by the attacker was minted without real backing, it now trades at a severe discount to its supposed peg — meaning liquidators would seize worthless tokens. Aave’s WETH reserve is now carrying approximately $196 million in debt it cannot recover through any standard mechanism.

Aave: Collateral Damage at the Largest Lender in DeFi

Aave did nothing wrong in a narrow technical sense. Its smart contracts were not compromised. Its own code did not fail. Aave’s founder Stani Kulechov was quick to clarify this on X, noting the exploit was entirely external and that Aave’s protocol had not been breached. But that distinction — sound code, catastrophic exposure — is precisely what makes the Kelp incident so instructive about the systemic risks embedded in modern DeFi.

Aave is the largest lending protocol in the ecosystem by total value locked, with over $26 billion deposited as of April 18. Ethereum alone holds $14.24 billion of the $17.82 billion in outstanding borrows across Aave’s 22-chain lending book. WETH — the exact asset the attacker borrowed — constitutes 39.49% of all loans on the protocol. The attack landed on the precise collateral-to-WETH pair that dominates Aave’s entire book.

The consequences were immediate and severe. Aave’s total value locked collapsed from $26.4 billion on April 18 to nearly $20 billion by Sunday morning — a $6.6 billion drop in under 24 hours, as depositors rushed to withdraw and the market priced in potential bad debt. The AAVE governance token fell approximately 16% over the same period.

Aave froze rsETH markets on both V3 and V4 within hours of the exploit. Initially, the protocol stated that its “Umbrella” reserve — a dedicated safety module designed to backstop bad debt scenarios — would cover any deficit. By Saturday evening, that language had softened considerably, with the team acknowledging they would “explore paths to offset the deficit.” The Umbrella reserve may not be large enough to cover the full $196 million shortfall, raising the prospect that staked AAVE token holders — who bear losses as a last resort — could face dilution.

Contagion Across the Ecosystem

The freeze cascade extended far beyond Aave. SparkLend halted its rsETH markets. Fluid froze rsETH collateral positions. Lido Finance paused further deposits into its earnETH product, which carries rsETH exposure, while carefully clarifying that its core stETH and wstETH products were entirely unaffected. Ethena, despite having no rsETH exposure, temporarily paused its own LayerZero OFT bridges as a precaution while the root cause was being identified — a bridge pause lasting roughly six hours.

The broader market impact was swift. Staked ETH derivatives stETH and wstETH fell approximately 4% as investors processed the news. rsETH itself broke sharply from its ETH peg as holders on more than 20 Layer 2 networks faced the prospect that the token’s reserve backing may have been permanently impaired. The question of whether rsETH holders on non-Ethereum networks can be made whole remains, as of publication, entirely unresolved.

“Liquid restaking tokens were whitelisted across every major lending protocol because they carried yield and represented a growing share of Ethereum’s locked value. The risk models priced them as if they would hold peg under normal conditions.”

The Broader Context: A DeFi Sector Under Siege

The KelpDAO exploit did not occur in isolation. It is the headline event in what security researchers are increasingly describing as a structural shift in how DeFi is being attacked. The Kelp incident cements 2026 as the worst year on record for DeFi security by cumulative losses. By mid-April, total losses across the sector had crossed $482 million across approximately 45 protocols — and this was before the KelpDAO drain was added to the tally.

The prior record holder for 2026’s largest exploit was the Drift Protocol attack on April 1, which cost the Solana-based perpetual futures exchange $285 million. In that case, attackers used social engineering to manipulate Security Council members into pre-signing transactions using Solana’s durable nonces feature — gaining administrative control and withdrawing real USDC and SOL within 12 minutes. Authorities later linked the attack to North Korea-affiliated actors.

Other notable incidents from the same 20-day period include: a domain hijacking attack on DEX aggregator CoW Swap ($1.2 million, April 14), a flash loan manipulation on Binance Smart Chain ($1.6 million), an oracle misconfiguration exploit targeting Silo Finance ($392,000, April 3), and a smart contract bug in bridge aggregator Dango ($410,000). Security firm Cyvers confirmed the Kelp attacker’s initial wallet was funded through Tornado Cash, the on-chain coin mixer, to cover gas fees and obscure origins.

What the incidents collectively illustrate is a profound evolution in attack vectors. Pure smart contract code exploits — the reentrancy bugs and integer overflow vulnerabilities of earlier DeFi eras — are no longer the dominant threat. Infrastructure-level attacks, including private key compromise, social engineering, compromised frontends, and cross-chain bridge manipulation, accounted for approximately 76% of losses in early 2026. AI-assisted phishing campaigns have reportedly scaled by an estimated 500% compared to the same period in 2025.

What This Means for Restaking and the Future of DeFi Collateral

The Kelp incident forces a reckoning with one of the most consequential decisions lending protocols made over the past two years: the wholesale acceptance of liquid restaking tokens as blue-chip collateral. rsETH, along with tokens from Ether.fi, Renzo, and Puffer, flooded into DeFi’s collateral frameworks because they represented real, yield-generating ETH — and because the restaking sector was growing at extraordinary speed, with EigenLayer attracting billions in deposits.

The implicit assumption in every risk model that whitelisted these tokens was that the peg would hold. That the backing would remain intact. That there would be no bridge failure, no minting exploit, no sudden decoupling between the receipt token and the real assets it was supposed to represent. The KelpDAO incident has now demonstrated that this assumption was not merely optimistic — it was catastrophically fragile, and it was exposed not by some exotic new vulnerability but by a forged message on a cross-chain bridge.

Cyvers CEO Deddy Lavid summarized the structural exposure bluntly: the incident shows the risks of composability in DeFi, where protocols are deeply connected. When a token’s backing collapses on one part of the infrastructure, every protocol that accepted it as collateral absorbs the impact — whether or not their own code was sound.

The immediate aftermath will likely include substantially tighter risk parameters for liquid restaking token collateral across major lending platforms, accelerated bridge security audits across the LRT ecosystem, and a broader industry debate about whether restaked Ether of any variety should be classified as equivalent to ETH itself for collateral purposes. KelpDAO has indicated it is working with LayerZero, its auditors, and external security researchers on a root cause analysis. As of publication, the exact mechanism by which the bridge’s validation logic was bypassed has not been publicly disclosed.

What Happens Next

For rsETH holders, the central question is redemption. With 116,500 tokens — 18% of total circulating supply — now unbacked, and with reserves previously held by the bridge now gone, the protocol faces a fundamental solvency challenge on its Layer 2 deployments. KelpDAO has deployed a temporary v2 pool for affected holders, though the economics of any recovery plan remain unclear.

For Aave, the path forward hinges on whether the Umbrella reserve can absorb the shortfall, whether the DAO votes to use treasury resources to offset remaining bad debt, or whether staked AAVE holders face dilution. The $6.6 billion TVL collapse may prove transitory if the protocol’s response is decisive; a prolonged period of uncertainty would be more damaging.

For the DeFi ecosystem broadly, the KelpDAO hack will be studied for years — not as an anomaly, but as a case study in how the sector’s greatest strength, the open, permissionless composability that allows protocols to build on each other, is also its deepest structural vulnerability. Until cross-chain bridges can be made reliably trustless, and until collateral risk frameworks account for the possibility that a token’s backing can evaporate in under an hour, no risk model in DeFi is complete.

— ◆ —

Update: April 20, 2026

Lazarus Group Attribution — North Korea Linked to the Attack

In the most significant development since the initial drain, LayerZero published a detailed post-mortem on April 20 shifting both the technical blame and the threat attribution squarely onto the record. LayerZero concluded the exploit stemmed entirely from Kelp’s own security choices — specifically its decision to run a 1-of-1 verifier configuration on its LayerZero bridge, meaning LayerZero Labs was the sole entity responsible for verifying cross-chain messages to and from the rsETH bridge. LayerZero’s public integration documentation and direct communications to Kelp had explicitly recommended a multi-verifier setup with redundancy, requiring consensus across several independent verifiers to confirm any message. Kelp did not implement this recommendation.

The mechanics of the attack, as LayerZero’s traffic logs now reveal, involved compromising two RPC nodes and deploying a distributed denial-of-service attack between 10:20 a.m. and 11:40 a.m. Pacific Time on Saturday. The DDoS forced a failover in the bridge’s infrastructure. Once that failover triggered, the compromised nodes told the sole verifier that a valid cross-chain message had arrived — and Kelp’s bridge released the 116,500 rsETH. The malicious node software then self-destructed, wiping binaries and local logs to complicate forensic analysis. LayerZero has stated it will no longer sign messages for any project still running a 1-of-1 verifier configuration.

Attribution — North Korea’s Lazarus Group

LayerZero’s post-mortem preliminarily attributes the attack to North Korea’s Lazarus Group — the same state-sponsored unit linked to the Drift Protocol exploit on April 1. If confirmed, Lazarus will have drained more than $575 million from DeFi in 18 days through two structurally different attack vectors: social engineering governance signers at Drift, and poisoning infrastructure RPCs at Kelp. The group appears to be adapting its playbook faster than DeFi protocols are hardening their defenses.

Aave’s Liquidity Crisis Deepens

What began as a bad debt problem has compounded into a full liquidity crisis. In the 48 hours following the exploit, Aave suffered $8.45 billion in total deposit outflows, driving the broader DeFi ecosystem’s total value locked down by $13.21 billion. The panic was not limited to rsETH holders — whales with unrelated positions fled the protocol en masse, pushing Aave’s ETH and WETH pools to 100% utilization.

When a lending pool reaches 100% utilization, withdrawals stop working. Every dollar deposited is already borrowed, leaving no idle liquidity for suppliers to redeem against. Depositors with USDT, USDC, and WETH positions found themselves trapped — unable to exit even though their assets had no direct rsETH exposure whatsoever. In a desperate secondary market response, some stranded users borrowed against their own locked stablecoin deposits at steep losses, accepting roughly 75 cents on the dollar just to extract any liquidity at all. Analysts at Spark estimated this dynamic drove a $300 million borrowing spike in USDT-collateralized positions in a single day.

A post on the Aave governance forum by a community member captured the mounting urgency around one underappreciated dimension: the bad debt is denominated in ETH, not dollars. The attacker borrowed approximately 126,000 ETH using the stolen rsETH as collateral. That debt is fixed in ETH terms. Aave’s Umbrella backstop and treasury reserves, however, are denominated in stablecoins. Every hour ETH price appreciates, the real cost of the shortfall grows — making speed of governance response a direct financial variable.

The Umbrella Gap and Governance Response

Aave’s Umbrella safety module — an automated backstop funded by protocol revenue and staked deposits — was designed for exactly this scenario. The mechanism allows staked aTokens to be slashed and burned to offset confirmed bad debt without requiring a governance vote, providing automated coverage. The problem is scale: as of mid-April 2026, the Umbrella reserve held an estimated $80–$100 million in assets, against a bad debt exposure of $196 million. The shortfall of roughly $96–$116 million cannot be covered automatically and will require explicit governance decisions.

The recovery waterfall, as described by The Defiant, runs in the following order: aWETH Umbrella stakers absorb the first slice via automatic slashing; WETH suppliers take a pro-rata haircut on remaining deposits; stkAAVE holders face potential governance-activated slashing for the next tranche; and finally the DAO treasury could fund a broader repayment proposal. None of these outcomes are comfortable. A governance proposal to slash a percentage of staked AAVE is being actively discussed, and stkAAVE holders are already pricing that risk.

On the governance front, the Aave Chan Initiative moved swiftly, announcing it was ending its Frontier staking program immediately in response to the wETH shortfall risk. Aave V4’s Security Council separately disabled supply and borrow on both the Core Hub and the Kelp E-Spoke, while a Risk Stewards proposal to reduce the WETH Slope1 — aimed at pulling new supply back into the pools — went live. A damaging governance detail also emerged: a proposal in January 2026 had raised the rsETH loan-to-value ratio to 93%, apparently without adequate bridge risk assessment, significantly amplifying the scale of the resulting bad debt.

Aave founder Stani Kulechov has maintained publicly that the protocol operated as designed and that its own contracts were not compromised. That distinction is technically accurate. But as one market observer noted: the risk models priced rsETH as if it would hold peg under normal conditions. None of them priced the scenario where the collateral goes to zero because a bridge on a chain Aave does not control gets poisoned on a Saturday afternoon.

— ◆ —

This article was originally compiled from on-chain data, blockchain investigator reports, and protocol statements published April 18–19, 2026, and updated on April 20, 2026 with new developments including LayerZero’s post-mortem, Lazarus Group attribution, and Aave’s ongoing liquidity and governance response. The situation remains active. Figures cited reflect best available reporting at time of each update.

Trader Loses $50M in AAVE Slippage Mishap | Crypto Coin Show

DeFi · Breaking

Trader Swaps $50M USDT for 324 AAVE in Catastrophic Slippage Event

A single on-chain transaction on March 12 became one of DeFi’s most expensive lessons — draining $50 million down to a handful of tokens while MEV bots and block builders walked away with tens of millions.

Crypto Coin ShowMarch 13, 20255 min read

$50MUSDT Swapped

324AAVE Received

>99%Price Slippage

On March 12, a single DeFi trade turned into one of the most dramatic value-destruction events the space has ever seen. A trader attempted to purchase AAVE tokens by swapping 50.4 million USDT through the official Aave interface, routed via CoW Protocol. The swap hit a SushiSwap liquidity pool that was nowhere near deep enough to absorb a trade of that scale — resulting in over 99% slippage and a final receipt of just 324 AAVE tokens.

At the time of the transaction, 324 AAVE was worth roughly $36,000 — a loss of nearly the entire $50 million principal in a single block.

What Went Wrong

The mechanics of the disaster aren’t complicated, but the scale is almost incomprehensible. When a trade of this size is routed through a liquidity pool, it consumes available liquidity at each price level — pushing the price exponentially higher with every dollar swapped. The SushiSwap pool hit by this transaction simply didn’t have the depth to handle a $50 million order without catastrophic price impact.

Both the Aave interface and CoW Protocol’s routing system displayed clear warnings before the transaction was confirmed. According to Aave founder Stani Kulechov, the interface required the user to acknowledge the extraordinary slippage via an explicit confirmation checkbox — a step they completed on a mobile device before proceeding.

“The transaction could not be moved forward without the user explicitly accepting the risk through the confirmation checkbox.”

— Stani Kulechov (@StaniKulechov), Aave Founder

Kulechov confirmed that the CoW Swap routers performed as intended and followed standard industry practices. The outcome, while catastrophic, was the result of the user proceeding with full on-screen disclosure of the risk.

Where Did the $50 Million Go?

The value didn’t simply disappear — it was redistributed across the DeFi ecosystem’s most aggressive participants almost instantly.

Where $50M Went

💸

User’s original USDT sent

$50.4M

🤖

MEV bots — arbitrage profit

~$10M

⛏️

Block builder tips captured

~$33.6M

🔵

Aave fees (to be refunded)

$600K

📦

AAVE tokens actually received

~$36K

MEV (Maximal Extractable Value) bots, which constantly monitor the mempool for profitable opportunities, detected the enormous trade and executed arbitrage strategies around it — capturing an estimated $10 million in profits. Block builders, who determine transaction ordering within each block, extracted an additional $33.6 million in tips from the chaotic price action the trade created.

Aave’s Response

Kulechov was candid in his public statement, expressing sympathy for the affected user while defending the protocol’s behavior. He confirmed that Aave will return $600,000 in protocol fees collected from the transaction as a goodwill gesture, and that the team is actively attempting to make contact with the trader.

⚠️ Key Takeaway from Stani Kulechov

While DeFi should remain open and permissionless — allowing users to transact freely — this event underscores the need for additional guardrails. Aave’s team will investigate improved safeguards to better protect users in extreme scenarios, particularly around very large single-order trades.

A Watershed Moment for DeFi UX

Events like this — while rare in raw frequency — are nearly inevitable in an open, permissionless system. DeFi protocols cannot prevent users from confirming transactions they have been warned against. But as the scale of on-chain capital grows, the gap between “technically compliant” and “genuinely safe” becomes harder to ignore.

The incident has reignited conversation across the industry about whether hard limits, mandatory delays, or multi-step confirmation flows should be standard for trades above certain thresholds. A $50 million single-transaction swap hitting a thin pool is not a normal use case — and current infrastructure, while technically functional, clearly wasn’t built with that scale in mind.

For the individual behind the trade, the outcome is devastating. For the broader DeFi ecosystem, it is an expensive but clarifying moment: open rails and full user sovereignty come with real consequences when warnings go unheeded at scale.

Seven Major Ethereum Protocols Launch Advocacy Alliance to Shape DeFi Policy – Crypto Coin Show

Aave, Aragon, Curve, Lido, Spark, The Graph, and Uniswap Unite to Give Protocol Builders Direct Voice in Global Regulation

Switzerland – November 5, 2025

Seven of Ethereum’s most established protocols — Aave Labs, Aragon, Curve, Lido Labs Foundation, Spark Foundation, The Graph Foundation, and the Uniswap Foundation — today announced the formation of the Ethereum Protocol Advocacy Alliance (EPAA), coordinating global advocacy efforts to defend core infrastructure securing over $100 billion in onchain assets without intermediaries.

Growing Demand Meets Policy Disconnect

This effort comes as public interest in digital assets continues to grow. According to the Crypto Survey 2025 by Strategy & PwC network, retail investors are increasingly turning to crypto, with typical portfolio allocations now ranging from 5% to 20%. In the United States, recent polling from the DeFi Education Fund and Ipsos finds that 56% of Americans want full personal control over their money, and more than half agree that people should be able to send it digitally without intermediaries. Notably, 42% say they would likely try decentralized finance if clear legislation were passed.

Ethereum protocols have spent the past decade building global, resilient, and verifiable infrastructure that allows users to self-custody and transact without intermediaries. As this infrastructure saw growing global demand and adoption, centralized actors invested heavily in lobbying and gained outsized influence in policymaking. Now, regulators are confronting increasingly complex questions about onchain systems, yet the principles and technologies underpinning the infrastructure are often misunderstood or dismissed.

This disconnect makes clear why the teams building protocols need a stronger voice to ensure policy reflects how these systems actually work and serves the people who access them globally.

Builders Take a Seat at the Policy Table

The formation of the EPAA marks a critical step toward ensuring that public policy is grounded in the technical realities of how onchain protocols operate and is aligned with the values of security, neutrality, and transparency. Leaders from the founding protocol teams emphasized the importance of giving builders a direct voice in policy discussions.

“We’ve seen firsthand the technical and practical complexity involved in building onchain systems. Bringing together the most credible protocol teams will help ensure regulatory outcomes are workable for the builders moving this space forward.”

— Anthony Leutenegger, CEO of Aragon

“Decentralization is the foundation of Ethereum’s credibility and resilience, and through the EPAA, we’re ensuring that policy recognizes and protects this principle.”

— Sam Kim, Chief Legal Officer of Lido Labs Foundation

“The Uniswap ecosystem has faced undue regulatory scrutiny in the past—that’s why we know how critical it is for actual builders to have a seat at the table when policy for decentralized financial systems is being shaped.”

— Brian Nistler, General Counsel of the Uniswap Foundation

Four Core Priorities

Through shared policy positions, technical input, and educational resources, the Alliance will advance four core priorities:

Protecting the neutrality of the protocol layer by ensuring regulation does not interfere with the code itself or how it is developed

Advancing onchain transparency as a real-time verifiable source of compliance

Preserving flexibility for protocol innovation by avoiding overbroad requirements or rigid standards

Upholding global, permissionless access to onchain infrastructure

Coalition-Building for Effective Advocacy

The Alliance will collaborate closely with aligned organizations such as the DeFi Education Fund, the Decentralization Research Center, and the European Crypto Initiative to support existing advocacy efforts with pragmatic and technical expertise. By involving protocol teams directly in policy discussions, the initiative aims to ground regulation in technical reality and strengthen the foundations of a decentralized ecosystem.

“At the Decentralization Research Center, we see the Ethereum Protocol Advocacy Alliance as a vital step toward ensuring that those who build decentralized systems also help shape the rules that govern them.”

— Connor Spelliscy, Executive Director of the Decentralization Research Center

The joint effort will help ensure regulation is effective, technically grounded, and supportive of the principles that keep Ethereum protocols secure, neutral, and transparent.

About

Ethereum Protocol Advocacy Alliance

The Ethereum Protocol Advocacy Alliance (EPAA) is a group of Ethereum protocol builders coordinating policy efforts and supporting the broader advocacy ecosystem. Representing protocols securing over $100B in onchain assets, EPAA brings the perspective of teams actively building and operating onchain infrastructure.

Aragon

Aragon provides the infrastructure for protocols to manage capital allocation, governance, and ownership onchain. Its full-stack framework helps secure over $40 billion in assets across leading protocols including Lido, Curve, Polygon, Taiko, Morpho, and Katana.

Lido Labs Foundation

Lido is an open-source liquid staking middleware that enables participation in Ethereum network validation without running infrastructure. With a mission to democratize staking, Lido middleware connects users with node operators to make staking more accessible and secure.

Uniswap Foundation

The Uniswap Foundation is a nonprofit dedicated to creating a more open and fair financial system by supporting innovation across the Uniswap community.

Frequently Asked Questions

Q: Why are you launching this alliance now?

To ensure regulation reflects how onchain protocols work in practice, at a time when protocol infrastructure is underrepresented, misunderstood, and often overlooked.

Q: Is this a replacement for trade associations like the Blockchain Association or Coin Center?

No. It complements existing efforts by contributing the builder perspective.

Q: What makes this different from other advocacy groups in crypto?

It’s led by protocol teams actively building and maintaining onchain systems.

Q: Who’s leading the Alliance?

The Alliance was initiated by Aragon, but there is no formal leadership. It’s a loose coalition coordinated by members.

Q: Is there a formal structure or governance model?

No. Participation is flexible and designed to support existing efforts and workstreams.

Q: Is this connected to the Ethereum Foundation?

The Ethereum Foundation is supportive of the initiative, but not a formal member.

Q: How were the founding members chosen?

They were invited based on longstanding, credible track records building Ethereum protocols.

Q: Will other protocols be able to join?

Yes. The Alliance is designed to grow over time, though there are no immediate plans to expand membership.

Q: Are the participating teams committing funding or resources?

Members may contribute to partner advocacy efforts, but there is no shared budget or central staff.

Q: Will the Alliance have a budget or staff in the future?

There are no current plans to do so. The structure is intentionally lean.

Q: Will members lobby directly?

Some may, but the focus is on coordination and shared policy input.

Q: What policies or jurisdictions are you engaging with first?

The focus is global, with initial attention on U.S. and EU frameworks.

Q: Will you take positions on legislation like MiCA or the CLARITY Act?

We will work with our advocacy partners where legislation directly affects protocols.

Q: How does this complement the work of DEF, DRC, or EUCI?

By contributing technical input and reinforcing their advocacy efforts.

Q: Are you collaborating with legal researchers or think tanks?

Yes. Through our partnerships with aligned advocacy organizations.

Crypto Coin Show is a leading Web3 media platform providing in-depth coverage of blockchain innovation, cryptocurrency markets, and decentralized technology developments. With 150,000+ YouTube subscribers and syndication on Reuters Insider/Refinitiv TV, Crypto Coin Show delivers expert analysis and interviews with industry leaders.