Pump Fun is unlocking $127M insider tokens worth double PUMP’s recent daily volume

Pump.fun built one of crypto’s fastest meme-token liquidity machines. Now, on July 12, its own token faces the kind of liquidity test the platform usually creates for others.

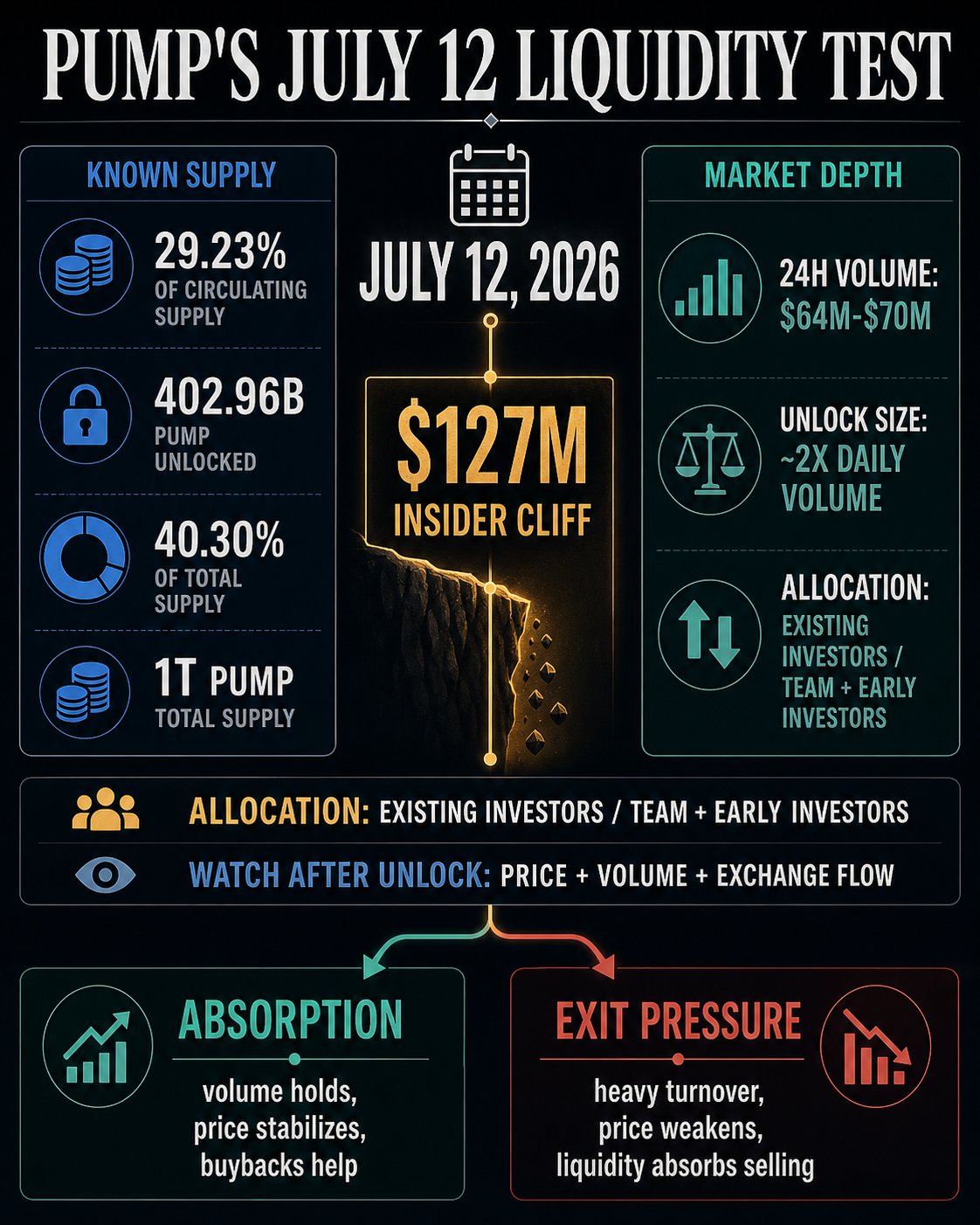

The platform’s PUMP token is set to unlock on July 12, with Tokenomist valuing it at $127 million, equal to 29.23% of the circulating supply.

The scheduled release is tied to insider allocations: Tokenomist’s weekly unlock digest describes the tranche as flowing to team and early investors, while its PUMP vesting page identifies the next release as Existing Investors.

That matters because PUMP is facing a large scheduled release against an order book that recently showed far less daily turnover than the unlock size.

CryptoSlate market pages showed PUMP trading near $0.00155 on July 8, with 24-hour volume between roughly $64 million and $70 million across the PUMP asset page and the broader coin rankings.

The scheduled cliff is therefore close to twice recent visible daily volume before any adjustment for how much of the unlocked allocation is actually sold.

The full $127 million may stay off exchanges if recipients hold. Unlock size only sets the maximum new supply available; sell-through decides the pressure.

But the token is entering a more direct liquidity test than most meme-coin narratives produce: if recipients hold, demand may absorb the date. If they sell into weak depth, the unlock can turn from a calendar entry into visible exit pressure.

Why the PUMP unlock comes in one block

Tokenomist’s vesting page says roughly 402.96 billion PUMP, or 40.30% of the token’s 1 trillion supply, has already been unlocked. The remaining supply is still governed by the project’s vesting schedule, which extends into 2029.

The same page says Pump.fun uses cliff vesting across most allocations, meaning tokens are released in large, scheduled blocks rather than being smoothed into the market over time.

That is why the July 12 event is more than a tokenomics footnote. Cliff structures concentrate risk into dates traders can see in advance.

Traders can price them in, hedge them, ignore them, or use them as liquidity windows. The supply still arrives in a visible block.

The upcoming release also lands in a token whose float is still maturing. Tokenomist lists the Initial Coin Offering at 33% of allocation, Community & Ecosystem Initiatives at 24%, Team at 20%, Existing Investors at 13%, Livestreaming at 3%, Liquidity & Exchanges at 2.6%, Ecosystem Fund at 2.4%, and Foundation at 2%. That mix puts a meaningful share of future supply in categories whose behavior can shape market confidence.

The strongest bearish case is simple. A large block of insider-controlled PUMP becomes available while the token’s daily trading volume is lower than the scheduled release amount.

If even a meaningful portion of that allocation seeks liquidity, buyers have to absorb it without demanding a larger discount. That is the definition of an exit-liquidity test.

The strongest counterargument is also straightforward. Recipients can hold unlocked tokens, and PUMP is attached to a platform with real activity, fees, and past buyback demand.

The trade turns on two observable outcomes: supply meets enough demand to clear without lasting damage, or the market reprices PUMP because the available bid is thinner than the insider supply.

For traders, timing is the point. Cliff vesting compresses a supply decision that could have unfolded over months into a single window, so price action around the date becomes a live signal of confidence, depth, and whether holders want cash or exposure.

Pump Fun retail demand was already tested once

The tension is more acute because Pump.fun’s token already had one spectacular demand event. CryptoSlate reported in July 2025 that the memecoin launchpad sold 150 billion PUMP tokens to retail investors, raising $600 million in 12 minutes and bringing total token-sale proceeds to $1.32 billion.

That was primary-market demand under launch conditions. The July 12 cliff tests something different: whether secondary-market liquidity can absorb supply after the trade has aged, the token has fallen far below its peak, and insiders have a new path to liquidity.

The platform context makes the reversal harder to miss. Pump.fun built its reputation by making meme-token creation and trading fast.

CryptoSlate’s launchpad review describes it as a Solana-native, bonding-curve launchpad where ordinary users can usually buy and sell quickly, and where the practical constraint is liquidity rather than formal vesting.

In other words, Pump.fun turned fast retail flow into a product.

Now PUMP has to demonstrate that the same market reflex exists for its own token when the seller profile changes. Retail buyers once funded the token sale at extraordinary speed.

The next question is whether secondary traders are willing to provide sufficient depth when the scheduled supply comes from the team and investor categories rather than from new public demand.

The question is market structure rather than a moral judgment about meme coins. PUMP can remain a tradable, revenue-linked token and still face pressure from cliff vesting.

It can also suffer short-term volatility without proving the business is broken. The important point is that the July 12 date turns an abstract dilution risk into a measurable trade.

That is where Pump.fun’s own design history tightens the story. The launchpad trained users to expect immediate market access and fast exits; PUMP’s unlock asks whether the platform’s token has the same depth when the flow moves in the other direction.

The platform created liquid attention for thousands of tokens, but insider supply tests whether attention is durable enough to support its own market.

PUMP buybacks make the case for absorption

The strongest case for absorption rests on Pump.fun’s revenue and buyback history. Tokenomist’s digest notes that Pump.fun has been a consistent revenue generator and has run token buybacks in the past, which can absorb some incremental supply if the program is large enough.

CryptoSlate previously examined that question in the broader token-buyback market, noting that Pump.fun had spent $233 million to buy 62.2 billion PUMP as of Jan. 6.

The same buyback analysis warned that buyback programs only change the supply picture when fee revenue scales faster than scheduled unlocks.

That is the relevant filter for the July 12 cliff. A buyback headline is insufficient on its own.

What matters is coverage: how much demand the program creates relative to newly available supply, and whether that demand is visible when insiders are allowed to sell.

If PUMP volume rises into the unlock, price holds, and buyback demand is evident, the market can interpret the event as manageable dilution.

The result would leave future vesting risk in place, but it would show that the token has a deeper bid than the headline unlock suggests.

If volume rises while price weakens, the signal changes. Heavy turnover can mean absorption, but it can also mean distribution.

The difference is whether buyers are taking supply without forcing a sustained discount. That is why post-unlock price behavior matters more than the unlock calendar itself.

The broader backdrop adds pressure. Tokenomist’s weekly digest described June as defensive, with Bitcoin dropping below $60,000 late in the month and spot Bitcoin ETF flows acting as a headwind.

It also said capital had become selective, favoring tokens with clearer revenue and value-accrual mechanics rather than the market as a whole. That is a mixed setup for PUMP: the project has revenue, but the token has a large insider cliff.

The verdict comes after July 12

Before the unlock, the cleanest conclusion is conditional. Pump.fun’s July 12 cliff is large enough, concentrated enough, and close enough to recent visible daily volume to qualify as PUMP’s first real exit-liquidity test.

Sell-through remains the missing variable.

The next signal will come from how PUMP trades after the tokens become available.

A constructive outcome would show elevated volume without a lasting price break, limited evidence of exchange-bound supply, and enough demand or buyback activity to keep the market orderly.

A weaker outcome would show heavy volume paired with price deterioration, suggesting that liquidity is being used to exit rather than to accumulate.

That makes July 12 a deadline with a measurable aftermath. Pump.fun built one of crypto’s fastest retail attention machines.

PUMP now has to show whether that attention is deep enough to meet insider supply when the cliff arrives.

The post Pump Fun is unlocking $127M insider tokens worth double PUMP’s recent daily volume appeared first on CryptoSlate.